Table of Contents - 2003 Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Republic of the Philippines 10.625% Global Bonds Due 2025

PROSPECTUS SUPPLEMENT TO PROSPECTUS DATED SEPTEMBER 24, 2003 R E S PU NE BLIC IPPI OF THE PHIL US$300,000,000 Republic of the Philippines 10.625% Global Bonds due 2025 Luxembourg Stock Exchange Listing Particulars The Republic will pay interest on the global bonds each March 16 and September 16. The Ñrst interest payment on the global bonds will be made on March 16, 2004. The global bonds will constitute a further issuance of, are fungible with and are consolidated and form a single series with, the 10.625% Global Bonds due 2025 issued by the Republic on March 16, 2000. The total principal amount of the previously issued global bonds and the global bonds now being issued is $1,300,000,000. The Republic may not redeem the global bonds prior to their maturity. The oÅering of the global bonds is conditional on the receipt of certain approvals of the Monetary Board of the Bangko Sentral ng Pilipinas, the central bank of the Republic. The global bonds are being oÅered globally for sale in the jurisdictions where it is lawful to make such oÅers and sales. We have applied to list the global bonds on the Luxembourg Stock Exchange. We cannot guarantee that the application to the Luxembourg Stock Exchange will be approved, and settlement of the global bonds is not conditioned on obtaining the listing. Per Bond Total Price to investors(1) ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 112.25% $336,750,000 Underwriting discounts and commissions ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 0.10% $ 300,000 Proceeds, before expenses, to the Republic ÏÏÏÏÏÏÏÏÏÏÏÏÏ 112.15% $336,450,000 (1) Plus accrued interest from and including September 16, 2003. -

Eduardo K"R*R, Insurance F, Commissioner 1U It T, ;L

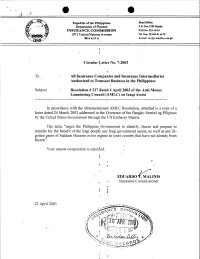

o o Republic of the Philippines Head OIEcc: Department of Finance P. O. Box 3589 Manila INSURANCE COMMISSION FAXNo.522.l+31 1071 United Nations Avenue Tel. Nos. 523-84-61 to 70 Manila. E-mail: [email protected] t t Circular l-etter No. 7-2003 il To" All Insurance Companies and Insurance Intermediaries Authorized to Transact Business in the Philippines i Subject Resolution # 227 dated 4 April 2003 of the Anti-Money Laundering Council (AMLC) on Iraqi Assets In accordance with the aforementioned AMLC Resolution, attached is a copy of a letter dated 24March 2003 addressed torthe Governor of the Bangko Sentral ng Pilipinas by the United States Government through the US Embassy Manila. { The letter "urges the Philippine. Government to identifu,, freeze and prepare to transfer for the benefJ of the Iraqi people any Iraqi government assets, as well as any ill- gotten gains of Saddam Hussein or his regime in (our) country that have not already been frozeft". Your utmost cooperation is enjoified. t t, it EDUARDo K"r*r, Insurance f, Commissioner 1u it t, ;l 22 Aprll2003 t' l' o 'mbassy ' r:t::i i;;.:i{FI 'r:. i\li^ '', 'i " , M_a,ilu, pltilippiftEggili1r':ll,r:,]. Bdrror:o serrrnal ti* ert.rFtllirs-----.,.--. ) OTFICE OFltrg (i$+rl,ritl(f,rM qtph,24, Z0O3 '03 /f* rry 3 -;; '03 ,f,r$:26 f')'r [1,1i1 25 Mr. Rafael Buenaventura Governor Banko Sentral ng pilipinas Dear Governor Buenaventura: iif, I 31:L,I*:!:gilSins of -hosririries in rraq, ir," unit.ar i i3" 1 linni : ;funds;i,inl,:a. -

CNMI Are Being Investigated by Government Operatives for Allegedly Selling Smuggled Merchandise, Gov

