Cornwall Council 2018/19 Annual Financial Report and Statement of Accounts

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Standards Exchange Website Extracts , Item 4. PDF 77 KB

STANDARDS ISSUES ARISEN FROM OTHER PARTS OF THE COUNTRY Cornwall Council A Cornwall councillor who said disabled children “should be put down” has been found guilty of breaching the councillors’ code of conduct – but cannot be suspended. Wadebridge East member Collin Brewer’s comments were described by a panel investigating the claims as “outrageous and grossly offensive”. Cornwall Council said it received 180 complaints about Mr Brewer following the revelation that he said disabled children should be put down as they cost the council too much – and a subsequent interview he gave to the Disability News Service after his re-election on May 2 where he likened disabled children to deformed lambs. On Friday its findings were considered by the council’s standards committee in a behind-closed-doors session. Although Mr Brewer has been found to be in breach of the Code of Conduct, the council does not have the legal power to remove him from his position as a councillor. A council spokesman said: “The authority previously had the ability to suspend councillors following the investigation and determination of Code of Conduct complaints, however, following the Government’s changes to the Code of Conduct complaints process, this sanction is no longer available.” The council said that “given the seriousness of the breach” the council’s monitoring has imposed the highest level of sanctions currently available to the council. These include: • Formally censuring Mr Brewer for the outrageous and grossly insensitive remarks he made in the telephone conversation with John Pring on May 8 and directing him to make a formal apology for the gross offensiveness of his comments and the significant distress they caused. -

Comparison of Overview and Scrutiny Functions at Similarly Sized Unitary Authorities

Appendix B (4) – Comparison of overview and scrutiny functions at similarly sized unitary authorities No. of Resident Authority elected Committees Committee membership population councillors Children and Families OSC 12 members + 2 co-optees Corporate OSC 12 members Cheshire East Council 378,800 82 Environment and Regeneration OSC 12 members Health and Adult Social Care and Communities 15 members OSC Children and Families OSC 15 members, 2 co-optees Customer and Support Services OSC 15 members Cornwall Council 561,300 123 Economic Growth and Development OSC 15 members Health and Adult Social Care OSC 15 members Neighbourhoods OSC 15 members Adults, Wellbeing and Health OSC 21 members, 2 co-optees 21 members, 4 church reps, 3 school governor reps, 2 co- Children and Young People's OSC optees Corporate Overview and Scrutiny Management Durham County Council 523,000 126 Board 26 members, 4 faith reps, 3 parent governor reps Economy and Enterprise OSC 21 members, 2 co-optees Environment and Sustainable Communities OSC 21 members, 2 co-optees Safeter and Stronger Communities OSC 21 members, 2 co-optees Children's Select Committee 13 members Environment Select Committee 13 members Wiltshere Council 496,000 98 Health Select Committee 13 members Overview and Scrutiny Management Committee 15 members Adults, Children and Education Scrutiny Commission 11 members Communities Scrutiny Commission 11 members Bristol City Council 459,300 70 Growth and Regeneration Scrutiny Commission 11 members Overview and Scrutiny Management Board 11 members Resources -

Cornwall Council) (Respondent) V Secretary of State for Health (Appellant)

