A New Multinomial Accuracy Measure for Polling Bias

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Pâques À Juhègues Sant Jordi Élections Présidentielles

Vendredi 14 avril 2017 N° 1154 QUAND LA "CARXOFA" FAIT LE BUZZZ ! L’artichaut de la Salanque est l'un des symboles du patrimoine agricole et culturel de notre commune. Cultivé sur nos terres depuis le 18ème siècle, il retrouve une place de choix sur les étals des maraîchers de toute la France après que des passionnés aient obtenu en 2015 la création d’une "indication géographique protégée" (IGP) qui lui a permis d’asseoir sa notoriété. Après quelques années difficiles, les ventes ont presque doublé en quatre ans et la production est en hausse avec cette année plusieurs semaines d’avance sur les artichauts de Bretagne. Une belle performance pour notre produit phare qui lui a valu un coup de projecteur de différents médias ces dernières semaines (L’Agri, l’Indépendant, France 3…). Félicitations à tous nos producteurs, notre mascotte Xofi est fière de vous ! LE ROND-POINT DE LA PLAGE S’OFFRE UNE OUVERTURE D'importants travaux ont débuté au niveau du rond-point de croisement des routes inter-plages et RD11E. Afin de fluidifier la circulation souvent chargée en saison dans le sens sortant de Torreilles plage et limiter la formation de bouchons sur le boulevard, une bretelle d'évitement du rond-point en direction de l'autoroute est en effet en cours de réalisation. Elle sera accompagnée de la mise à deux voies de la sortie du boulevard sur le rond-point. Les conditions de circulation des torreillans habitant la plage et des touristes devraient être significativement améliorées par ces aménagements, et ce dès cet été puisque le chantier sera achevé avant la saison estivale. -

Athis-Mons Info N°29 Complet

n°29 Mai / Juin en images 2-3 JUILLET - AOÛT 2004 Spécial ORU 4 Dossier : un été à Athis-Mons 5-8 Tribune libre 9 État civil - Brèves 10 Élections 11 Actualités 12 www.mairie-athis-mons.fr SOMMAIRE Tél : 01 69 54 54 54 POINT FORT UN ÉTÉ À de l'environnement, notre ville ne serait pas ce qu'elle est aujourd'hui sans l'action des équipes municipales qu'elle a conduites. Maire ATHIS-MONS adjoint à ses côtés de 1989 à 1995 , puis maire de la com- mune lorsqu'elle a été appe- lée à participer au gouverne- ment de Lionel Jospin, j'ai conscience de l'immense © DR. tâche qu'elle a accomplie. Sa e 13 juin dernier, pugnacité à défendre les Marie-Noëlle Liene- intérêts de notre ville, son mann était élue combat contre les injustices députée européenne et les inégalités, son attache- dans la région Nord ment aux valeurs républicai- LPas de Calais. Elle mettait nes, sa conviction dans un ainsi un terme à son engage- service public fort au service ment politique en Essonne, de tous restent, pour nomb- après avoir démissionné de re d'entre nous, des référen- ses mandats de Présidente de ces dans ce que l'action poli- la Communauté de Commu- tique a de plus noble. Depuis nes Les Portes de l'Essonne et 2001, l'équipe municipale de d'élue d'Athis-Mons il y a gauche renouvelée que j'ani- quelques semaines. me s'attache à consolider le Je tenais à lui rendre un travail engagé, à améliorer hommage tout particulier en sans cesse le service rendu saluant chaleureusement aux habitants et à préserver l'action qu'elle a menée, qui et valoriser les atouts de aura donné à notre ville une notre ville dans un environ- dimension et un dynamisme nement social et écono- sans précédent. -

