Chicago Office Market

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

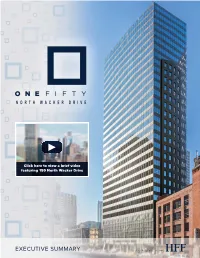

150 North Wacker Drive

Click here to view a brief video featuring 150 North Wacker Drive EXECUTIVE SUMMARY Holliday Fenoglio Fowler, L.P. (“HFF”) Holliday Fenoglio Fowler, L.P. (“HFF”) is pleased to present the sale of the 100% fee simple interest in 150 North Wacker Drive (the “Property”) located in the heart of Chicago’s Central Business District’s (“CBD”) most desirable submarket, the West Loop. The 31-story office tower is located one block east of Chicago’s Ogilvie Transportation Center on Wacker Drive – the home to many of Chicago’s most prestigious firms. The Property, consisting of 246,613 rentable square feet (“RSF”), is currently 91.9% leased and offers a significant mark to market opportunity in a best-in-class location on Wacker Drive. The Property is easily accessible via three major highways and the Chicago Transit Authority’s (“CTA”) transit and bus system, yet is still located in one of the most walkable areas of the city. Given the extensive common area renovations and recent leasing momentum, 150 North Wacker is a truly unique investment opportunity to acquire a rare asset with a premier Wacker Drive address and significant upside potential. KEY PROPERTY STATISTICS Location: 150 North Wacker Submarket: West Loop Total Rentable Area: 246,613 RSF Stories: 31 Percent Leased: 91.9% Weighted Average Lease Term: 4.0 Years Date Completed/Renovated: 1970/2002/2015 Average Floor Plates: 9,300 RSF Finished Ceiling Height: 8'9'' Slab to Slab Ceiling Height: 11'8'' Architect: Joel R. Hillman Parking: 134 Parking Stalls; Valet facilitates up to 160 Vehicles Transit Score: 100 Walk Score: 98 2 EXECUTIVE SUMMARY INVESTMENT HIGHLIGHTS NO. -

Les Numéros En Bleu Renvoient Aux Cartes

276 Index Les numéros en bleu renvoient aux cartes. 10 South LaSalle 98 American Writers Museum 68 35 East Wacker 88 Antiquités 170, 211 55 West Monroe Building 96 Aon Center 106 57th Street Beach 226 Apollo Theater 216 63rd Street Beach 226 Apple Michigan Avenue 134 75 East Wacker Drive 88 Aqua Tower 108 77 West Wacker Drive 88 Archbishop Quigley Preparatory Seminary 161 79 East Cedar Street 189 Architecture 44 120 North LaSalle 98 Archway Amoco Gas Station 197 150 North Riverside 87 Argent 264 181 West Madison Street 98 Arrivée 256 190 South LaSalle 98 Arthur Heurtley House 236 225 West Wacker Drive 87 Articles de voyage 145 300 North LaSalle Drive 156 Art Institute of Chicago 112 311 South Wacker Drive Building 83 Artisanat 78 321 North Clark 156 Art on theMART 159 A 325 North Wells 159 Art public 49 330 North Wabash 155 Arts and Science of the Ancient World: 333 North Michigan Avenue 68 Flight of Daedalus and Icarus 98 333 West Wacker Drive 87 Arts de la scène 40 360 CHICAGO 138 Astor Court 190 INDEX 360 North Michigan Avenue 68 Astor Street 189 400 Lake Shore Drive 158 AT&T Plaza 118 515 North State Building 160 Atwood Sphere 127 543-545 North Michigan Avenue 134 Auditorium Building 73 606, The 233 Auditorium Theatre 80 646 North Michigan Avenue 134 Autocar 258 730 North Michigan Avenue Building 137 Avion 256 860-880 North Lake Shore Drive 178 Axis Apartments & Lofts 179 875 North Michigan Avenue 138 900 North Michigan Shops 139 919 North Michigan Avenue 139 B 1211 North LaSalle Street 192 Baha’i House of Worship 247 1260 North Astor -

