Infrastructure Development: Experience and Policy Options for the Future

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Transportation History of the Philippines

Transportation history of the Philippines This article describes the various forms of transportation in the Philippines. Despite the physical barriers that can hamper overall transport development in the country, the Philippines has found ways to create and integrate an extensive transportation system that connects the over 7,000 islands that surround the archipelago, and it has shown that through the Filipinos' ingenuity and creativity, they have created several transport forms that are unique to the country. Contents • 1 Land transportation o 1.1 Road System 1.1.1 Main highways 1.1.2 Expressways o 1.2 Mass Transit 1.2.1 Bus Companies 1.2.2 Within Metro Manila 1.2.3 Provincial 1.2.4 Jeepney 1.2.5 Railways 1.2.6 Other Forms of Mass Transit • 2 Water transportation o 2.1 Ports and harbors o 2.2 River ferries o 2.3 Shipping companies • 3 Air transportation o 3.1 International gateways o 3.2 Local airlines • 4 History o 4.1 1940s 4.1.1 Vehicles 4.1.2 Railways 4.1.3 Roads • 5 See also • 6 References • 7 External links Land transportation Road System The Philippines has 199,950 kilometers (124,249 miles) of roads, of which 39,590 kilometers (24,601 miles) are paved. As of 2004, the total length of the non-toll road network was reported to be 202,860 km, with the following breakdown according to type: • National roads - 15% • Provincial roads - 13% • City and municipal roads - 12% • Barangay (barrio) roads - 60% Road classification is based primarily on administrative responsibilities (with the exception of barangays), i.e., which level of government built and funded the roads. -

Company Registration and Monitoring Department

Republic of the Philippines Department of Finance Securities and Exchange Commission SEC Building, EDSA, Greenhills, Mandaluyong City Company Registration and Monitoring Department LIST OF CORPORATIONS WITH APPROVED PETITIONS TO SET ASIDE THEIR ORDER OF REVOCATION SEC REG. HANDLING NAME OF CORPORATION DATE APPROVED NUMBER OFFICE/ DEPT. A199809227 1128 FOUNDATION, INC. 1/27/2006 CRMD A199801425 1128 HOLDING CORPORATION 2/17/2006 CRMD 3991 144. XAVIER HIGH SCHOOL INC. 2/27/2009 CRMD 12664 18 KARAT, INC. 11/24/2005 CRMD A199906009 1949 REALTY CORPORATION 3/30/2011 CRMD 153981 1ST AM REALTY AND DEVLOPMENT CORPORATION 5/27/2014 CRMD 98097 20th Century Realty Devt. Corp. 3/11/2008 OGC A199608449 21st CENTURY ENTERTAINMENT, INC. 4/30/2004 CRMD 178184 22ND CENTURY DEVELOPMENT CORPORATION 7/5/2011 CRMD 141495 3-J DEVELOPMENT CORPORATION 2/3/2014 CRMD A200205913 3-J PLASTICWORLD & DEVELOPMENT CORP. 3/13/2014 CRMD 143119 3-WAY CARGO TRANSPORT INC. 3/18/2005 CRMD 121057 4BS-LATERAL IRRIGATORS ASSN. INC. 11/26/2004 CRMD 6TH MILITARY DISTRICT WORLD WAR II VETERANS ENO9300191 8/16/2004 CRMD (PANAY) ASSOCIATION, INC. 106859 7-R REALTY INC. 12/12/2005 CRMD A199601742 8-A FOOD INDUSTRY CORP. 9/23/2005 CRMD 40082 A & A REALTY DEVELOPMENT ENTERPRISES, INC. 5/31/2005 CRMD 64877 A & S INVESTMENT CORPORATION 3/7/2014 CRMD A FOUNDATION FOR GROWTH, ORGANIZATIONAL 122511 9/30/2009 CRMD UPLIFTMENT OF PEOPLE, INC. (GROUP) GN95000117 A HOUSE OF PRAYER FOR ALL NATIONS, INC. CRMD AS095002507 A&M DAWN CORPORATION 1/19/2010 CRMD A. RANILE SONS REALTY DEVELOPMENT 10/19/2010 CRMD A.A. -

