Anglo American 1

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Consolidated Gold Fields, PLC V. Minorco, SA

American University International Law Review Volume 6 | Issue 3 Article 5 1991 Consolidated Gold Fields, PLC v. Minorco, S.A.: The Growing Over-Extension of United States Antitrust Law Jacqueline B. Berman Follow this and additional works at: http://digitalcommons.wcl.american.edu/auilr Part of the International Law Commons Recommended Citation Berman, Jacqueline B. "Consolidated Gold Fields, PLC v. Minorco, S.A.: The Growing Over-Extension of United States Antitrust Law." American University International Law Review 6, no. 3 (1991): 399-433. This Article is brought to you for free and open access by the Washington College of Law Journals & Law Reviews at Digital Commons @ American University Washington College of Law. It has been accepted for inclusion in American University International Law Review by an authorized administrator of Digital Commons @ American University Washington College of Law. For more information, please contact [email protected]. NOTE CONSOLIDATED GOLD FIELDS, PLC V. MINORCO, S.A.: THE GROWING OVER-EXTENSION OF UNITED STATES ANTITRUST LAW Jacqueline B. Berman* INTRODUCTION As the number of antitrust cases grows, so does the United States judiciary's application and expansion of antitrust law. The Second Cir- cuit's decision in ConsolidatedGold Fields, PLC v. Minorco, S.A.' is a prime example of this expansion. In this case, the Second Circuit used inapplicable antitrust principles to gain jurisdiction over a foreign merger. The case, in which a British target company attempted to stop a Luxembourg-based company's hostile takeover,2 raises important an- * J.D. Candidate, 1992, Washington College of Law, The American University. 1. -

Consolidated Gold Fields in Australia the Rise and Decline of a British Mining House, 1926–1998

CONSOLIDATED GOLD FIELDS IN AUSTRALIA THE RISE AND DECLINE OF A BRITISH MINING HOUSE, 1926–1998 CONSOLIDATED GOLD FIELDS IN AUSTRALIA THE RISE AND DECLINE OF A BRITISH MINING HOUSE, 1926–1998 ROBERT PORTER Published by ANU Press The Australian National University Acton ACT 2601, Australia Email: [email protected] Available to download for free at press.anu.edu.au ISBN (print): 9781760463496 ISBN (online): 9781760463502 WorldCat (print): 1149151564 WorldCat (online): 1149151633 DOI: 10.22459/CGFA.2020 This title is published under a Creative Commons Attribution-NonCommercial- NoDerivatives 4.0 International (CC BY-NC-ND 4.0). The full licence terms are available at creativecommons.org/licenses/by-nc-nd/4.0/legalcode Cover design and layout by ANU Press. Cover photograph John Agnew (left) at a mining operation managed by Bewick Moreing, Western Australia. Source: Herbert Hoover Presidential Library. This edition © 2020 ANU Press CONTENTS List of Figures, Tables, Charts and Boxes ...................... vii Preface ................................................xiii Acknowledgements ....................................... xv Notes and Abbreviations ................................. xvii Part One: Context—Consolidated Gold Fields 1. The Consolidated Gold Fields of South Africa ...............5 2. New Horizons for a British Mining House .................15 Part Two: Early Investments in Australia 3. Western Australian Gold ..............................25 4. Broader Associations .................................57 5. Lake George and New Guinea ..........................71 Part Three: A New Force in Australian Mining 1960–1966 6. A New Approach to Australia ...........................97 7. New Men and a New Model ..........................107 8. A Range of Investments. .115 Part Four: Expansion, Consolidation and Restructuring 1966–1981 9. Move to an Australian Shareholding .....................151 10. Expansion and Consolidation 1966–1976 ................155 11. -

