Universal Registration Document 2020 | Societe Generale Group | and Chief Executive Officer

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Mybank Short Template Document

MyBank List of Buyer Banks MyBank May 2017 Classification: Public MyBank List of Buyer Banks May 2017 Classification: Public ALLIANZ BANK FINANCIAL ADVISORS SPA ALPHA BANK ALTO ADIGE BANCA - SUEDTIROL BANK B.C.C. DI BASILIANO B.C.C. DI RECANATI E COLMURANO B.C.C. SAN GIUSEPPE DI MUSSOMELI BANCA ADRIA CREDITO COOP. DEL DELTA BANCA ALPI MARITTIME - CC CARRU BANCA ALTO VICENTINO BANCA ATESTINA CC BANCA CENTRO EMILIA BANCA CENTROPADANA BANCA CR FIRENZE S.P.A. BANCA CRAS BANCA D'ALBA CREDITO COOPERATIVO BANCA DEI COLLI EUGANEI BANCA DEL PIEMONTE SPA BANCA DELLA MARCA C.C. BANCA DI BOLOGNA BANCA DI CAPRANICA CREDITO COOP. BANCA DI CARAGLIO RIVIERA DEI FIORI BANCA DI CARNIA E GEMONESE BANCA DI CASCINA CREDITO COOP. BANCA DI CESENA BANCA DI CHERASCO BANCA DI FILOTTRANO BANCA DI FORLI BANCA DI FRASCATI BANCA DI IMOLA SPA BANCA DI MONASTIER E DEL SILE BANCA DI PESARO Page 1 of 7 MyBank List of Buyer Banks MyBank May 2017 Classification: Public BANCA DI PIACENZA SCPA BASSANO BANCA BANCA DI TARANTO BANCA DI VERONA CC CADIDAVID BANCA DON RIZZO CC SICILIA OCC. BANCA FIDEURAM BANCA FINNAT EURAMERICA SPA BANCA GENERALI SPA BANCA ITB S.P.A. BANCA MALATESTIANA BANCA MONTE PRUNO BANCA NUOVA SPA BANCA PATAVINA BANCA POPOLARE - VOLKSBANK BANCA POPOLARE DEL LAZIO SCPA BANCA POPOLARE DI MILANO BANCA POPOLARE DI SONDRIO BANCA POPOLARE DI VICENZA S.P.A. BANCA POPOLARE ETICA BANCA POPOLARE PUGLIESE BANCA POPOLARE VALCONCA SCPA BANCA PROSSIMA S.P.A. BANCA S.BIAGIO DEL VENETO ORIENTALE BANCA SISTEMA SPA BANCA SVILUPPO COOPERAZ. CREDITO BANCA SVILUPPO TUSCIA BANCA VALSABBINA S.C.P.A. -

Elenco Dei Soggetti Richiedenti Che Operano Con Il Fondo, Con Specifica

Elenco dei soggetti richiedenti che operano con il Fondo – account abilitati all’utilizzo della procedura telematica - Ottobre 2020 (informativa ai sensi del Piano della Trasparenza - parte X delle Disposizioni operative) DENOMINAZIONE SOGGETTO RICHIEDENTE COGNOME NOME E-MAIL TELEFONO AAREAL BANK MAZZA ANTONIO [email protected] 0683004228 AAREAL BANK CIPOLLONE LORELLA [email protected] 0683004305 AGFA FINANCE ITALY SPA CRIPPA ANTONELLA [email protected] 023074648 AGFA FINANCE ITALY SPA BUSTI FILIPPO [email protected] AGRIFIDI ZAPPA GIUSEPPE [email protected] 3371066673 AGRIFIDI EMILIA ROMAGNA TEDESCHI CARLO ALBERTO [email protected] 05211756120 AGRIFIDI MODENA REGGIO FERRARA TINCANI ENNIO EMANUELE [email protected] 059208524 AGRIFIDI UNO EMILIA ROMAGNA EVANGELISTI CARLOTTA [email protected] 0544271787 AGRIFIDI UNO EMILIA ROMAGNA MONTI LUCA [email protected] 0544271787 A-LEASING SPA LOMBARDO CLAUDIO [email protected] 0422409820 ALLIANZ BANK FINANCIAL ADVISORS PISTARINO FRANCA [email protected] 0131035420 ALLIANZ BANK FINANCIAL ADVISORS CORIGLIANO FABIO [email protected] 0272168085 ALLIANZ BANK FINANCIAL ADVISORS CHIARI STEFANO [email protected] 0272168518 ALLIANZ BANK FINANCIAL ADVISORS CANNIZZARO FEDERICO [email protected] 3421650350 ALLIANZ BANK FINANCIAL ADVISORS KOFLER SAMUEL [email protected] 3466001059 ALLIANZ BANK FINANCIAL ADVISORS FERRARI PIERO [email protected] 3477704188 ALLIANZ -

