Food Security Outlook, October 2020 to May 2021

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Humanitarian Situation Report No. 19 Q3 2020 Highlights

Sudan Humanitarian Situation Report No. 19 Q3 2020 UNICEF and partners assess damage to communities in southern Khartoum. Sudan was significantly affected by heavy flooding this summer, destroying many homes and displacing families. @RESPECTMEDIA PlPl Reporting Period: July-September 2020 Highlights Situation in Numbers • Flash floods in several states and heavy rains in upriver countries caused the White and Blue Nile rivers to overflow, damaging households and in- 5.39 million frastructure. Almost 850,000 people have been directly affected and children in need of could be multiplied ten-fold as water and mosquito borne diseases devel- humanitarian assistance op as flood waters recede. 9.3 million • All educational institutions have remained closed since March due to people in need COVID-19 and term realignments and are now due to open again on the 22 November. 1 million • Peace talks between the Government of Sudan and the Sudan Revolu- internally displaced children tionary Front concluded following an agreement in Juba signed on 3 Oc- tober. This has consolidated humanitarian access to the majority of the 1.8 million Jebel Mara region at the heart of Darfur. internally displaced people 379,355 South Sudanese child refugees 729,530 South Sudanese refugees (Sudan HNO 2020) UNICEF Appeal 2020 US $147.1 million Funding Status (in US$) Funds Fundi received, ng $60M gap, $70M Carry- forward, $17M *This table shows % progress towards key targets as well as % funding available for each sector. Funding available includes funds received in the current year and carry-over from the previous year. 1 Funding Overview and Partnerships UNICEF’s 2020 Humanitarian Action for Children (HAC) appeal for Sudan requires US$147.11 million to address the new and protracted needs of the afflicted population. -

“Kankasha” in Kassala: a Prospective Observational Cohort Study of the Clinical Characteristics, Epidemiology, Genetic Origi

medRxiv preprint doi: https://doi.org/10.1101/2020.09.23.20199976; this version posted September 24, 2020. The copyright holder for this preprint (which was not certified by peer review) is the author/funder, who has granted medRxiv a license to display the preprint in perpetuity. It is made available under a CC-BY-NC-ND 4.0 International license . 1 1 Title [216/250 characters] 2 “Kankasha” in Kassala: a prospective observational cohort study of the clinical characteristics, 3 epidemiology, genetic origin, and chronic impact of the 2018 epidemic of Chikungunya virus 4 infection in Kassala, Sudan 5 Short title: [66/70characters] 6 Understanding the 2018 Chikungunya virus epidemic in Eastern Sudan 7 8 Authors: Hilary Bower1*, Mubarak el Karsany2,3*, Abd Alhadi Adam Hussein4, Mubarak Ibrahim 9 Idriss5, Ma’aaza Abasher AlZain6, Mohamed Elamin Ahmed Alfakiyousif2, Rehab Mohamed2, Iman 10 Mahmoud2, Omer Albadri,7 Suha Abdulaziz Alnour Mahmoud10, Orwa Ibrahim Abdalla10, Mawahib 11 Eldigail2, Nuha Elagib2, Ulrike Arnold1, Bernardo Gutierrez8, Oliver G. Pybus8, Daniel P. Carter9, Steven 12 T. Pullan9, Shevin T. Jacob11, Tajeldin Mohammedein Abdallah4,10#, Benedict Gannon1# , Tom E. 13 Fletcher11# 14 * Equal first authors, # Equal senior authors 15 16 Authors’ affiliations 17 1. UK Public Health Rapid Support Team, London School of Hygiene & Tropical Medicine/Public Health 18 England, London, United Kingdom 19 2. National Public Health Laboratory, Federal Ministry of Health, Khartoum, Sudan 20 3. Karary University, Omdurman, Sudan 21 4. University of Kassala, Kassala, Sudan 22 5. Laboratory Division, Kassala State Ministry of Health, Kassala, Sudan 23 6. Communicable Disease Surveillance & Events Unit, Federal Ministry of Health, Khartoum, Sudan 24 7. -