Country by Country Reporting

COUNTRY BY COUNTRY REPORTING PUBLICATION REPORT 2018 (REVISED) Anglo American is a leading global mining company We take a responsible approach to the management of taxes, As we strive to deliver attractive and sustainable returns to our with a world class portfolio of mining and processing supporting active and constructive engagement with our stakeholders shareholders, we are acutely aware of the potential value creation we operations and undeveloped resources. We provide to deliver long-term sustainable value. Our approach to tax is based can offer to our diverse range of stakeholders. Through our business on three key pillars: responsibility, compliance and transparency. activities – employing people, paying taxes to, and collecting taxes the metals and minerals to meet the growing consumer We are proud of our open and transparent approach to tax reporting. on behalf of, governments, and procuring from host communities – driven demands of the world’s developed and maturing In addition to our mandatory disclosure obligations, we are committed we make a significant and positive contribution to the jurisdictions in economies. And we do so in a way that not only to furthering our involvement in voluntary compliance initiatives, such which we operate. Beyond our direct mining activities, we create and generates sustainable returns for our shareholders, as the Tax Transparency Code (developed by the Board of Taxation in sustain jobs, build infrastructure, support education and help improve but also strives to make a real and lasting positive Australia), the Responsible Tax Principles (developed by the B Team), healthcare for employees and local communities. By re-imagining contribution to society. -

REVIEW: ANGLO -Anglo American and the Rise of Modern South Africa

REVIEW: ANGLO -Anglo American and the rise of modern South Africa Duncan Innes Raven Press, Johannesburg, 1984, 358 pp, (R14,95) South African workers are probably aware of the significant role which a few large companies play in their lives. How those companies reached their present positions of power is less well-known, and how they are linked together is a sub ject shrouded in mystery. Duncan Innes*s book, Anglo, deals first with the origins of Anglo American Corporation. Because Anglo Americans growth was made possible in large part by its association with De Beers Consolidated Diamond Mines, Dr Innes begins with a short history of diamond mining and the development of the De Beers near-monopoly in this industry. This material prov ides the background for an account of the way in which the group system was formed on the Witwatersrand gold fields dur ing the years 1886-1910. Under this system, most gold mines came under the control of a small number of mining "houses" such as Gold Fields and the Corner House group (a forerunner of Barlow Rand). Anglo American itself was born during the first world war. The company was formed to tap American as well as other sourc- ®s of finance, but its base lay in gold and coal mining groups which already owned rich properties in various areas. From the start, Anglo American was a highly profitable venture. Its rich mines allowed it to ride out problems - including the strikes of 1920 and 1922 - better than some others. Meanwhile, De Beers faced mounting problems in the diamond ^rket. -

The Post-Apartheid Restructuring of South Africa's Steel And

DRAFT – NOT FOR DISTRIBUTION OR CITATION Engineering Deindustrialisation: the Post-apartheid Restructuring of South Africa’s Steel and Engineering Sectors Nimrod Zalk, Industrial Development Advisor, Department of Trade and Industry, South Africa Draft paper: 8th European Conference on African Studies, University of Edinburgh, June 11-14 2019 1. Introduction Capitalist development since the Second World War ushered in unprecedented rates of capital accumulation and structural change in the world economy through industrialization (Maddison 2007). However, the pace of South African industrialization was poor relative to middle income developing countries, both during the last quarter century of apartheid (Fallon & de Silva 1994; Feinstein 2005; Fine & Rustomjee 1996; Gelb 1991; Joffe et al. 1995) and the first twenty five years of democracy (Bell et al. 2018; Rodrik 2008). How is mediocre post-apartheid industrialisation to be understood? I tackle this question through the lens of the post-apartheid restructuring of the three private and public conglomerates – Iscor, Anglo American and Rembrandt – that dominated the steel and engineering sectors over South Africa’s transition from apartheid to democracy. This focus is justified first, because various development theorists have singled out the steel and engineering sectors as central to industrialisation due to positive linkage, spillover and balance of payments effects (Amsden 1992 p. 198; Hirschman 1988; Mahalanobis 1953; Nolan 2001; Woo-Cumings 1999). Second, steel has been an exemplar of apartheid heavy industrialisation under a “Minerals Energy Complex” (Cross 1994; Fine & Rustomjee 1996) with engineering playing a subordinate role (Rustomjee 1993; Zalk Page 1 of 52 DRAFT – NOT FOR DISTRIBUTION OR CITATION 2017). Third, Anglo American (Anglo) and Rembrandt were the two largest apartheid private conglomerates and, together with state-owned Iscor, collectively dominated the steel and engineering sectors. -