30Th Anniversary Conference of the Schiller Institute

The Schiller Institute The New Silk Road and China’s Lunar Program: MANKIND IS THE ONLY CREATIVE SPECIES! 30th Anniversary Conference of the Schiller Institute OCTOBER 18-19, 2014 FRANKFURT AM MAIN, GERMANY SATURDAY, 18.10.2014 8:30 – 9:45 Registration 10:00 – 10:15 Musical offering PANEL I: The New Silk Road is Transforming the Planet 10:15 – 11:00 Keynote: A New Era of Mankind Helga Zepp-LaRouche, President of the Schiller Institute 11:00 – 11:20 Some Innovative Ideas Concerning the Mode of Cooperation along the Silk Road Prof. Shi Ze, China Institute of International Studies, Beijing, China 11:20 – 11:40 Iran’s Role in the New Silk Road Strategy in the Third Millennium Dr. Fatemeh Hashemi, President of WSA (Women’s Solidarity Association), Teheran, Islamic Republic of Iran 11:40 – 12:00 BRICS and the New International World Order Jayshree Sengupta, Senior Fellow, Observer Research Foundation, New Delhi, India 12:00 – 12:20 A Constructive Alternative to the Existing World Order, and Stability in Ukraine – Pathway to Saving Mankind Natalja Vitrenko, Economist, Chairwoman of the Progressive Socialist Party of Ukraine, Kiev, Ukraine 12:20 – 12:40 A Vision of the Future of Eurasia Ali Rastbeen, Founder and President of Paris Academy of Geopolitics, Paris, France Discussion 13:30 – 14:30 Lunch PANEL II: The Future of Europe – Transatlantic Collapse or Alliance of Sovereign Republics? 14:30 – 14:50 The Role of Steel in the New Silk Road Perspective Professor Dr. Dieter Ameling, President of the German Steel Federation (until 2008), Essen, Germany 15:20 – 15:40 Greece and the Silk Road Economic Belt Panos Kammenos, Chairman of the Independent Greeks, Member of Hellenic Parliament, Athens, Greece 15:40 – 16:00 Mediterranean Bridging Professor Enzo Siviero, Member of Italian National Council of Universities, Venice, Italy 16:00 – 16:20 Common Security Interests in Eurasia Col. -

Facing the Coming Crash of the Financial System

Click here for Full Issue of EIR Volume 32, Number 30, July 29, 2005 EIRBerlin Seminar Facing the Coming Crash Of the Financial System EIR’s June 28-29 seminar in Berlin brought together distin- follow-up presentation by Jacques Cheminade, the LaRouche guished representatives of 15 nations, to discuss what had to movement’s chief representative in France. be done to address the coming crash of the world financial system. In the keynote to the meeting, Lyndon LaRouche The Global Overview stressed not only the nature of the worldwide reorganization While EIR is working toward producing an English- that was required, but made a sharp polemical point about the language proceedings of the conference as a whole, we con- fact that it is from the United States, despite the character of sider it a priority to provide our readers with all the major the current occupants of the White House, that the positive presentations, which often dealt with the economic and strate- change has to be initiated, and soon. gic problems being faced in Eurasia, and with Lyndon After reviewing the history of the founding of the United LaRouche’s response to those presentations, as soon as pos- States, based on the best republican principles developed in sible. Europe, LaRouche put it this way: “So therefore, the United So far, we have published the speeches of LaRouche States is crucial, in this respect: The United States is crucial, (July 8); Helga Zepp-LaRouche (July 15); Italian parliamen- because we have an economic system which is not the so- tarian Mario Lettieri (July 15); Russian parliamentarian called capitalist system. -

