ANNUAL REPORT 2019 BRAC UGANDA BANK LTD We Have Transformed

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Brac Lanka Finance PLC 2013 Cover

CHANGING LIVES ANNUAL REPORT 2013/14 OUR VISION To be a customer centric, innovative and broad based financial solutions partner. OUR MISSION Operate and expand aggressively, efficiently and Setup the ‘best-in-the-breed’ operational platform to profitably; with special focus on the Micro, Small and support growth aspirations Medium Enterprise segments Offer a challenging and rewarding work environment that Develop and offer high quality, innovative products and provides opportunities for growth services Contribute to the quality of life in our communities Seek and grow business and markets with significant potential growth Transform the company into a trusted household financial brand Make products easily accessible to the target consumer by investing in distribution channels CONTENTS MANAGEMENT INFORMATION FINANCIAL INFORMATION Chairman’s Review 04 Independent Auditors’ Report 66 CEO’s Report 06 Statement of Comprehensive Income 67 Board of Directors 08 Statement of Financial Position 68 Management Discussion & Analysis 12 Statement of Changes in Equity 69 Operational Review 14 Cash Flow Statement 70 Financial Review 16 Notes to the Financial Statements 71 Risk Management 18 Shareholders’ Information 98 Branch Network 100 SUSTAINABILITY REPORT Notice of Meeting 101 Sustainability Report 24 Notes 102 Our Events 27 Brac Lanka Finance PLC Form of Proxy Corporate Governance Report 29 Corporate Information - Inner Back Cover Report of the Directors 55 Director’s Statement on Internal Controls Over Financial Reporting 60 Report of the Audit Committee 61 Report of the Integrated Risk Management Committee 61 Report of The Remuneration Committee 62 Directors‘ Responsibility For Financial Reporting 63 CHANGING LIVES BRAC Lanka Finance PLC was established with a passion and tenaciousness to support and sustain the emerging lives of Sri Lankans. -

Self-Settled Refugees and the Impact on Service Delivery in Koboko

Self-Settled Refugees and the Impact on Service Delivery in Koboko Municipal Council Empowering Refugee Hosting Districts in Uganda: Making the Nexus Work II2 Empowering Refugee Hosting Districts in Uganda: Making the Nexus Work Foreword This report ‘Self-Settled Refugees and the Impact on Service Delivery in Koboko Municipal Council’ comes in a time when local governments in Uganda are grappling with the effects of refugees who have moved and settled in urban areas. As a country we have been very welcoming to our brothers and sisters who have been seeking refuge and we are proud to say that we have been able to assist the ones in need. Nonetheless, we cannot deny that refugees have been moving out of the gazetted settlements and into the urban areas, which has translated into increasing demands on the limited social amenities and compromises the quality of life for both refugees and host communities, this whilst the number of self-settled refugees continues to grow. This report aims to address the effects the presence self-settled refugees have on urban areas and the shortfalls local governments face in critical service delivery areas like education, health, water, livelihoods and the protection of self-settled refugees if not properly catered for. So far, it has been difficult for the local governments to substantiate such cases in the absence of reliable data. We are therefore very pleased to finally have a reference document, which addresses the unnoticed and yet enormous challenges faced by urban authorities hosting refugees, such as Koboko Municipal Council. This document provides us with more accurate and reliable data, which will better inform our planning, and enhances our capacity to deliver more inclusive services. -

Former DFCU Bank Bosses Charged Over Global Fund Scam

4 NEW VISION, Thursday, April 3, 2014 NATIONAL NEWS Former DFCU Bank bosses charged over Global Fund scam By Edward Anyoli Lule, while employed by Lule through manipulation of 300 sub-recipients and DFCU – a company in which Former Global Global Fund foreign exchange, individuals be audited further Two former managers of DFCU the Government had shares – falsely claiming that it was and that former health minister, Bank have been charged with directed the bank to convert Fund boss Dr. commission fees for soliciting Maj. Gen. Jim Muhwezi and abuse of office, costing the $2m Global Fund money into Global Fund business. his deputies; Mike Mukula Government sh479m. the local currency at an inflated Muhebwa was last Kantuntu, Lule and Kituuma and Alex Kamugisha, be Robert Katuntu, the former foreign exchange rate of Magala (a city lawyer, who is prosecuted. managing director of DFCU sh1,839 per dollar, which was week charged with summoned to appear in court This resulted into the and Godffrey Lule, the bank’s higher than the rate of sh1,815, on April 11) are jointly facing establishment of the anti- former head of treasury, were raising a difference of sh48m. causing financial the charges with Dr. Tiberius corruption division of the yesterday charged before the On another charge, Lule Muhebwa, the former Global High Court in December Anti-Corruption Court chief is accused of fraudulently loss of sh108m Fund project co-ordinator. 2008, which has convicted magistrate. They denied the directing the bank staff to Muhebwa has been charged two suspects; Teddy Cheeye charges and were granted cash convert $1m Global Fund with causing financial loss of the presidential adviser on bail of sh3m each. -