Art of Nation Building

SINING-BAYAN: ART OF NATION BUILDING Social Artistry Fieldbook to Promote Good Citizenship Values for Prosperity and Integrity PHILIPPINE COPYRIGHT 2009 by the United Nations Development Programme Philippines, Makati City, Philippines, UP National College of Public Administration and Governance, Quezon City and Bagong Lumad Artists Foundation, Inc. Edited by Vicente D. Mariano Editorial Assistant: Maricel T. Fernandez Border Design by Alma Quinto Project Director: Alex B. Brillantes Jr. Resident Social Artist: Joey Ayala Project Coordinator: Pauline S. Bautista Siningbayan Pilot Team: Joey Ayala, Pauline Bautista, Jaku Ayala Production Team: Joey Ayala Pauline Bautista Maricel Fernandez Jaku Ayala Ma. Cristina Aguinaldo Mercedita Miranda Vincent Silarde ALL RIGHTS RESERVED Apart from fair dealing for the purpose of research or review, as permitted under the copyright, this book is subject to the condition that it should not, by way of trade or otherwise, be lent, sold, or circulated in any form, without the prior permission in writing of the publisher. The scanning, uploading and distribution of this book via the Internet or via other means without the permission of the publisher is illegal and punishable by applied laws. ALL SONGS COPYRIGHT Joey Ayala PRINTED IN THE PHILIPPINES by JAPI Printzone, Corp. Text Set in Garamond ISBN 978 971 94150 1 5 TABLE OF CONTENTS i MESSAGE Mary Ann Fernandez-Mendoza Commissioner, Civil Service Commission ii FOREWORD Bro. Rolando Dizon, FSC Chair, National Congress on Good Citizenship iv PREFACE: Siningbayan: Art of Nation Building Alex B. Brillantes, Jr. Dean, UP-NCPAG vi ACKNOWLEDGEMENTS vii INTRODUCTION Joey Ayala President, Bagong Lumad Artists Foundation Inc.(BLAFI) 1 Musical Reflection: KUNG KAYA MONG ISIPIN Joey Ayala 2 SININGBAYAN Joey Ayala 5 PART I : PAGSASALOOB (CONTEMPLACY) 9 “BUILDING THE GOOD SOCIETY WE WANT” My Hope as a Teacher in Political and Governance Jose V. -

MUD CRAB a Report on the Seminar Convened in Surat Thani, Thailand, November 5-8, 1991 BAY of BENGAL PROGRAMME BOBP/REP/51 Brackishwater Culture GCP/RAS/ I 18/MUL

BOBP/REP/51 THE MUD CRAB A report on the Seminar convened in Surat Thani, Thailand, November 5-8, 1991 BAY OF BENGAL PROGRAMME BOBP/REP/51 Brackishwater Culture GCP/RAS/ I 18/MUL REPORT OF THE SEMINAR ON THE MUD CRAB CULTURE AND TRADE held at Swat Thani, Thailand, November 5-8,1991 Edited: C.A. ANGELL Sr. Aquaculturist BOBP BAY OF BENGAL PROGRAMME, Madras, India 1992 The mud crab, Scylla sp.. found throughout the Indo-Pacific region. has become in- creasingly popular by virtue of its meat quality and large size. While regional trade in the species has been growing. very little attention has been given to the fishery and culture in the Bay of Bengal region. The fishery, culture and trade in Scylla sp. is small-scale and involves artisanal fisherfolk, thus attracting the interest of the Bay of Bengal Programme (BOBP). As little is known of the state of the fishery, culture and trade. it was felt that a regional seminar might be an appropriate medium for an exchange of information among BOBP’s member countries. A seminar would also provide an opportunity to update knowledge of the industry. Southern Thailand, particularly the province of Surat Thani. has long been a centre for the capture and culture of the mud crab. With the proximity of the provincial brackishwater station and the opportunity to observe the industry first-hand. the town of Surat Thani promised to be an ideal venue for the seminar. And so. BOBP. in collaboration with the Department of Fisheries (DOCF) of the Government of Thailand, convened the seminar from November 5 to 8. -

2021–2029 Iloilo City Comprehensive Land Use Plan (CLUP) Volume 1 Preliminary Pages

2021–2029 Iloilo City Comprehensive Land Use Plan (CLUP) Volume 1 Preliminary Pages 3 City Planning and Development Office i 2021–2029 Iloilo City Comprehensive Land Use Plan (CLUP) Volume 1 Preliminary Pages Message from the Mayor Our beloved Iloilo City has progressively built on its glorious past to usher in a present, which is a source of pride and hope for our people, and an inspiring benchmark for our neighbors in Western Visayas, and beyond. Yet we are not a people who rest on our laurels. We aim higher. We move further. We scale greater heights. We level up. To level up Iloilo City, we begin with the end in mind. We need to envision a future where our city is livable, sustainable and resilient. We aim for a culturally vibrant and economically well-developed city where governance is a shared responsibility and where people are innovative and creative. We dream big, yet we stay realistic. We know that our collective journey as Ilonggos towards our envisioned future has to factor in developments in our external environment. Prudence likewise dictates that our resolve to level-up needs to consider our strengths and weaknesses as a local government unit and as a community. We need to assess our competencies and our resources, particularly our land and its current and future uses, so we are well-informed in determining the best development strategy to level up Iloilo City. I am, therefore, most pleased that we have already crafted the 2021-2029 Iloilo City Comprehensive Land Use Plan (CLUP), which is a product of a series of consultations with various sectors. -