Relazione Sull'attività Dell'arbitro Bancario Finanziario

Relazione sull’attività dell’Arbitro Bancario Finanziario Appendice numero anno 2019 10 Relazione sull’attività dell’Arbitro Bancario Finanziario Appendice anno 2019 Numero 10 - luglio 2020 © Banca d’Italia, 2020 Indirizzo Via Nazionale, 91 00184 Roma - Italia Telefono +39 06 47921 Sito internet http://www.bancaditalia.it ISSN 2281-4809 (online) Tutti i diritti riservati. È consentita la riproduzione a fini didattici e non commerciali, a condizione che venga citata la fonte. Grafica a cura della Divisione Editoria e stampa della Banca d’Italia INDICE DATI STATISTICI 5 Tav. 1 Ricorsi ricevuti per tipologia di intermediario 7 “ 2 Ricorsi ricevuti e decisi per tipologia di ricorrente 7 “ 3 Ricorsi dei consumatori per area rispetto alla popolazione 7 “ 3bis Ricorsi dei consumatori per regione 8 “ 4 Ricorsi ricevuti per oggetto della controversia 9 “ 5 Ricorsi decisi e numero di riunioni per mese 10 “ 6 Ricorsi ricevuti ed esito per Collegio 10 “ 7 Ricorsi ricevuti per intermediario 11 “ 7bis Ricorsi ricevuti per intermediario e incidenza sul totale ABF 18 “ 8 Ricorsi decisi per intermediario 18 “ 9 Intermediari inadempienti 26 “ 10 Ricorsi decisi per gruppo bancario: primi 10 gruppi per ricorsi decisi nell’anno 27 NOTE METODOLOGICHE 28 Appendice Anno 2019 Relazione sull’attività dell’Arbitro Bancario Finanziario 3 DATI STATISTICI Tavola 1 Ricorsi ricevuti per tipologia di intermediario (1) (unità e valori percentuali) 2018 2019 Variaz. 2018 2019 INTERMEDIARIO Unità Unità % % % Banche 17.577 12.513 -29 65,0 56,7 di cui: banche spa 15.159 11.539 -24 56,0 52,3 banche estere 1.986 543 -73 7,3 2,5 banche popolari 226 243 8 0,8 1,1 banche di credito cooperativo 206 189 -8 0,8 0,9 Società finanziarie 6.618 4.977 -25 24,5 22,6 Poste Italiane spa 2.345 3.672 57 8,7 16,6 Istituti di pagamento 55 36 -35 0,2 0,2 Confidi 7 8 14 0,0 0,0 Imel 282 804 185 1,0 3,6 Soggetti non tenuti ad aderire 163 48 -71 0,6 0,2 Totale 27.047 22.059 -18 100 100 (1) Il dato del 2018 riflette la classificazione dell’intermediario al 31 dicembre 2019. -

Rilevazione Dei Dati Granulari Sul Credito: Istruzioni Per Gli Intermediari Segnalanti”