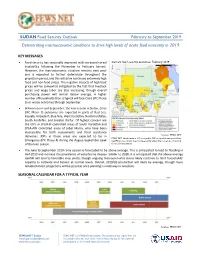

Sudan Food Security Outlook Report

SUDAN Food Security Outlook February to September 2019 Deteriorating macroeconomic conditions to drive high levels of acute food insecurity in 2019 KEY MESSAGES • Food security has seasonally improved with increased cereal Current food security outcomes, February 2019 availability following the November to February harvest. However, the macroeconomic situation remains very poor and is expected to further deteriorate throughout the projection period, and this will drive continued extremely high food and non-food prices. The negative impacts of high food prices will be somewhat mitigated by the fact that livestock prices and wage labor are also increasing, though overall purchasing power will remain below average. A higher number of households than is typical will face Crisis (IPC Phase 3) or worse outcomes through September. • Between June and September, the lean season in Sudan, Crisis (IPC Phase 3) outcomes are expected in parts of Red Sea, Kassala, Al Gadarif, Blue Nile, West Kordofan, North Kordofan, South Kordofan, and Greater Darfur. Of highest concern are the IDPs in SPLM-N controlled areas of South Kordofan and SPLA-AW controlled areas of Jebel Marra, who have been inaccessible for both assessments and food assistance deliveries. IDPs in these areas are expected to be in Source: FEWS NET FEWS NET classification is IPC-compatible. IPC-compatible analysis follows Emergency (IPC Phase 4) during the August-September peak key IPC protocols but does not necessarily reflect the consensus of national of the lean season. food security partners. • The June to September 2019 rainy season is forecasted to be above average. This is anticipated to lead to flooding in mid-2019 and increase the prevalence of waterborne disease. -

Sudan's Spreading Conflict (II): War in Blue Nile

Sudan’s Spreading Conflict (II): War in Blue Nile Africa Report N°204 | 18 June 2013 International Crisis Group Headquarters Avenue Louise 149 1050 Brussels, Belgium Tel: +32 2 502 90 38 Fax: +32 2 502 50 38 [email protected] Table of Contents Executive Summary ................................................................................................................... i Recommendations..................................................................................................................... iii I. Introduction ..................................................................................................................... 1 II. A Sudan in Miniature ....................................................................................................... 3 A. Old-Timers Versus Newcomers ................................................................................. 3 B. A History of Land Grabbing and Exploitation .......................................................... 5 C. Twenty Years of War in Blue Nile (1985-2005) ........................................................ 7 III. Failure of the Comprehensive Peace Agreement ............................................................. 9 A. The Only State with an Opposition Governor (2007-2011) ...................................... 9 B. The 2010 Disputed Elections ..................................................................................... 9 C. Failed Popular Consultations ................................................................................... -

SUDAN Livelihood Profiles, North Kordofan State August 2013

SUDAN Livelihood Profiles, North Kordofan State August 2013 FEWS NET FEWS NET is a USAID-funded activity. The content of this report does Washington not necessarily reflect the view of the United States Agency for [email protected] International Development or the United States Government. www.fews.net SUDAN Livelihood Profiles, North Kordofan State August 2013 TABLE OF CONTENTS Acknowledgements ................................................................................................................................................ 3 Acronyms and Abbreviations .................................................................................................................................. 4 Summary of Household Economy Approach Methodology ................................................................................... 5 The Household Economy Assessment in Sudan ..................................................................................................... 6 North Kordofan State Livelihood Profiling .............................................................................................................. 7 Overview of Rural Livelihoods in North Kordofan .................................................................................................. 8 Zone 1: Central Rainfed Millet and Sesame Agropastoral Zone (SD14) ............................................................... 10 Zone 2: Western Agropastoral Millet Zone (SD13) .............................................................................................. -

