Crossrail Property Impact & Regeneration Study

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Land Adjacent to 16 Beardell Street, Crystal Palace, London SE19 1TP Freehold Development Site with Planning Permission for 5 Apartments View More Information

CGI of proposed Land adjacent to 16 Beardell Street, Crystal Palace, London SE19 1TP Freehold development site with planning permission for 5 apartments View more information... Land adjacent to 16 Beardell Street, Crystal Palace, London SE19 1TP Home Description Location Planning Terms View all of our instructions here... III III • Vacant freehold plot • Sold with planning permission for 5 apartments • Contemporary 3 storey block • Well-located close by to Crystal Palace ‘triangle’ and Railway Station • OIEO £950,000 F/H DESCRIPTION An opportunity to acquire a freehold development site sold with planning permission for the erection for a 3 storey block comprising 5 apartments (2 x studio, 2 x 2 bed & 1 x 3 bed). LOCATION Positioned on Beardell Street the property is located in the heart of affluent Crystal Palace town centre directly adjacent to the popular Crystal Palace ‘triangle’ which offers an array of independent shops, restaurants and bars mixed in with typical high street amenities. In terms of transport, the property is located 0.5 miles away from Crystal Palace Station which provides commuters with National Rail services to London Bridge, London Victoria, West Croydon, and Beckenham Junction and London Overground services between Highbury and Islington (via New Cross) and Whitechapel. E: [email protected] W: acorncommercial.co.uk 120 Bermondsey Street, 1 Sherman Road, London SE1 3TX Bromley, Kent BR1 3JH T: 020 7089 6555 T: 020 8315 5454 Land adjacent to 16 Beardell Street, Crystal Palace, London SE19 1TP Home Description Location Planning Terms View all of our instructions here... III III PLANNING The property has been granted planning permission by Lambeth Council (subject to S106 agreement which has now been agreed) for the ‘Erection of 3 storey building plus basement including a front lightwell to provide 5 residential units, together with provision of cycle stores, refuse/recycling storages and private gardens.’ Under ref: 18/00001/FUL. -

NOTICE of RELEASE of TRUSTEES. O O No

NOTICE OF RELEASE OF TRUSTEES. o o No. of o Debtor's Name. Debtor's Address. Debtor's Description. Court. Matter. Trustee's Name. Trustee's Address. Trustee's Description. Date ot Release. Ball, William 2, 3, 4, 14, 15, 16, and 17, Tauntqn- Cab Proprietor High Court of Justice 890 William Rooke 11, Milk-street-buildings, Accountant Nov. 28, 1888 mews, Dorset-square, Middlesex in Bankruptcy of 18SG Cheapside, London Bunting, William Goggs 9, Penywern-road, Earl's Court, Fancy Box Manufac- High Court of Justice 738 Henry John Leslie ... 4, Coleman-street, Lon- Chartered Account- Nov. 29, 1888 (otherwise De Bunting, Middlesex turer in Bankruptcy of 1885 don ant H W. G.) W Rl Campbell, Percy 5, Drapers'-gardens, Throgmorton- Stockbroker High Court of Justice 492 Horace Woodburn 4, Coloman- street, Lon- Chartered Account- Nov. 29, 1888 street, London in Bankruptcy of 1885 Kirby don, E.C. ant t-i O Coulter, Thomas W. Late of 62, Carter-lane, E.C. Coulter, Charles 'A., and ... Late of 62, Carter-lane, E.C. ^ Ennery, L. D Late of 62, Carter-lane, E.G. u (trading as o Coulters and Co.) Lately trading at 62, Carter-lane, Shippers and Mer- High Court of Justice 1249 Frederick Adolphus 82, Queen-street, Cheap- Chartered Account- Nov. 29, 1888 London, and residing at 54, chants ' in Bankruptcy of 1886 Rawlings side, E.C. ant Addison-road, Kensington, Mid- dlesex • Cox, William Joseph 253, Portobello-road, Netting Hill, Upholsterer and Cabi- High Court of Justice 951 Pullam Markham 2, Gresham - buildings, Chartered Account- Nov. -

