Evidence from Hamburg's Import Trade, Eightee

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Consumer Behaviour and International Trade in the Western Mediterranean: South-Eastern Spain in a Trans-National Perspective (1730/1808)

Department of History and Civilization Consumer Behaviour and International Trade in the Western Mediterranean: South-Eastern Spain in a Trans-National Perspective (1730/1808) MANUEL PEREZ GARCIA Thesis submitted for assessment with a view to obtaining the degree of Doctor of History and Civilization of the European University Institute Florence, June 2011 Perez Garcia, Manuel (2011), Consumer Behaviour and International Trade in the Western Mediterranean: South-Eastern Spain in a trans-national perspective (1730-1808) European University Institute DOI: 10.2870/31934 EUROPEAN UNIVERSITY INSTITUTE Department of History and Civilization Consumer Behaviour and International Trade in the Western Mediterranean: South-Eastern Spain in a Trans-National Perspective (1730/1808) MANUEL PEREZ GARCIA Examining Board: Bartolomé Yun-Casalilla, supervisor (European University Institute) Luca Molà (European University Institute) Jan De Vries (University of California at Berkeley) Gerard Chastagnaret (Université de Provence) © 2011, Manuel Pérez García No part of this thesis may be copied, reproduced or transmitted without prior permission of the author Perez Garcia, Manuel (2011), Consumer Behaviour and International Trade in the Western Mediterranean: South-Eastern Spain in a trans-national perspective (1730-1808) European University Institute DOI: 10.2870/31934 Perez Garcia, Manuel (2011), Consumer Behaviour and International Trade in the Western Mediterranean: South-Eastern Spain in a trans-national perspective (1730-1808) European University Institute DOI: 10.2870/31934 Abstract How to focus the analysis of the birth of mass consumption society has been a scholarly obsession over the last few decades. This thesis suggests that an analytical approach must be taken in studies on consumption paying special attention to the socio-cultural and economic transfers which occur when different commodities are introduced to territories with diverse socio-cultural values and identities. -

THE TOWN HALL Station on the Route Charlemagne Table of Contents

THE TOWN HALL Station on the Route Charlemagne Table of contents Route Charlemagne 3 Palace of Charlemagne 4 History of the Building 6 Gothic Town Hall 6 Baroque period 7 Neo-Gothic restoration 8 Destruction and rebuilding 9 Tour 10 Foyer 10 Council Hall 11 White Hall 12 Master Craftsmen‘s Court 13 Master Craftsmen‘s Kitchen 14 “Peace Hall“ (Red Hall) 15 Ark Staircase 16 Charlemagne Prize 17 Coronation Hall 18 Service 22 Information 23 Imprint 23 7 6 5 1 2 3 4 Plan of the ground floor 2 The Town Hall Route Charlemagne Aachen‘s Route Charlemagne connects significant locations around the city to create a path through history – one that leads from the past into the future. At the centre of the Route Charlemagne is the former palace complex of Charlemagne, with the Katschhof, the Town Hall and the Cathedral still bearing witness today of a site that formed the focal point of the first empire of truly European proportions. Aachen is a historical town, a centre of science and learning, and a European city whose story can be seen as a history of Europe. This story, along with other major themes like religion, power, economy and media, are all reflected and explored in places like the Cathedral and the Town Hall, the International Newspaper Museum, the Grashaus, Haus Löwenstein, the Couven-Museum, the Axis of Science, the SuperC of the RWTH Aachen University and the Elisenbrunnen. The central starting point of the Route Charlemagne is the Centre Charlemagne, the new city museum located on the Katschhof between the Town Hall and the Cathedral. -