Magazine Layout 2 LR

SAT 12 OCT SPEKE RESORT LET’S GOAT IT On! RACE PROGRAMME #goatraceskla ENJOY RESPONSIBLY: EXCESSIVE CONSUMPTION OF ALCOHOL IS HARMFUL TO YOUR HEALTH. Don’t Choose What You Want to Do. Choose Who You want to be. Faculty of ; • Business and Management • Health Sciences • Humanities and Social Sciences • Science and Technology • Dept. of Petroleum and Energy Studies CORPORATE TRAINING AND SHORT COURSES AVAILABLE, UPSKILL YOURSELF TODAY! : TABLE OF CONTENTS Organisers Message .............................................................................................................................................1 Security information..............................................................................................................................................2 Goat Race 2018 Pictorial ................................................................................................................................. 3-4 Race 1 information ................................................................................................................................................5 Humor......................................................................................................................................................................7 Race 2 information ................................................................................................................................................9 Race 3 information ............................................................................................................................................ -

Public Notice

PUBLIC NOTICE PROVISIONAL LIST OF TAXPAYERS EXEMPTED FROM 6% WITHHOLDING TAX FOR JANUARY – JUNE 2016 Section 119 (5) (f) (ii) of the Income Tax Act, Cap. 340 Uganda Revenue Authority hereby notifies the public that the list of taxpayers below, having satisfactorily fulfilled the requirements for this facility; will be exempted from 6% withholding tax for the period 1st January 2016 to 30th June 2016 PROVISIONAL WITHHOLDING TAX LIST FOR THE PERIOD JANUARY - JUNE 2016 SN TIN TAXPAYER NAME 1 1000380928 3R AGRO INDUSTRIES LIMITED 2 1000049868 3-Z FOUNDATION (U) LTD 3 1000024265 ABC CAPITAL BANK LIMITED 4 1000033223 AFRICA POLYSACK INDUSTRIES LIMITED 5 1000482081 AFRICAN FIELD EPIDEMIOLOGY NETWORK LTD 6 1000134272 AFRICAN FINE COFFEES ASSOCIATION 7 1000034607 AFRICAN QUEEN LIMITED 8 1000025846 APPLIANCE WORLD LIMITED 9 1000317043 BALYA STINT HARDWARE LIMITED 10 1000025663 BANK OF AFRICA - UGANDA LTD 11 1000025701 BANK OF BARODA (U) LIMITED 12 1000028435 BANK OF UGANDA 13 1000027755 BARCLAYS BANK (U) LTD. BAYLOR COLLEGE OF MEDICINE CHILDRENS FOUNDATION 14 1000098610 UGANDA 15 1000026105 BIDCO UGANDA LIMITED 16 1000026050 BOLLORE AFRICA LOGISTICS UGANDA LIMITED 17 1000038228 BRITISH AIRWAYS 18 1000124037 BYANSI FISHERIES LTD 19 1000024548 CENTENARY RURAL DEVELOPMENT BANK LIMITED 20 1000024303 CENTURY BOTTLING CO. LTD. 21 1001017514 CHILDREN AT RISK ACTION NETWORK 22 1000691587 CHIMPANZEE SANCTUARY & WILDLIFE 23 1000028566 CITIBANK UGANDA LIMITED 24 1000026312 CITY OIL (U) LIMITED 25 1000024410 CIVICON LIMITED 26 1000023516 CIVIL AVIATION AUTHORITY -

