Improved Performance from South Africa Region

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

South Africa

PUBLIC VERSION DOC Investigation No. A-791-825 ITC Investigation Nos. 701-TA-___-___ and 731-TA- ___-___ Total No. of Pages: 370 AD/CVD Operations Petitioners’ Business Proprietary Information for Which Proprietary Treatment Has Been Requested Deleted at Exhibits AD-ZA-1 (Atts. 1, 2, 5, 7,), AD-ZA- 2, AD-ZA-4, and AD-ZA-5 PUBLIC VERSION BEFORE THE INTERNATIONAL TRADE ADMINISTRATION OF THE U.S. DEPARTMENT OF COMMERCE AND THE U.S. INTERNATIONAL TRADE COMMISSION ANTIDUMPING DUTY PETITION VOLUME XVI SOUTH AFRICA COMMON ALLOY ALUMINUM SHEET FROM BAHRAIN, BRAZIL, CROATIA, EGYPT, GERMANY, GREECE, INDIA, INDONESIA, ITALY, KOREA, OMAN, ROMANIA, SERBIA, SLOVENIA, SOUTH AFRICA, SPAIN, TAIWAN, AND TURKEY PETITIONERS: THE ALUMINUM ASSOCIATION COMMON ALLOY ALUMINUM SHEET TRADE ENFORCEMENT WORKING GROUP AND ITS INDIVIDUAL MEMBERS W. BRAD HUDGENS JOHN M. HERRMANN DAVID C. SMITH WILLIAM H. CROW II PAUL C. ROSENTHAL GRACE W. KIM EMILY R. MALOOF KATHLEEN W. CANNON MELISSA M. BREWER NEREUS JOUBERT R. ALAN LUBERDA JOSHUA R. MOREY VLADIMIR VARBANOV BROOKE M. RINGEL MATTHEW G. PEREIRA GEORGETOWN ECONOMIC KELLEY DRYE & WARREN LLP SERVICES, LLC 3050 K Street, N.W., Suite 400 3050 K Street, N.W. Washington, DC 20007 Washington, D.C. 20007 (202) 342-8400 (202) 945-6660 Counsel to Petitioners March 9, 2020 PUBLIC VERSION Table of Contents Page I COMMON ALLOY ALUMINUM SHEET FROM SOUTH AFRICA IS BEING SOLD OR OFFERED FOR SALE AT LESS THAN FAIR VALUE .......,.1 A. Introduction............... 1 B. Producers in South Africa."..'. ,2 C. Export Price or Constructed Export Price' .4 D. Normal Value........ 5 E. -

Deloitte Africa

Next >> Quick Tax Guide 2019/20 South Africa Making an impact that matters << Previous | Next >> Contents Individuals ........................................................................................................... 1 Tax Rates and Rebates ................................................................................................1 Exemptions ...................................................................................................................1 Deductions and Tax Credits .......................................................................................2 Benefits and Allowances .............................................................................................3 Retirement Fund Lump Sum Withdrawal Benefits .................................................4 Severance Benefits and Retirement Fund Lump Sum Benefits ...........................4 Companies and Trusts ....................................................................................... 5 Tax Rates ........................................................................................................................5 Capital Allowances ......................................................................................................6 Employees’ Tax ............................................................................................................7 Skills Development Levy (SDL) ...................................................................................7 Unemployment Insurance Fund (UIF) Contributions .............................................7 -

