Office Market Review

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The “International” Skyscraper: Observations 2. Journal Paper

ctbuh.org/papers Title: The “International” Skyscraper: Observations Author: Georges Binder, Managing Director, Buildings & Data SA Subject: Urban Design Keywords: Density Mixed-Use Urban Design Verticality Publication Date: 2008 Original Publication: CTBUH Journal, 2008 Issue I Paper Type: 1. Book chapter/Part chapter 2. Journal paper 3. Conference proceeding 4. Unpublished conference paper 5. Magazine article 6. Unpublished © Council on Tall Buildings and Urban Habitat / Georges Binder The “International” Skyscraper: Observations While using tall buildings data, the following paper aims to show trends and shifts relating to building use and new locations accommodating high-rise buildings. After decades of the American office building being dominate, in the last twelve years we have observed a gradual but major shift from office use to residential and mixed-use for Tall Buildings, and from North America to Asia. The turn of the millennium has also seen major changes in the use of buildings in cities having the longest experience with Tall Buildings. Chicago is witnessing a series of office buildings being transformed into residential or mixed-use buildings, a phenomenon also occurring on a large scale in New York. In midtown Manhattan of New York City we note the transformation of major hotels into residential projects. The transformation of landmark projects in midtown New York City is making an impact, but it is not at all comparable to the number of new projects being built in Asia. When conceiving new projects, we should perhaps bear in mind that, in due time, these will also experience major shifts in uses and we should plan for this in advance. -

Structural Developments in Tall Buildings: Current Trends and Future Prospects

© 2007 University of Sydney. All rights reserved. Architectural Science Review www.arch.usyd.edu.au/asr Volume 50.3, pp 205-223 Invited Review Paper Structural Developments in Tall Buildings: Current Trends and Future Prospects Mir M. Ali† and Kyoung Sun Moon Structures Division, School of Architecture, University of Illinois at Urbana-Champaign, Champaign, IL 61820, USA †Corresponding Author: Tel: + 1 217 333 1330; Fax: +1 217 244 2900; E-mail: [email protected] Received 8 May; accepted 13 June 2007 Abstract: Tall building developments have been rapidly increasing worldwide. This paper reviews the evolution of tall building’s structural systems and the technological driving force behind tall building developments. For the primary structural systems, a new classification – interior structures and exterior structures – is presented. While most representative structural systems for tall buildings are discussed, the emphasis in this review paper is on current trends such as outrigger systems and diagrid structures. Auxiliary damping systems controlling building motion are also discussed. Further, contemporary “out-of-the-box” architectural design trends, such as aerodynamic and twisted forms, which directly or indirectly affect the structural performance of tall buildings, are reviewed. Finally, the future of structural developments in tall buildings is envisioned briefly. Keywords: Aerodynamics, Building forms, Damping systems, Diagrid structures, Exterior structures, Interior structures, Outrigger systems, Structural performance, Structural systems, Tall buildings Introduction Tall buildings emerged in the late nineteenth century in revolution – the steel skeletal structure – as well as consequent the United States of America. They constituted a so-called glass curtain wall systems, which occurred in Chicago, has led to “American Building Type,” meaning that most important tall the present state-of-the-art skyscraper. -

Bringing an Icon Into the Future: Willis Tower

CTBUH Research Paper ctbuh.org/papers Title: Bringing an Icon into the Future: Willis Tower Author: Stephen Katz, Senior Associate, Gensler Subjects: Architectural/Design Building Case Study Interior Design Keywords: Renovation Supertall Publication Date: 2019 Original Publication: 2019 Chicago 10th World Congress Proceedings - 50 Forward | 50 Back Paper Type: 1. Book chapter/Part chapter 2. Journal paper 3. Conference proceeding 4. Unpublished conference paper 5. Magazine article 6. Unpublished © Council on Tall Buildings and Urban Habitat / Stephen Katz Bringing an Icon into the Future: Willis Tower Abstract Stephen Katz Senior Associate Few buildings are as iconic as Willis Tower. Generations of Chicagoans have a collective memory Gensler of this building playing a role in their entire lives. Chicagoans mark time with Willis Tower, but Chicago, United States time has caught up with this aging supertall. The way the building engages with the city and its occupants needed a fresh approach. Understanding how Willis Tower is being reimagined Based in Gensler’s Chicago office, Stephen is a by new owners is crucial to the success of old and new supertall towers around the globe. This Senior Associate and Technical Director. Stephen paper examines the efforts of the design team as it created a new path forward for Willis Tower. has worked and lectured in the United States, Asia, and Europe and has authored papers about A new city-block-sized podium structure and substantial infrastructure improvements are part façade design and sustainability. Stephen is a of this work (see Figure 1), and the results have a dramatic effect on a piece of civic history while founding member of Gensler Enclosures; a group transforming the building into a destination for tenants and visitors alike. -

