The Budget and Accounting Act

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Records of the Immigration and Naturalization Service, 1891-1957, Record Group 85 New Orleans, Louisiana Crew Lists of Vessels Arriving at New Orleans, LA, 1910-1945

Records of the Immigration and Naturalization Service, 1891-1957, Record Group 85 New Orleans, Louisiana Crew Lists of Vessels Arriving at New Orleans, LA, 1910-1945. T939. 311 rolls. (~A complete list of rolls has been added.) Roll Volumes Dates 1 1-3 January-June, 1910 2 4-5 July-October, 1910 3 6-7 November, 1910-February, 1911 4 8-9 March-June, 1911 5 10-11 July-October, 1911 6 12-13 November, 1911-February, 1912 7 14-15 March-June, 1912 8 16-17 July-October, 1912 9 18-19 November, 1912-February, 1913 10 20-21 March-June, 1913 11 22-23 July-October, 1913 12 24-25 November, 1913-February, 1914 13 26 March-April, 1914 14 27 May-June, 1914 15 28-29 July-October, 1914 16 30-31 November, 1914-February, 1915 17 32 March-April, 1915 18 33 May-June, 1915 19 34-35 July-October, 1915 20 36-37 November, 1915-February, 1916 21 38-39 March-June, 1916 22 40-41 July-October, 1916 23 42-43 November, 1916-February, 1917 24 44 March-April, 1917 25 45 May-June, 1917 26 46 July-August, 1917 27 47 September-October, 1917 28 48 November-December, 1917 29 49-50 Jan. 1-Mar. 15, 1918 30 51-53 Mar. 16-Apr. 30, 1918 31 56-59 June 1-Aug. 15, 1918 32 60-64 Aug. 16-0ct. 31, 1918 33 65-69 Nov. 1', 1918-Jan. 15, 1919 34 70-73 Jan. 16-Mar. 31, 1919 35 74-77 April-May, 1919 36 78-79 June-July, 1919 37 80-81 August-September, 1919 38 82-83 October-November, 1919 39 84-85 December, 1919-January, 1920 40 86-87 February-March, 1920 41 88-89 April-May, 1920 42 90 June, 1920 43 91 July, 1920 44 92 August, 1920 45 93 September, 1920 46 94 October, 1920 47 95-96 November, 1920 48 97-98 December, 1920 49 99-100 Jan. -

Glossary of Terms for Budget Publications

GLOSSARY OF TERMS ADOPTED EXPENSE AND REVENUE BUDGET: A BUDGET CODE: A 4-character code assigned to a financial plan for the City and its agencies for a fiscal schedule within an agency which identifies the year, setting forth operating expenditures and allocation made in such schedule in terms of its anticipated revenues, following due authorization accounting fund class, unit of appropriation, through the charter-mandated process. responsibility center, control category, local service district and program. ALLOCATION: A sum of money set aside for a specific purpose. BUDGET GAP: The difference between estimated expenditures and revenues for a future fiscal year. ANNUALIZATION: The impact of a new appropriation or expenditure reduction on the basis of a full year. For BUDGET LINE: An identified amount allocated for a instance, if an employee is terminated halfway through specific purpose in the expense budget supporting the fiscal year, the budget reduction in that year will schedules for each budget code within a unit of equal half the employee’s annual salary. The appropriation. Budget lines are used to provide “annualized” reduction is the full amount of the detailed information on the number of positions, titles, employee’s salary. salaries and other expenses in a budget code. ANNUAL RATE: Sum of the salaries paid to the full- BUDGET MODIFICATION: A change in an amount in time active employees in a title description. any budget line during the fiscal year. APPROPRIATION: A general term used to denote the BUDGET STABILIZATION ACCOUNT: An amount authorized in the budget for expenditure by an appropriation which applies excess revenues to prepay agency. -

Preparing a Short-Term Cash Flow Forecast

Preparing a short-term What is a short-term cash How does a short-term cash flow forecast and why is it flow forecast differ from a cash flow forecast important? budget or business plan? 27 April 2020 The COVID-19 crisis has brought the importance of cash flow A short-term cash flow forecast is a forecast of the The income statement or profit and loss account forecasting and management into sharp focus for businesses. cash you have, the cash you expect to receive and in a budget or business plan includes non-cash the cash you expect to pay out of your business over accounting items such as depreciation and accruals This document explores the importance of forecasting, explains a certain period, typically 13 weeks. Fundamentally, for various expenses. The forecast cash flow how it differs from a budget or business plan and offers it’s about having good enough information to give statement contained in these plans is derived from practical tips for preparing a short-term cash flow forecast. you time and money to make the right business the forecast income statement and balance sheet decisions. on an indirect basis and shows the broad categories You can also access this information in podcast form here. of where cash is generated and where cash is spent. Forecasts are important because: They are produced on a monthly or quarterly basis. • They provide visibility of your future cash position In contrast, a short-term cash flow forecast: and highlight if and when your cash position is going to be tight. -