October 24-25, 2018 Solaire Resort and Casino Manila

ã§ŴÕ§ª¼ªÕÕªÃŴŴت¼ôúŴ ÂÉØêÿãªÉÃŴÃŴ ùÕÃܪÉÃŴÜèªãŴ ĊĈĉĐ OCTOBER 24-25, 2018 SOLAIRE RESORT AND CASINO MANILA, PHILIPPINES THE PHILIPPINE RAILWAY MODERNIZATION AND EXPANSION SUMMIT Photo Credit: http://media.philstar.com/images/the-philippine-star/headlines/20150609/lrt-2.jpg PHILIPPINE RAILWAY PROJECT PIPELINE PROJECTS Budget (in US$) PROJECT PI PELI NE LRTA Mega Manila Subway $ 4,472,245,480.96 LRT 1 South (Cavite) Extension Project Phase1 $ 1,278,628,774.07 LRT Line 2 West (Tutuban) Extension Project $ 11,978,525.34 LRT Line 2 East (Masinag) Extension Project $ 16,457,272.32 MLRT Line 4 Taytay - Ortigas Center $ 989,016,401.52 Line 7 (MRT 7) $ 1,500,000,000.00 LRT Line 1 North Extension Common Station $ 23,641,826.33 Total $ 8,268,326,454.21 PNR PNR North 1 (North South Commuter Rail) $ 2,074, 570,260.55 PNR North 2 $ 2,955,228,291.39 PNR South Commuter Manila - Los Baños, Laguna $ 2,640,003,940.30 PNR South Long Haul $ 2,974,929,813.33 Mindanao Railway: Tagum-Davao City-Digos (TDD) Segment $ 503,000,000.00 Subic-Clark Cargo Railway Project $ 1,134,807,663.89 Malolos-Clark Railway Project (MRCP) $ 2,068,659,803.97 Total $14,351,199,773.43 Grand Total $22,619,526,227.64 For inquiries: Robert James Limjoco | Event Manager (Telephone +63929564524 / Mobile +639209584847) • Email: [email protected] Éèã¼Éɹ CONFIRMED GUESTS THE golden age of infrastructure in the Philippines now begins. Around P8 trillion are budgeted until 2021 in planning, developing and constructing mega- infrastructure projects. -

World Bank Document

Document of The World Bank FOR OFFICIAL USE ONLY Public Disclosure Authorized Report No. 4535-PH Public Disclosure Authorized STAFF APPRAISAL REPORT PHILIPPINES FIFTH HIGHWAY PROJECT Public Disclosure Authorized May 1, 1984 Public Disclosure Authorized Transportation Division 2 Projects Department East Asia & Pacific Regional Office This document has a restricted distribution and may be used by recipients only in the performance of their official duties. Its contents may not otherwise be disclosed without World Bank authorization. CURRENCY EQUIVALENTS Currency Unit = Pesos (P) US$1.00 = P 14.00 P 1.00 = US$0.07 FISCAL YEAR January 1 to December 31 ABBREVIATIONS AA - Advise of Allotment ADT - Average Daily Traffic AASHTO - American Association of State Highway Officials ADB - Asian Development Bank BAT - Bureau of Air Transport of MOTC BLT - Bureau of Land Transport of MOTC BOM - Bureau of Maintenance of MPWH BP - Batasang Pambansa CDC - Cash Disbursement Ceiling; CIAP - Construction Industry Authority of the Philippines CO - City Office of MPWH COA - Commission on Audit DBCC - Development Budget Coordinating Committee DO - District Office of MPWH EMK - Equivalent Maintenance Kilometer ERR - Economic Rate of Return GRT - Gross Registered Tonnage MARINA - Maritime Industry Authority MDS - Manpower Development Service of MPWH MLG - Ministry of Local Government MOB - Ministry of Budget MOTC - Ministry of Transport and Communications MPH - Ministry of Public Highways MPW - Ministry of Public Works MPWH - Ministry of Public Works and Highways -