The Economics of Ethnic Cleansing in Darfur

The Economics of Ethnic Cleansing in Darfur John Prendergast, Omer Ismail, and Akshaya Kumar August 2013 WWW.ENOUGHPROJECT.ORG WWW.SATSENTINEL.ORG The Economics of Ethnic Cleansing in Darfur John Prendergast, Omer Ismail, and Akshaya Kumar August 2013 COVER PHOTO Displaced Beni Hussein cattle shepherds take shelter on the outskirts of El Sereif village, North Darfur. Fighting over gold mines in North Darfur’s Jebel Amer area between the Janjaweed Abbala forces and Beni Hussein tribe started early this January and resulted in mass displacement of thousands. AP PHOTO/UNAMID, ALBERT GONZALEZ FARRAN Overview Darfur is burning again, with devastating results for its people. A kaleidoscope of Janjaweed forces are once again torching villages, terrorizing civilians, and systematically clearing prime land and resource-rich areas of their inhabitants. The latest ethnic-cleans- ing campaign has already displaced more than 300,000 Darfuris this year and forced more than 75,000 to seek refuge in neighboring Chad, the largest population displace- ment in recent years.1 An economic agenda is emerging as a major driver for the escalating violence. At the height of the mass atrocities committed from 2003 to 2005, the Sudanese regime’s strategy appeared to be driven primarily by the counterinsurgency objectives and secondarily by the acquisition of salaries and war booty. Undeniably, even at that time, the government could have only secured the loyalty of its proxy Janjaweed militias by allowing them to keep the fertile lands from which they evicted the original inhabitants. Today’s violence is even more visibly fueled by monetary motivations, which include land grabbing; consolidating control of recently discovered gold mines; manipulating reconciliation conferences for increased “blood money”; expanding protection rackets and smuggling networks; demanding ransoms; undertaking bank robberies; and resum- ing the large-scale looting that marked earlier periods of the conflict. -

North Darfur II

Darfur Humanitarian Profile Annexes: I. North Darfur II. South Darfur III. West Darfur Darfur Humanitarian Profile Annex I: North Darfur North Darfur Main Humanitarian Agencies Table 1.1: UN Agencies Table 1.2: International NGOs Table 1.3: National NGOs Intl. Natl. Vehicl Intl. Natl. Vehic Intl. Natl. Vehic Agency Sector staff staff* es** Agency Sector staff staff* les** Agency Sector staff staff les FAO 10 1 2 2 ACF 9 4 12 3 Al-Massar 0 1 0 Operations, Logistics, Camp IOM*** Management x x x GAA 1, 10 1 3 2 KSCS x x x OCHA 14 1 2 3 GOAL 2, 5, 8, 9 6 117 10 SECS x x x 2, 3, 7, UNDP*** 15 x x x ICRC 12, 13 6 20 4 SRC 1, 2 0 10 3 2, 4, 5, 6, UNFPA*** 5, 7 x x x IRC 9, 10, 11 1 5 4 SUDO 5, 7 0 2 0 Protection, Technical expertise for UNHCR*** site planning x x x MSF - B 5 5 10 0 Wadi Hawa 1 1 x 2, 3, 4, 5, 6, 8, Oxfam - UNICEF 9 11, 12 4 5 4 GB 2, 3, 4 5 30 10 Total 1 14 3 1, 3, 4, 5, 6, 8, 9, UNJLC*** 17 x x x SC-UK 11, 12 5 27 8 Technical Spanish UNMAS*** advice x x x Red Cross 3, 4 1 0 1 UNSECOORD 16 1 1 1 DED*** x x x WFP 1, 9, 11 1 12 5 NRC*** x x x WHO 4, 5, 6 2 7 2 Total 34 224 42 Total 10 29 17 x = information unavailable at this time Sectors: 1) Food 2) Shelter/NFIs 3) Clean water 4) Sanitation 5) Primary Health Facilities *Programme and project staff only. -