An Overview of Structural & Aesthetic Developments in Tall Buildings

ctbuh.org/papers Title: An Overview of Structural & Aesthetic Developments in Tall Buildings Using Exterior Bracing & Diagrid Systems Authors: Kheir Al-Kodmany, Professor, Urban Planning and Policy Department, University of Illinois Mir Ali, Professor Emeritus, School of Architecture, University of Illinois at Urbana-Champaign Subjects: Architectural/Design Structural Engineering Keywords: Structural Engineering Structure Publication Date: 2016 Original Publication: International Journal of High-Rise Buildings Volume 5 Number 4 Paper Type: 1. Book chapter/Part chapter 2. Journal paper 3. Conference proceeding 4. Unpublished conference paper 5. Magazine article 6. Unpublished © Council on Tall Buildings and Urban Habitat / Kheir Al-Kodmany; Mir Ali International Journal of High-Rise Buildings International Journal of December 2016, Vol 5, No 4, 271-291 High-Rise Buildings http://dx.doi.org/10.21022/IJHRB.2016.5.4.271 www.ctbuh-korea.org/ijhrb/index.php An Overview of Structural and Aesthetic Developments in Tall Buildings Using Exterior Bracing and Diagrid Systems Kheir Al-Kodmany1,† and Mir M. Ali2 1Urban Planning and Policy Department, University of Illinois, Chicago, IL 60607, USA 2School of Architecture, University of Illinois at Urbana-Champaign, Champaign, IL 61820, USA Abstract There is much architectural and engineering literature which discusses the virtues of exterior bracing and diagrid systems in regards to sustainability - two systems which generally reduce building materials, enhance structural performance, and decrease overall construction cost. By surveying past, present as well as possible future towers, this paper examines another attribute of these structural systems - the blend of structural functionality and aesthetics. Given the external nature of these structural systems, diagrids and exterior bracings can visually communicate the inherent structural logic of a building while also serving as a medium for artistic effect. -

Read More and Download The

Case Study: Vista Tower, Chicago A New View, and a New Gateway, for Chicago Abstract Upon completion, Vista Tower will become Chicago’s third tallest building, topping out the Lakeshore East development, where the Chicago River meets Lake Michigan. Juliane Wolf will participate in the Session 7C panel discussion High-Rise Occupying a highly visible site on a north- Design Drivers: Now to 2069, on Jeanne Gang Juliane Wolf south view corridor within the city’s grid, and in Wednesday, 30 October. Vista Tower is the subject of the off-site close proximity to the Loop, the river, and the program on Thursday, Authors city’s renowned lakefront park system, this 31 October. Jeanne Gang, Founding Principal and Partner Juliane Wolf, Design Principal and Partner mixed-use supertall building with a porous Studio Gang 1520 West Division Street base is simultaneously a distinctive landmark Chicago, IL 60642 USA at the scale of the city and a welcoming connector at the ground plane. Clad in a t: +1 773 384 1212 gradient of green-blue glass and supported by a reinforced concrete structure, the e: [email protected] studiogang.com tower is composed of an interconnected series of stacked, frustum-shaped volumes that move rhythmically in and out of plane and extend to various heights. The Jeanne Gang, architect and MacArthur Fellow, is the Founding Principal and Partner of Studio tower is lifted off the ground plane at the center, creating a key gateway for Gang, an architecture and urban design practice headquartered in Chicago with offices in New York, pedestrians accessing the Riverwalk from Lakeshore East Park. -