ACTIVE PLA PROJECTS • One Chicago Square

ACTIVE PLA PROJECTS • One Chicago Square (Chicago, State, Superior, Dearborn) (Power) 2019 • 3/Eleven Chicago 301-33 West Illinois, Chicago(Power) 2016 • 10-30 South Wacker (Lendlease) 2018 • 105 North May (Skender) 2018 • 110 North Wacker (Office Building) (Clark) 2017 • 178 West Randolph – Courtyard Marriott (Pepper) 2020 • 210 North Carpenter ((Leopardo) 2017 • 243 East Ontario (18 Story Hotel) (AECOM) 2017 • 311 West Monroe (15 Story Office Bldg.) (Leopardo) 2018 • 312 North Carpenter (LG Construction) 2016 • 320 South Canal (Clark Construction) 2019 • 333 North Green (19 Story Office Bldg. & Parking) (Power) 2018 • 345 North Morgan (11 Story Office Blg.) (Skender) 2020 • 403 North Wabash (17 Story – Condos) (McHugh) 2017 • 448 North LaSalle (13 Story office building) (Lendlease) 2019 • 633 West North Avenue (11 Story Apartment Bldg.) (Power) 2018 • 717 South Clark (31 Story Apartment Bldg.) (Lendlease) 2019 • 740 North Aberdeen (12 Story Apartment Bldg.) (McHugh) 2019 • 800 West Fulton Market (19 Story Office Bldg.) (Lendlease) 2019 • 840 South Canal (Data Center) (Clune Construction) 2018 • 845 West Madison (Lendlease) 2018 • 949 West Dakin (Apartment Development) (Leopardo) 2020 • 955 East 131st/Altgeld Gardens (Comm./Library Facility) (ALL Masonry) 2019 • 1000M (1000 South Michigan Avenue – Mixed Use High Rise) (McHugh) 2020 • 1100 West Fulton (5 Story Building/Renovation) (Skender) 2019 • 1200 South Indiana (McHugh) 2017 • 1313 West Morse (8 Story Mixed Use) (Pepper) 2017 • 1326 South Michigan (500 Unit Apt. Bld.) (Walsh) 2017 • 1375 West Fulton Office Building (Power) 2019 • 1515 West Webster (4 Story Shell & Core Office Bldg.)(Power) 2016 • 1550 North Clark (10 story condo) (Power) 2018 • 3501 South Pulaski (warehouse & distribution center/Hilco) 2018 • Advocate South Suburban Hospital Procedural Ctr. -

Morton Salt Company Warehouse Complex 1357 North Elston Avenue

PRELIMINARY SUMMARY OF INFORMATION SUBMITTED TO THE COMMISSION ON CHICAGO LANDMARKS IN FEBRUARY 2021 MORTON SALT COMPANY WAREHOUSE COMPLEX 1357 NORTH ELSTON AVENUE CITY OF CHICAGO Lori E. Lightfoot, Mayor Department of Planning and Development Maurice D. Cox, Commissioner The Commission on Chicago Landmarks, whose nine members are appointed by the Mayor and City Council, was established in 1968 by city ordinance. The Commission is responsible for recommending to the City Council that individual building, sites, objects, or entire districts be designated as Chicago Landmarks, which protects them by law. The Commission is staffed by the Chicago Department of Planning and Development, Historic Preservation Division, City Hall, 121 North LaSalle Street, Room 1000, Chicago, IL 60602; (312-744-3200) phone; web site: www.cityofchicago.org/landmarks This Preliminary Summary of Information is subject to possible revision and amendment during the designation process. Only language contained within the final landmark designation ordinance as approved by City Council should be regarded as final. CONTENTS Location Map 2 Location, Description, and Construction of the Morton Salt Company Warehouse Complex 3 Location 3 Description 3 Construction 6 The Morton Salt Complex and the Production Shed Building Type 8 History of Salt Production in the United States 12 History of the Morton Salt Company 14 Joy Morton (1855-1934) 14 Joy Morton & Company: 1886-1910 14 The Morton Salt Company: 1910 to 1965 16 Later History: 1965 to 2015 21 Morton Salt and De-icing for Wintertime Road Safety 21 Architects Graham, Anderson, Probst & White 24 Criteria for Designation 28 Significant Historical and Architectural Features 32 Bibliography 34 MORTON SALT COMPANY WAREHOUSE COMPLEX 1357 NORTH ELSTON AVENUE DATE OF CONSTRUCTION: 1929-1930 ARCHITECT: GRAHAM, ANDERSON, PROBST & WHITE The Morton Salt Company Warehouse Complex on Elston Avenue is one of the most iconic industrial sites along the North Branch of the Chicago River. -

