Public Transport Plan for Perth in 2031? 25 6.1 Short Term Perth PT Plan Funding Mechanisms

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Heritage Inventory

Heritage Inventory Central Perth Redevelopment Area March 2016 Page 1 // MRA Central Perth Heritage Inventory Page 2 // MRA Central Perth Heritage Inventory Central Perth Heritage Inventory Contents 1. INTRODUCTION pg 4 2. MANAGEMENT OF PLACES IN THE HERITAGE INVENTORY pg 7 3. THEMATIC HISTORY OF THE CENTRAL PERTH REDEVELOPMENT AREA pg 10 4. CLAISEBOOK VILLAGE PROJECT AREA pg 17 5. EAST PERTH POWER STATION PROJECT AREA pg 25 6. NEW NORTHBRIDGE PROJECT AREA pg 31 7. RIVERSIDE PROJECT AREA pg 117 8. PERTH CITY LINK PROJECT AREA pg 135 9. PERTH CULTURAL CENTRE PROJECT AREA pg 143 10. ELIZABETH QUAY PROJECT AREA pg 261 11. IMAGE REFERENCES pg 279 Page 3 // MRA Central Perth Heritage Inventory 1. Introduction THE INVENTORY The Metropolitan Redevelopment Authority (the MRA) is responsible for the urban renewal of the Central Perth Redevelopment Area (the Redevelopment Area) and proposes to recognise and afford protective measures to those places that have cultural heritage significance. The Central Perth Redevelopment Scheme (the Scheme) empowers the MRA to compile and maintain a list of Heritage Places and Precincts, called a Heritage Inventory (HI). The Central Perth HI has been developed in accordance with the provisions of the Heritage of Western Australia Act 1990, which requires all Local Governments to compile an inventory of heritage places as the foundation of sound local heritage planning. As MRA assumes responsibility as the planning authority within the Redevelopment Area, the MRA is acknowledging its role and responsibilities in “recognising, promoting and protecting” the cultural heritage that falls under its jurisdiction, as articulated in the State Cultural Heritage Policy. -

MIGRATION STORIES Northbridge Walking Trail

017547PD MIGRATION STORIES Northbridge Walking Trail 1 5 8 Start at State Library Francis Street entrance. The Cross Roe Street at the lights and walk west. You’ll Continue along James Street to Russell Square. Perth railway station and bus stations are close to find the Northbridge Chinese Restaurant. Walk through the entrance and up Moon Chow the Library. *PUBLIC TOILETS Promenade to the central rotunda. Moon Chow, a carpenter, is Western Australia is rich with stories of people considered the first Chinese person This square was named for Lord John Russell, the who have migrated here. The State Library shares to settle in Western Australia in Secretary of State and Colonies, 1839, and later minutes minutes these stories and records the impact of migration. 1829. Chinese people migrating to Prime Minister of Great Britain. It became known 30 3 Perth came as labourers and farm as Parco dei Sospire, ‘the park of sighs’ referring lking Trail lking Wa dge Northbri slwa.wa.gov.au/our-services/teachers minutes hands and ran businesses such as to the homesick Italian migrants who would AREAS WHERE GROUPS 15 market gardens, laundries, bakeries, meet here. ATION STORIES ATION MIGR CAN REST AND PLAY furniture factories, tailor shops and What do you think they would talk about? 2 grocery stores. In 1886, Western Walk through to the Perth Cultural Centre, head Australia introduced an Act to 9 west towards William Street. Stop on the corner regulate and restrict the immigration BA1483 Russell Square of William and James streets. of Chinese people. Rotunda. slwa.info/teacher-resources slwa.info/2011-census The history of This park was Northbridge 6 designed by head has been formed by Keep walking west until you see the Chinese gardener for the minutes gates. -

Public Interest Assessment

Form 2A Public Interest Assessment Where a Public Interest Assessment is required this form can be completed and lodged with the licensing authority. Applicants should ensure they read the Director of Liquor Licensing’s policy - Public Interest Assessment prior to completing this form. PART 1 - Application details 1.1 Applicant name: Potent Group Pty Ltd 1.2 Application for: Hotel (inc Hotel Restricted) New licence Removal of licence Tavern (inc Tavern Restricted) New licence Removal of licence Small Bar New licence Removal of licence Liquor Store New licence Removal of licence Nightclub New licence Removal of licence Special Facility New licence Removal of licence Restaurant New licence Removal of licence Club New licence Club Restricted New licence X Extended Trading Permit x Ongoing Hours Liquor Without a Meal (more than 120 persons) Other 1.3 Premises name: Wow Karaoke 1.4 Address of proposed premises: 21B Lake Street Northbridge WA 6003 Form 2A Page 1 Form 2A Introduction The public interest test is based on the principle that licensed premises must operate within the interests of the local community. The Butterworth’s Australian Legal Dictionary defines the term “public interest” as: “an interest in common to the public at large or a significant portion of the public and which may, or may not involve the personal or propriety rights of individual people” The public interest provisions enable the licensing authority to consider a broad range of issues specific to each licence or permit application, and flexibility exists to assess each individual application on its merits. Each community is different and has individual characteristics. -