Soil and Oil

COALITION FOR INTERNATIONAL JUSTICE COALITION FOR I NTERNATIONAL JUSTICE SOIL AND OIL: DIRTY BUSINESS IN SUDAN February 2006 Coalition for International Justice 529 14th Street, N.W. Suite 1187 Washington, D.C., 20045 www.cij.org February 2006 i COALITION FOR INTERNATIONAL JUSTICE COALITION FOR I NTERNATIONAL JUSTICE SOIL AND OIL: DIRTY BUSINESS IN SUDAN February 2006 Coalition for International Justice 529 14th Street, N.W. Suite 1187 Washington, D.C., 20045 www.cij.org February 2006 ii COALITION FOR INTERNATIONAL JUSTICE © 2006 by the Coalition for International Justice. All rights reserved. February 2006 iii COALITION FOR INTERNATIONAL JUSTICE ACKNOWLEDGMENTS CIJ wishes to thank the individuals, Sudanese and not, who graciously contributed assistance and wisdom to the authors of this research. In particular, the authors would like to express special thanks to Evan Raymer and David Baines. February 2006 iv 25E 30E 35E SAUDI ARABIA ARAB REPUBLIC OF EGYPT LIBYA Red Lake To To Nasser Hurghada Aswan Sea Wadi Halfa N u b i a n S aS D e s e r t ha ah raar a D De se es re tr t 20N N O R T H E R N R E D S E A 20N Kerma Port Sudan Dongola Nile Tokar Merowe Haiya El‘Atrun CHAD Atbara KaroraKarora RIVER ar Ed Damer ow i H NILE A d tb a a W Nile ra KHARTOUM KASSALA ERITREA NORTHERN Omdurman Kassala To Dese 15N KHARTOUM DARFUR NORTHERN 15N W W W GEZIRA h h KORDOFAN h i Wad Medani t e N i To le Gedaref Abéche Geneina GEDAREF Al Fasher Sinnar El Obeid Kosti Blu WESTERN Rabak e N i En Nahud le WHITE DARFUR SINNAR WESTERN NILE To Nyala Dese KORDOFAN SOUTHERN Ed Damazin Ed Da‘ein Al Fula KORDOFAN BLUE SOUTHERN Muglad Kadugli DARFUR NILE B a Paloich h 10N r e 10N l 'Arab UPPER NILE Abyei UNIT Y Malakal NORTHERN ETHIOPIA To B.A.G. -

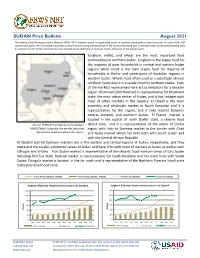

SUDAN Price Bulletin August 2021

SUDAN Price Bulletin August 2021 The Famine Early Warning Systems Network (FEWS NET) monitors trends in staple food prices in countries vulnerable to food insecurity. For each FEWS NET country and region, the Price Bulletin provides a set of charts showing monthly prices in the current marketing year in selected urban centers and allowing users to compare current trends with both five-year average prices, indicative of seasonal trends, and prices in the previous year. Sorghum, millet, and wheat are the most important food commodities in northern Sudan. Sorghum is the staple food for the majority of poor households in central and eastern Sudan regions while millet is the main staple food for majority of households in Darfur and some parts of Kordofan regions in western Sudan. Wheat most often used as a substitute all over northern Sudan but it is a staple food for northern states. Each of the markets represented here act as indicators for a broader region. Khartoum (Om Durman) is representative for Khartoum state, the main urban center of Sudan, and it has linkages with most of other markets in the country. El Obeid is the main assembly and wholesale market in North Kordofan and it is representative for the region, and it links market between central, western, and southern Sudan. El Fasher market is located in the capital of north Darfur state, a chronic food Source: FEWS NET gratefully acknowledges deficit area, and it is representative of the entire of Darfur FAMIS/FMoA, Sudan for the market data and region with links to Geneina market in the border with Chad information used to produce this report. -