Anglo American and the Rise of Modern South Mrica

I I I I Anglo American and the Rise of Modern South Mrica Duncan Innes (@ MONTHLY REVIEW PRESS NEW YORK For my father, and to the . memories ofmy mother and sUiter Copyright © 1984 by Duncan Innes All rights reserved Library ofCongress Cataloging in Publication Data Innes, Duncan. Anglo American and the rise of modern South Africa. Bihliography, p. Includes index. 1. Anglo American Corporation of.South Africa, Ltd. History. 2. South Africa-Economic conditions. 3. Mineral industries-South Africa-History. 4. South Africa-Industries_History. I. Title. HD9506. S74A534 1983 338.7'622342'0968 83-42523 ISBN 0-85345-628_3 ISBN 0-85345-629-1 (pbk.) Monthly Review Press 155 West 23rd Street New York, N. Y. l0011 Manufactured in the United States ofAmerica 10 9 8 7 6 5 4 3 2 1 APPENDIX 2 A Survey of the Anglo American Group of Companies INTRODUCTION This appendix lists and provides information on 656 companies in the Anglo American Croup. The list is not a fully comprehensive record, but is the most extensive public compilation of those companies involved with the Group up to the end of 1976. The appendix is divided info two parts. The first lists the most important 14 holding companies in the Group. isolating the 6 companies which form the core ofGroup structure. Information on the cross-holdings among these 6, and on some of the cross-holdings among the 14 companies, is also provided. A diagram is included. The second and major part of the appendix lists those companies which form the bulk of the Anglo American Group. -

Per Country, Business Unit & Project

Country Highlights Summary - Per Country, Business Unit & Project Total EUAD & Total EUAD other taxes excluding Total other taxes Total other taxes borne and USD millions infrastructure borne collected collected Argentina Exploration Corporate level - Minera Anglo American Argentina SA 0.1 0.4 0.5 Agua Amarga Argentina greenfields Cerro Verde Piuquenes Total Argentina - 0.1 0.4 0.5 Australia Coal Moronbah North 36.8 11.7 19.3 67.8 Dawson 39.4 17.0 26.1 82.5 Foxleigh 9.6 6.0 5.6 21.2 Capcoal 63.3 22.3 34.7 120.3 German Creek Grasstree Management Callide 14.5 9.0 13.4 36.9 Drayton 6.1 5.6 16.3 28.0 Grosvenor 10.8 5.7 6.1 22.6 Dartbrook 0.4 0.4 Monash CAML resources Corporate level - Anglo American Australia Ltd Corporate level - Anglo American Metallurgical Coal Pty Ltd 9.4 27.8 37.2 Corporate level - Anglo American Thermal Coal (Australia) Pty Ltd 0.1 0.1 0.2 Corporate level - Anglo Operations (Australia) Pty Ltd Total Coal 180.5 87.2 149.4 417.1 Exploration Asia Australia Greenfields Moronbah South exploration 2.3 2.3 Dawson South 1.4 1.4 Drayton South Blue Dog (Previously Ebony Coal) Bushranger Earaheedy (Anglo 100%) Earaheedy (Cazally JV) Fe Generative - Australia Musgraves Fairhills Met Coal Theodore Exploration JV 0.2 0.2 Corporate level - Anglo American Exploration (Australia) Pty Ltd 0.6 1.2 1.8 Total Exploration - 4.5 1.2 5.7 Total Australia 180.5 91.7 150.6 422.8 Brazil Iron Ore & Manganese Corporate level - Anglo American Minerio de Ferro Brasil S.A 24.2 24.2 Minas-Rio 19.8 1.3 19.1 40.2 Ferroport Total Iron Ore & Manganese 19.8 25.5 19.1 64.4 Nickel Corporate level - Anglo American Niquel Brasil Ltda 1.1 10.3 9.3 20.7 Barro Alto 2.8 6.3 31.6 40.7 Codemin 0.2 2.6 3.6 6.4 Forests (4 licences on registry) Total Nickel 4.1 19.2 44.5 67.8 Country Highlights Summary - Per Country, Business Unit & Project Total EUAD & Total EUAD other taxes excluding Total other taxes Total other taxes borne and USD millions infrastructure borne collected collected Niobium & Phosphates Corporate level - Anglo American Niobio Ltda. -