A Survey of Race Relations in South Africa: 1968

A survey of race relations in South Africa: 1968 http://www.aluka.org/action/showMetadata?doi=10.5555/AL.SFF.DOCUMENT.BOO19690000.042.000 Use of the Aluka digital library is subject to Aluka’s Terms and Conditions, available at http://www.aluka.org/page/about/termsConditions.jsp. By using Aluka, you agree that you have read and will abide by the Terms and Conditions. Among other things, the Terms and Conditions provide that the content in the Aluka digital library is only for personal, non-commercial use by authorized users of Aluka in connection with research, scholarship, and education. The content in the Aluka digital library is subject to copyright, with the exception of certain governmental works and very old materials that may be in the public domain under applicable law. Permission must be sought from Aluka and/or the applicable copyright holder in connection with any duplication or distribution of these materials where required by applicable law. Aluka is a not-for-profit initiative dedicated to creating and preserving a digital archive of materials about and from the developing world. For more information about Aluka, please see http://www.aluka.org A survey of race relations in South Africa: 1968 Author/Creator Horrell, Muriel Publisher South African Institute of Race Relations, Johannesburg Date 1969-01 Resource type Reports Language English Subject Coverage (spatial) South Africa, South Africa, South Africa, South Africa, South Africa, Namibia Coverage (temporal) 1968 Source EG Malherbe Library Description A survey of race -

Inside Africa

INSIDE AFRICA 17 February 2017 Now is the time to invest in Africa BRIEFS Africa • G20 foreign ministers to tackle fight against poverty in Africa • West African CFA franc zone to see strong growth, increased CONTENTS risks: IMF • Ecobank CEO wants 100 mln customers by 2020 In-Depth: Angola - Africa can become a global economic powerhouse. This is • Angola's economy contracted 4.3 percent in Q3, 2016 - stats how .......................................................................................... 2 agency • - Making Renewable Energy More Accessible in Sub-Saharan Angola inflation slows to 40.4 percent year/year in January • Non-resident investors will be able to invest in Angola Stock Africa ................................................................................. 3 Exchange • IMF, WORLD BANK& AFDB ................................................... 5 Eni starts production of East Pole field in Angola - state oil firm • INVESTMENTS ........................................................................... 8 Angola’s Endiama negotiates financing for another diamond project BANKING Egypt • Banks ....................................................................................................... 10 Italy's Eni to start production in Egypt by end of year Ivory Coast Markets 11 .................................................................................................... • Ivory Coast consumer inflation rises to 1.1 pct yr/yr in January ENERGY .................................................................................... -

1935 Time Capsule Part 3

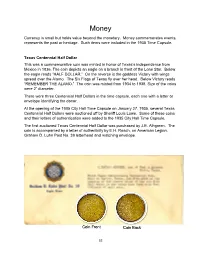

Money Currency is small but holds value beyond the monetary. Money commemorates events, represents the past or heritage. Such items were included in the 1935 Time Capsule. Texas Centennial Half Dollar This was a commemorative coin was minted in honor of Texas’s independence from Mexico in 1836. The coin depicts an eagle on a branch in front of the Lone Star. Below the eagle reads “HALF DOLLAR.” On the reverse is the goddess Victory with wings spread over the Alamo. The Six Flags of Texas fly over her head. Below Victory reads “REMEMBER THE ALAMO.” The coin was minted from 1934 to 1938. Size of the coins were 2” diameter. There were three Centennial Half Dollars in the time capsule, each one with a letter or envelope identifying the donor. At the opening of the 1905 City Hall Time Capsule on January 27, 1935, several Texas Centennial Half Dollars were auctioned off by Sheriff Louis Lowe. Some of these coins and their letters of authentication were added to the 1935 City Hall Time Capsule. The first auctioned Texas Centennial Half Dollar was purchased by J.E. Alhgreen. The coin is accompanied by a letter of authenticity by E.H. Roach, on American Legion, Graham D. Luhn Post No. 39 letterhead and matching envelope. Coin Front Coin Back 32 Letter Front 33 Letter Back 34 The second Texas Centennial Half Dollar was purchased at the same auction by E.E. Rummel. Shown below are the paperwork establishing the authenticity of the purchase by E.H. Roach, on American Legion, Graham D. -