History and Culture

HISTORY AND CULTURE A HAMBURG PORTUGUESE IN THE SERVICE OF THE HAGANAH: THE TRIAL AGAINST DAVID SEALTIEL IN HAMBURG (1937) Ina Lorenz (Hamburg. Germany) Spotlighted in the story here to be told is David de Benjamin Sealtiel (Shaltiel, 1903–1969), a Sephardi Jew from Hamburg, who from 1934 worked for the Haganah in Palestine as a weapons buyer. He paid for that activity with 862 days in incarceration under extremely difficult conditions of detention in the concentration camps of the SS.1 Jewish Immigration into Palestine and the Founding of the Haganah2 In order to be able to effectively protect the new Jewish settlements in Palestine from Arab attacks, and since possession of weapons was prohibited under the British Mandatory administration, arms and munitions initially were generally being smuggled into Palestine via French- controlled Syria. The leaders of the Haganah and Histadrut transformed the Haganah with the help of the Jewish Agency from a more or less untrained militia into a paramilitary group. The organization, led by Yisrael Galili (1911–1986), which in the rapidly growing Jewish towns had approximately 10,000 members, continued to be subordinate to the civilian leadership of the Histadrut. The Histadrut also was responsible for the ———— 1 Michael Studemund-Halévy has dealt with the fascinating, complex personality of David Sealtiel/Shaltiel in a number of publications in German, Hebrew, French and English: “From Hamburg to Paris”; “Vom Shaliach in den Yishuv”; “Sioniste au par- fum romanesque”; “David Shaltiel.” See also [Shaltiel, David]. “In meines Vaters Haus”; Scholem. “Erinnerungen an David Shaltiel (1903–1968).” The short bio- graphical sketches on David Sealtiel are often based on inadequate, incorrect, wrong or fictitious informations: Avidar-Tschernovitz. -

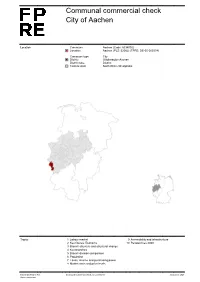

Communal Commercial Check City of Aachen

Eigentum von Fahrländer Partner AG, Zürich Communal commercial check City of Aachen Location Commune Aachen (Code: 5334002) Location Aachen (PLZ: 52062) (FPRE: DE-05-000334) Commune type City District Städteregion Aachen District type District Federal state North Rhine-Westphalia Topics 1 Labour market 9 Accessibility and infrastructure 2 Key figures: Economy 10 Perspectives 2030 3 Branch structure and structural change 4 Key branches 5 Branch division comparison 6 Population 7 Taxes, income and purchasing power 8 Market rents and price levels Fahrländer Partner AG Communal commercial check: City of Aachen 3rd quarter 2021 Raumentwicklung Eigentum von Fahrländer Partner AG, Zürich Summary Macro location text commerce City of Aachen Aachen (PLZ: 52062) lies in the City of Aachen in the District Städteregion Aachen in the federal state of North Rhine-Westphalia. Aachen has a population of 248'960 inhabitants (31.12.2019), living in 142'724 households. Thus, the average number of persons per household is 1.74. The yearly average net migration between 2014 and 2019 for Städteregion Aachen is 1'364 persons. In comparison to national numbers, average migration tendencies can be observed in Aachen within this time span. According to Fahrländer Partner (FPRE), in 2018 approximately 34.3% of the resident households on municipality level belong to the upper social class (Germany: 31.5%), 33.6% of the households belong to the middle class (Germany: 35.3%) and 32.0% to the lower social class (Germany: 33.2%). The yearly purchasing power per inhabitant in 2020 and on the communal level amounts to 22'591 EUR, at the federal state level North Rhine-Westphalia to 23'445 EUR and on national level to 23'766 EUR. -

Demshuk CV2020-Extended

ANDREW THOMAS DEMSHUK, Ph.D. Associate Professor of History Battelle-Tompkins Hall, 119 American University 4400 Massachusetts Ave NW [email protected] Washington, DC 20016 Peer-Reviewed Monographs: Three Cities after Hitler: Redemptive Reconstruction across Cold War Borders (Pittsburgh: University of Pittsburgh Press, forthcoming 2022). Bowling for Communism: Urban Ingenuity at the End of East Germany (Ithaca, NY: Cornell University Press, forthcoming October 2020). Demolition on Karl Marx Square: Cultural Barbarism and the People’s State in 1968 (Oxford and New York: Oxford University Press, 2017). The Lost German East: Forced Migration and the Politics of Memory, 1945-1970 (Cambridge and New York: Cambridge University Press, 2012). Paperback Edition, 2014. Co-Editor and Contributor: “The Voice of the Lost German East: Heimat Bells as Soundscapes of Memory,” in Cultural Landscapes: Transatlantische Perspektiven auf Wirkungen und Auswirkungen deutscher Kultur und Geschichte im östlichen Europa, ed. Andrew Demshuk and Tobias Weger (Munich: Oldenbourg Wissenschaftsverlag, 2015). Current Book-Length Projects: “Alien Homeland: Human Encounters after Forced Migration on a German-Polish Borderland, 1970-1990” Peer-Reviewed Articles: “The People’s Bowling Palace: Building Underground in Late Communist Leipzig,” Contemporary European History 29, no. 3 (August 2020): 339-355. “A Polish Approach for German Cities? Cement Old Towns and the Search for Rootedness in Postwar Leipzig and Frankfurt/Main,” European History Quarterly 50, no. 1 (Jan. 2020): 88-127. “Rebuilding after the Reich: Sacred Sites in Frankfurt, Leipzig, and Wrocław, 1945-1949,” in War and the City: The Urban Context of Conflict and Mass Destruction, ed. Tim Keogh (Paderborn: Ferdinand Schöningh, 2019): 167-193. -