Executive Intelligence Review, Volume 34, Number 22, June 1, 2007

Executive Intelligence Review EIRJune 1, 2007 Vol. 34 No. 22 www.larouchepub.com $10.00 Moscow Report: An FDR Policy for the Next 20 Years Only Four-Power Alliance Can Stop World War III Man and the Skies Above LaRouche Warning: ‘Democrats, Wake Up!’ SEE LAROUCHE ON CABLE TV All programs are The LaRouche Connection unless otherwise noted. (*) Call station for times. INTERNET • SANTA MONICA • CAMBRIDGE • ST.CROIX VLY. • ERIE COUNTY • STATEWIDE • LAROUCHEPUB.COM T/W Ch.77 Comcast Ch. 10 Comcast Ch.14 Adelphia Ch.20 RI Interconnect Click LaRouche Writings Wed: 3-3:30 pm Tue: 2:30 pm Thu: 1 & 7 pmThu: 10:35 pm Cox Ch.13 (Available 24/7) • VENTURA CITY Fri: 10:30 am Fridays—9 am • IRONDEQUOIT Tue:10-10:30 am • MNN.ORG T/W-Wave Ch.6 • WALPOLE • ST.PAUL T/W Ch.15 TEXAS Click on Watch Now Mon: 7 am Comcast Ch.8 (city only) Mon/Thu: 7 pm • DALLAS TW/67-RCN/86 Fri: 10 am Tue: 1-1:30 pm Comcast Ch.15 • JEFFERSON Comcast Ch.13-B Fri: 2 am • VENTURA COUNTYMICHIGAN Fri: 11 pm • LEWIS Tue: 10:30 pm (Eastern Time only) T/W Ch.8/16/25• BYRON CENTER • St.PAUL T/W Ch.99 • EL PASO CTY • SCANTV.ORG Mon: 1 pmComcast Ch.25 (S&W suburbs) Unscheduled pop-ins T/W Ch.15 Click Scan on the Web • WALNUT CREEKMon: 2&7pm Comcast Ch.15 • MANHATTAN Wed: 5:05 pm Sat: 2 pm Comcast Ch.6• DETROIT Wed: 10:30 am T/W Ch.67 RCN Ch.86 • HOUSTON (Pacific Time only) 2nd Tue: 7 pmComcast Ch.68 Fri: 7:30 pm Fri: 2 am T/W Ch.17 • WUWF.ORG Astound Ch.31Unscheduled pop-ins • S.WASHINGTON • NIAGARA/ERIE TV Max Ch.95 Click Watch WUWF-TV Tue: 7:30 pm• KALAMAZOO Comcast Ch.14 T/W Ch.20 Wed: 5:30 pm Last Mon: 4:30-5 pm • W.SAN FDO.VLY.Charter Ch. -

Le Mouvement Larouche À L'international

LE MOUVEMENT LAROUCHE À L’INTERNATIONAL Julien Giry To cite this version: Julien Giry. LE MOUVEMENT LAROUCHE À L’INTERNATIONAL. Politeia - Les Cahiers de l’Association Française des Auditeurs de l’Académie Internationale de Droit constitutionnel, Associ- ation française des auditeurs de l’Académie internationale de droit constitutionnel, 2016, 28. hal- 01686670 HAL Id: hal-01686670 https://hal.archives-ouvertes.fr/hal-01686670 Submitted on 17 Jan 2018 HAL is a multi-disciplinary open access L’archive ouverte pluridisciplinaire HAL, est archive for the deposit and dissemination of sci- destinée au dépôt et à la diffusion de documents entific research documents, whether they are pub- scientifiques de niveau recherche, publiés ou non, lished or not. The documents may come from émanant des établissements d’enseignement et de teaching and research institutions in France or recherche français ou étrangers, des laboratoires abroad, or from public or private research centers. publics ou privés. LE MOUVEMENT LAROUCHE À L’INTERNATIONAL Impact du territoire et stratégies politiques d’implantation à l’échelle nationale et locale. Approche comparée France États-Unis Par Julien GIRY Docteur en Science Politique Institut du Droit Public et de la Science Politique (IDPSD) Université de Rennes 1 SOMMAIRE I. – UN MOUVEMENT IDÉOLOGIQUEMENT EXTRÉMISTE AU FONCTIONNEMENT SECTAIRE A. – Un mouvement idéologique extrémiste B. – Un mouvement sectaire II. – LES STRATÉGIES POLITIQUES DU MOUVEMENT A. – Sur la scène nationale B. – Sur la scène locale on ami Lyndon LAROUCHE est l’homme politique américain le plus controversé et le plus diffamé de notre temps et, sans doute, de tous les temps : ceux qui ne l’ont ni lu, ni entendu, ni connu ne sont pas les « Mmoins acharnés. -