Joint Analysis Enacted 2021-22 Budget July 13, 2021

Joint Analysis Enacted 2021-22 Budget July 13, 2021 Table of Contents BACKGROUND ..........................................................................................................3 INTRODUCTION ........................................................................................................3 BUDGET OVERVIEW ..................................................................................................3 Budget Shaped by recovery from covid-related Recession .............................................. 3 Investments focus on relief and recovery for californians................................................ 4 CALIFORNIA COMMUNITY COLLEGES FUNDING ..........................................................5 Immediate Action Package ............................................................................................... 5 Proposition 98 Estimates.................................................................................................. 6 California Community Colleges Funding Levels ............................................................... 6 Changes in Funding .......................................................................................................... 7 Local Support Funding by Program ................................................................................ 17 Capital Outlay ................................................................................................................. 21 State Operations ........................................................................................................... -

The Submarine and the Washington Conference Of

477 THE SUBMARINE AND THE WASHINGTON CONFERENCE OF 1921 Lawrence H. Douglas Following the First World War, the tation of this group, simply stated, was tide of public opinion was overwhelm that second best in naval strength meant ingly against the submarine as a weapon last. A policy of naval superiority was of war. The excesses of the German necessary, they felt, for "history consis U-boat had stunned the sensibilities of tently shows that war between no two the world but had, nonetheless, pre peoples or nations can be unthink sented new ideas and possibilities of this able.,,1 A second group, the Naval weapon to the various naval powers of Advisory Committee (Admirals Pratt the time. The momentum of these new and Coontz and Assistant Secretary of ideas proved so strong that by the the Navy Theodore Roosevelt, Jr.) also opening of the first major international submitted recommendations concerning disarmament conference of the 20th the limitation of naval armaments. century, practical uses of the submarine From the outset their deliberations were had all but smothered the moral indig guided by a concern that had become nation of 1918. more and more apparent-the threat Several months prior to the opening posed to the security and interests of of the conference, the General Board of this country by Japan. This concern was the American Navy was given the task evidenced in an attempt to gain basic of developing guidelines and recommen understandings with Britain. dations to be used by the State Depart The submarine received its share of ment in determining the American attention in the deliberations of these proposals to be presented. -

RF Annual Report

K.I: 10 •; i;.-/-,|i c /;-vi fiU |:-f I 1 l: 1 11 /: I; Y- ' ' The Rockefeller Foundation Annual Report 1921 The Rockefeller Foundation 61 Broadway, New York ,1 AH-fW M J) t-l Jl AO il MW I'l A,') Nil YMAJIH I.I >Uin Y W i M CONTENTS THE ROCKEFELLER FOUNDATION FACE President's Review 1 Report of the Secretary 75 Report of the Treasurer 339 INTERNATIONAL HEALTH BOARD Report of the General Director 85 Appendix 159 CHINA MEDICAL BOARD Report of the Director 243 DIVISION OF MEDICAL EDUCATION Report of the General Director... 311 ILLUSTRATIONS PAGE Map of world-wide activities of the Rockefeller Foundation 4-5 Full-time health workers in United States, 1921 IS Professional training of health officials 17 Students at work in the bacteriological laboratory of the School of Hygiene and Public Health of Johns Hopkins University 25 Class in protozoology, Johns Hopkins School of Hygiene and Public Health 25 Architect's drawing of proposed new building to house the School of Hygiene and Public Health of Johns Hopkins University 26 The " Pay Clinic " of Cornell University Medical College 26 Staff and students of the Peking Union Medical College 41 Academic procession at dedication of the Peking Union Medical College 42 A part of the academic procession at the dedication of the Peking Union Medical College, September 19, 1921 42 Map used in anti-malaria campaign in Louisiana 58 Yellow fever map of the Western Hemisphere 96 Scene of violent yellow fever epidemic in Peru during 1921....... 98 Three aspects of yellow fever control effort in Peru during 1921... -