.L...,.......:VNNERSITY . OF HAWAII LIBRARY- arianas %rietYr;~ Micronesia's Leading Newspaper Since 1972 · · ~ Vol. 26· No .. 48 : . - . .. 0 ·, • : • • ••• •• F,, ~d. ' '·M: '. z 1 "' 1 9 ft 9 . ' . .. .. .·: : . S_aipan, MP 969~p.'. .· .·.. ),::;-1·;¢:-· . ©1999Ma~ianas\iariety .-·· ;. _·.·.;. · ..... ,.: :- .·. , • .-y .•.., , ,aY. .. ~ .. 7 ..... ·.· .. : _Serving_C_NMlf~r~6.Y~ar~:.:.~> ... '.,,;.:- .. ' ," < • \ • ,0 < • • • • • ' • • • ~ ~ • 0 ' < • < • .. r • ' • ~ Retail stores under watch According to Capitol Hill resident: for selling smuggled items By Aldwin R. Fajardo Variety News Staff 'Gov't e1D.ployees AT LEAST 87 retail stores in the CNMI are being investigated by government operatives for allegedly selling smuggled merchandise, Gov. Pedro P. Tenorio disclosed yesterday. Tenorio warned that businesses selling smuggled items face clo in burglary ring' sure while store owners would be slapped with criminal and civil charges. By Zaldy Dandan out that some government employ fied during yesterday's oversight "If businesses violate local and federal laws, they are subject not Variety News Staff ees are believed to be involved in a hearing to complain about the un only to prosecution but also closure." A CAPITOL Hill resident yester burglary ring. solved burglary cases on their During the governor's meeting with members of the Saipan Cham day said certain government em Public Safety Commissioner neighborhood. ber of Commerce, concerns about the proliferation of smuggled ployees are involved in a syndicate Charles W. Ingram Jr. neither con The public hearing, the second items on Saipan were raised. that is responsible for the spate of firmed nor denied the allegation, but in a series, is in response to the Tenorio said the Chamber is wary about unfair trade competition burglaries in her neighborhood. -

Global Finance Announces the Winners' Circle a Ranking of the Top

Global Finance announces The Winners' Circle The reach of Global Finance A ranking of the Top Winners of our Annual Awards Global Finance, founded in over the magazine's 25-year history 1987, has a circulation of 50,050 and readers in 163 countries. Its circulation is audited by BPA. Global NEW YORK, June 4, 2012 – Global Finance magazine is proud to announce The Winners' Circle – the Top Winners from 25 years of the magazine's annual awards Finance’s audience includes program. chairmen, presidents, CEOs, CFOs, treasurers and other “The world has changed dramatically since Global Finance first appeared in 1987. Global senior financial officers respon- financial markets have undergone a seismic shift, and the firms and individuals that made sible for making investment it into our Winners' Circle are those that have shown their true mettle and transformed and strategic decisions at themselves to meet the demands of a changing environment," says Global Finance’s publisher, Joseph D. Giarraputo. “We recognize these firms and individuals for their multinational companies and outstanding accomplishments over the past 25 years.” Global Finance’s annual awards financial institutions. Global program is a recognized and trusted standard for the entire financial world. Finance also targets the 8,000 international portfolio investors A full report on the winners will appear in the Special Commemorative 25th Anniversary responsible for more than Issue, released on June 25th, 2012. Award tallies are calculated to June 2012 issue. To compile the winners, we tallied winners/those taking first place over all of the years that a 80% of all global assets under particular award was given. -

70, Wanted to Own the Best Bar in Ann Arbor 25 Years Ago — Instead He Became CEO of a $9 Billion Food Company