Executive Intelligence Review, Volume 27, Number 23, June 9, 2000

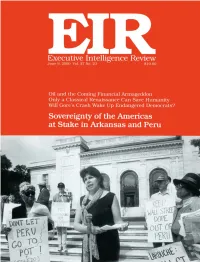

EIR Founder and Contributing Editor: Lyndon H. LaRouche, Jr. Editorial Board: Lyndon H. LaRouche, Jr., Muriel Mirak-Weissbach, Antony Papert, Gerald From the Associate Editor Rose, Dennis Small, Edward Spannaus, Nancy Spannaus, Jeffrey Steinberg, William Wertz Associate Editors: Ronald Kokinda, Susan Welsh Managing Editor: John Sigerson n page 57, you will find a chart reproduced from Al Gore’s cam- Science Editor: Marjorie Mazel Hecht O Special Projects: Mark Burdman paign website, which claims—in flagrant violation of Arkansas law Book Editor: Katherine Notley and the votes of 53,000 Arkansas Democratic voters—that Gore won Photo Editor: Stuart Lewis Circulation Manager: Stanley Ezrol all 45 delegates from the state to the Democratic National Conven- INTELLIGENCE DIRECTORS: tion. The fact that Lyndon LaRouche took 22% of the vote, entitling Asia and Africa: Linda de Hoyos him to between 6 and 10 delegates, is simply obliterated from history. Counterintelligence: Jeffrey Steinberg, Paul Goldstein Imagine for a moment that instead of Gore and LaRouche, the Economics: Marcia Merry Baker, contestants were Peru’s Alberto Fujimori and Alejandro Toledo. William Engdahl History: Anton Chaitkin Imagine that President Fujimori’s website had published a chart Ibero-America: Robyn Quijano, Dennis Small which eliminated 53,000 votes for Toledo. What would Madeleine Law: Edward Spannaus Russia and Eastern Europe: Albright’s State Department do? Impose economic sanctions? Break Rachel Douglas, Konstantin George off diplomatic relations? Bomb the Presidential -

Hissez Les Voiles ! 2 Ville-Enghienlesbains.Fr Sommaire

.MAGAZINE MUNICIPAL. Reflet DES ENGHIENNOIS. MAI - JUIN 2017 / VILLE-ENGHIENLESBAINS.FR 92 12 ENTRETIENS EUROPÉENS 16 AGENDA 21 24 CULTURE ET NUMÉRIQUE L'Europe dans la tourmente La culture de la durabilité L'expertise enghiennoise Sport et handicap HISSEZ LES VOILES ! 2 VILLE-ENGHIENLESBAINS.FR SOMMAIRE 12 17 24 Sommaire N° 92 • MAI - JUIN 2017 8 10 12 15 IMAGES DE VILLE ÉCONOMIE CADRE DE VILLE ENVIRONNEMENT Retour sur le festival L’excellence artisanale • Entretiens européens Une prairie urbaine • Eau’Zen et la semaine FISAC, une aide au d’Enghien • Résultats de Enghien éco-citoyenne • cubaine commerce local la présidentielle • La culture de la durabilité La solidarité en action 17 22 24 26 DOSSIER JEUNESSE VILLE CRÉATIVE ASSOCIATIONS Sport et handicap : Hissez La tribune CMJ • L’expertise enghiennoise Dans les bras des les voiles ! • 3 questions à La citoyenneté au cœur reconnue dans le monde pompiers • Festicart’ Jean-Pierre Haimart de la jeunesse entier Don du sang gastronome 28 30 36 36 SPORT SORTIR VISAGE D'ENGHIEN TRIBUNES Ronde d’Enghien, une Découvrez les 116 villes les Martin Wible - Sapeur course qui a de l’allure ! plus créatives au monde • pompier, passion d'enfance Barrière Enghien Jazz Festival • Fraîch’attitude Magazine de la Ville d’Enghien-les-Bains • Hôtel de ville • 57 rue du Général-de-Gaulle • 95880 Enghien-les-Bains • tél. : 01 34 28 45 46 • Directeur de la publication : Philippe Sueur • Directrice de la communication : Katia Guerin - [email protected] • Rédaction : Katia Guerin • Marie-Charlotte Mallard - [email protected] -