British Security Policy in Ireland, 1920-1921: a Desperate Attempt by the Crown to Maintain Anglo-Irish Unity by Force

British Security Policy in Ireland, 1920-1921: A Desperate Attempt by the Crown to Maintain Anglo-Irish Unity by Force ‘What we are trying to do is to stop the campaign of assassination and arson, initiated and carried on by Sinn Fein, with as little disturbance as possible to people who are and who wish to be law abiding.’ General Sir Nevil Macready ‘outlining the British policy in Ireland’ to American newspaper correspondent, Carl W. Ackerman, on 2 April 1921.1 In the aftermath of victory in the Great War (1914-1918) and the conclusion to the peacemaking process at Versailles in 1919, the British Empire found itself in a situation of ‘imperial overstretch’, as indicated by the ever-increasing demands for Crown forces to represent and maintain British interests in defeated Germany, the Baltic and Black Seas regions, the Middle East, India and elsewhere around the world. The strongest and most persistent demand in this regard came from Ireland – officially an integral part of the United Kingdom itself since the Act of Union came into effect from 1 January 1801 – where the forces of militant Irish nationalism were proving difficult, if not impossible to control. Initially, Britain’s response was to allow the civil authorities in Ireland, based at Dublin Castle and heavily reliant on the enforcement powers of the Royal Irish Constabulary (RIC), to deal with this situation. In 1920, however, with a demoralised administration in Ireland perceived to be lacking resolution in the increasingly violent struggle against the nationalists, London -

Growing Your Business Through Mergers & Acquisitions

Growing Your Business Through Mergers & Acquisitions Mergers and acquisitions occur when companies consolidate, usually with a larger company acquiring a smaller company, or two companies merging their business activities. There can be many benefits of M&A such as increased growth, cost synergies, complementary product and service offerings, skilled talent, new markets, increased liquidity and much more. The current economic environment may present excellent opportunities for M&A. Suitors may find opportunities to acquire companies that may otherwise not be open to being acquired. Struggling companies may find a lifeline from a merger or acquisition. Even if neither company is struggling, combining forces may give companies the ability to aggressively gain market share when competitors are just trying to maintain the business that they have. Depending on your goals and options at hand, you may want to consider M&A as part of your company’s growth strategy. This article cover some of the benefits, challenges and key things to consider with M&A. Benefits One of the primary benefits of merging companies over more traditional forms of growth is the speed with which a merger can be implemented. Growth through traditional sales and marketing simply takes time. And, the more crowded and competitive a market, the more time it can take. Mergers, on the other hand, can often grow a business much faster - as quickly as the merger can be completed. Time may not be the only benefit from a customer and revenue growth perspective. Traditional sales and marketing can be expensive and carries a certain cost to acquire a customer. -

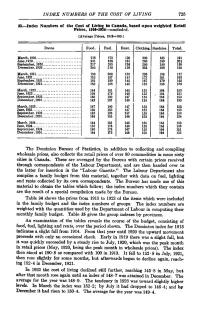

INDEX NUMBERS of the COST of LIVING 725 33.—Index Numbers of the Cost of Living in Canada, Based Upon Weighted Retail Prices

INDEX NUMBERS OF THE COST OF LIVING 725 33.—Index Numbers of the Cost of Living in Canada, based upon weighted Retail Prices, 1910-1934—concluded. (Average Prices, 1913=100.) Dates. Food. Fuel. Rent. Clothing. Sundries. Total. March, 1920 218 173 120 260 185 191 June,1920 231 186 133 260 190 201 September, 1920 217 285 136 260 190 199 December, 1920. 202 218 139 235 190 192 March, 1921 180 208 139 195 188 177 June,1921 152 197 143 173 181 163 September, 1921 161 189 145 167 170 162 December, 1921. 150 186 145 158 166 156 March, 1922 144 181 145 155 164 153 June, 1922 139 179 146 155 . 164 151 September, 1922. 140 190 147 155 164 153 December, 1922. 142 187 146 155 164 153 March, 1923 147 190 147 155 164 155 June,1923 139 182 147 155 164 152 September, 1923. 142 183 147 155 164 153 December, 1923. 146 185 146 155 164 154 March, 1924 144 181 146 155 164 153 June,1924 133 176 146 155 164 149 September, 1924. 140 176 147 155 164 151 December, 1924. 144 175 146 155 164 152 The Dominion Bureau of Statistics, in addition to collecting and compiling wholesale prices, also collects the retail prices of over 80 commodities in some sixty cities in Canada. These are averaged by the Bureau with certain prices received through correspondents of the Labour Department, and are then handed over to the latter for insertion in the "Labour Gazette." The Labour Department also compiles a family budget from this material, together with data on fuel, lighting and rents collected by its own correspondents. -