Uncovering the Underground's Role in the Formation of Modern London, 1855-1945

University of Kentucky UKnowledge Theses and Dissertations--History History 2016 Minding the Gap: Uncovering the Underground's Role in the Formation of Modern London, 1855-1945 Danielle K. Dodson University of Kentucky, [email protected] Digital Object Identifier: http://dx.doi.org/10.13023/ETD.2016.339 Right click to open a feedback form in a new tab to let us know how this document benefits ou.y Recommended Citation Dodson, Danielle K., "Minding the Gap: Uncovering the Underground's Role in the Formation of Modern London, 1855-1945" (2016). Theses and Dissertations--History. 40. https://uknowledge.uky.edu/history_etds/40 This Doctoral Dissertation is brought to you for free and open access by the History at UKnowledge. It has been accepted for inclusion in Theses and Dissertations--History by an authorized administrator of UKnowledge. For more information, please contact [email protected]. STUDENT AGREEMENT: I represent that my thesis or dissertation and abstract are my original work. Proper attribution has been given to all outside sources. I understand that I am solely responsible for obtaining any needed copyright permissions. I have obtained needed written permission statement(s) from the owner(s) of each third-party copyrighted matter to be included in my work, allowing electronic distribution (if such use is not permitted by the fair use doctrine) which will be submitted to UKnowledge as Additional File. I hereby grant to The University of Kentucky and its agents the irrevocable, non-exclusive, and royalty-free license to archive and make accessible my work in whole or in part in all forms of media, now or hereafter known. -

N11 Bus Time Schedule & Line Route

N11 bus time schedule & line map N11 Liverpool Street - Ealing Broadway View In Website Mode The N11 bus line (Liverpool Street - Ealing Broadway) has 2 routes. For regular weekdays, their operation hours are: (1) Ealing Broadway: 12:21 AM - 4:51 AM (2) Liverpool Street: 12:15 AM - 11:45 PM Use the Moovit App to ƒnd the closest N11 bus station near you and ƒnd out when is the next N11 bus arriving. Direction: Ealing Broadway N11 bus Time Schedule 81 stops Ealing Broadway Route Timetable: VIEW LINE SCHEDULE Sunday 12:21 AM - 4:51 AM Monday 12:21 AM - 4:51 AM Liverpool Street Station (L) 192 Bishopsgate, London Tuesday 12:21 AM - 4:51 AM Wormwood Street (Y) Wednesday 12:21 AM - 4:51 AM 99 Bishopsgate, London Thursday 12:21 AM - 4:51 AM Old Broad Street (LL) Friday 12:21 AM - 4:51 AM 5 Old Broad Street, London Saturday 12:21 AM - 4:51 AM Bank Station / Queen Victoria Street 1 Poultry, London St Paul's Churchyard (SH) Old Change Court, London N11 bus Info Direction: Ealing Broadway St Paul's Cathedral (SJ) Stops: 81 10 Saint Paul's Church Yard, London Trip Duration: 83 min Line Summary: Liverpool Street Station (L), City Thameslink Stn / Ludgate Circus (F) Wormwood Street (Y), Old Broad Street (LL), Bank 65 Ludgate Hill, London Station / Queen Victoria Street, St Paul's Churchyard (SH), St Paul's Cathedral (SJ), City Thameslink Stn / Shoe Lane (H) Ludgate Circus (F), Shoe Lane (H), Fetter Lane (W), Fleet Street, London Chancery Lane (W), The Royal Courts Of Justice (P), Aldwych / Drury Lane (R), Savoy Street (U), Bedford Fetter Lane (W) Street -