Political Reviews

Political Reviews 0LFURQHVLDLQ5HYLHZ,VVXHVDQG(YHQWV-XO\ WR-XQH david w kupferman, kelly g marsh, donald r shuster, tyrone j taitano 3RO\QHVLDLQ5HYLHZ,VVXHVDQG(YHQWV-XO\ WR-XQH lorenz gonschor, hapakuke pierre leleivai, margaret mutu, forrest wade young 7KH&RQWHPSRUDU\3DFL²F9ROXPH1XPEHU¥ E\8QLYHUVLW\RI+DZDL©L3UHVV 127 political reviews polynesia 183 lt, La Tercera Online. Daily Internet news. 7ëSXUD5H©R Monthly Rapa Nui–language Santiago, Chile. http://latercera.com/ newspaper. Hanga Roa, Rapa Nui. Métis National Council. 2011. Métis UN, United Nations. 2007. United Nations Nation President Visits Easter Island to Declaration of the Rights of Indigenous Support Indigenous Rights Struggle. 8 Peoples. March. http://www.un.org/esa/ August. http://www.metisnation.ca/index socdev/unpfii/documents/DRIPS_en.pdf .php/news/metis-nation-president-visits [accessed 1 October 2012] -easter-island-to-support-indigenous US Congress. 2011. Calling for a Peaceful -rights-struggle [accessed 1 October 2012] Solution to the Easter Island Crisis. Con- Moore, Sally Faulk. 2000. Law as Process: gressional Record 157 (19). 8 February. An Anthropological Approach. Oxford: http://www.gpo.gov/fdsys/pkg/CREC James Currey Publishers. -2011-02-08/html/CREC-2011-02-08 -pt1-PgH544-2.htm MV, Moe Varua Rapa Nui. Monthly magazine. Municipality of Hanga Roa, Wolfe, Patrick. 2006. Settler Colonialism Rapa Nui. and the Elimination of the Native. Journal of Genocide Research 8 (4): 387–409. Nelson, Aaron. 2012. A Quest For Inde- pendence: Who Will Rule Easter Island’s Young, Forrest Wade. 2012. Polynesia in Stone Heads? Time Magazine, World edi- Review: Issues and Events, 1 July 2010 to tion, March. -

Of European and National Election Results Update: September 2018

REVIEW OF EUROPEAN AND NATIONAL ELECTION RESULTS UPDATE: SEPTEMBER 2018 A Public Opinion Monitoring Publication REVIEW OF EUROPEAN AND NATIONAL ELECTION RESULTS UPDATE: SEPTEMBER 2018 Directorate-General for Communication Public Opinion Monitoring Unit September 2018 - PE 625.195 TABLE OF CONTENTS EDITORIAL 1 1. COMPOSITION OF THE EUROPEAN PARLIAMENT 5 DISTRIBUTION OF SEATS EE2019 6 OVERVIEW 1979 - 2014 7 COMPOSITION OF THE EUROPEAN PARLIAMENT LAST UPDATE (10/09/2018) 8 CONSTITUTIVE SESSION (01/07/2014) 9 PROPORTION OF WOMEN AND MEN PROPORTION - LAST UPDATE 10 PROPORTIONS IN POLITICAL GROUPS - LAST UPDATE 11 PROPORTION OF WOMEN IN POLITICAL GROUPS - SINCE 1979 12 2. NUMBER OF NATIONAL PARTIES IN THE EUROPEAN PARLIAMENT 13 3. TURNOUT: EE2014 15 TURNOUT IN THE LAST EUROPEAN AND NATIONAL ELECTIONS 16 TURNOUT IN THE EE2014 18 TURNOUT COMPARISON: 2009 (2013) - 2014 19 TURNOUT IN THE EE2014 - BREAKDOWN BY GENDER 20 TURNOUT IN THE EE2014 - BREAKDOWN BY AGE 21 TURNOUT OVERVIEW SINCE 1979 22 TURNOUT OVERVIEW SINCE 1979 - BY MEMBER STATE 23 4. NATIONAL RESULTS BY MEMBER STATE 27-301 GOVERNMENTS AND OPPOSITION IN MEMBER STATES 28 COMPOSITION OF THE EP: 2014 AND LATEST UPDATE POLITICAL PARTIES IN THE EP MEMBERS OF THE EUROPEAN PARLIAMENT - BY MEMBER STATE EE2014 TOTAL RESULTS EE2014 ELECTORAL LISTS - BY MEMBER STATE RESULTS OF TWO LAST NATIONAL ELECTIONS AND THE EE 2014 DIRECT PRESIDENTIAL ELECTIONS SOURCES EDITORIAL First published in November 2014, the Review of European and National Elections offers a comprehensive, detailed and up-to-date overview on the composition of the European Parliament, national elections in all EU Member States as well as a historical overview on the now nearly forty years of direct elections to the European Parliament since 1979. -