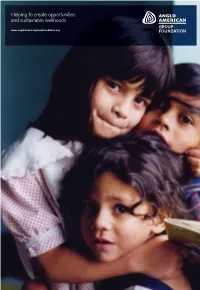

Helping to Create Opportunities and Sustainable Livelihoods GROUP FOUNDATION

Helping to create opportunities and sustainable livelihoods GROUP www.angloamericangroupfoundation.org FOUNDATION 01 Note from the Chair 02 Anglo American plc: our funder 03 04 05 Engineers Without CARE The funding from The Connection Borders UK Anglo American Group at St Martin’s Focusing on the fight Foundation has also against poverty supported CARE’s Alleviating poverty microfinance programme, Helping homeless people through engineering by creating 400 to make lasting changes savings groups in their lives The Foundation is currently funding a community-driven water, 06 07 education and sanitation project which includes Fairbridge PLAN education on the importance of safe Promoting the rights Working with 13-25 year olds in hygiene and sanitation of children worldwide some of the most disadvantaged for 3000 residents within areas in the UK target communities 08 Pro Mujer Providing credit, healthcare and business training for poor Anglo American Group women entrepreneurs Foundation funding will enable Sightsavers and its partners to reach 1,500,000 people 10 Anglo American Group Foundation Trustees 11 Governance and Application process 09 12 Financial Information Sightsavers Fighting blindness worldwide Note from the Chair 01 Cover: This is the first public report produced Three children who benefit from the services given at Ponte en Mi Lugar. In late 2005, the Anglo American plc by the Anglo American Group Foundation began engaging with charity organisation Children of the Andes, COA. Children of the Andes is a UK based charity that provides support Foundation. It provides a brief account to Columbia’s most vulnerable children through working with local NGOs. COA was established in 1991 to support of some of the activities of the children living on the streets and in the sewers of Bogotá Foundation since it was established in 2005. -

Major Sectoral Developments

September 1986 Major Sectoral Developments The following section focuses on major investment transaction trends in the more active industrial sectors during 1985. Metal Mining (SIC 10) - Foreign direct investment in U.S. metal mining firms, at a low ebb for the past few years, rebounded slightly in 1985. Concerns over political instability abroad, country debt repayment problems and a weakening U.S. dollar were factors that accounted for increased foreign investment in this sector. In 1985,10 completed transactions were identified; 7 of them had a total value or $124.4 million, a four-fold increase over the 1984 figure. The largest transaction was the acquisition of Copper Range Co. by Echo Bay Mines Ltd. of Edmonton, Canada for $55 million. Echo Bay Mines, operator of Canada's second largest gold mine, will expand its interests through the purchase of Copper Range which has several gold exploration projects in Nevada as well as copper interests in Michigan. The second largest transaction was the addition of a new mill at Newmont Mining Corp.'s Carlin gold mine in northeastern Nevada valued at $33.9 million. Newmont Mining is 26.1 percent owned by Consolidated Gold Fields Ltd. of England, itself 29 percent owned by Minorco, a Bermuda-based firm controlled by Anglo-American Corp. of South Africa Ltd. Canada was the primary source country for investors in the metal mining sector in 1985. Canadian investors accounted for almost half of the transactions (5). In second place were investors from the United Kingdom with 2 transactions. These investments were largely mine expansions (4) or acquisitions (3). -