Trinity Term [2015] UKSC 46 On appeal from: [2014] EWCA Civ 12 JUDGMENT R (on the application of Cornwall Council) (Respondent) v Secretary of State for Health (Appellant) R (on the application of Cornwall Council) (Respondent) v Somerset County Council (Appellant) before Lady Hale, Deputy President Lord Wilson Lord Carnwath Lord Hughes Lord Toulson JUDGMENT GIVEN ON 8 July 2015 Heard on 18 and 19 March 2015 Appellant (Secretary of Respondent (Cornwall State for Health) Council) Clive Sheldon QC David Lock QC Deok-Joo Rhee Charles Banner (Instructed by (Instructed by Cornwall Government Legal Council Legal Services) Department) Appellant /Intervener (Somerset County Council) David Fletcher (Instructed by Somerset County Council Legal Services Department) Intervener (South Gloucestershire Council) Helen Mountfield QC Sarah Hannett Tamara Jaber (Instructed by South Gloucestershire Council Legal Services) Intervener (Wiltshire Council) Hilton Harrop-Griffiths (Instructed by Wiltshire Council Legal Services) LORD CARNWATH: (with whom Lady Hale, Lord Hughes and Lord Toulson agree) Introduction 1. PH has severe physical and learning disabilities and is without speech. He lacks capacity to decide for himself where to live. Since the age of four he has received accommodation and support at public expense. Until his majority in December 2004, he was living with foster parents in South Gloucestershire. Since then he has lived in two care homes in the Somerset area. There is no dispute about his entitlement to that support, initially under the Children Act 1989, and since his majority under the National Assistance Act 1948. The issue is: which authority should be responsible? 2. This depends, under sections 24(1) and (5) of the 1948 Act, on, where immediately before his placement in Somerset, he was “ordinarily resident”. -

Local Authority / Combined Authority / STB Members (July 2021)

Local Authority / Combined Authority / STB members (July 2021) 1. Barnet (London Borough) 24. Durham County Council 50. E Northants Council 73. Sunderland City Council 2. Bath & NE Somerset Council 25. East Riding of Yorkshire 51. N. Northants Council 74. Surrey County Council 3. Bedford Borough Council Council 52. Northumberland County 75. Swindon Borough Council 4. Birmingham City Council 26. East Sussex County Council Council 76. Telford & Wrekin Council 5. Bolton Council 27. Essex County Council 53. Nottinghamshire County 77. Torbay Council 6. Bournemouth Christchurch & 28. Gloucestershire County Council 78. Wakefield Metropolitan Poole Council Council 54. Oxfordshire County Council District Council 7. Bracknell Forest Council 29. Hampshire County Council 55. Peterborough City Council 79. Walsall Council 8. Brighton & Hove City Council 30. Herefordshire Council 56. Plymouth City Council 80. Warrington Borough Council 9. Buckinghamshire Council 31. Hertfordshire County Council 57. Portsmouth City Council 81. Warwickshire County Council 10. Cambridgeshire County 32. Hull City Council 58. Reading Borough Council 82. West Berkshire Council Council 33. Isle of Man 59. Rochdale Borough Council 83. West Sussex County Council 11. Central Bedfordshire Council 34. Kent County Council 60. Rutland County Council 84. Wigan Council 12. Cheshire East Council 35. Kirklees Council 61. Salford City Council 85. Wiltshire Council 13. Cheshire West & Chester 36. Lancashire County Council 62. Sandwell Borough Council 86. Wokingham Borough Council Council 37. Leeds City Council 63. Sheffield City Council 14. City of Wolverhampton 38. Leicestershire County Council 64. Shropshire Council Combined Authorities Council 39. Lincolnshire County Council 65. Slough Borough Council • West of England Combined 15. City of York Council 40. -

Street Lighting As an Asset; Smart Cities and Infrastructure Developments ADEPTE ASSOCIATION of DIRECTORS of ENVIRONMENT, ECONOMY PLANNING and TRANSPORT