ELENCO ENTI CREDITIZI SEGNALANTI MENSILMENTE 1 ai sensi del Capitolo 1 della Circolare n. 297 del 16 maggio 2017 “Rilevazione dei dati granulari sul credito: istruzioni per gli intermediari segnalanti” ENTI CREDITIZI OPERANTI IN ITALIA Soggetto Operatore Prima data Paese dichiarante monitorato Denominazione dell'Operatore Modello Modello contabile casa [Reporting [Observed monitorato [Observed Agent (Template) (Template) [First madre Agent] Agent] (codice description] 1 2 reference [Home (codice ABI) censito) date] country] BANCA NAZIONALE DEL LAVORO 1005 0002733874564 S.P.A. (IN FORMA CONTRATTA Si Si 30/06/2018 IT BNL S.P.A.) 1015 0000865027966 BANCO DI SARDEGNA S.P.A. Si Si 30/06/2018 IT BANCA MONTE DEI PASCHI DI 1030 0000203426147 Si Si 30/06/2018 IT SIENA S.P.A. UNICREDIT, SOCIETA' PER 2008 0000102484824 Si Si 30/06/2018 IT AZIONI 3009 0000959743258 FCE BANK PLC Si Si 30/06/2018 GB FINECOBANK BANCA FINECO 3015 0000364341654 Si Si 30/06/2018 IT S.P.A. 0000828560480 INVEST BANCA SOCIETA' PER 3017 Si Si 30/09/2022 IT AZIONI 3021 0000430754720 HSBC BANK PLC Si Si 30/06/2018 GB 3025 0000710833803 BANCA PROFILO S.P.A. Si Si 30/06/2018 IT 3030 0000270254364 DEXIA CREDIOP S.P.A. Si Si 30/06/2018 IT 3032 0000126876530 CREDITO EMILIANO S.P.A. Si Si 30/06/2018 IT 3040 0000671441052 CREDIT SUISSE AG Si Si 30/06/2018 CH BANCA INTERMOBILIARE DI 3043 0000300865080 INVESTIMENTI E GESTIONI Si Si 30/06/2018 IT SOCIETA' PER AZIONI 3045 0000422149578 BANCA AKROS S.P.A. Si Si 30/06/2018 IT 3048 0000100240817 BANCA DEL PIEMONTE S.P.A. -

Elenco Banche Convenzionate

OFFERTA XPAY: ELENCO BANCHE 1015 Banco di Sardegna SpA 1030 Banca Monte dei Paschi di Siena SpA 3011 Hypo Alpe Adria Bank 3019 Credito Siciliano 3032 Credito Emiliano SpA 3047 Banca Capasso 3048 Banca del Piemonte SpA 3062 Banca Mediolanum SpA 3083 Ubi Banca Private Investment SpA 3087 Banca Finnat 3084 Banca Cesare Ponti 3104 Deutsche Bank SpA 3111 Unione di Banche Italiane SpA 3124 Banca del Fucino SpA 3127 UGF Banca SpA 3138 Banca Reale 3141 Banca di Treviso 3158 Banca Sistema SpA 3165 IW Bank SpA 3177 Banca Sai SpA 3185 Banca Ifigest 3204 Banca di Legnano 3229 Banca Modenese Spa 3242 Banco di Lucca 3253 Banca Federico Del Vecchio 3259 Nordest Banca 3262 Asset Banca 3265 Banca Promos SpA 3287 Banca Sammarinese d’Investimenti 3301 Carimilo - Cassa dei Risparmi di Milano e della Lombardia 3310 Eticredito Banca Etica Adriatica 3317 Banca della Provincia di Macerata 3323 GBM Banca 3332 Banca Passadore & C. SpA 3336 Credito Bergamasco Offerta XPay: Elenco Banche 1 di 4 3338 Banca Serfina 3353 Banca del Sud 3399 Extra Banca 3403 Imprebanca 3425 Banco di Credito P. Azzoaglio SpA 3426 Credito Peloritano 3440 Banco di Desio e della Brianza 3488 Cassa Lombarda 3493 Cassa Centrale Raiffeisen dell’Alto Adige SpA 3512 Credito Artigiano 3566 Citibank National Associaton 3589 Allianz Bank 3599 Cassa Centrale Banca - Cred. Coop. del Nord Est SpA 5000 Istituto Centrale Banche Popolare Italiane 5018 Banca Popolare Etica 5023 Banca Regionale Sviluppo 5030 Credito Salernitano 5034 Banco Popolare Soc. Coop. 5035 Veneto Banca Holding SpA 5036 Banca Agricola -