2018 Budget Review

Budget Review 2018 Naational Treasury Republic of South Africa 21 February 2018 ISBN: 978-0-621-46020-9 RP: 03/2018 The Budget Review is compiled using the latest available information from departmental and other sources. Some of this information is unaudited or subject to revision. To obtain additional copies of this document, please contact: Communications Directorate National Treasury Private Bag X115 Pretoria 0001 South Africa Tel: +27 12 315 5944 Fax: +27 12 407 9055 The document is also available on the internet at: www.treasury.gov.za. ii iii iii iv iv v v vi Foreword The 2018 Budget arrives at a moment of opportunity for South Africa. A renewed sense of optimism has provided a much-needed boost to confidence and investment. The economic outlook has improved. And government has expressed a new resolve to strengthen policy coordination. Yet this positive turn of events should not blind us to the enormous economic and fiscal challenges facing our country. Economic growth is far too low to reduce alarmingly high unemployment and inequality. Revenue collection, on which government depends to fund social and economic spending programmes, will fall short of projections by R48.2 billion in 2017/18. The finances of several state- owned companies are in a precarious state. The 2017 Medium Term Budget Policy Statement (MTBPS) pointed out that extraordinary measures would be needed to stabilise the public finances. Without such measures, we would only delay the debt reckoning, and a growing share of spending would be absorbed by interest payments. The 2018 Budget proposals address these concerns with resolve. -

The World Bank

Document of The World Bank FOR OFFICIAL USE ONLY Ca- ZC~ / 3 7 Public Disclosure Authorized Report No. 7630-BO STAFF APPRAISALREPORT Public Disclosure Authorized REPUBLICOF BOLIVIA MINING SECTORREHABILITATION PROJECT APRIL 17, 1989 Public Disclosure Authorized Industry,Trade and FinanceOperations Division Country DepartmentIII Public Disclosure Authorized Latin America and the CaribbeanRegion This document hasa resticted dsibuto0vand may be used by oenpienlsoly In the perdonnanoe of their official duties. Its contents may - A otherwise be disclosed wt World Bank authorizatin CURRENCYEQUIVALENTS Currency Name - Boliviano US$1.00 - Bolivianos 2.47 Bolivianos 1.00 - US$0.405 FISCAL YEAR January 1 to December 31 WEIGHTS AND MEASURES 1 meter (m) G 3.281 feet (ft) 1 kilometer (km) = 0.622 miles (mi) 1 kilogram (kg) 2.205 pounds (lb) 1 troy ounce (troy oz) - 31.: grams 1 gram (g) - .032 troy ox 1 metric tonne (mt) - S2,151 troy oz | 2.205 lbs 1 short ton (T) - 2,000 lbs PRINCIPAL ABBREVIATIONS AND ACRONYMS BAMIN - Banco Minero BCB - Banco Central de Bolivia SA - Banco Industrial SA . - Centro de Investigacion Minero Metalurgica IMITBOL - Corporacion Hinera de Bolivia -'D - Development Credit Department (Central Bank) ,TAW - Empresa Nacional de Fundiciones FCNEM - Fondo Nacional de Exploracion Minera FSE - Fondo Social de Emergencia FSTMN - Federacion Sindical de Trabajadores Mineros de Bolivia GEOBOL - Servicio Geologico de Bolivia IDB - Interamerican Developi*ent Bank IDM - Instituto de Desarrollo Minero INK - Instituto de Investigacion Minero Metalurgica MMK - Ministry of Mining and Metallurgy STCM - Servicio Tecnico del Cadastro Minero FOR OMFCIL USE ONLY STAFF APPRAISAL REPORT BOLIVIA MINING SECTOR REHABILITATION PROJECT TABLE OF CONTENTS Page No. -

Elimination of the One Cent Coin the Bahamian One Cent Coin Or the “Penny” Is Being Phased