Debt Service Deeming Resolution Deferral of Budget Authority

Terms and Definitions Debt Service Payment of interest on, and repayment of principal on, borrowed funds. The term may also be used to refer to payment of interest alone. (See also Means of Financing.) As used in the Congressional Budget Office’s (CBO) Budget and Economic Outlook, debt service refers to a change in interest payments resulting from a change in estimates of the surplus or the deficit. Deeming Resolution An informal term that refers to a resolution or bill passed by one or both houses of Congress that in the absence of a concurrent resolution, serves for the chamber passing it as an annual budget resolution for purposes of establishing enforceable budget levels for a budget cycle. The Congressional Budget and Impoundment Control Act of 1974 requires the adoption each year of a concurrent resolution on the budget. (See Concurrent Resolution on the Budget.) At a minimum, deeming resolutions provide new spending allocations to the appropriations committees, but they also may set new aggregate budget levels, provide revised spending allocations to other House and Senate committees, or provide for other related purposes. A deeming resolution may even declare that a budget resolution (in its entirety), passed earlier in the session by one house is deemed to have the force and effect as if adopted by both houses. Deferral of Budget Authority Temporary withholding or delaying of the obligation or expenditure of budget authority or any other type of executive action, which effectively precludes the obligation or expenditure of budget authority. A deferral is one type of impoundment. Under the Impoundment Control Act of 1974 (2 U.S.C. -

IFRS Example Consolidated Financial Statements 2019

IFRS Assurance IFRS Example Global Consolidated Financial Statements 2019 with guidance notes Contents Introduction 1 19 Cash and cash equivalents 61 IFRS Example Consolidated Financial 3 20 Disposal groups classified as held for sale and 61 Statements discontinued operations Consolidated statement of financial position 4 21 Equity 63 Consolidated statement of profit or loss 6 22 Employee remuneration 65 Consolidated statement of comprehensive income 7 23 Provisions 71 Consolidated statement of changes in equity 8 24 Trade and other payables 72 Consolidated statement of cash flows 9 25 Contract and other liabilities 72 Notes to the IFRS Example Consolidated 10 26 Reconciliation of liabilities arising from 73 Financial Statements financing activities 1 Nature of operations 11 27 Finance costs and finance income 73 2 General information, statement of compliance 11 28 Other financial items 74 with IFRS and going concern assumption 29 Tax expense 74 3 New or revised Standards or Interpretations 12 30 Earnings per share and dividends 75 4 Significant accounting policies 15 31 Non-cash adjustments and changes in 76 5 Acquisitions and disposals 33 working capital 6 Interests in subsidiaries 37 32 Related party transactions 76 7 Investments accounted for using the 39 33 Contingent liabilities 78 equity method 34 Financial instruments risk 78 8 Revenue 41 35 Fair value measurement 85 9 Segment reporting 42 36 Capital management policies and procedures 89 10 Goodwill 46 37 Post-reporting date events 90 11 Other intangible assets 47 38 Authorisation -

Budget Management and Financial Reporting

BUDGET MANAGEMENT AND FINANCIAL REPORTING BUDGET MANAGEMENT AND FINANCIAL REPORTING Presented by: AMANDA DUNLAP COMMUNICATIONS & TRAINING COORDINATOR OFFICE OF FINANCE BRUCE AIRD UNIVERSITY BUDGET OFFICER BUDGET OFFICE February 16, 2017 Part of the Certificate in University Financial Management – revised February 16, 2017 BUDGET MANAGEMENT AND FINANCIAL REPORTING TABLE OF CONTENTS Overview and Objectives ............................................................................................................ 3 Definitions ................................................................................................................................... 4 Fund/Ledger Information ............................................................................................................ 8 Accrual Accounting .................................................................................................................... 11 Budget Management (Minding the Store) .................................................................................. 12 Establishing a New Budget ........................................................................................................ 12 Budget Unit Director’s Responsibilities .................................................................................... 13 Requesting Banner Finance Access ......................................................................................... 14 Master Signature List .................................................................................................................