ADEPTE ASSOCIATION OF DIRECTORS OF ENVIRONMENT, ECONOMY PLANNING AND TRANSPORT DAVE JOHNSON ADEPT Street Lighting Group chair ADEPT Engineering Board member UKLB member TfL Contracts Development Manager ADEPTE ASSOCIATION OF DIRECTORS OF ENVIRONMENT, ECONOMY PLANNING AND TRANSPORT • Financial impact of converting to LED • Use of Central Management Systems to profile lighting levels • Street Lighting as an Asset; Smart Cities and Infrastructure Developments ADEPTE ASSOCIATION OF DIRECTORS OF ENVIRONMENT, ECONOMY PLANNING AND TRANSPORT ASSOCIATION OF DIRECTORS OF ENVIRONMENT, ECONOMY, PLANNING AND TRANSPORT Representing directors from county, unitary and metropolitan authorities, & Local Enterprise Partnerships. Maximising sustainable community growth across the UK. Delivering projects to unlock economic success and create resilient communities, economies and infrastructure. http://www.adeptnet.org.uk ADEPTE SOCIETY OF CHIEF OFFICERS OF CSS Wales TRANSPORTATION IN SCOTLAND ASSOCIATION OF DIRECTORS OF ENVIRONMENT, ECONOMY PLANNING AND TRANSPORT ADEPTE SOCIETY OF CHIEF OFFICERS OF CSS Wales TRANSPORTATION IN SCOTLAND ASSOCIATION OF DIRECTORS OF ENVIRONMENT, ECONOMY PLANNING AND TRANSPORT Bedford Borough Council Gloucestershire County Council Peterborough City Council Blackburn with Darwen Council Hampshire County Council Plymouth County Council Bournemouth Borough Council Hertfordshire County Council Portsmouth City Council Bristol City Council Hull City Council Solihull MBC Buckinghamshire County Council Kent County Council Somerset County -

Cornwall and Isles of Scilly Industrial Strategy 2030 (Draft)

Information Classification: CONTROLLED Cornwall and Isles of Scilly DRAFT Industrial Strategy Contents Introduction .............................................................................................................................................................................. 2 Vision ...................................................................................................................................................................................... 3 Cornwall and Isles of Scilly Industrial Strategy Overview ................................................................................. 4 Cornwall and the Isles of Scilly .......................................................................................................................................... 5 Distinctive challenges ...................................................................................................................................................... 5 Where we are: the economy today ............................................................................................................................. 7 The future economy of CIoS ........................................................................................................................................... 8 Our administration and devolution ......................................................................................................................... 10 Principles of design and metrics ................................................................................................................................... -

Agenda Item 1

5 Agenda Item 1 Minutes of a meeting of the Scrutiny Commission held at County Hall, Glenfield on Friday, 30 November 2018. PRESENT Mr. S. J. Galton CC (in the Chair) Mr. D. C. Bill MBE CC Mrs. R. Page CC Mr. G. A. Boulter CC Mr. A. E. Pearson CC Dr. T. Eynon CC Mr. T. J. Pendleton CC Dr. R. K. A. Feltham CC Mr. T. J. Richardson CC Mr. D. Harrison CC Mrs B. Seaton CC Mr. J. Morgan CC 53. Minutes. The minutes of the meeting held on 14 November 2018 were taken as read, confirmed and signed. 54. Question Time. The Chief Executive reported that no questions had been received under Standing Order 35. 55. Questions asked by members under Standing Order 7(3) and 7(5). The Chief Executive reported that no questions had been received under Standing Order 7(3) and 7(5). 56. Urgent Items. There were no urgent items for consideration. 57. Declarations of Interest. The Chairman invited members who wished to do so to declare any interest in respect of items on the agenda for the meeting. All members of the Commission who were also members of district or parish councils declared a personal interest in the report on proposals for a unitary structure of local government in Leicestershire (minute 60 refers). 58. Declarations of the Party Whip in accordance with Overview and Scrutiny Procedure Rule 16. There were no declarations of the party whip. 6 59. Presentation of Petitions under Standing Order 36. The Chief Executive reported that no petitions had been received under Standing Order 36. -

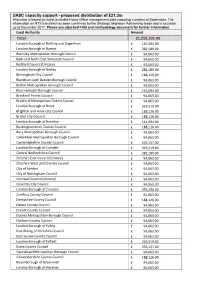

UASC Capacity Support - Proposed Distribution of £21.3M Allocation Is Based on Latest Available Home Office Management Data Capturing Numbers at September