The Case of Jacques Cheminade: Violation of Human Rights in France

Click here for Full Issue of EIR Volume 24, Number 39, September 26, 1997 The case of Jacques Cheminade: violation of human rights in France by Our Paris Bureau The case of Jacques Cheminade, president of the Solidarity wealthy lady, had both the time and the desire to foster the and Progress Party in France and longtime ally of Lyndon well-being of her country by supporting such causes. Between LaRouche, is the best example of the brutality the French 1982 and early 1986, she contributed a total of 1,197,000 nomenklatura is prepared to use against its political oppo- francs (around $200,000), to associations such as the Anti- nents. Drug Coalition, the Fusion Energy Foundation, and the Schil- During the 1995 Presidential elections, a relatively un- ler Institute. Of that sum, half were loans and the rest, contri- known political candidate, Jacques Cheminade, appeared on butions. the French political scene. No sooner had he announced his In October 1986, Mrs. Pa´zery died, and in March 1987, candidacy, than a virulent, nationwide slander campaign was her family initiated legal action against Cheminade et al., launched against him, aimed at portraying him as an extreme accusing them of having defrauded their mother, in spite of right-winger and a thief. This smear campaign was intended the fact that the associations had already paid back 170,000 to prevent people from becoming interested in Cheminade’s francs on outstanding loans and had never denied their inten- message, at a time when corruption scandals have consider- tion to pay back all the loans. -

Is the French Presidential Election a Referendum On

.17 # 3 APRIL 2017 Is the French presidential election a referendum on EU membership ? Olivier Costa relationship with the EU leads to little clearly argued Executive Summary discussions or precise proposals, but it created a fundamental dividing line amongst the candidates, in > European issues are traditionally poorly a globally Eurosceptic context. addressed in French political debates. They The reasons behind the candidates’ lack of interest in are all the less present in 2017, due to the the EU campaign’s main focus on current legal cases and the ongoing political reconfigurations. The European issue is generally less prominent in the founding countries of the European Community than in > However, Europe is one of the fundamental the more recent member states: EU membership dividing lines of the campaign. The majority appears obvious to them, and public action seems to be of the 11 candidates have developed a highly irremediably Europeanized. In France, however, Eurosceptic discourse. Only Emmanuel European issues are not particularly present, and Macron (EM), François Fillon (LR) and Benoît especially not during campaigns for the presidential Hamon (PS) have adopted a moderate elections. The presidential function is directly linked to position on the matter. the idea of French sovereignty: the President is considered as the leader of a major actor in > This rejection of EU integration is above all a international relations, sitting on the UN Security reflection of the rise of populism. The Council and owning nuclear weapons. It is therefore arguments behind this rejection appear difficult for the candidates to admit that the country is weak. closely intertwined to a supranational structure whose > Abroad, the French election is worrying influence is felt in most areas of public action, and that observers because of its uncertain character, France may be required to respect EU institutions’ judged to be a form of referendum on decisions, even when French representatives were France's EU membership.