Office Market Review

METROPOLITAN CHICAGO Office Market Review MID-YEAR 2020 To our valued customers, partners and future clients… There’s a moment in the middle of JRR Tolkien’s “The Hobbit” when the protagonist Bilbo and his traveling companions become frustrated while hiking through the seemingly endless Mirkwood Forest. The group nominates Bilbo to climb a tall tree to have a look around. Poking his head above the treetops, he sees nothing but green trees in every direction. Despondent, he climbs back down to tell everyone the unfortunate news. “Actually,” Tolkien writes, “they were not far off from the edge of the forest…the tree he had climbed, though it was tall in itself, was standing near the bottom of a wide valley, so that from its top the trees seemed to swell up all round like the edges of a great bowl, and he could not expect to see how far the forest lasted.” It's always hard to have a clear perspective from the middle of a situation, or draw conclusions with incomplete data. That may be a strange message coming from a Market Report intended to provide that bigger picture – but it’s also hopefully a reminder that we can’t ever possibly know everything, and only with the benefit of hindsight will we fully understand the twists, turns and challenges of 2020. Businesses and building owners are implementing best practices to operate safely and efficiently, strategizing the most effective way for employees to safely inhabit their workplaces. A similar situation is apparent as school districts across the country contemplate their back-to-school plans. -

THE GEORGES Shaping Chicago’S Skyline Father/Daughter Team Is Respected for Their Honesty, Integrity and Hard Work

JANUARY 2019 LEADING LAWYERS MAGAZINE REAL ESTATE, CONSTRUCTION & ENVIRONMENTAL EDITION THE TOP REAL ESTATE, CONSTRUCTION, ENVIRONMENTAL, AGRICULTURE, ENERGY, PUBLIC FINANCE AND PUBLIC UTILITIES LAWYERS IN ILLINOIS THE GEORGES Shaping Chicago’s Skyline Father/daughter team is respected for their honesty, integrity and hard work FEATURING: ARNIE MALK SARAH SHAW TOM BOYLAN JEFF YOUNGERMAN PAUL KELLEY AS WELL AS 16 OTHERS AND TOP 10 & 100 LISTS ALSO, EMERGING LAWYERS PRACTICING REAL ESTATE- RELATED AREAS OF LAW LEADINGLAWYERS.COM AKERMAN LLP THE Navigating Their Clients Through the GEORGES Complexities of Urban Redevelopment by Mike Bailey In the bewildering world of urban the redevelopment business. developments in the country and what we redevelopment, one Chicago law firm has a “Our company has used Jack George for consider ‘a village in the heart of the city.’ demonstrated track record of getting a project over the past 20 years,” says Joel Carlins, co- “We also are currently developing Vista, over the finish line. That consistent and CEO of Magellan Development. “I am a which will be the third tallest residential reliable performance is not achieved by guile, developer and an attorney since 1960. Our development in Chicago consisting of 101 but by adherence to a set of principles and a company has retained Jack for virtually all of stories, all of which have had the assistance reputation for honesty. our development in the city of Chicago. Several of Jack, with respect to various requirements It has taken years, but Jack George and have had a number of complexities, which were including all zoning and most governmental his daughter and protégé, Meg, have helped uncommon to most of our past developments. -