University of Michigan Business School Alumni Connection Company Connection Degree Programs Executive Education Faculty Expertise Resources & Facilities University Home Page World Wide Web Address: http://www.bus.umich.edu Check Us Out t might well take a week of phone is an interview with Professor Joel The Business School student calls as well as numerous visits to Slemrod, director of the Office of newspaper The Monroe Street Journal, the School to access the wealth of Tax Policy Research, about the pros is now also being published on-line information now available by and cons of the flat tax. (http://www.umich.edu/~msjrnl), as Iaccessing the home page of the Dividend is also available through is detailed information about the city University of Michigan Business the alumni section of the home of Ann Arbor (http://online. ann- School (http://www.bus.umich.edu/). page. There you can write a letter to arbor.mi.us/ann-arbor/online. There you can find information the editor, change your address, or html). The University of Michigan about the admissions office, execu contribute a "Class Notes" item. and the U-M Alumni Association also tive education programs, office of Excerpts from the current issue are have home pages on the Internet career development, the William also on-line at that site. (http://www.umich.edu). Davidson Institute, the Tauber Tom Shaheen, computer systems Manufacturing Institute, the BBA consultant in Computing Services at A Classroom on the Web program, the Global MBA, and our the School, designed and produced curriculum. And with the Web's the Web Site, working with BBA ability to link documents together students Rich Blank and David Cole. -

Why Immigrants Benefit the United States Economy and the Legal and Tax Issues Chinese, Filipinos and Vietnamese Face When Immigrating to the U.S

Golden Gate University School of Law GGU Law Digital Commons Theses and Dissertations Student Scholarship 4-14-2016 Why Immigrants Benefit the nitU ed States Economy and the Legal and Tax Issues Chinese, Filipinos and Vietnamese Face When Immigrating to the U.S. Marc Santamaria Golden Gate University School of Law, [email protected] Follow this and additional works at: http://digitalcommons.law.ggu.edu/theses Part of the Comparative and Foreign Law Commons, and the Immigration Law Commons Recommended Citation Santamaria, Marc, "Why Immigrants Benefit the nitU ed States Economy and the Legal and Tax Issues Chinese, Filipinos and Vietnamese Face When Immigrating to the U.S." (2016). Theses and Dissertations. Paper 67. This Dissertation is brought to you for free and open access by the Student Scholarship at GGU Law Digital Commons. It has been accepted for inclusion in Theses and Dissertations by an authorized administrator of GGU Law Digital Commons. For more information, please contact [email protected]. GOLDEN GATE UNIVERSITY SCHOOL OF LAW ÈÈÈÈÈ Why Immigrants Benefit the United States Economy and the Legal and Tax Issues Chinese, Filipinos and Vietnamese Face When Immigrating to the U.S. Attorney Marc Santamaria, J.D., LL.M. S.J.D. Candidate ÈÈÈÈÈ SUBMITTED TO THE GOLDEN GATE UNIVERSITY SCHOOL OF LAW, DEPARTMENT OF INTERNATIONAL LEGAL STUDIES, IN FULFILLMENT OF THE REQUIREMENT FOR THE CONFERMENT OF THE DEGREE OF SCIENTIAE JURIDICAE DOCTOR (SJD). Professor Dr. Christian Nwachukwu Okeke Professor Dr. Remigius Chibueze Professor Dr. Gustave Lele SAN FRANCISCO, CALIFORNIA April 14, 2016 Acknowledgments To our God and Father be glory for ever and ever. -

Advancing Corporate Governance in the Philippines

PwC GGAPP Philippines Corporate Governance Survey Finding the true north Advancing corporate governance in the Philippines www.pwc.com/ph Foreword Message from the SEC Chairperson My warmest congratulations to In addition, the SEC believes that the the Good Governance Advocates results of this Survey would be most and Practitioners of the Philippines beneficial in the implementation (GGAPP) on the success of its 2016 of the 2016 Code of Corporate Code of Corporate Governance Governance for PLCs. The new Survey. The GGAPP has been a Code aims to make Philippine consistent partner of the Securities corporate governance standards at and Exchange Commission (SEC) par with regional and international in its advocacy to promote good standards and this Survey would corporate governance for Philippine be a useful tool for providing both corporations. As actual practitioners the SEC and PLCs the necessary of good corporate governance from information on the focus areas to various publicly listed companies be addressed in the advancement of (PLCs), GGAPP has consistently corporate governance for Philippine provided the SEC invaluable insights corporations. Atty. Teresita J. Herbosa Chairperson, Securities & Exchange on the application of best corporate Commissions (SEC) governance and ethical practices. The promotion of good corporate Moreover, GGAPP has contributed governance is an uphill battle. greatly to both the SEC Philippine However, with partners such as Corporate Governance Blueprint GGAPP assisting SEC in instilling and the 2016 Code of Corporate the proper corporate governance Governance for PLCs. foundation in PLCs, it is certain that the time will come when corporate This recent initiative of conducting governance will be second nature to the 2016 Code of Corporate companies and due recognition will Governance Survey in partnership be given to the benefits of compliance with Isla Lipana & Co./PwC with good practices. -