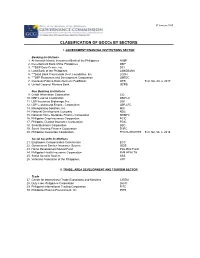

Classification of Goccs by SECTORS As of 07 January 2020

07 January 2020 CLASSIFICATION OF GOCCs BY SECTORS I. GOVERNMENT FINANCIAL INSTITUTIONS SECTOR Banking Institutions 1. Al-Amanah Islamic Investment Bank of the Philippines AIIBP 2. Development Bank of the Philippines DBP 3. ***DBP Data Center, Inc. DCI 4. Land Bank of the Philippines LANDBANK 5. ***Land Bank Countryside Dev't Foundation, Inc. LCDFI 6. ***LBP Resources and Development Corporation LBRDC 7. Overseas Filipino Bank (formerly PostBank) OFB E.O. No. 44, s. 2017 8. United Coconut Planters Bank UCPB Non Banking Institutions 9. Credit Information Corporation CIC 10. DBP Leasing Corporation DBP-LC 11. LBP Insurance Brokerage, Inc. LIBI 12. LBP Leasing and Finance Corporation LBP-LFC 13. Masaganang Sakahan, Inc. MSI 14. National Development Company NDC 15. National Home Mortgage Finance Corporation NHMFC 16. Philippine Crop Insurance Corporation PCIC 17. Philippine Deposit Insurance Corporation PDIC 18. Small Business Corporation SBC 19. Social Housing Finance Corporation SHFC 20. Philippine Guarantee Corporation PHILGUARANTEE E.O. No. 58, s. 2018 Social Security Institutions 21. Employees Compensation Commission ECC 22. Government Service Insurance System GSIS 23. Home Development Mutual Fund Pag-IBIG Fund 24. Philippine Health Insurance Corporation PHILHEALTH 25. Social Security System SSS 26. Veterans Federation of the Philippines VFP II. TRADE, AREA DEVELOPMENT AND TOURISM SECTOR Trade 27. Center for International Trade Expositions and Missions CITEM 28. Duty Free Philippines Corporation DFPC 29. Philippine International Trading Corporation PITC 30. Philippine Pharma Procurement, Inc. PPPI 07 January 2020 CLASSIFICATION OF GOCCs BY SECTORS Area Development 31. Bases Conversion Development Authority BCDA 32. Clark Development Corporation CDC 33. John Hay Management Corporation JHMC 34. -

TOURISM Guidebook for LOCAL GOVERMENT UNITS (Revised Edition)

TOURISM Guidebook FOR LOCAL GOVERMENT UNITS (Revised Edition) Revised © 2017 By Department of Tourism Department of the Interior and Local Government Department of Environment and Natural Resources Development Academy of the Philippines This knowledge product is produced through the collaboration among the Department of Tourism (DOT), Department of the Interior and Local Government (DILG) and Department of Environment and Natural Resources (DENR) with the funding support provided by the Government of Canada thru the Local Governance Support Program for Local Economic Development (LGSP-LED) project and the United Nations Development Programme (UNDP) thru the Biodiversity Partnership Project (BPP) and the Center for Governance of the Devepopment Academy of the Philippines (DAP). Please direct your subscription and inquiries to the: Offi ce of Tourism Development Planning, Research and Information Management Department of Tourism 5th Floor, 351 DOT Building, Sen. Gil Puyat Avenue, Makati City 459-5200 loc 506 [email protected] www.tourism.gov.ph ISBN 978-971-91303-9-0 This Guidebook is owned jointly by the DOT, DILG, DENR and DAP, with each party having royalty free non-exclusive and irrevocable license to use, publish, copy, reproduce or distribute the work for government or public purposes. Getting started... Do you think your city, municipality, or province has potential for tourism development that you want to harness? Is tourism a thriving industry in your locality and you want to take better advantage of it? Do you currently observe undesirable impacts of tourism in your area that you want to manage or control? Then this Tourism Guidebook is for you. -

Along Da Riles – Issue 8 (2019 20Th Anniversary)