List of Significant and Less Significant Supervised Institutions

List of supervised entities Cut-off date for changes in group structures: 1 November 2018 Cut-off date for significance decisions: 14 December 2018 Number of significant supervised entities: 119 This list displays the significant (part A) and less significant credit institutions (part B) w hich are supervised entities. The list is compiled on the basis of significance decisions adopted and notified by the ECB that refer to events that became effective up to the cut-off date. A. List of significant supervised entities Country of LEI Type Name establishment Grounds for significance MFI code for branches of group entities Belgium 1 LSGM84136ACA92XCN876 Credit Institution AXA Bank Belgium SA ; AXA Bank Belgium NV Size (total assets EUR 30-50 bn) (**) CVRWQDHDBEPUUVU2FD09 Credit Institution AXA Bank Europe SCF France Banque Degroof Petercam SA ; Bank Degroof 2 549300NBLHT5Z7ZV1241 Credit Institution Significant cross-border assets Petercam NV 54930017BFF0C5RWQ245 Credit Institution Banque Degroof Petercam France S.A. France NCKZJ8T1GQ25CDCFSD44 Credit Institution Banque Degroof Petercam Luxembourg S.A. Luxembourg 95980020140005218292 Credit Institution Bank Degroof Petercam Spain, S.A. Spain Belfius Banque SA ; Belfius Bank NV ; Belfius Bank 3 A5GWLFH3KM7YV2SFQL84 Credit Institution Size (total assets EUR 100-150 bn) SA 4 D3K6HXMBBB6SK9OXH394 Financial Holding Dexia SA Size (total assets EUR 150-300 bn) F4G136OIPBYND1F41110 Credit Institution Dexia Crédit Local France 52990081RTUT3DWKA272 Credit Institution Dexia Kommunalbank Deutschland GmbH -

ELENCO ADERENTI AI CIRCUITI BANCOMAT®E Pagobancomat® AGGIORNATO Al 13 Maggio 2020

ELENCO ADERENTI AI CIRCUITI BANCOMAT®e PagoBANCOMAT® AGGIORNATO al 13 maggio 2020 Prog Cod ABI Cod. ABI Cod_ABI_ DENOMINAZIONE INDIRIZZO SEDE LEGALE COD. FISC. CAP Alias CapoGru CITTA' ppo 1 01005 01005 BANCA NAZIONALE DEL LAVORO - S.P.A. VIALE ALTIERO SPINELLI, 30 ROMA 09339391006 00157 2 01015 05387 BANCO DI SARDEGNA - S.P.A. VIALE BONARIA, 33 CAGLIARI 01564560900 09125 3 01030 01030 BANCA MONTE DEI PASCHI DI SIENA - S.P.A. PIAZZA SALIMBENI, 3 SIENA 00884060526 53100 4 02008 02008 UNICREDIT S.P.A. P.ZA G. AULENTI, 3 - TOWER A MILANO 00348170101 20154 5 03015 03015 FINECOBANK BANCA FINECO - S.P.A. PIAZZA DURANTE 11 MILANO 01392970404 20131 6 03017 03017 INVEST BANCA - S.P.A. VIA CHERUBINI, 99 EMPOLI (FI) 02586460582 50053 7 03032 03032 CREDITO EMILIANO S.P.A. VIA EMILIA S. PIETRO, 4 REGGIO EMILIA 01806740153 42100 8 03034 03034 BANCA AGRICOLA COMMERCIALE ISTITUTO BANCARIO SAMMARINESE S.P.A. VIA TRE SETTEMBRE, 316 DOGANA REPUBBLICA S. MARINO (SM) SM00087 47031 9 03043 03043 BANCA INTERMOBILIARE DI INVESTIMENTI E GESTIONI - S.P.A. VIA GRAMSCI, 7 TORINO 02751170016 10121 10 03047 03599 BANCA CAPASSO ANTONIO - S.P.A. PIAZZA TERMINI, 1 ALIFE (CE) 00095310611 81011 11 03048 03048 BANCA DEL PIEMONTE - S.P.A. VIA CERNAIA, 7 TORINO 00821100013 10121 12 03058 03058 CHE BANCA! - S.P.A. VIA LUIGI BODIO, 37 MILANO 10359360152 20158 13 03062 03062 BANCA MEDIOLANUM - S.P.A. VIA F. SFORZA - PAL. MEUCCI MILANO 3 BASIGLIO (MI) 02124090164 20080 14 03069 03069 INTESA SANPAOLO - S.P.A. P.ZZA SAN CARLO, 156 TORINO 00799960158 10121 15 03075 03075 BANCA GENERALI - S.P.A. -