Lobbyist Data - Clients

Lobbyist Data - Clients Year CLIENT_ID NAME ADDRESS_1 2020 2386215978 SERVICENOW 2225 LAWSON 2020 758020543 JOINT CIVIC COMMITTEE OF ITALIAN 3800 DIVISION STREET AMERICANS 2020 3083112841 EDUCATORS FOR EXCELLENCE 351 W. HUBBARD STREET 2020 867465402 CAPITAL ONE FINANCIAL CORPORATION 1717 E. CARY STREET 2020 3078620549 ATRIUM MALL, LLC 7 BULLFINCH PLACE 2020 4087680836 CED FOOD LLC 230 W. AVENUE 26 2020 257472130 CHANDLER CONDOMINIUM ASSOCIATION 450 E WATERSIDE DRIVE 2020 4276518099 CHICAGO ASHLAND WEBSTER, LLC STATE FARM INSURANCE COMPANIES 2020 4219481870 TRACY BAIM AND MARCY BAIM 1900 SOUTH PRAIRIE AVENUE 2020 641249032 SOUTHERN WISCONSIN BANCSHARES 1629 W. COLONIAL PARKWAY CORPORATION 2020 3441035479 YESHIVA GEDOLA OF THE MIDWEST 333 W WACKER 2020 3965667581 SOUTH CHICAGO PACKING CO 945 W 38TH ST. 2020 1091448180 MIDWAY TECHNOLOGY CENTRE OWNER 96 FRENEAU AVE LLC 2020 3084486012 GOOGLE LLC AND ITS AFFILIATES C/O 28 LIBERTY SHIP WAY, SUITE 2815 2020 286906209 NEUTRON HOLDINGS, INC DBA LIMEBIKE 80 M STREET SE 2020 407051315 ASHLEY WENDELA AND BRENDAN 816 N MAY ST METZGER 2020 819549338 ESSENTIAL HOUSING CHICAGO 1101 W. MONROE STREET, 2ND FLOOR 2020 2821932813 LINCOLN PROVISION, INC. 824 WEST 38TH PLACE Page 1 of 783 09/24/2021 Lobbyist Data - Clients ADDRESS_2 CITY STATE ZIP SANTA CLAIRE CA 95054 STONE PARK IL 60165 SUITE 805 CHICAGO IL 60654 RICHMOND VA 23223 SUITE 500 BOSTON MA 02114 LOS ANGELES CA 90031 CHICAGO IL 60601 ONE STATE FARM PLAZA, A-3 BLOOMINGTON IL 61710-0001 CHICAGO IL 60616 INVERNESS IL 60067 #2000 CHICAGO IL 60606 CHICAGO -

Chicago Venue Portfolio

CHICAGO2015 VENUE PORTFOLIO 1932 W. LAKE STREET CHICAGO, IL 60612 [email protected] 773.880.8044 PARAMOUNTEVENTSCHICAGO.COM Paramount Events is ready to help you plan a spectacular event with a delicious SET menu, but to truly make an impact, the perfect backdrop is absolutely essential. THE We have connections at some of the best venues in Chicago, including The Smith on Lake, our own private space that guarantees dedicated service and personalized attention. SCENE You’re welcome to explore the following pages, but don’t forget – we’re here for you! We know every location inside and out and will be happy to offer our suggestions as a guide. ENJOY! TABLE OF 19th Century Club 1 Garfield Park Conservatory 43 Park West 86 1st Ward at Chop Shop 2 Glessner House Museum 44 Parliament 87 CONTENTS 345 North 3 Goodman Theatre 45 Peggy Notebaert Nature Museum 88 360 Chicago 4 Harold Washington Library Center 46 Pittsfield Building 89 63rd Street Beach House 5 Harris Theatre 47 Pleasant Home 90 A New Leaf 6 Highland Park Community House 48 Portfolio Annex 91 Anita Dee Charters 7 Hilton | Asmus Contemporary 49 Prairie Production 93 Aragon Ballroom 8 Hinsdale Community House 50 Primitive Art 94 Artifact Events 9 Humboldt Park & Boat House 51 Pritzker Military Museum & Library 95 Auditorium Theatre 10 Ida Noyes Hall at University of Chicago 52 Promontory Point 96 Bentley Gold Coast 12 Ignite Glass Studios 53 Ravenswood Event Center 97 Berger Park 13 International House at University of Chicago 54 Redmoon Theater 98 Beth-El 14 International -