Project Information

KfW Development Bank Project Information Implemented by: Project approach Tax System Reform – Uganda The project financed by KfW Development Bank aims at the implementation of an information technology appli- cation to improve public financial management in Implementing new technologies to increase reve- nues to the state budget Uganda. Precisely, it encompasses the establishment of a data warehouse. In addition, newly introduced The collection of taxes and other duties from citi- software allows for the analysis of the pooled data and zens plays a vital role in the consolidation of gov- the generation of reports as well as improved forecast- ernment budgets. The state can use the money ing. Along with these measures, the respective busi- from the tax payers to invest in public services and ness processes are optimised and the staff receives infrastructure. Such government spending sup- training in the use of the data warehouse. ports the achievement of the sustainable devel- opment goals and the reduction of poverty. Well- Relevant data on taxes and customs is so far being fed functioning and efficient tax and customs systems into several different systems, so that comprehensive can strengthen the ownership of governments and analyses are challenging. The data warehouse however thus have a positive impact on good financial gov- ernance. With a healthy budget, partner countries become more independent from financial contribu- Project name Support for Tax System Reform tions by donors in order to finance their national development agendas. Despite substantial reforms in the recent past, the tax collection level in Ugan- Commissioned German Federal Ministry for da is among the lowest in Eastern Africa. -

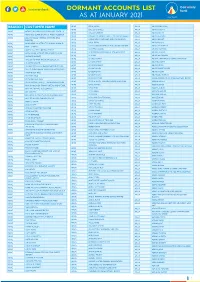

1612517024List of Dormant Accounts.Pdf

DORMANT ACCOUNTS LIST AS AT JANUARY 2021 BRANCH CUSTOMER NAME APAC OKAE JASPER ARUA ABIRIGA ABUNASA APAC OKELLO CHARLES ARUA ABIRIGA AGATA APAC ACHOLI INN BMU CO.OPERATIVE SOCIETY APAC OKELLO ERIAKIM ARUA ABIRIGA JOHN APAC ADONGO EUNICE KAY ITF ACEN REBECCA . APAC OKELLO PATRICK IN TRUST FOR OGORO ISAIAH . ARUA ABIRU BEATRICE APAC ADUKU ROAD VEHICLE OWNERS AND OKIBA NELSON GEORGE AND OMODI JAMES . ABIRU KNIGHT DRIVERS APAC ARUA OKOL DENIS ABIYO BOSCO APAC AKAKI BENSON INTRUST FOR AKAKI RONALD . APAC ARUA OKONO DAUDI INTRUST FOR OKONO LAKANA . ABRAHAM WAFULA APAC AKELLO ANNA APAC ARUA OKWERA LAKANA ABUDALLA MUSA APAC AKETO YOUTH IN DEVELOPMENT APAC ARUA OLELPEK PRIMARY SCHOOL PTA ACCOUNT ABUKO ONGUA APAC AKOL SARAH IN TRUST FOR AYANG PIUS JOB . APAC ARUA OLIK RAY ABUKUAM IBRAHIM APAC AKONGO HARRIET APAC ARUA OLOBO TONNY ABUMA STEPHEN ITO ASIBAZU PATIENCE . APAC AKULLU KEVIN IN TRUST OF OLAL SILAS . APAC ARUA OMARA CHRIST ABUME JOSEPH APAC ALABA ROZOLINE APAC ARUA OMARA RONALD ABURA ISMAIL APAC ALFRED OMARA I.T.F GERALD EBONG OMARA . APAC ARUA OMING LAMEX ABURE CHRISTOPHER APAC ALUPO CHRISTINE IN TRUST FOR ELOYU JOVIN . APAC ARUA ONGOM JIMMY ABURE YASSIN APAC AMONG BEATRICE APAC ARUA ONGOM SILVIA ABUTALIBU AYIMANI APAC ANAM PATRICK APAC ARUA ONONO SIMON ACABE WANDI POULTRY DEVELPMENT GROUP APAC ANYANGO BEATRASE APAC ARUA ONOTE IRWOT VILLAGE SAVINGS AND LOAN ACEMA ASSAFU APAC ANYANZO MICHEAL ITF TIZA BRENDA EVELYN . APAC ARUA OPIO JASPHER ACEMA DAVID APAC APAC BODABODA TRANSPORTERS AND SPECIAL APAC ARUA OPIO MARY ACEMA ZUBEIR APAC APALIKA FARMERS ASSOCIATION APAC ARUA OPIO RIGAN ACHEMA ALAHAI APAC APILI JUDITH APAC ARUA OPIO SAM ACHIDRI RASULU APAC APIO BENA IN TRUST OF ODUR JONAN AKOC . -