Survey on Italian Household Income and Wealth in 2016

SURVEY ON ITALIAN HOUSEHOLD INCOME AND WEALTH IN 2016 QUESTIONNAIRE FOR THE REFERENCE PERSON OF THE HOUSEHOLD 1. QUESTIONNAIRE No. |__|__|__|__|__|__|__| (enter the number from the list of names) NQUEST (for new households formed from former PANEL households enter the QUESTIONNAIRE No. for the original panel household and tick the box on the right ) ¶ 2. DATE OF INTERVIEW: |__|__| / |__|__| / 2017 DATA11* DATA12* 3. TIME OF INTERVIEW: | | |,| | | ORA11* ORA12* 4. NAME OF INTERVIEWER __________________________________________________________ 5. CODE OF INTERVIEWER | | | | | | | I I CODINT* _________________________________________________________ 6. PLACE OF INTERVIEW: ICOM* IPROV* _________________________________________________________ 7. TYPE OF SAMPLE UNIT: QUEST - New: unit drawn from primary list (O) .......................................................1 replacement drawn from reserve list (R) .........................................2 - Panel (interviewed in 2015) (P) ........................................................................3 - New household formed by member of panel household (ex PANEL ) ............. 4 NQUESTP CONTINT 8. How many times did you contact the household in order to obtain the interview? (Including present interview) No. | | 9. Random number rotation assigned to the family : Rotation 1............................. 1 ROTAZIONE Rotation 2 ............................ 2 i THE VARIABLES MARKED WITH THE SYMBOL * ARE NOT AVAILABLE FOR OUTSIDE USERS i THE VARIABLES MARKED WITH THE SYMBOL € ARE AMONG THE VARIABLES OF THE HARMONIZED SURVEY IN THE EURO AREA (http://www.ecb.int/home/html/researcher_hfcn.en.html ) 1 A. COMPOSITION OF HOUSEHOLD ON 31-12-2016 ALL HOUSEHOLD MEMBERS I would first like to record the composition of the household. Please list all household members on 31-12-2016. (Include all persons normally living in the dwelling on 31-12-2016 who contributed at least part of their income to the household. -