Neighbourhood Governance Note of Ealing Broadway Ward Forum Meeting ______

Neighbourhood Governance Note of Ealing Broadway Ward Forum Meeting ______________________________________________________________________________________ Ealing Broadway Ward Forum meeting – held at 8pm until 9.30pm on Wednesday 8 October 2008 in the hall of St Stephen’s Church Centre, W5. Present: Councillors Young (Chairman), Potts and Scott Attendees: over 83 people attended with 65 people signing the attendance sheet. Note taker: Evelyn Gloyn (EG) - Neighbourhood Co-ordinator South Item Notes Actions/Information 1/2 Chairman’s Introduction and the Role of the Ward Forums People were offered light refreshments as they arrived and the meeting started promptly at 8 pm in the hall of St Stephen’s Church Centre. Councillor Anthony Young (Chairman) opened the meeting with introductions and explained the purpose of ward forums; the old area committees had been reviewed and were not effective as few attended. Ward forums were proposed in their place. Their purpose is so people could find out more about what is happening in their local and their concerns about the local (ward) area could be raised; and they could also discuss how they would like to spend £40,000 within the ward on capital projects. The Neighbourhood Co-ordinator explained her role; she To contact your 1 Item Notes Actions/Information will post notes from the meetings with action points on the Neighbourhood Co-ordinator council’s website, then be working with both Councillors Evelyn Gloyn and council colleagues to address the concerns raised and Email:[email protected] attend a further 2/3 ward meetings ward per year. She will Tel: (020) 8825 8021 also be producing 2 ward newsletters over the year. -

Rail Accident Report

Rail Accident Report Derailment of a passenger train at Ealing Broadway 2 March 2016 Report 24/2016 December 2016 This investigation was carried out in accordance with: l the Railway Safety Directive 2004/49/EC; l the Railways and Transport Safety Act 2003; and l the Railways (Accident Investigation and Reporting) Regulations 2005. © Crown copyright 2016 You may re-use this document/publication (not including departmental or agency logos) free of charge in any format or medium. You must re-use it accurately and not in a misleading context. The material must be acknowledged as Crown copyright and you must give the title of the source publication. Where we have identified any third party copyright material you will need to obtain permission from the copyright holders concerned. This document/publication is also available at www.raib.gov.uk. Any enquiries about this publication should be sent to: RAIB Email: [email protected] The Wharf Telephone: 01332 253300 Stores Road Fax: 01332 253301 Derby UK Website: www.gov.uk/raib DE21 4BA This report is published by the Rail Accident Investigation Branch, Department for Transport. Preface Preface The purpose of a Rail Accident Investigation Branch (RAIB) investigation is to improve railway safety by preventing future railway accidents or by mitigating their consequences. It is not the purpose of such an investigation to establish blame or liability. Accordingly, it is inappropriate that RAIB reports should be used to assign fault or blame, or determine liability, since neither the investigation nor the reporting process has been undertaken for that purpose. The RAIB’s findings are based on its own evaluation of the evidence that was available at the time of the investigation and are intended to explain what happened, and why, in a fair and unbiased manner. -

Cinnabar Wharf Central, 24 Wapping High Street, London, E1w 1Nq

CINNABAR WHARF CENTRAL, 24 WAPPING HIGH STREET, LONDON, E1W 1NQ Furnished, £1,250 per week + £276 inc VAT one off admin and other charges may apply.* Available Now FLAT 60 CINNABAR WHARF CENTRAL, 24 £1,250 per week Furnished reception room • kitchen • 3 bedrooms • 3 bathrooms • balcony with views of the River Thames • parking • 24hr porterage • administrative EPC Rating = charges D apply Council Tax = H Description A well appointed 3 bedroom apartment in this prestigious development close to St. Katharine’s Dock and Tower Hill. The apartment benefits from a river facing wrap around balcony, higher tiered mezzanine which offer views over Tower Bridge. The property further benefits from private parking and 24hr security. The City, Canary Wharf and West End are conveniently accessed via Wapping and Tower Hill underground stations. Energy Performance A copy of the full Energy Performance Certificate is available on request. Viewing Strictly by appointment with Savills. FLOORPLANS Gross internal area: 0 sq ft, m² Gross external area: FILL IN *Admin fees including drawing up the tenancy agreement, reference charge for one tenant – £276 inc VAT. £36 inc VAT for each additional tenant, occupant, guarantor reference where required. Inventory check-out fee – charged at end of tenancy. Third party charge dependant on property size and whether furnished/unfurnished/part furnished and the company available at the time. Deposit – usually equivalent to 6 weeks rent, though may be greater subject to mutual agreement. Pets – additional Savills Wapping deposit required generally equivalent to two weeks rent. For more details, visit savills.co.uk/fees. Kristina Dabrila Important notice: Savills, their clients and any joint agents give notice that: 1: They are not authorised to make or give any representations or warranties in relation to the property either here or elsewhere, [email protected] either on their own behalf or on behalf of their client or otherwise. -