UASC capacity support - proposed distribution of £21.3m Allocation is based on latest available Home Office management data capturing numbers at September. The information on NTS transfers has been confirmed by the Strategic Migration Partnership leads and is accurate up to December 2017. Please see attached FAQ and methodology document for further information. Local Authority Amount Total 21,258,203.00 London Borough of Barking and Dagenham £ 141,094.00 London Borough of Barnet £ 282,189.00 Barnsley Metropolitan Borough Council £ 94,063.00 Bath and North East Somerset Council £ 94,063.00 Bedford Council (Unitary) £ 94,063.00 London Borough of Bexley £ 282,189.00 Birmingham City Council £ 188,126.00 Blackburn with Darwen Borough Council £ 94,063.00 Bolton Metropolitan Borough Council £ 94,063.00 Bournemouth Borough Council £ 141,094.00 Bracknell Forest Council £ 94,063.00 Bradford Metropolitan District Council £ 94,063.00 London Borough of Brent £ 329,219.00 Brighton and Hove City Council £ 188,126.00 Bristol City Council £ 188,126.00 London Borough of Bromley £ 141,094.00 Buckinghamshire County Council £ 188,126.00 Bury Metropolitan Borough Council £ 94,063.00 Calderdale Metropolitan Borough Council £ 94,063.00 Cambridgeshire County Council £ 235,157.00 London Borough of Camden £ 329,219.00 Central Bedfordshire Council £ 282,189.00 Cheshire East Council (Unitary) £ 94,063.00 Cheshire West and Chester Council £ 94,063.00 City of London £ 94,063.00 City of Nottingham Council £ 94,063.00 Cornwall Council (Unitary) £ 94,063.00 Coventry City -

Cheshire East Council

Cheshire East Council Carbon Neutrality Action Plan 2020-2025 January 2020 Contents Introduction & Context Page 3 1. Process Page 6 2. Council Influence Page 7 3. Carbon Neutrality Page 10 4. Current Emissions Profile and Pathways Page 11 5. The Action Plan Page 16 Topic 1: Behaviour Change and Internal Policy Page 18 Topic 2: Energy Demand Reduction Page 29 Topic 3: Increase Low Carbon Energy Supply Page 38 Topic 4: Natural Capital Page 48 Topic 5: Reduce Borough-wide Emissions/External Policy Page 54 6. Summary of Measures Page 73 2 Introduction and Context Introduction At the Council meeting on 22 May 2019 the Elected Members of Cheshire East Council (CEC) approved the following Notice of Motion relating to Climate Change. “This Council notes that on 1 May Parliament declared an environment and climate emergency and a) Requests that a Cheshire East Environmental Strategy is brought forward as a matter of urgency; b) Commits to the target of Cheshire East Council being carbon neutral by 2025 and asks that details of how to meet this commitment are included in the Environmental Strategy; c) Will work to encourage all businesses, residents and organisations in Cheshire East to reduce their carbon footprint by reducing energy consumptions and promoting healthy lifestyles.” This work is being commissioned by Cheshire East Council in response to this motion. Document purpose This Carbon Neutral Action Plan is focused on actions that CEC should consider deploying directly in support of the carbon neutral 2025 target. A separate Supplementary -