A. List of Significant Supervised Entities

List of supervised entities Cut-off date for significance decisions: 01 January 2016 Number of significant supervised entities: 129 A. List of significant supervised entities Belgium Name Country of Grounds for establishment significance of the group entities Investeringsmaatschappij Argenta nv Size (total assets EUR 30 - 50 bn) Argenta Bank- en Verzekeringsgroep nv Belgium Argenta Spaarbank NV Belgium AXA Bank Europe SA Size (total assets EUR 30-50 bn) AXA Bank Europe SCF France Banque Degroof Petercam SA Significant cross-border assets Banque Degroof Petercam France S.A. France Banque Degroof Luxembourg S.A. Luxembourg Privat Bank Degroof, S.A.U. Spain Belfius Banque S.A. Size (total assets EUR 150-300 bn) Dexia NV Size (total assets EUR 150-300 bn) Dexia Crédit Local France Dexia Flobail France Dexia CLF Banque France Dexia CLF Régions Bail France Dexia Kommunalbank Deutschland AG Germany Dexia Crediop S.p.A. Italy Dexia Sabadell, S.A. Spain KBC Group N.V. Size (total assets EUR 150-300 bn) KBC Bank N.V. Belgium CBC Banque Belgium KBC Bank Ireland plc Ireland Československá obchodná banka, a.s. Slovakia ČSOB stavebná sporiteľňa, a.s. Slovakia The Bank of New York Mellon S.A. Size (total assets EUR 50-75 bn) Germany Name Country of Grounds for establishment significance of the group entities Aareal Bank AG Size (total assets EUR 50-75 bn) Westdeutsche ImmobilienBank AG Germany Bayerische Landesbank Size (total assets EUR 150-300 bn) Deutsche Kreditbank Aktiengesellschaft Germany COMMERZBANK Aktiengesellschaft Size (total assets EUR 500-1,000 bn) European Bank for Financial Services GmbH (ebase) Germany Hypothekenbank Frankfurt AG Germany comdirect bank AG Germany Commerzbank International S.A. -

ELENCO ADERENTI AI CIRCUITI BANCOMAT E Pagobancomat

ELENCO ADERENTI AI CIRCUITI BANCOMAT® e PagoBANCOMAT® AGGIORNATO al 1 dicembre 2020 Prog Cod ABI Cod. ABI Cod_ABI_CapoGruppo DENOMINAZIONE INDIRIZZO SEDE LEGALE COD. FISC. CAP Alias CITTA' 1 01005 01005 BANCA NAZIONALE DEL LAVORO - S.P.A. VIALE ALTIERO SPINELLI, 30 ROMA 09339391006 00157 2 01015 05387 BANCO DI SARDEGNA - S.P.A. VIALE BONARIA, 33 CAGLIARI 01564560900 09125 3 01030 01030 BANCA MONTE DEI PASCHI DI SIENA - S.P.A. PIAZZA SALIMBENI, 3 SIENA 00884060526 53100 4 02008 02008 UNICREDIT S.P.A. PIAZZA G. AULENTI, 3 - TOWER A MILANO 00348170101 20154 5 03015 03015 FINECOBANK BANCA FINECO - S.P.A. PIAZZA DURANTE, 11 MILANO 01392970404 20131 6 03017 03017 INVEST BANCA - S.P.A. VIA CHERUBINI, 99 EMPOLI (FI) 02586460582 50053 7 03032 03032 CREDITO EMILIANO S.P.A. VIA EMILIA S. PIETRO, 4 REGGIO EMILIA 01806740153 42121 8 03034 03034 DOGANA REPUBBLICA S. MARINO SM00087 47891 BANCA AGRICOLA COMMERCIALE ISTITUTO BANCARIO SAMMARINESE S.P.A. VIA TRE SETTEMBRE, 316 (RSM) 9 03043 03043 BANCA INTERMOBILIARE DI INVESTIMENTI E GESTIONI - S.P.A. VIA SAN DALMAZZO, 15 TORINO 02751170016 10122 10 03047 03599 BANCA CAPASSO ANTONIO - S.P.A. PIAZZA TERMINI, 1 ALIFE (CE) 00095310611 81011 11 03048 03048 BANCA DEL PIEMONTE - S.P.A. VIA CERNAIA, 7 TORINO 00821100013 10121 12 03058 03058 CHE BANCA! - S.P.A. VIA LUIGI BODIO, 37 MILANO 10359360152 20158 13 03062 03062 BANCA MEDIOLANUM - S.P.A. VIA F. SFORZA - PAL. MEUCCI MILANO 3 BASIGLIO (MI) 02124090164 20079 14 03069 03069 INTESA SANPAOLO - S.P.A. PIAZZA SAN CARLO, 156 TORINO 00799960158 10121 15 03075 03075 BANCA GENERALI - S.P.A. -