London Guide Welcome to London

Visitor information Welcome to London Your guide to getting around central London on public transport and making the most of your visit. tfl.gov.uk/visitinglondon Tube and central London bus maps inside #LondonIsOpen Welcome to London Paying for your travel Public transport is the best way to get There are different ways to pay for your around London and discover all that the travel. For most people, pay as you go - city has to offer. This guide will help you paying for the trips you make - with a plan how to get around the Capital on contactless payment card, an Oyster card or public transport. a Visitor Oyster card, is the best option as it If you have just arrived at an airport and are offers value, flexibility and convenience. looking for ways to get to central London, go to page 11 in this guide. Getting around London London’s transport system is iconic. With its world famous Underground (Tube) and iconic red buses, travelling around the Capital is an experience in itself. But London is much more than just the Tube or the bus; our vast network of transport services includes: Contactless payment cards If your credit, debit, charge card or wearable device has the contactless symbol above you can use it for pay as you go travel on London’s public transport. Android Pay and Apple Pay are also accepted. Benefits of contactless • It’s quick and easy – there’s no need to queue to buy a ticket • It offers great value – pay as you go with contactless is better value than buying a single ticket and you can benefit from both Night Tube daily and weekly capping (see page 5) • 14 million people have used contactless Night Tube services run on the to travel in London – including customers Jubilee, Victoria and most of from over 90 countries the Central and Northern lines all night on Fridays and Saturdays. -

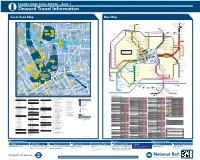

London Kings Cross Station – Zone 1 I Onward Travel Information Local Area Map Bus Map

London Kings Cross Station – Zone 1 i Onward Travel Information Local Area Map Bus Map 1 35 Wellington OUTRAM PLACE 259 T 2 HAVELOCK STREET Caledonian Road & Barnsbury CAMLEY STREET 25 Square Edmonton Green S Lewis D 16 L Bus Station Games 58 E 22 Cubitt I BEMERTON STREET Regent’ F Court S EDMONTON 103 Park N 214 B R Y D O N W O Upper Edmonton Canal C Highgate Village A s E Angel Corner Plimsoll Building B for Silver Street 102 8 1 A DELHI STREET HIGHGATE White Hart Lane - King’s Cross Academy & LK Northumberland OBLIQUE 11 Highgate West Hill 476 Frank Barnes School CLAY TON CRESCENT MATILDA STREET BRIDGE P R I C E S Park M E W S for Deaf Children 1 Lewis Carroll Crouch End 214 144 Children’s Library 91 Broadway Bruce Grove 30 Parliament Hill Fields LEWIS 170 16 130 HANDYSIDE 1 114 CUBITT 232 102 GRANARY STREET SQUARE STREET COPENHAGEN STREET Royal Free Hospital COPENHAGEN STREET BOADICEA STREE YOR West 181 212 for Hampstead Heath Tottenham Western YORK WAY 265 K W St. Pancras 142 191 Hornsey Rise Town Hall Transit Shed Handyside 1 Blessed Sacrament Kentish Town T Hospital Canopy AY RC Church C O U R T Kentish HOLLOWAY Seven Sisters Town West Kentish Town 390 17 Finsbury Park Manor House Blessed Sacrament16 St. Pancras T S Hampstead East I B E N Post Ofce Archway Hospital E R G A R D Catholic Primary Barnsbury Handyside TREATY STREET Upper Holloway School Kentish Town Road Western University of Canopy 126 Estate Holloway 1 St. -

Transport with So Many Ways to Get to and Around London, Doing Business Here Has Never Been Easier