Perth's Urban Rail Renaissance

University of Wollongong Research Online Faculty of Engineering and Information Faculty of Engineering and Information Sciences - Papers: Part B Sciences 2016 Perth's urban rail renaissance Philip G. Laird University of Wollongong, [email protected] Follow this and additional works at: https://ro.uow.edu.au/eispapers1 Part of the Engineering Commons, and the Science and Technology Studies Commons Recommended Citation Laird, Philip G., "Perth's urban rail renaissance" (2016). Faculty of Engineering and Information Sciences - Papers: Part B. 277. https://ro.uow.edu.au/eispapers1/277 Research Online is the open access institutional repository for the University of Wollongong. For further information contact the UOW Library: [email protected] Perth's urban rail renaissance Abstract Over the past thirty five years, instead of being discontinued from use, Perth's urban rail network has been tripled in route length and electrified at 25,000 oltsv AC. The extensions include the Northern Suburbs Railway (with stage 1 opened in 1993 and this line reaching Butler in 2014), and, the 72 kilometre Perth Mandurah line opening in 2007. Integrated with a well run bus system, along with fast and frequent train services, there has been a near ten fold growth in rail patronage since 1981 when some 6.5 million passengers used the trains to 64.2 million in 2014-15. Bus patronage has also increased. These increases are even more remarkable given Perth's relatively low population density and high car dependence. The overall improvements in Perth's urban rail network, with many unusual initiatives, have attracted international attention. -

PERTH CITY LINK BUS MASTER PLAN New Underground Wellington Street Bus Station March 2010

PERTH CITY LINK BUS MASTER PLAN New Underground Wellington Street Bus Station March 2010 kconnecting www.perthcitylink.wa.gov.au In 2009, the Public Transport Authority of Western Australia (PTA) undertook planning for the Perth City Link Rail and Bus Projects. During this time the project was known as ‘The HUB’. In March 2010, the PTA’s ‘HUB’ project and the East Perth Redevelopment Authority’s ‘Link’ project were joined to form the ‘Perth City Link’ Project. This Master Plan outlines the PTA’s Bus project works for the Perth City Link Project. Throughout this document ‘Perth City Link Bus’ will be referred to as ‘The HUB’. THE HUB : Master Plan for New Underground Wellington Street Bus Station THE HUB Master Plan Part 2: New Underground Wellington Street Bus Station March 2010 FINAL Latest version March 30, 2010. PRODUCED BY : Infrastructure Planning and Land Services Division Public Transport Authority of Western Australia Level 5 Public Transport Centre West Parade PERTH WA 6000 ISBN : 978‐0‐646‐51795‐7 Capital funding for this project is provided by the State of Western Australia and the City of Perth THE HUB : Master Plan for New Underground Wellington Street Bus Station 3.2.5. BUS PASSENGER SET‐DOWN ....................................................... 18 CONTENTS 3.2.6. BUS LAYOVER .............................................................................. 21 FOREWORD ................................................................................................ v 3.2.7. TOTAL BUS SPACE REQUIREMENTS ............................................ -

2002-03 WAGR Annual Report.Pdf

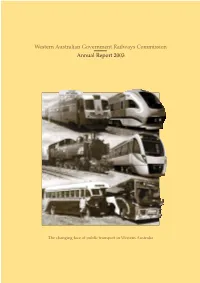

Western Australian Government Railways Commission Annual Report 2003 The changing face of public transport in Western Australia Cover Images Passing of an era. The original Prospector which was Prior to 1877, government regulation of railways launched in December 1971. was administered by the Colonial Secretary’s Office. Courtesy of Battye Library BA 369/EB-15 In 1877, a Director of Public Works was appointed New Prospector - Australia's newest and in the following year this position also acquired regional train, due to come into service the title of Commissioner of Railways, paving the in late 2003. way for the establishment of the Department of Photo: Danny Brennan, Motive Audio Visual Works and Railways. Suburban steam passenger train, In 1890, the Department of Works and Railways DM587, on its last day of regular service 4 October 1968. was split into two entities and the first State Photo: A.J. Tilley and the Australian Railway Government agency known as Western Australian Historical Society (W.A. Division) Government Railways (WAGR) was established. The new EMU (Electrical Multiple On 1 July 2003, the Public Transport Authority Unit) that will come into service on (PTA) was formed, amalgamating WAGR with the metropolitan network in late 2004. Transperth and School Bus Services. One of WAGR's South-West coach fleet based at Bunbury, 1946-47. The formation of the PTA marked the end of a long and rich history of Western Australian One of the fleet of 21 new regional Government agencies that included ‘railways’ as coaches introduced into service in 2003. part of their title. -