Toward a Philippine Legal Response to Global Finance: a National Security Perspective∗

Toward a Philippine Legal Response To Global Finance: A National Security Perspective∗ HECTOR DANNY D. UY∗∗ Introduction National security has been defined as that state or condition of the nation wherein the people’s way of life and institutions, their territorial integrity and sovereignty including their well-being are protected and enhanced. Its several components include the economic, political, military, environmental and socio-cultural dimensions of security. Threats to national existence that take any of these forms are actually threats to national security. There are seven fundamental elements that lie at the core of national security. These are: territorial integrity, ecological balance, socio-political stability, cultural cohesiveness, moral-spiritual consensus, external peace and economic solidarity. Economic solidarity is achieved when the economy is strong, capable of supporting national endeavors and derives its strength from the people who have an organic stake in it through their participation and ownership. On dealing with economic issues and concerns, the state shall continue implementing reforms that would generally improve the people’s lives and boost the economy by strengthening the capital markets, enhancing the foreign and domestic investment, and improving the business climate of the country.1 The recent Asian financial crisis of 1997 threatened the very existence of the Philippines as a state, just like other global financial crises that have left their indelible marks of destruction on other nations. The ∗ This paper is a condensed version of a thesis submitted by the author to the National Defense College of the Philippines (NDCP) in August 2005 to complete the requirements for a Master in National Security Administration (MNSA) degree. -

International Financial Policy John Coleman up to This

International Financial Policy John Coleman Up to this point in the course we developed the concept of a “real” (or “supply”) shock as well as a framework to understand the effects of real shocks on the global economy. Variables we considered consisted of the real values of the wage rate, employment, GDP, the interest rate, savings, consumption, investment, the current account, and the exchange rate. We also built on this material by examining the long-run determinants of the price level and its rate of change (inflation). Once we understood what determined the price level and its rate of change we were in a position to discuss key determinants of nominal variables such as nominal GDP, nominal interest rates, and nominal exchange rates. This lecture develops the concept of a “monetary” shock as well as a framework to understand the effects of monetary shocks on the global economy. Once we have a solid understanding of the effects of monetary shocks, we will be in a position to understand how any country uses its international financial policy to manipulate its economy, and the goals it attempts to achieve be setting its international financial policy. In this sense, this lecture is perhaps the key lecture in this course. I wish to start this lecture on monetary policy and the economy with a cautionary note. In attributing real effects to shocks stemming from monetary policy, in this course we will take the perspective of the loanable-funds theory. This view of the effects of monetary policy shocks seems to closely reflect the views of both central banks and the financial press. -

Divided Politics and Economic Growth in the Philippines Batalla, Eric Vincent C

www.ssoar.info Divided politics and economic growth in the Philippines Batalla, Eric Vincent C. Veröffentlichungsversion / Published Version Zeitschriftenartikel / journal article Zur Verfügung gestellt in Kooperation mit / provided in cooperation with: GIGA German Institute of Global and Area Studies Empfohlene Zitierung / Suggested Citation: Batalla, E. V. C. (2016). Divided politics and economic growth in the Philippines. Journal of Current Southeast Asian Affairs, 35(3), 161-186. https://nbn-resolving.org/urn:nbn:de:gbv:18-4-10145 Nutzungsbedingungen: Terms of use: Dieser Text wird unter einer CC BY-ND Lizenz (Namensnennung- This document is made available under a CC BY-ND Licence Keine Bearbeitung) zur Verfügung gestellt. Nähere Auskünfte zu (Attribution-NoDerivatives). For more Information see: den CC-Lizenzen finden Sie hier: https://creativecommons.org/licenses/by-nd/3.0 https://creativecommons.org/licenses/by-nd/3.0/deed.de Journal of Current Southeast Asian Affairs The Early Duterte Presidency in the Philippines Batalla, Eric Vincent C. (2016), Divided Politics and Economic Growth in the Philippines, in: Journal of Current Southeast Asian Affairs, 35, 3, 161–186. URN: http://nbn-resolving.org/urn/resolver.pl?urn:nbn:de:gbv:18-4-10145 ISSN: 1868-4882 (online), ISSN: 1868-1034 (print) The online version of this article can be found at: <www.CurrentSoutheastAsianAffairs.org> Published by GIGA German Institute of Global and Area Studies, Institute of Asian Studies and Hamburg University Press. The Journal of Current Southeast Asian Affairs is an Open Access publication. It may be read, copied and distributed free of charge according to the conditions of the Creative Commons Attribution-No Derivative Works 3.0 License. -