Against Apartheid

REPORT OF THE SPECIAL COMMITTEE AGAINST APARTHEID GENERAL ASSEMBLY OFFICIAL RECORDS: FORTY-FOURTH SESSION SUPPLEMENT No. 22 (A/44/2~) UNITED NATIONS New York, 1990 NOTE Symbols of United Nations documents are composed ofcapital letters combined with figures. Mention of sl!ch a symbol indicates a reference to a United Nations document. The present. report was also submitted to the Security Council under the symbol S/20901. ISSN 0255-1845 1111 iqlllllll l~uqllHh) I!i li'alHlltHy 19~O 1 CONTENTS LBTTER OF TRANSMITTAL •••••••••••••••••••••••••••• l1li •• l1li ••••••••••••••••••••••• PART ONE ~~AL RBPORT OF THE SPECIAL COMMITTEE •...•....••............... 1 275 2 I • INTRODUCTION ••••••••••.•••.••.••.......•.......•. l1li •••••••• 1 1 3 11. RBVIBW OF DEVELOPMENTS IN SOUTH AFRICA .........•.......... [, q4 1 A. General political conditions !l 15 4 B. Repression of the r~pulation .......................... 1.6 4" () 1.. Overview ...•.......•.............................. 1(; fi 2. Political trials, death sentences and executions .. I.., - 7.4 r; 3. Detention without trial ?!l 7.11 IJ 4. Vigilante groups, death squads and covert activities .. ' . 29 35 y 5. Security laws, banning and restriction or(\ers ..... lfi :19 11 6. Forced population removals ..••....••...•.......... 10 .. 45 12 7. Press censorship I ••••••••• 46 - 47 13 C. Resistance to apartheid .•.......•..................... 411 .. 03 13 1. Organizing broader fronts of resistance .....•..... 40 5n 11 2. National liberation movements . !i9 1;1 I. t) 3. Non-racial trade union movement Ij tl 1;9 l" 4. Actions by religious, youth and student gr Il\lllt~ ••.. "10 .,., III 5. Whites in the resistance . "111 1I:cl ),0 1)4 D. Destabilization and State terrorism . " 'I 7.2 Ill. EXTERNAL RELATIONS OF SOUTH AFRICA , . -

The Mineral Industries of Latin America and Canada in 1999

THE MINERAL INDUSTRIES OF LATIN AMERICA AND CANADA1 By David B. Doan, Alfredo C. Gurmendi, Ivette E. Torres, and Pablo Velasco INTRODUCTION Canada led the world in the production of uranium and was the second largest producer of zinc after China, with a strong Mining and related activities in the countries of Latin America showing in output of gold, nickel, and silver. Chile led the and Canada, as well as the Caribbean Islands, during 1998 are world in the production of copper, and Mexico led in the described in this regional summary.2 As with the United States, production of silver and strontium. Peru was third in world these other countries of the Western Hemisphere are endowed production of silver after Mexico and the United States. Brazil with a great diversity of minerals, comprising metals, industrial led in output of columbium and, although not the largest minerals, and fuel minerals. For several of these countries, the producer of iron ore, has been the leading exporter in recent mining, processing, and marketing of the mineral commodities years, as well as eighth largest steel producer in the world. In play significant roles in supporting their economies, in many the Western Hemisphere, Brazil and Canada were second and instances earning export revenues and foreign exchange reserves third largest producers of steel, respectively, after the United and offering business opportunities via privatization of state-run States. Brazil was also the fourth ranking source of manganese corporations, direct acquisitions made by foreign and domestic in the world, followed in Latin America by Mexico. After investors, joint-venture projects (investment in equity), and debt Russia, Canada was the second largest world nickel producer, flows (credits). -

Anglo American1

STATEMENT BY UNITED KINGDOM NATIONAL CONTACT POINT FOR OECD GUIDELINES FOR MULTINATIONAL ENTERPRISES (NCP): ANGLO AMERICAN1 May 2008-08-04 1. A ‘specific instance’ relating to Anglo American plc was submitted to the NCP on 21 February 2002 under the auspices of the OECD Guidelines for Multinational Enterprises by Non-Government Organisation Rights and Accountability in Development (RAID). The OECD Guidelines for Multinational Enterprises 2. The Guidelines are recommendations that governments endorse and promote in relation to the behaviour of multinational enterprises. The Guidelines are voluntary principles and standards for responsible business conduct. They are the only comprehensive, multilaterally- endorsed code of conduct for multinational enterprises. 3. The Guidelines establish non-legally binding principles covering a broad range of issues in business ethics in the following areas of operation: general company policies, disclosure of information, employment and industrial relations, environment, combating bribery, consumer interests, responsible use of science and technology, competition and taxation. 4. The Guidelines are not legally binding but OECD governments and a number of non OECD members are committed to promoting their observance. The Guidelines are also supported by the business community and labour federations. In addition, a number of Non- Governmental Organisations are also heavily involved the work of the OECD Investment Committee responsible for monitoring and reviewing the Guidelines and are increasingly involved in overseeing the operation and promotion of the Guidelines. The complainants: 5. Rights and Accountability in Development (RAID). A Non-Government Organisation founded in 1997 that aims through its research to promote social and economic rights and improve corporate accountability. The company subject of the allegations Anglo American plc.