Amir Warns Against Oil Dependence, Terrorism

SUBSCRIPTION WEDNESDAY, OCTOBER 29, 2014 MUHARRAM 5, 1436 AH www.kuwaittimes.net Amir on Bahrain Macy’s heads Anelka makes brotherly bans main overseas with nightmarish visit to opposition branch in comeback Saudi Arabia3 group 7 Abu21 Dhabi in19 India Amir warns against oil Max 33º Min 21º dependence, terrorism High Tide 01:50 & 16:10 Low Tide PM calls to ‘tighten belts’ Speaker blasts opposition 09:25 & 21:25 40 PAGES NO: 16326 150 FILS • from the editor’s desk It’s time to get to work By Abd Al-Rahman Al-Alyan [email protected] is Highness the Amir Sheikh Sabah Al- Ahmad Al-Jaber Al-Sabah opened the 14th Hsession of Kuwait’s National Assembly yes- terday, urging lawmakers and the government to control spending and diversify Kuwait’s economy in the face of falling oil prices. “Here again, we are witnessing another cycle of sliding oil prices as a result of economic and politi- cal factors hitting the global economy, which is negatively affecting the national economy,” the KUWAIT: (From left) HH the Amir Sheikh Sabah Al-Ahmad Al-Sabah, HH the Prime Minister Sheikh Jaber Al-Mubarak Al-Sabah and Speaker Marzouq Al-Ghanem attend the opening session of the new parliamentary term yesterday. — Photos by Yasser Al-Zayyat and KUNA Amir said. “I call on you, government and Assembly, to shoulder your national responsibility to issue the required legislation and decisions to By B Izzak safeguard our oil and fiscal wealth which is not for KUWAIT: His Highness the Amir Sheikh Sabah Al- us alone but also for our future generations,” Ahmad Al-Sabah yesterday opened the new parliamen- Sheikh Sabah said. -

Sudan: West Kordofan - Who Does What Where (3Ws) 1 April 2018 Jebrat El Sheikh Sodari

Sudan: West Kordofan - Who Does What Where (3Ws) 1 April 2018 Jebrat El Sheikh Sodari 2(UN/IOs) Organizations per locality / per sector NORTH KORDOFAN (INGOs) El Kuma 2 No. of organizations per sector: < 5 5 - 10 11 - 20 > 20 No data Sodari 8(NNGOs) 12 Localities Sectors Level of needs O per locality Total number of organizations SRCS IOM, SRCS SRCS SRCS IOM, SOS Sahel, SRCS Bara D Low Map legend A No. of organizations B Medium A State capital Umm Keddada per locality High Primary towns Total El Nehoud ABU Z Primary/paved road < 5 Acute Locality boundary 5 - 10 - 1 2 1 - 1 - - 3 - 3 Umm Keddada KalimendoState Boundary El Obeid 11 - 20 Undetermined Boundary > 20 WEST No data SRCS SRCS SRCS GAH SRCS Badya, SOS Sahel Wad Banda D SRCS KORDOFAN Shiekan GLA Abu Zabad Wad Banda El Nehoud U NORTH Abu Zabad En Nehoud Um Rawaba Localities Sectors DARFUR YEI -M Total Ghubaysh B Al Sunut A - 1 1 1 1 1 2 - 1 - 4 El Taweisha Al Qoz SRCS SRCS SRCS SRCS SRCS El Salam Ghubaysh Babanusa Lagawa IOM IOM Al Sunut Rashad T Ailliet Dilling Total Ghubaysh Abyei - Muglad KHOWAI AL Dalami Abu Karinka Habila Keilak - 1 1 1 - 1 - - 1 - 1 El Fula SUNU L Ed Daein A Total SOUTH - - 1 - - - - - 1 - 1 Adila KORDOFAN Um Heitan El Salam SRCS SRCS SRCS SC-S SRCS SRCS Heiban A Assalaya I Ed Daein EAST Babanussa Lagawa Reif Ashargi SRCS SRCS SRCS SC-S SRCS SOS Sahel SECS, Y SRCS Y Babanusa A DARFUR Heiban D UN /IOs & INGOs staff no. -

Rapid Assessment Report the Impact of Drought in Red Sea State, Sudan

Rapid Assessment Report On The impact of Drought in Red Sea State, Sudan 6 April 2018 Early Warning Early Action (EWEA) Initiative, FAO Sudan Rapid Assessment on the impact of drought in Red Sea State Early Warning Early Action (EWEA) Initiative, FAO Sudan Contents Page Acronyms and abbreviations ................................................................................................................... 2 Assessment Highlights ............................................................................................................................ 3 1. OVERVIEW ..................................................................................................................................... 4 2. BACKGROUND .............................................................................................................................. 5 3. ASSESSED AREAs ........................................................................................................................ 5 4. OBJECTIVE .................................................................................................................................... 6 5. METHODOLOGY ............................................................................................................................ 6 6. LIVELIHOOD PROFILE AND POPULATION ................................................................................. 7 7. RAINFALL AND KHOR BARAKA FLOODING ............................................................................... 8 8. LIVESTOCK ...................................................................................................................................