CS 4700: Foundations of Artificial Intelligence

CS 4700: Foundations of Artificial Intelligence Bart Selman [email protected] Module: Informed Search Readings R&N - Chapter 3: 3.5 and 3.6 Search Search strategies determined by choice of node (in queue) to expand Uninformed search: – Distance to goal not taken into account Informed search : – Information about cost to goal taken into account Aside: “Cleverness” about what option to explore next, almost seems a hallmark of intelligence. E.g., a sense of what might be a good move in chess or what step to try next in a mathematical proof. We don’t do blind search… Basic idea: State evaluation Start state function can effectively guide search. Also in multi-agent settings. (Chess: board eval.) Reinforcement learning: Learn the state eval function. Goal A breadth-first search tree. Perfect “heuristics,” eliminates search. Approximate heuristics, significantly reduces search. Best (provably) use of search heuristic info: Best-first / A* search. Outline • Best-first search • Greedy best-first search • A* search • Heuristics How to take information into account? Best-first search. Idea : use an evaluation function for each node – Estimate of “desirability” of node – Expand most desirable unexpanded node first (“best-first search”) – Heuristic Functions : • f: States à Numbers • f(n): expresses the quality of the state n – Allows us to express problem-specific knowledge, – Can be imported in a generic way in the algorithms. – Use uniform-cost search. See Figure 3.14 but use f(n) instead of path cost g(n). – Queuing based on f(n): Order the nodes in fringe in decreasing order of desirability Special cases: • greedy best-first search • A* search Romanian path finding problem Base eg on GPS info. -

NORTH RHINE WESTPHALIA 10 REASONS YOU SHOULD VISIT in 2019 the Mini Guide

NORTH RHINE WESTPHALIA 10 REASONS YOU SHOULD VISIT IN 2019 The mini guide In association with Commercial Editor Olivia Lee Editor-in-Chief Lyn Hughes Art Director Graham Berridge Writer Marcel Krueger Managing Editor Tom Hawker Managing Director Tilly McAuliffe Publishing Director John Innes ([email protected]) Publisher Catriona Bolger ([email protected]) Commercial Manager Adam Lloyds ([email protected]) Copyright Wanderlust Publications Ltd 2019 Cover KölnKongress GmbH 2 www.nrw-tourism.com/highlights2019 NORTH RHINE-WESTPHALIA Welcome On hearing the name North Rhine- Westphalia, your first thought might be North Rhine Where and What? This colourful region of western Germany, bordering the Netherlands and Belgium, is perhaps better known by its iconic cities; Cologne, Düsseldorf, Bonn. But North Rhine-Westphalia has far more to offer than a smattering of famous names, including over 900 museums, thousands of kilometres of cycleways and a calendar of exciting events lined up for the coming year. ONLINE Over the next few pages INFO we offer just a handful of the Head to many reasons you should visit nrw-tourism.com in 2019. And with direct flights for more information across the UK taking less than 90 minutes, it’s the perfect destination to slip away to on a Friday and still be back in time for your Monday commute. Published by Olivia Lee Editor www.nrw-tourism.com/highlights2019 3 NORTH RHINE-WESTPHALIA DID YOU KNOW? Despite being landlocked, North Rhine-Westphalia has over 1,500km of rivers, 360km of canals and more than 200 lakes. ‘Father Rhine’ weaves 226km through the state, from Bad Honnef in the south to Kleve in the north. -