Transport With so many ways to get to and around London, doing business here has never been easier First Capital Connect runs up to four trains an hour to Blackfriars/London Bridge. Fares from £8.90 single; journey time 35 mins. firstcapitalconnect.co.uk To London by coach There is an hourly coach service to Victoria Coach Station run by National Express Airport. Fares from £7.30 single; journey time 1 hour 20 mins. nationalexpress.com London Heathrow Airport T: +44 (0)844 335 1801 baa.com To London by Tube The Piccadilly line connects all five terminals with central London. Fares from £4 single (from £2.20 with an Oyster card); journey time about an hour. tfl.gov.uk/tube To London by rail The Heathrow Express runs four non- Greater London & airport locations stop trains an hour to and from London Paddington station. Fares from £16.50 single; journey time 15-20 mins. Transport for London (TfL) Travelcards are not valid This section details the various types Getting here on this service. of transport available in London, providing heathrowexpress.com information on how to get to the city On arrival from the airports, and how to get around Heathrow Connect runs between once in town. There are also listings for London City Airport Heathrow and Paddington via five stations transport companies, whether travelling T: +44 (0)20 7646 0088 in west London. Fares from £7.40 single. by road, rail, river, or even by bike or on londoncityairport.com Trains run every 30 mins; journey time foot. See the Transport & Sightseeing around 25 mins. -

Shoreditch E1 01–02 the Building

168 SHOREDITCH HIGH ST. SHOREDITCH E1 01–02 THE BUILDING 168 Shoreditch High Street offers up to 35,819 sq ft of contemporary workspace over six floors in Shoreditch’s most sought after location. High quality architectural materials are used throughout, including linear handmade bricks and black powder coated windows. Whilst the top two floors use curtain walling with black vertical fins – altogether a dramatic first impression for visitors on arrival. The interior is designed with dynamic businesses in mind – providing a stunning, light environment in which to work and create. STELLAR WORK SPACE 03–04 SHOREDITCH Shoreditch is still the undisputed home of the creative and tech industries – but has in recent years attracted other business sectors who crave the vibrant local environment, diverse amenity offering and entrepreneurial spirit. ORIGINALS ARTISTS VISIONARIES HOXTON Crondall St. d. Rd R st nd . Ea la s ng Ki xton St Ho . 05–06 SHOREDITCH Columbia Rd St Hoxton Sq. Rd 6 y d. R Pitfield ckne t s Ha Ea k Pl. Brunswic City 5 R d. 5 Cu St. d r Ol ta Calv et Ave i . 4 n Rivington Rd. Rd WALK TIMES . Arnold Circus. 3 11 OLD ST. 8 8 4 3 6 5 12 SHOREDITCH HIGH ST. STATION 7 MINS Shor 03 9 Gr 168 edit Leonard St. eat 1 10 1 E New Yard Inn. ch High . aste 4 6 7 11 2 Rd 2 10 h St. OLD SPITALFIELD MARKET . 2 churc een t rn 3 Red 4 MINS . 1 9 S St 9 07 8 . -

Hampton Court to Berrylands / Oct 2015

Crossrail 2 factsheet: Services between Berrylands and Hampton Court New Crossrail 2 services are proposed to serve all stations between Berrylands and Hampton Court, with 4 trains per hour in each direction operating directly to, and across central London. What is Crossrail 2? Crossrail 2 in this area Crossrail 2 is a proposed new railway serving London and the wider South East that could be open by 2030. It would connect the existing National Rail networks in Surrey and Hertfordshire with trains running through a new tunnel from Wimbledon to Tottenham Hale and New Southgate. Crossrail 2 will connect directly with National Rail, London Underground, London Overground, Crossrail 1, High Speed 1 international and domestic and High Speed 2 services, meaning passengers will be one change away from over 800 destinations nationwide. Why do we need Crossrail 2? The South West Main Line is one of the busiest and most congested routes in the country. It already faces capacity constraints and demand for National Rail services into Waterloo is forecast to increase by at least 40% by 2043. This means the severe crowding on the network will nearly double, and would likely lead to passengers being unable to board trains at some stations. Crossrail 2 provides a solution. It would free up space on the railway helping to reduce congestion, and would enable us to run more local services to central London that bypass the most congested stations. Transport improvements already underway will help offset the pressure in the short term. But we need Crossrail 2 to cope with longer term growth.