2004–05 Budget

2004–05 BUDGET BUDGET STATEMENTS Volume 3 PRESENTED TO THE LEGISLATIVE ASSEMBLY ON 6 MAY 2004 Budget Paper No.2 2004–05 Budget Statements (Budget Paper No. 2 Volume 3) © Government of Western Australia Excerpts from this publication may be reproduced, with appropriate acknowledgement, as permitted under the Copyright Act. For further information please contact: Department of Treasury and Finance 197 St George’s Terrace Perth WA 6000 Telephone:+61 8 9222 9222 Facsimile: +61 8 9222 9117 Website: http://ourstatebudget.wa.gov.au Published May 2004 John A. Strijk, Government Printer ISSN 1448–2630 BUDGET 2004-05 BUDGET STATEMENTS TABLE OF CONTENTS Volume Page Chapter 1: Consolidated Fund Expenditure Estimates ............... 1 1 Chapter 2: Net Appropriation Determinations ............................ 1 23 Chapter 3: Agency Information in Support of the Estimates ...... 1 33 PART 1 – PARLIAMENT Parliament .......................................................................................... 1 37 Parliamentary Commissioner for Administrative Investigations ....... 1 54 PART 2 - PREMIER; MINISTER FOR PUBLIC SECTOR MANAGEMENT; FEDERAL AFFAIRS; SCIENCE; CITIZENSHIP AND MULTICULTURAL INTERESTS Premier and Cabinet........................................................................... 1 67 Royal Commission Into Whether There Has Been Any Corrupt or Criminal Conduct by Western Australian Police Officers ........... 1 106 Anti-Corruption Commission............................................................. 1 110 Governor's Establishment.................................................................. -

Western Australian Government Railways Commission Annual Report 2003

Western Australian Government Railways Commission Annual Report 2003 The changing face of public transport in Western Australia Cover Images Passing of an era. The original Prospector which was Prior to 1877, government regulation of railways launched in December 1971. was administered by the Colonial Secretary’s Office. Courtesy of Battye Library BA 369/EB-15 In 1877, a Director of Public Works was appointed New Prospector - Australia's newest and in the following year this position also acquired regional train, due to come into service the title of Commissioner of Railways, paving the in late 2003. way for the establishment of the Department of Photo: Danny Brennan, Motive Audio Visual Works and Railways. Suburban steam passenger train, In 1890, the Department of Works and Railways DM587, on its last day of regular service 4 October 1968. was split into two entities and the first State Photo: A.J. Tilley and the Australian Railway Government agency known as Western Australian Historical Society (W.A. Division) Government Railways (WAGR) was established. The new EMU (Electrical Multiple On 1 July 2003, the Public Transport Authority Unit) that will come into service on (PTA) was formed, amalgamating WAGR with the metropolitan network in late 2004. Transperth and School Bus Services. One of WAGR's South-West coach fleet based at Bunbury, 1946-47. The formation of the PTA marked the end of a long and rich history of Western Australian One of the fleet of 21 new regional Government agencies that included ‘railways’ as coaches introduced into service in 2003. part of their title. -

Announcement Investment in an Office

ANNOUNCEMENT INVESTMENT IN AN OFFICE BUILDING IN PERTH, AUSTRALIA 1. INTRODUCTION The Board of Directors (the “Board”) of The Straits Trading Company Limited (the “Company”) wishes to announce that Straits Real Estate Pte. Ltd. (“SREPL”), its indirect subsidiary, through 45SGT Unit Trust, an indirect subsidiary of SREPL, has entered into a sale and purchase agreement with St Georges Terrace Real Estate Netherlands BV to acquire an office building located at 45 St Georges Terrace, Perth, Australia (the “Property”) (the “Acquisition”). 2. INFORMATION ON THE ACQUISITION 2.1 Information on the Property The Property is an 11-storey office building with two basement levels. Located in the main commercial thoroughfare of the Perth Central Business District, the Property is surrounded by high quality office buildings and in close proximity to numerous retail and dining amenities, including the Hay Street malls and the iconic Cathedral and Treasury Precinct. The Perth railway station, Perth underground station, Elizabeth Quay station, and Elizabeth Quay bus station are within walking distance of the Property. With the ongoing development of Elizabeth Quay less than 300 metres away, the Property is well positioned to benefit from the continuing rejuvenation of the city centre. 2.2 Rationale for the Acquisition The Company has previously articulated to shareholders its strategy of redeploying capital from its existing property portfolio of high quality, but low yielding investment properties into potentially higher return real estate opportunities via SREPL. The Acquisition is in line with this stated strategy. 2.3 Information on the Consideration The consideration for the Acquisition is approximately AUD54.2 million (approximately SGD55.7 million1), which will be funded by internal resources and bank borrowings, was arrived at on a willing-buyer and willing-seller basis, and taking into consideration the valuation of the Property. -