Cornwall Local Plan: Strategic Policies

Planning for Cornwall Cornwall’s future Local Plan Strategic Policies 2010 - 2030 Towl leel Kernow Policis Stratejek 2010 - 2030 www.cornwall.gov.uk Cornwall is the second largest local authority in the south west, covering an area of Crime in Cornwall is 3,559 sq km generally low with a coastline of 697km and it is a safe place in which to live and work Cornwall’s environmental assets are extremely valuable and are a 76% (as at 2014) of Cornwall’s key contributor to the economy and population and quality of life (414,466 people) are of working age (2011) Over of the population of Cornwall40% live in settlements of less than 3,000 people Median gross annual pay in Cornwall is £22,068 Agriculture and fishing compared to England at £26,165 (2011) account for a larger share of employment in Cornwall (3%) than Strengthening Cornwall’s economy the regional (2%) or national (1%) is an ongoing challenge - l (2010). economic output, low wages,ow low productivity and a lack of big companies are challenges Education and Skills - Over 69,900 Six universities and children colleges and young people are educated in make up the Combined University for state funded schools and academies Cornwall which attracted over 7,700 with a further 2,525 pupils on roll higher education students in 2009/10. across independent schools in Cornwall) To support the delivery of over 38,000 jobs over the plan period the target of 422,400 sq m of employment floorspace has been provided Planning for Cornwall Cornwall’s future Local Plan Strategic Policies 2010 - 2030 Adopted November 2016 Note: This document should be read in conjunction with the Policies maps and the Community Network Area Sections. -

Electric Chargepoint Analysis 2017: Local Authority Rapids

Statistical Release 13 December 2018 Electric Chargepoint Analysis 2017: Local Authority Rapids About this release This publication has been revised for the following reasons: This statistical release • The original release omitted data from Cornwall Council, approximately 2,500 presents experimental charging events. This has now been added to the underlying data and analysis statistics on local authority presented in this release. rapid plug-in vehicle • Some of the chargepoints reported to DfT as rapids were actually fast chargers. chargepoints in England in Charging events from fast chargers have been removed and added to our separate 2017. Data from the 27 local publication on Public Sector Fasts. This removed approximately 25,000 events from authorities that received the dataset and resulted in slightly higher average energy supplied per event and grants from the Local shorter average durations. Most of the figures in the release have been revised. Authority Grant Fund (LAGF) was provided as a condition • Further analysis has revealed that several local authorities received funding for of the grants. Complete data chargepoints outside their geographical boundaries, for example via joint bids. is only available for 2017. Therefore the local authority name does not indicate where the chargepoint is located. Consequently this report Less than half of the chargepoints had an identifiable location, so geographical focuses on that year alone. analysis is not possible and the local authority map has been removed. The Local Authority Grant Fund was set up in 2013 by the Office for Low Emission Vehicles (OLEV) to deliver recharging infrastructure in the UK. This analysis has been produced to help support and inform Key findings: the strategy for ultra low emission vehicles in the • Energy supplied The median average energy supplied by rapid UK. -

Housing Board Governance Review V0.1 Draft Report June 2017

Wiltshire Council Housing Board Governance Review v0.1 Draft report June 2017 Property People Strategy & Governance Finance Client Name Wiltshire Council – Housing Board Governance Review Contents 1 | Introduction – the brief and our approach 3 2 | Findings 4 3 | Options 14 Appendix 1 | Documents reviewed 16 Appendix 2 | Persons interviewed 17 Appendix 3 | Housing boards and scrutiny panels research 18 Our report is addressed to Wiltshire Council. We stress that our report is confidential and prepared for the addressees only. It should not be used, reproduced or circulated for any other purpose, whether in whole or in part without our prior written consent, which consent will only be given after full consideration of the circumstances at the time. If the report is released to a third party without prior consent from Altair, we do not acknowledge any duty of care to the third party and do not accept liability for any reliance placed on the report. Page | 2 Client Name Wiltshire Council – Housing Board Governance Review 1 | Introduction – the brief and our approach 1.1. The Brief 1.1.1. Wiltshire Council (the Council) owns and manages some 5,289 homes1, mostly in the Salisbury and South Wiltshire areas of the county. The Council is also developing some 200 new homes, funded by the Housing Revenue Account (HRA)2. In 2013, the Council set up the Wiltshire Council Housing Board (Housing Board) to support the Executive (Cabinet) in the oversight of its housing services to tenants and leaseholders. The Housing Board first met in December 2013 and holds meetings approximately bi-monthly.