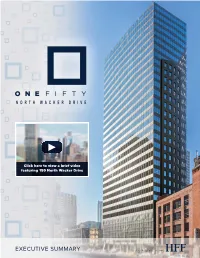

150 North Wacker Drive

Click here to view a brief video featuring 150 North Wacker Drive EXECUTIVE SUMMARY Holliday Fenoglio Fowler, L.P. (“HFF”) Holliday Fenoglio Fowler, L.P. (“HFF”) is pleased to present the sale of the 100% fee simple interest in 150 North Wacker Drive (the “Property”) located in the heart of Chicago’s Central Business District’s (“CBD”) most desirable submarket, the West Loop. The 31-story office tower is located one block east of Chicago’s Ogilvie Transportation Center on Wacker Drive – the home to many of Chicago’s most prestigious firms. The Property, consisting of 246,613 rentable square feet (“RSF”), is currently 91.9% leased and offers a significant mark to market opportunity in a best-in-class location on Wacker Drive. The Property is easily accessible via three major highways and the Chicago Transit Authority’s (“CTA”) transit and bus system, yet is still located in one of the most walkable areas of the city. Given the extensive common area renovations and recent leasing momentum, 150 North Wacker is a truly unique investment opportunity to acquire a rare asset with a premier Wacker Drive address and significant upside potential. KEY PROPERTY STATISTICS Location: 150 North Wacker Submarket: West Loop Total Rentable Area: 246,613 RSF Stories: 31 Percent Leased: 91.9% Weighted Average Lease Term: 4.0 Years Date Completed/Renovated: 1970/2002/2015 Average Floor Plates: 9,300 RSF Finished Ceiling Height: 8'9'' Slab to Slab Ceiling Height: 11'8'' Architect: Joel R. Hillman Parking: 134 Parking Stalls; Valet facilitates up to 160 Vehicles Transit Score: 100 Walk Score: 98 2 EXECUTIVE SUMMARY INVESTMENT HIGHLIGHTS NO. -

List of World's Tallest Buildings in the World

Height Height Rank Building City Country Floors Built (m) (ft) 1 Burj Khalifa Dubai UAE 828 m 2,717 ft 163 2010 2 Shanghai Tower Shanghai China 632 m 2,073 ft 121 2014 Saudi 3 Makkah Royal Clock Tower Hotel Mecca 601 m 1,971 ft 120 2012 Arabia 4 One World Trade Center New York City USA 541.3 m 1,776 ft 104 2013 5 Taipei 101 Taipei Taiwan 509 m 1,670 ft 101 2004 6 Shanghai World Financial Center Shanghai China 492 m 1,614 ft 101 2008 7 International Commerce Centre Hong Kong Hong Kong 484 m 1,588 ft 118 2010 8 Petronas Tower 1 Kuala Lumpur Malaysia 452 m 1,483 ft 88 1998 8 Petronas Tower 2 Kuala Lumpur Malaysia 452 m 1,483 ft 88 1998 10 Zifeng Tower Nanjing China 450 m 1,476 ft 89 2010 11 Willis Tower (Formerly Sears Tower) Chicago USA 442 m 1,450 ft 108 1973 12 Kingkey 100 Shenzhen China 442 m 1,449 ft 100 2011 13 Guangzhou International Finance Center Guangzhou China 440 m 1,440 ft 103 2010 14 Dream Dubai Marina Dubai UAE 432 m 1,417 ft 101 2014 15 Trump International Hotel and Tower Chicago USA 423 m 1,389 ft 98 2009 16 Jin Mao Tower Shanghai China 421 m 1,380 ft 88 1999 17 Princess Tower Dubai UAE 414 m 1,358 ft 101 2012 18 Al Hamra Firdous Tower Kuwait City Kuwait 413 m 1,354 ft 77 2011 19 2 International Finance Centre Hong Kong Hong Kong 412 m 1,352 ft 88 2003 20 23 Marina Dubai UAE 395 m 1,296 ft 89 2012 21 CITIC Plaza Guangzhou China 391 m 1,283 ft 80 1997 22 Shun Hing Square Shenzhen China 384 m 1,260 ft 69 1996 23 Central Market Project Abu Dhabi UAE 381 m 1,251 ft 88 2012 24 Empire State Building New York City USA 381 m 1,250 -