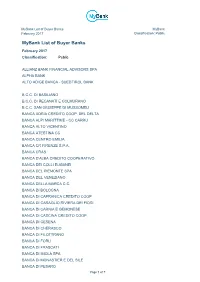

Mybank Short Template Document

MyBank List of Buyer Banks MyBank February 2017 Classification: Public MyBank List of Buyer Banks February 2017 Classification: Public ALLIANZ BANK FINANCIAL ADVISORS SPA ALPHA BANK ALTO ADIGE BANCA - SUEDTIROL BANK B.C.C. DI BASILIANO B.C.C. DI RECANATI E COLMURANO B.C.C. SAN GIUSEPPE DI MUSSOMELI BANCA ADRIA CREDITO COOP. DEL DELTA BANCA ALPI MARITTIME - CC CARRU BANCA ALTO VICENTINO BANCA ATESTINA CC BANCA CENTRO EMILIA BANCA CR FIRENZE S.P.A. BANCA CRAS BANCA D'ALBA CREDITO COOPERATIVO BANCA DEI COLLI EUGANEI BANCA DEL PIEMONTE SPA BANCA DEL VENEZIANO BANCA DELLA MARCA C.C. BANCA DI BOLOGNA BANCA DI CAPRANICA CREDITO COOP. BANCA DI CARAGLIO RIVIERA DEI FIORI BANCA DI CARNIA E GEMONESE BANCA DI CASCINA CREDITO COOP. BANCA DI CESENA BANCA DI CHERASCO BANCA DI FILOTTRANO BANCA DI FORLI BANCA DI FRASCATI BANCA DI IMOLA SPA BANCA DI MONASTIER E DEL SILE BANCA DI PESARO Page 1 of 7 MyBank List of Buyer Banks MyBank February 2017 Classification: Public BANCA DI PIACENZA SCPA BANCA DI ROMANO E S.CATERINA BANCA DI TARANTO BANCA DI VERONA CC CADIDAVID BANCA DON RIZZO CC SICILIA OCC. BANCA FIDEURAM BANCA FINNAT EURAMERICA SPA BANCA GENERALI SPA BANCA ITB S.P.A. BANCA MALATESTIANA BANCA NUOVA SPA BANCA PATAVINA BANCA POPOLARE - VOLKSBANK BANCA POPOLARE DEL LAZIO SCPA BANCA POPOLARE DI MILANO BANCA POPOLARE DI SONDRIO BANCA POPOLARE DI VICENZA S.P.A. BANCA POPOLARE ETICA BANCA POPOLARE PUGLIESE BANCA POPOLARE VALCONCA SCPA BANCA PROSSIMA S.P.A. BANCA S.BIAGIO DEL VENETO ORIENTALE BANCA SISTEMA SPA BANCA SVILUPPO COOPERAZ. -

Financial Statements at December 31, 2011 Iccrea Bancaimpresa S.P.A

Financial Statements 2o11 Financial Statements at December 31, 2011 Iccrea BancaImpresa S.p.A Iccrea BancaImpresa S.p.A ICCREA BANKING GROUP INDEX Shareholders ................................................................................................................. 1 Corporate Officers .......................................................................................................... 7 Calling of Ordinary Shareholders’ Meeting .............................................................................. 8 Report on operations ....................................................................................................... 9 Balance Sheet............................................................................................................... 37 Income Statement ......................................................................................................... 39 Statement of changes in shareholders' equity ......................................................................... 41 Statement of cash flows (Indirect method) ............................................................................ 43 Part A – Accounting Policies .............................................................................................. 45 Part B – Information on the Balance Sheet ............................................................................. 69 Part C – Information on the Income Statement ...................................................................... 119 Part D – Comprehensive Income .......................................................................................