ALONG DA RILES ISSUE #9 JANUARY 2019 EDITOR: BRAD PEADON A SPECIAL PUBLICATION OF THE ‘PHILIPPINE RAILWAY HISTORICAL SOCIETY’ PHILIPPINE RAILWAY HISTORICAL SOCIETY 20th ANNIVERSARY This special ninth issue of our former ‘Along Da Riles’ magazine has been put together to celebrate the 20th anniversary of our group. ‘Along Da Riles’ started as a magazine back in 2009, at the me of the group’s tenth anniversary and was inially meant to aid in fundraising for a preservaon group. Following on from the demise of this preservaon effort, the publicaon connued on for a short me as both a hard copy magazine for rail industry people and contributors, but also an ezine for others. The final issue (#7) was published in 2011, while a special issue #8 was commenced in 2014 but never completed. While the publicaon was very popular, a lack of willing contributors, plus many other projects, made it hard to compile a regular publicaon. SEMI RETIRED FOAMER Four Decades of Transport Photography hp://[email protected] ———————————————————————— PRHS.Society @ gmail. com This issue is dedicated to my dear friend hps://prhsociety.wordpress.com/ Tony Bailey (Transit Australia Editor) Rest In Peace. Cover Photo: 918 has just arrived in Naga from Sipocot. It will soon head south to Ligao. Bicol Commuter Train 2010 Photo: Brad Peadon alcogoodwin.blogspot.com Mr Regulto (PNR) 2017 Photo: Ana Peadon James Mangun 2017 Photo: Ana Peadon PH Model Railroaders 2018 Photo: Brad Peadon Team PNR Naga 2010 Photo: Brad Peadon LRT1 HQ Visit 2011 Photo: Someone PHILIPPINE RAILWAY HISTORICAL SOCIETY The First 20 Years! Two Decades. -

13. Cold Chain for Fishery Products in Panay Island

13. COLD CHAIN FOR FISHERY PRODUCTS IN PANAY ISLAND JICA-MARINA The Study on Domestic Shipping Development Plan in the Philippines (DSDP) Final Report 13. COLD CHAIN FOR FISHERY PRODUCTS IN PANAY ISLAND 13.1 Introduction (1) STUDY BACKGROUND The Philippines is by and large an agricultural economy – in particular the island economies of the Visayas and the remote regions of Mindanao. Agricultural commodities are mostly perishable; hence it is important that a fast and cost-effective transport be available so that agricultural economies in the countryside could reach principal markets, in particular Metro Manila. Quality preservation is vital so that perishable commodities retain their market value – thus, the development of cold chain system is thought to be one of the key components to improve the domestic shipping service and industry. It is for this reason that it is selected as the subject of further study as discussed in the Domestic Shipping Development Policies and Strategies. Several corridors have been identified as potential corridors for cold chain development. And as a subject for a pilot study – the Panay to Metro Manila fish corridor was selected. Panay Island is composed of four provinces – Aklan, Antique, Capiz and Iloilo and its geographic center is roughly 300 nautical miles from Metro Manila. Panay Island is the primary fish producer in the Visayas Region and is one of the primary producers of bangus in the country – an important fish in the Filipino diet, which is referred to as the national fish of the Philippines. Figure 13.1.1 Location of Panay Island Metro Manila Aklan Capiz Antique Iloilo Panay In terms of marketing and distribution, two main issues face the Panay bangus industry – first is the difficulty in reaching markets due to insufficient maritime transport and second is the marginal value of its products in primary markets, particularly Metro Manila, where quality deterioration due to transport time makes it uncompetitive. -

Experience and Policy Options for the Future Gilberto M

Philippine Institute for Development Studies 1977 Surian sa mga Pag-aaral Pangkaunlaran ng Pilipinas 252002 Infrastructure Development: Experience and Policy Options for the Future Gilberto M. Llanto DISCUSSION PAPER SERIES NO. 2002-26 Service through policy research The PIDS Discussion Paper Series constitutes studies that are preliminary and subject to further revisions. They are be- ing circulated in a limited number of cop- ies only for purposes of soliciting com- ments and suggestions for further refine- ments. The studies under the Series are unedited and unreviewed. The views and opinions expressed are those of the author(s) and do not neces- sarily reflect those of the Institute. Not for quotation without permission from the author(s) and the Institute. December 2002 For comments, suggestions or further inquiries please contact: The Research Information Staff, Philippine Institute for Development Studies 3rd Floor, NEDA sa Makati Building, 106 Amorsolo Street, Legaspi Village, Makati City, Philippines Tel Nos: 8924059 and 8935705; Fax No: 8939589; E-mail: [email protected] Or visit our website at http://www.pids.gov.ph ABSTRACT Global markets for goods and services have opened for countries that have made substantial investments in technological innovations in transportation, communications and production techniques, inventory management and the rapid rate of innovation in financial instruments, among others. This study presents in broad strokes a chronicle of infrastructure development in the Philippines in the last twenty-five years. It covers the infrastructure experience across the Marcos regime to the Estrada administration. The main objective of this paper is to flag those gaps and issues for future research, policy analysis and policy formulation.