Lernen Von Vauban. Ein Studienprojekt Und Mehr…

PT_Materialien 32 Lernen von Vauban. Ein Studienprojekt und mehr… vorgelegt von Ulrike Sommer und Carolin Wiechert Frontbild: Selle, Klaus (2013); Aufnahmen während der Exkursionen nach Vauban; innerhalb des Projektes M2.1, Von Vauban Lernen. Aachen Lernen von Vauban. Ein Studienprojekt und mehr… Durchgeführt von Studierenden an der Fakultät für Architektur der RWTH Aachen University im Rahmen eines studentischen Projektes. Die Ergebnisse wurden zusammengestellt von Dipl.-Ing., M.Sc- Ulrike Sommer und M.Sc. Carolin Wiechert RWTH Aachen University Lehrstuhl für Planungstheorie und Stadtentwicklung Layout: Carolin Wiechert Aachen, im Februar 2014 Inhalt Vorwort 8 Lernen von Vauban. Ein Studienprojekt und mehr… 8 1. Zur Einführung 13 Das Quartier Vauban 13 Akteure 14 Städtebauliche Struktur 17 Verkehrskonzept 18 2. Methodisches Vorgehen 22 3. Die sechs Zieldimensionen und weitere Erkenntnisse 25 3.1 Städtebauliche Struktur 25 Stadt der kurzen Wege 25 Parzellierung und Baustrukturen 31 Urbane Dichte 33 Verknüpfung mit dem Naherholungsgebiet und der Nachbargemeinde 35 Bestandserhalt 36 Fazit Städtebauliche Struktur 37 3.2 Wohnen 38 Wohnraumversorgung und Art der Bebauung 38 Bauen in selbstorganisierten Gruppen 44 Fazit Wohnen 46 3.3 Bevölkerung, Soziales 46 Preiswerter, öffentlich geförderter Wohnungsbau 46 Soziale Durchmischung 49 Infrastruktur für Familien 51 Nachbarschaften 52 Fazit Bevölkerung, Soziales 54 Lernen von Vauban. Ein Studienprojekt und mehr... 3.4 Mobilität 54 Verkehrsberuhigung 54 ÖPNV- Anbindung 65 Fußgänger und Radverkehr 68 Wohnen ohne Auto 72 Fazit Mobilität 78 3.5 Umwelt 79 Energie 79 Entwässerung 85 Lärm 88 Vegetation 91 Fazit Umwelt 94 3.6 Prozess 95 Erweiterte Bürgerbeteiligung und lernende Planung 95 Fazit Prozess 101 3.7 Weitere Erkenntnisse 102 Älter werden in Vauban 102 Konflikte unter den Bewohnern in Vauban 103 Infrastruktur für Besucher 104 4. -

Wars Between the Danes and Germans, for the Possession Of

DD 491 •S68 K7 Copy 1 WARS BETWKEX THE DANES AND GERMANS. »OR TllR POSSESSION OF SCHLESWIG. BV t>K()F. ADOLPHUS L. KOEPPEN FROM THE "AMERICAN REVIEW" FOR NOVEMBER, U48. — ; WAKS BETWEEN THE DANES AND GERMANS, ^^^^ ' Ay o FOR THE POSSESSION OF SCHLESWIG. > XV / PART FIRST. li>t^^/ On feint d'ignorer que le Slesvig est une ancienne partie integTante de la Monarchie Danoise dont I'union indissoluble avec la couronne de Danemarc est consacree par les garanties solennelles des grandes Puissances de I'Eui'ope, et ou la langue et la nationalite Danoises existent depuis les temps les et entier, J)lus recules. On voudrait se cacher a soi-meme au monde qu'une grande partie de la popu- ation du Slesvig reste attacliee, avec une fidelite incbranlable, aux liens fondamentaux unissant le pays avec le Danemarc, et que cette population a constamment proteste de la maniere la plus ener- gique centre une incorporation dans la confederation Germanique, incorporation qu'on pretend medier moyennant une armee de ciuquante mille hommes ! Semi-official article. The political question with regard to the ic nation blind to the evidences of history, relations of the duchies of Schleswig and faith, and justice. Holstein to the kingdom of Denmark,which The Dano-Germanic contest is still at the present time has excited so great a going on : Denmark cannot yield ; she has movement in the North, and called the already lost so much that she cannot submit Scandinavian nations to arms in self-defence to any more losses for the future. The issue against Germanic aggression, is not one of a of this contest is of vital importance to her recent date. -

The Relationship of Religion and Consumerism in Eighteenth Century Colonial America