South West Metropolitan Railway Perth to Mandurah

South West Metropolitan Railway Perth to Mandurah Commissioner of Railways Report and recommendations of the Environmental Protection Authority Environmental Protection Authority Perth, Western Australia Bulletin 1102 July 2003 ISBN. 0 7307 6738 8 ISSN. 1030 - 0120 Assessment No. 1395 Summary and recommendations This report provides the Environmental Protection Authority’s (EPA’s) advice and recommendations to the Minister for the Environment and Heritage on the environmental factors relevant to the proposal to construct and operate the South West Metropolitan Railway from Perth to Mandurah. The proponent is the Commissioner of Railways. Section 44 of the Environmental Protection Act 1986 requires the EPA to report to the Minister for the Environment and Heritage on the environmental factors relevant to the proposal and on the conditions and procedures to which the proposal should be subject, if implemented. In addition, the EPA may make recommendations as it sees fit. Relevant environmental factors The EPA decided that the following environmental factors relevant to the proposal required detailed evaluation in the report: (a) Terrestrial flora; (b) Fauna; (c) Wetlands; (d) Noise and vibration – operations phase; (e) Surface water and groundwater quality; and (f) Visual amenity. There were a number of other factors which were very relevant to the proposal, but the EPA is of the view that the information set out in Appendix 3 provides sufficient evaluation. Conclusion The EPA has considered the proposal by the Commissioner of Railways to construct and operate the South West Metropolitan Railway from Perth to Mandurah. The EPA notes that portions of the roads and railways reserves that accommodate the proposal have been the subject of previous environmental assessments. -

Excursion Management Information

EXCURSION MANAGEMENT INFORMATION The following information has been compiled to assist in planning for your excursion to Perth Festival 2021. Name of Organisation Perth Festival Postal Address M418 The University of Western Australia Crawley, WA 6009 Phone Number 6488 2000 Email Address [email protected] Website Address perthfestival.com.au Contact Person Jenna Mathie, Producer – Connect PURPOSE OF THE EXCURSION Perth Festival presents world class events that showcase the very best artistry, performances and interpretations of text. An excursion to a Perth Festival event has the potential to develop students: • Ability to connect with curriculum content in new ways • Confidence in becoming innovative and creative artists and thinkers • Skills to critically engage with texts from Australia and other cultures • Engagement with a variety of learning styles • Communication skills, methodologies and awareness • Empathy and self-awareness to explore, depict and celebrate the human experience • Comprehension of texts through listening and viewing • Knowledge of how visual information contributes to the meanings created in texts • Artistic, aesthetic and cultural appreciation of art forms from past and contemporary contexts, including cross-cultural and multi-disciplinary events • Respect for, and knowledge of, the diverse purposes, traditions, histories and cultures of art making and critical response • Reflection on thinking and processes • Knowledge of methods used to apply and control elements, skills, techniques, processes, forms and styles of art making • Skills and techniques to actively analyse and create art • Understanding of the adaptation of texts for live performance • Understanding that languages are living ENVIRONMENT Perth Festival events take place in numerous venues around Perth, Crawley and Subiaco. -

ORDINARY COUNCIL MEETING M I N U T E S Table of Contents

ORDINARY COUNCIL MEETING M I N U T E S Table of Contents 1. DECLARATION OF OPENING / ANNOUNCEMENT OF VISITORS.................................................5 2. DISCLAIMER ...........................................................................................................................................5 3. ANNOUNCEMENTS FROM THE PRESIDING MEMBER ..................................................................5 3.1 Activities Report Mayor Best / Council Representatives ..................................................................5 3.2 Public Question Time ........................................................................................................................5 3.3 Audio Recording of Council meeting ................................................................................................5 4. ATTENDANCE.........................................................................................................................................6 4.1 Apologies ...........................................................................................................................................6 4.2 Approved Leave of Absence..............................................................................................................6 5. DECLARATION OF INTEREST .............................................................................................................6 6. PUBLIC QUESTION TIME......................................................................................................................6