Implementation of BSP Rules on the Transport of Currencies

Rafael Buenaventura: Implementation of BSP rules on the transport of currencies Keynote address by Mr Rafael Buenaventura, Governor of Bangko Sentral ng Pilipinas (Central Bank of the Philippines), at the BSP Strategic Planning Conference, Manila, at the signing of the Memorandum of Agreement for the Effective Implementation of BSP rules on Physical Cross-border Transport of Currencies, Manila, 17 January 2005. * * * Good afternoon, friends, ladies and gentlemen. I would like to thank the agencies represented here for their full cooperation in the preparation of the Memorandum of Agreement (MOA) for the effective implementation of BSP rules on the physical cross-border transport of currencies, which will be signed today. We know that, each agency has more than enough work in its hands, and therefore, it is not easy to define and accept additional responsibilities, as would be the case in this MOA. I also want to thank the following signatories to this MOA who have taken time off from their busy schedules for this signing ceremony: 1. Bureau of Customs Commissioner George M. Jereos, 2. Manila International Airport Authority General Manager Alfonso G. Cusi, 3. Philippine National Police Director General Edgar B. Aglipay, 4. Bureau of Immigration Commissioner Alipio F. Fernandez 5. Air Transportation Office Executive Director Helen N. Camua, and 6. Philippine Ports Authority General Manager Oscar M. Sevilla. Of course, I am also a signatory under two hats, as BSP Governor and as Chairman of the Anti-Money Laundering Council. This MOA seeks to ensure the effective implementation of BSP rules on the physical cross-border transport of foreign currencies and the Philippine peso (PhP). -

DLSU Facts and Figures Is Produced by the Office for Strategic Communications of De La Salle University

FACTS AND FIGURES achieve a better future. FACTS FIGURESand DL SU THE FUTURE POWERHOUSE THE AGE BEGINS HERE THE TRANSFER OF TALENTS OF RECOVERY TO TAFT AVENUE 1910 1930 THE WAR YEARS 1920 1940 1950 1930 1954 1921 Extracurricular clubs De La Salle College Auxiliary Bishop of Manila and activities flourished Hernando Antiporda is the transferred to its present site during this decade. La on Taft Avenue, Manila. first La Salle alumnus to Salle’s star shone brightly become a member of the in the sports arena, Philippine hierarchy. The architectural design of with National Collegiate St. La Salle Hall was created Athletic Association 1956 by Tomas Mapua. It was (NCAA) championships in 1911 the winning entry in a Br. Bede Athanasius, the first The Brothers of the Christian basketball, football, and 1945 Filipino to become a Brother competition sponsored by the The War Years brought Schools opened the first La track events. of the Christian Schools from school. shell shock and damage to Salle School at 652 Calle the Baguio Novitiate, began the school, both in terms Nozaleda, Paco, Manila with Back then, La Salle also teaching at DLSC 125 students. During this time, many heads had a 200-member Glee of ruined buildings and of state visited it, not the Club, a combo of jazz human carnage. Sixteen least of which were then- Brothers and 25 civilians 1957 Nine Brothers (five Frenchmen, musicians, a reputed The College of Liberal Governor-General Leonard were massacred one tragic three Irish, and one American) oratorical team, and a Arts and the College of formed what would be the Wood and Senate President cheering squad named February day in 1945.