World Bank Document

Public Disclosure Authorized ENVIRONMENTAL AND SOCIAL MANAGEMENT AND MONITORING PLAN Public Disclosure Authorized Public Disclosure Authorized Ministry of Energy and Mineral Development Rural Electrification Agency ENERGY FOR RURAL TRANSFORMATION PHASE III GRID INTENSIFICATION SCHEMES PACKAGED UNDER WEST NILE, NORTH NORTH WEST, AND NORTHERN SERVICE TERRITORIES Public Disclosure Authorized JUNE, 2019 i LIST OF ABBREVIATIONS AND ACRONYMS CDO Community Development Officer CFP Chance Finds Procedure DEO District Environment Officer ESMP Environmental and Social Management and Monitoring Plan ESMF Environmental Social Management Framework ERT III Energy for Rural Transformation (Phase 3) EHS Environmental Health and Safety EIA Environmental Impact Assessment ESMMP Environmental and Social Mitigation and Management Plan GPS Global Positioning System GRM Grievance Redress Mechanism MEMD Ministry of Energy and Mineral Development NEMA National Environment Management Authority OPD Out Patient Department OSH Occupational Safety and Health PCR Physical Cultural Resources PCU Project Coordination Unit PPE Personal Protective Equipment REA Rural Electrification Agency RoW Right of Way UEDCL Uganda Electricity Distribution Company Limited WENRECO West Nile Rural Electrification Company ii TABLE OF CONTENTS LIST OF ABBREVIATIONS AND ACRONYMS ......................................................... ii TABLE OF CONTENTS ........................................................................................ iii EXECUTIVE SUMMARY ....................................................................................... -

THE REPUBLIC of UGANDA in the CHIEF MAGISTRATES COURT of MAKINDYE at MAKINDYE CRIMINAL REGISTRY CAUSELIST for the SITTINGS of : 07-10-2019 to 11-10-2019

THE REPUBLIC OF UGANDA IN THE CHIEF MAGISTRATES COURT OF MAKINDYE AT MAKINDYE CRIMINAL REGISTRY CAUSELIST FOR THE SITTINGS OF : 07-10-2019 to 11-10-2019 MONDAY, 07-OCT-2019 MAGISTRATE GRADE I MBABAZI EDITH BEFORE:: MARY Case Nature of Time Case number Pares Charge CRB No Sing Type Category Appl./Appeal Hearing - Criminal UGANDA VS 1. 09:00 MAK-00-CR-CO-1260-2018 THEFT Kabalagala/1118/2018 prosecuon Offence BIKOLIMANA ALEX case UGANDA VS BUKENYA STEALING BY AGENTS- Hearing - Criminal 2. 09:00 MAK-00-CR-CO-0961-2018 BRIAN & KAWOOYA PROPERTY WHICH HAS Katwe/854/2018 prosecuon Offence FRED BEEN RECEIV case UGANDA VS Hearing - Traffic TRAFFIC-RECKLESS 3. 09:00 MAK-00-CR-TO-0010-2019 MUSINGUZI Katwe/22/2019 prosecuon Offence DRIVING CHRISTOPHER case Hearing - Criminal UGANDA VS NSUBUGA 4. 09:00 MAK-00-CR-CO-0847-2019 BREAKING/BURGLARY-(A-B) Katwe/1155/2019 prosecuon Offence JAMIRU case Hearing - Criminal UGANDA VS KAVUMA 5. 09:00 MAK-00-CR-CO-0606-2019 STEALING VEHICLE Katwe/2000/2018 prosecuon Offence ABDUL case Hearing - Criminal UGANDA VS KIBIRIGE 6. 09:00 MAK-00-CR-CO-0511-2019 THEFT Kabalagala/542/2019 prosecuon Offence DAN case Hearing - Criminal UGANDA VS MUGISHA 7. 09:00 MAK-00-CR-CO-0169-2019 THEFT Kabalagala/152/2019 prosecuon Offence ABEL case UGANDA VS Hearing - Criminal 8. 09:00 MAK-00-CR-CO-1451-2018 SSEMWOGERERE BREAKING/BURGLARY-(A-B) Kabalagala/129/2018 prosecuon Offence MATIYA case 9. 09:00 MAK-00-CR-CO-1218-2018 Criminal UGANDA VS KANGABE BREAKING/BURGLARY-(A-B) Katwe/1533/2018 Hearing - Offence KRARISA prosecuon case CARELESS OR Hearing - Traffic UGANDA VS MUJUNI 10. -