Chicago Venue Portfolio

CHICAGO VENUE PORTFOLIO 1750 WEST LAKE STREET – CHICAGO, ILLINOIS 60612 [email protected] – 773.880.8044 – PARAMOUNTEVENTSCHICAGO.COM Paramount Events is ready to help you plan a spectacular event with a delicious SET THE menu, but to truly make an impact, the perfect backdrop is absolutely essential. SCENE We have connections at some of the best venues in Chicago, including The Lakewood and HighGround, our own private spaces that guarantee dedicated service and personalized attention. You’re welcome to explore the following pages, but don’t forget – we’re here for you! We know every location inside and out and will be happy to offer our suggestions as a guide. ENJOY! TABLE OF CONTENTS 360 Chicago 4 Columbus Park Refectory 36 Loft Lucia 70 Serosun Farms 103 63rd Street Beach House 5 Creativo Loft 37 Loft on Lake 71 South Shore Cultural Center 104 AmazingSpace@625 6 DeskLabs 38 Maggie Daley Park 72 Stan Mansion 105 American writers Museum 7 DL Loft 39 Mars Gallery 73 The Arbory 106 Anita Dee Charters 8 Dl studio 40 Merchandise Mart 74 The Athletico Center 107 Aragon Ballroom 9 Douglas Park Cultural & Community Center 41 Millennium Park Choral Room 75 The Geraghty 108 Artifact Events 10 Elawa Farm 42 Millennium Park Harris Theater The Joinery 109 Auditorium Theatre of Roosevelt University 11 Epiphany Arts Center 43 Rooftop Terrace 76 The Laugh Factory 110 B’nai Jehoshua Beth Elohim (BJBE) 12 Exchange 312 44 Millennium Park Jay Pritzker Pavilion Stage 77 The Library 111 Bentley Gold Coast 13 Fairlie 45 Moonlight Studios 78 The -

Cso Ambrosetti Mar09.Pdf

A B C D E F G Application Industry Employer Website Job/Internship Location Corporate Office Address Notes 1 Deadline 2 Advertising 24/7 Real Media http://www.24-7media.de/ NYC N/A 132 W. 31st Street, Floor 9, New York, NY 10001 N/A 360i produces integrated digital marketing campaigns for large brand advertisers with a foundation in Advertising 360i 3 http://www.360i.com/ NYC N/A 28 West 23rd St, 6th Floor, New York, NY 10010 search marketing. 4 Advertising 50,000feet, Inc. www.50000feet.com CHI N/A 1700 W. Irving Park Rd. Chicago IL 60613 Strategy, Marketing, Interactive, and Corporate. Founded in 1981, Abelson Taylor has grown to become the largest, independently pwned full-service Advertising Abelson Taylor, Inc. 5 http://www.abelsontaylor.com/ Chicago N/A 33 w. Monroe Street, Chicago, IL 60603 healthcare advertising agency in the world. For over 20 years, we have been commited to advance our clients' presence in the Latino market and Advertising Acento 6 http://www.acento.com/ Chicago N/A 900 W. Jackson Chicago IL 60607 further theory brand equity with the best creative solutions. Each year, one student who shows promise and a desire to gain experience in the media aspect of advertising will be selected to complete a 10-week summer internship at Adweekmagazine's Advertising American Advertising Federation headquarters in New York. The intern will work in the marketing department and will be exposed to various projects that support advertising sales. The intern will be provided with a $4,500 stipend to 7 http://www.aaf.org/default.asp?id=148 DC 6-Feb 1101 Vermont Avenue NW, Suite 500, Washington DC 20005 cover transportation costs, food, lodging and other living expenses during the 10-week internship. -