The-Hows-Whats-And-Wows-Of-Willis

There are enough impressive facts about the When you get back to your school, we hope Willis Tower to make even the most worldly your students will send us photos or write or among us say, “Wow!” So many things at the create artwork about their experiences and Willis Tower can be described by a share them with us (via email or the mailing superlative: biggest, fastest, and longest. But address at the end of this guide). there is more to the building than all these “wows”: 1,450 sky-scraping, cloud-bumping One photo will be selected as the “Photo of feet of glass and steel, 43,000 miles of the Day” and displayed on our Skydeck telephone cable, 25,000 miles of plumbing, monitors for all to see. Artwork and writing 4.56 million square feet of floor space and a will posted on bulletin boards in the view of four states. lunchroom area. We would also love to have you and your students post you Skydeck Behind the “wows” are lots of “hows” and Chicago photos to the Skydeck Chicago pages “whats” for you and your students to on Facebook, Instagram, and Twitter. explore. In this guide you will be introduced to the building—its beginnings as the Sears As you get ready for your trip, please call us Tower and its design, construction and place with any questions at (312) 875-9447. We aim in the pantheon of skyscrapers. Its name to make your visit your best school trip ever. was recently changed to the Willis Tower, proudly reflecting the name of the global insurance broker who makes the Tower its Chicago home. -

Office Markets & Public Policy

REAL ESTATE ISSUES Office Markets REAL ESTATE ISSUES & Public Policy This is the first book that looks at how offices and office markets in cities have Also available in the series changed over the last 30 years. It analyses the long-term trends and processes Markets & Institutions in Real within office markets, and the interaction with the spatial economy and the Estate & Construction planning of cities. It draws on examples around the world, and looking forward Ball Policy Public & Markets Office at the future consequences of information communication technologies and the 9781405110990 sustainability agenda, it sets out the challenges that now face investors. The Right to Buy: Analysis & Evaluation of a Housing Policy The traditional business centres of cities are losing their dominance to the brash Jones & Murie new centres of the 1980s and 1990s, as the concept of the central business 9781405131971 district becomes more diffuse. Edge cities, business space and office parks have Housing Markets & Planning Policy entered the vocabulary as offices have also decentralised. The nature and pace of Jones & Watkins changes to office markets set within evolving spatial structures of cities has had 9781405175203 implications for tenants and led to a demand for shorter leases. The consequence is a rethink of the traditional perception of property investment as a secure long Challenges of the Housing Economy: An International Perspective term investment, and this is reflected in reduced investment holding periods by Jones, White & Dunse financial institutions. 9780470672334 Office Markets & Public Policy analyses these processes and policy issues from an Towers of Capital: Office Markets & international perspective and covers: International Financial Services Lizieri l A descriptive and theoretical base encompassing an historical context, 9781405156721 a review of the fundamentals of the demand for and supply of the office Office Markets market and offices as an investment. -

Chicago Office Market

RESEARCH Q4 2020 Chicago Office Market Supply Outweighs Demand The Chicago Metro office market finished 2020 similar to most Current Conditions major U.S. markets that experienced the stress and ramifications – Metro vacancy increased to 18.4%, up 170 basis points from the of the pandemic. The market suffered the greatest loss in annual first quarter of 2020. absorption since 2009, with approximately 1.6 million square feet of negative absorption this year. The loss is primarily attributed to – The new Bank of America Tower at 110 North Wacker Avenue remote working, increased sublease space, layoffs and financial delivered this quarter. uncertainty. As a result, vacancy climbed to 18.4% in the fourth – Sublease availability surpassed the peak during the Great quarter of 2020, an increase of 170 basis points from the start of Recession of 2009. 2020. Average rental rates held steady at $30.32/SF across all – Sterling Bay sold McDonald’s Global HQ in Fulton Market classes, a 1.8% increase year over year, revealing landlords aren’t for $717/SF. budging on rates. Market Summary Central Business District Overview Current Prior Year Ago 12-Month Vacancy increased 130 basis points this quarter to an eight-year Quarter Quarter Period Forecast high of 15.6% in Downtown. This was largely due to the negative Total Inventory (SF) 242.1M 241.0M 239.0M 613,305 square feet of absorption and the sublease inventory that Vacancy Rate 18.4% 17.6% 16.9% has nearly doubled since the beginning of the pandemic. Despite Quarterly Net (844,558) (1.68M) 234,771 Absorption (SF) two consecutive quarters of negative absorption, year-end Average Asking $30.32 $30.02 $29.76 absorption remained positive, totaling 6,500 square feet. -