Bank of Uganda

Status of Financial Inclusion in Uganda First Edition- March 2014 BANK OFi UGANDA Table of Contents List of Abbreviations and Acronyms ..................................................................................................... iii Executive Summary ....................................................................................................................................iv 1.0 Introduction ............................................................................................................................................. 1 2.0 Concept of Financial Inclusion ......................................................................................................... 1 3.0 Financial Inclusion Landscape for Uganda .................................................................................. 4 3.1 Data Sources ...................................................................................................................................... 4 3.2 Demand Side Indicators ................................................................................................................. 5 3.3 Supply Side Indicators .................................................................................................................... 7 3.3.1 Financial Access Indicators .................................................................................................... 7 3.3.2 Comparison of Access Indicators across Countries. ...................................................................... 14 3.3.3 Geographic Indicators -

Brac Saajan Exchange Ltd Annual Report and Financial Statements for the Year Ended 31 December 2020

Company Registration No. 06469886 (England and Wales) BRAC SAAJAN EXCHANGE LTD ANNUAL REPORT AND FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2020 BRAC SAAJAN EXCHANGE LTD COMPANY INFORMATION Directors Mr Kazi Mahmood Sattar Mr Selim Reza Farhad Hussain Mr Abdus Salam Secretary Mr Rais Uddin Ahmed Company number 06469886 Registered office 160-162 Lozells Road Lozells Birmingham B19 2SX Auditor Reddy Siddiqui LLP 183-189 The Vale Acton London W3 7RW BRAC SAAJAN EXCHANGE LTD CONTENTS Page Strategic report 1 - 6 Directors' report 7 - 8 Directors' responsibilities statement 9 Independent auditor's report 10 - 12 Statement of comprehensive income 13 Balance sheet 14 Statement of changes in equity 15 Statement of cash flows 16 Notes to the financial statements 17 - 35 BRAC SAAJAN EXCHANGE LTD STRATEGIC REPORT FOR THE YEAR ENDED 31 DECEMBER 2020 The directors present the strategic report for the year ended 31 December 2020. Fair Review of the Business The company, a subsidiary of BRAC Bank Limited of Bangladesh, provides remittance services and cross- border payment solutions for South Asian migrants living in UK and Europe. It offers a wide range of payment services principally to Bangladesh and Pakistan but also to India, Sri Lanka and Nepal. The company also offers its services through a French subsidiary, based in Paris. Revenue is earned through a combination of transaction fees and foreign exchange margin. Total remittance to all receiving countries fell by 16% from £542m in 2019 to £455m in 2020. UK retail volume which has been effected by the Covid-19 pandemic, saw a reduction of 20% to £189m. -

Crane Bank to Appeal to Supreme Court

Plot 37/43 Kampala Road, P.O. Box 7120 Kampala Cable Address: UGABANK, Telex: 61069/61244 General Lines: (+256-414) 258441/6, 258061/6, 0312-392000 or 0417-302000. Fax: (+256-414) 233818 Website: www.bou.or.ug E-mail: [email protected] CRANE BANK TO APPEAL TO SUPREME COURT KAMPALA – 30 June 2020 – Bank of Uganda (BoU) wishes to inform the public of its decision to appeal the Court of Appeal’s dismissal of the case filed by Crane Bank Limited (in Receivership) vs. Sudhir Ruparelia and Meera Investments Limited to the Supreme Court. In exercise of its powers under sections 87(3), 88(1)(a)&(b) of the Financial Institutions Act, 2004, BoU placed Crane Bank Ltd (In Receivership) [“Crane Bank”] under Statutory Management on 20th October 2016. This decision was necessary upon discovering that Crane Bank had significant and increasing liquidity problems that could not be resolved without the Central Bank’s intervention given that Crane Bank had failed to obtain credit from anywhere else. An inventory by external auditors found that the assets of Crane Bank were significantly less than its liabilities. In order to protect the financial system and prevent loss to the depositors of Crane Bank, Bank of Uganda had to spend public funds to pay Crane Bank’s depositors. A subsequent forensic investigation as to why Crane Bank became insolvent found a number of wrongful and irregular activities linked to Sudhir Ruparelia and Meera Investments Ltd. These findings form the basis of the claims in the lawsuit by Crane Bank. The suit was necessary for recovery of the taxpayers’ money used to pay depositors’ funds as well as the other liabilities of Crane Bank.