In Chicago Cultural Hits & Urban Adventures

B TRAVEL PROFESSIONALS GUIDE CHOOSECHICAGO.COM 72 HOURS IN CHICAGO CULTURAL HITS & URBAN ADVENTURES SUGGESTED SEASONAL ITINERARIES CHICAGO FOR SENIOR & STUDENT GROUPS | CHICAGO MUST-SEES OPEN DAILY GLASS Oct - Feb: 10am - 8pm* BALCONIES Mar - Sept: 9am - 10pm* PUT YOU *Plus extended Saturday hours 1,353 FEET & Call 312.875.9696 103 FLOORS to book your groups today! OVER THE WINDY • Free Bus Parking CITY! • Free Escort Tickets • Early Group Entry WILLIS TOWER 103rd floor • 233 S Wacker Dr. • Chicago, IL 60606 CHICAGO SKYLINE WELCOME TO CHICAGO Welcome to the city that feels like home. More than 55 million visitors experienced Chicago’s authentic hospitality and cultural and culinary diversity last year. That was a goal I had hoped we would reach by the end of the decade. Thanks to you and millions like you, we did — three years early. Speaking of diversity, it’s everywhere you look. More than 100 countries are represented in Chicago’s 77 communities, making it easy to sample the culture and cuisine of many nations — all within easy walking or riding distance. Chicago’s equally diverse food scene is world renowned, with Michelin-starred and James Beard Award-winning restaurants all over the city. NAVY PIER Chicago’s cultural diversity is enhanced by its more than 250 theaters, 56 museums, 225 music venues and more than 700 public works of art, many of which are found in or near Chicago’s nearly 600 parks. Add to that an iconic skyline along much of the city’s 26 miles of lakefront and it’s no wonder Condé Nast Traveler readers named Chicago the Best Big City in the U.S. -

The Rock Report Chicago Central Business District (CBD) Q4 2018

The Rock Report Chicago Central Business District (CBD) Q4 2018 New developments and office space trends are key Total RBA Average Estimated Gross Class components in the Chicago office market, playing a (RSF) Vacancy Rental Rates significant role in the increased vacancy rate within the CBD. A 56,219,708 13.8% $44.00 - $62.00/SF Through December 2018, Chicago’s CBD vacancy B 62,040,951 15.3% $35.00 - $43.00/SF rate increased by 39 basis points with six (6) new office building deliveries. Class A+ Trophy buildings in Chicago’s CBD are in the spotlight, generating C 14,784,979 12.7% $28.00 - $33.00/SF ferocious competition among users looking to occupy office space. If strong preleasing and demand for Class A Prospective Tenants that demand amenity-rich buildings persists, the development pipeline will spaces with abundant natural light in a continue to grow in 2019 to meet demand for this transit-oriented location have their eyes set on new product type. construction, while older Class B and C buildings seek to maintain occupancy by increasing Class A assets reported 2,111,989 of positive net concessions and adding amenities to their existing absorption in 2018, while Class B assets reported space. 631,028 of negative net absorption. Professional service firms continued the trend of densification in relocations and emerging technology firms continue At year-end, Trophy buildings recorded a 10.0% to credit their office space and environment as overall vacancy, while Class A stood at 13.8% and key components of the recruitment and retention Class B increased to 15.3% vacancy rate.