ABSTRACT Evangelical Jeremiads and Consuming Eves: The Relationship of Religion and Consumerism in Eighteenth Century Colonial America Amanda S. Mylin, M.A. Mentor: Thomas S. Kidd, Ph.D. This thesis examines the commercial world of the American British colonies from the Great Awakening to the American Revolution through the lens of eighteenth century American religious history. It examines evangelical and Quaker responses to the consumer market through published sermons and other religious rhetoric. Colonial ministers discussed the dangers of consumerism through the format of jeremiads, seeing God’s punishment for indulgence in luxury through the turmoil of the eighteenth century. However, revival ministers also used commercial methods to spread the gospel. Additionally, women in particular were a focal point of religious discussion about consumerism. While many historians have focused on the consumer revolution, and many have focused on early American religion, little has been done to unite these threads. This thesis hopes to do that by showing that religious discussion was essential to the American tradition of participating in the marketplace. Evangelical Jeremiads and Consuming Eves: The Relationship of Religion and Consumerism in Eighteenth-Century Colonial America by Amanda S. Mylin, B.A. A Thesis Approved by the Department of History Kimberly R. Kellison, Ph.D., Chairperson Submitted to the Graduate Faculty of Baylor University in Partial Fulfillment of the Requirements for the Degree of Master of Arts Approved by the Thesis Committee Thomas S. Kidd, Ph.D., Chairperson Andrea L. Turpin, Ph.D. Julie Holcomb, Ph.D. Accepted by the Graduate School August 2015 J. Larry Lyon, Ph.D., Dean Page bearing signatures is kept on file in the Graduate School. -

1 Co? Was? German-Polish Linguistic Attitudes in Frankfurt (Oder)

Co? Was ? German-Polish Linguistic Attitudes in Frankfurt (Oder) Megan Clark Senior Linguistics Thesis Bryn Mawr College 2010 In this study I analyze the linguistic attitudes held by Polish and German speakers in the border towns of Frankfurt an der Oder, Germany and Słubice, Poland, held together by a cross-border university. I consider the historical background in the relationship between the two communities, including but not limited to the effect of Germany and Poland’s separate entrances into the European Union and Schengen zone, which have divided the two countries until recently, as well as the adoption of the Euro in both Germany and, later, Poland. With consideration of this history, I explore the concept of linguistic attitudes in other border communities to mark parallels and differences in the attitudes of speakers on each side of the border, most notably different because of the presence of the university on both sides of the dividing river. I supplement this research with a study conducted on speakers themselves within each side of the community to explore the underlying thoughts and ideas behind attitudes toward speakers of the other language, investigating why so many Polish speakers are fluent in German, while only a few German students endeavor to learn Polish. The research we have conducted here explores a very important aspect of language attitudes as a proxy for European geo-political relations as exemplified in the role of Poland as an outlier in the European Union due to its late joining and reluctant acceptance of the Euro. Though student relations on the border are strong, the heart of Słubice remains untouched by German residents, despite full osmosis of Polish citizens into the heart of Frankfurt. -

Marten Stol WOMEN in the ANCIENT NEAR EAST

Marten Stol WOMEN IN THE ANCIENT NEAR EAST Marten Stol Women in the Ancient Near East Marten Stol Women in the Ancient Near East Translated by Helen and Mervyn Richardson ISBN 978-1-61451-323-0 e-ISBN (PDF) 978-1-61451-263-9 e-ISBN (EPUB) 978-1-5015-0021-3 This work is licensed under the Creative Commons Attribution-NonCommercial- NoDerivs 3.0 License. For details go to http://creativecommons.org/licenses/ by-nc-nd/3.0/ Library of Congress Cataloging-in-Publication Data A CIP catalog record for this book has been applied for at the Library of Congress. Bibliographic information published by the Deutsche Nationalbibliothek The Deutsche Nationalbibliothek lists this publication in the Deutsche Nationalbibliografie; detailed bibliographic data are available on the Internet at http://dnb.dnb.de. Original edition: Vrouwen van Babylon. Prinsessen, priesteressen, prostituees in de bakermat van de cultuur. Uitgeverij Kok, Utrecht (2012). Translated by Helen and Mervyn Richardson © 2016 Walter de Gruyter Inc., Boston/Berlin Cover Image: Marten Stol Typesetting: Dörlemann Satz GmbH & Co. KG, Lemförde Printing and binding: cpi books GmbH, Leck ♾ Printed on acid-free paper Printed in Germany www.degruyter.com Table of Contents Introduction 1 Map 5 1 Her outward appearance 7 1.1 Phases of life 7 1.2 The girl 10 1.3 The virgin 13 1.4 Women’s clothing 17 1.5 Cosmetics and beauty 47 1.6 The language of women 56 1.7 Women’s names 58 2 Marriage 60 2.1 Preparations 62 2.2 Age for marrying 66 2.3 Regulations 67 2.4 The betrothal 72 2.5 The wedding 93 2.6