Les Numéros En Bleu Renvoient Aux Cartes

276 Index Les numéros en bleu renvoient aux cartes. 10 South LaSalle 98 American Writers Museum 68 35 East Wacker 88 Antiquités 170, 211 55 West Monroe Building 96 Aon Center 106 57th Street Beach 226 Apollo Theater 216 63rd Street Beach 226 Apple Michigan Avenue 134 75 East Wacker Drive 88 Aqua Tower 108 77 West Wacker Drive 88 Archbishop Quigley Preparatory Seminary 161 79 East Cedar Street 189 Architecture 44 120 North LaSalle 98 Archway Amoco Gas Station 197 150 North Riverside 87 Argent 264 181 West Madison Street 98 Arrivée 256 190 South LaSalle 98 Arthur Heurtley House 236 225 West Wacker Drive 87 Articles de voyage 145 300 North LaSalle Drive 156 Art Institute of Chicago 112 311 South Wacker Drive Building 83 Artisanat 78 321 North Clark 156 Art on theMART 159 A 325 North Wells 159 Art public 49 330 North Wabash 155 Arts and Science of the Ancient World: 333 North Michigan Avenue 68 Flight of Daedalus and Icarus 98 333 West Wacker Drive 87 Arts de la scène 40 360 CHICAGO 138 Astor Court 190 INDEX 360 North Michigan Avenue 68 Astor Street 189 400 Lake Shore Drive 158 AT&T Plaza 118 515 North State Building 160 Atwood Sphere 127 543-545 North Michigan Avenue 134 Auditorium Building 73 606, The 233 Auditorium Theatre 80 646 North Michigan Avenue 134 Autocar 258 730 North Michigan Avenue Building 137 Avion 256 860-880 North Lake Shore Drive 178 Axis Apartments & Lofts 179 875 North Michigan Avenue 138 900 North Michigan Shops 139 919 North Michigan Avenue 139 B 1211 North LaSalle Street 192 Baha’i House of Worship 247 1260 North Astor -

Signature Redacted Department of Civil and Environmental Engineering May 21, 2015

TRENDS AND INNOVATIONS IN HIGH-RISE BUILDINGS OVER THE PAST DECADE ARCHIVES 1 by MASSACM I 1TT;r OF 1*KCHN0L0LGY Wenjia Gu JUL 02 2015 B.S. Civil Engineering University of Illinois at Urbana-Champaign, 2014 LIBRAR IES SUBMITTED TO THE DEPARTMENT OF CIVIL AND ENVIRONMENTAL ENGINEERING IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF MASTER OF ENGINEERING IN CIVIL ENGINEERING AT THE MASSACHUSETTS INSTITUTE OF TECHNOLOGY JUNE 2015 C2015 Wenjia Gu. All rights reserved. The author hereby grants to MIT permission to reproduce and to distribute publicly paper and electronic copies of this thesis document in whole or in part in any medium now known of hereafter created. Signature of Author: Signature redacted Department of Civil and Environmental Engineering May 21, 2015 Certified by: Signature redacted ( Jerome Connor Professor of Civil and Environmental Engineering Thesis Supervisor Accepted bv: Signature redacted ?'Hei4 Nepf Donald and Martha Harleman Professor of Civil and Environmental Engineering Chair, Departmental Committee for Graduate Students TRENDS AND INNOVATIONS IN HIGH-RISE BUILDINGS OVER THE PAST DECADE by Wenjia Gu Submitted to the Department of Civil and Environmental Engineering on May 21, 2015 in Partial Fulfillment of the Degree Requirements for Master of Engineering in Civil and Environmental Engineering ABSTRACT Over the past decade, high-rise buildings in the world are both booming in quantity and expanding in height. One of the most important reasons driven the achievement is the continuously evolvement of structural systems. In this paper, previous classifications of structural systems are summarized and different types of structural systems are introduced. Besides the structural systems, innovations in other aspects of today's design of high-rise buildings including damping systems, construction techniques, elevator systems as well as sustainability are presented and discussed.