Central Bank of The Bahamas FAQS: Elimination of the One Cent Coin The Bahamian one cent coin or the “penny” is being phased out of circulation. After the end of 2020 it will no longer be legal tender in The Bahamas. It is further proposed that circulation of or acceptance of US pennies will cease at the same time as the Bahamian coin. Why is the one cent coin or penny being phased out? Rising cost of production relative to face value Increased accumulation and non-use of pennies The significant handling cost of pennies When will the Central Bank stop distributing the penny? The Central Bank will stop distributing pennies to commercial banks on the 31st January 2020. Financial institutions will no longer be providing new supplies of the coins to consumers and businesses. Are businesses required to accept pennies after the end of January 2020? NO. Businesses may decide to stop accepting pennies anytime after the end of January 2020. Can businesses continue to accept pennies after the end of December 2020? NO. Businesses will not be able to accept payment or give change in one cent pieces after the end of December 2020. All cash payments will to be rounded to the nearest five cents. How will cash amounts be rounded? Business must round the total amount due to the nearest five cents If your total bill is $9.42 or $9.41. The nearest five cents to either of these would be $9.40 If your total bill is $9.43 or $9.44, the nearest five cents to either of these would be $9.45. -

A History of the Canadian Dollar 53 Royal Bank of Canada, $5, 1943 in 1944, Banks Were Prohibited from Issuing Their Own Notes

Canada under Fixed Exchange Rates and Exchange Controls (1939-50) Bank of Canada, $2, 1937 The 1937 issue differed considerably in design from its 1935 counterpart. The portrait of King George VI appeared in the centre of all but two denominations. The colour of the $2 note in this issue was changed to terra cotta from blue to avoid confusion with the green $1 notes. This was the Bank’s first issue to include French and English text on the same note. The war years (1939-45) and foreign exchange reserves. The Board was responsible to the minister of finance, and its Exchange controls were introduced in chairman was the Governor of the Bank of Canada through an Order-in-Council passed on Canada. Day-to-day operations of the FECB were 15 September 1939 and took effect the following carried out mainly by Bank of Canada staff. day, under the authority of the War Measures Act.70 The Foreign Exchange Control Order established a The Foreign Exchange Control Order legal framework for the control of foreign authorized the FECB to fix, subject to ministerial exchange transactions, and the Foreign Exchange approval, the exchange rate of the Canadian dollar Control Board (FECB) began operations on vis-à-vis the U.S. dollar and the pound sterling. 16 September.71 The Exchange Fund Account was Accordingly, the FECB fixed the Canadian-dollar activated at the same time to hold Canada’s gold value of the U.S. dollar at Can$1.10 (US$0.9091) 70. Parliament did not, in fact, have an opportunity to vote on exchange controls until after the war. -

CURRICULUM VITAE JONATHAN CROWTHER OPERATIONS MANAGER Environmental Management Planning & Approvals, Africa

CURRICULUM VITAE JONATHAN CROWTHER OPERATIONS MANAGER Environmental Management Planning & Approvals, Africa QUALIFICATIONS M.Sc 1988 Environmental Science B.Sc (Hons) 1983 Geology B.Sc 1982 Geology and Geography z EXPERTISE Jonathan is the SLR Operations Manager for Environmental Management Planning & Approvals, Africa. He has over 30 years of experience with expertise in a wide Environmental Impact and range of environmental disciplines, including Environmental Impact and Social Social Assessment Assessments (ESIA), Environmental Management Plans, Environmental Planning, Environmental Environmental Compliance & Monitoring, and Public Participation & Facilitation. Management He has project managed a large number of offshore oil and gas EIAs for various Plans/Programmes exploration and production activities in Southern Africa. He also has extensive Public Participation & experience in large scale infrastructure projects including some of the largest road Facilitation projects in South Africa, ESIAs for waste landfill facilities, general industry and the Environmental Compliance built environment. & Monitoring PROJECTS Oil and Gas Exploration and Production Total E&P South Africa B.V. Provided environmental support ahead of an exploration well drilling operation, Provision of environmental environmental compliance services during the drilling operation and appointed to services for well drilling in prepare a close-out report on completion of the drilling operation. Project director, Block 11B/12B, offshore client liaison, report compilation and ECO services. South Coast, South Africa (2019 - ongoing) . 1 CURRICULUM VITAE JONATHAN CROWTHER Total E&P South Africa B.V. TEPSA is the holder of an Environmental Management Programme to undertake Application to amend exploration well drilling in Block 11B/12B offshore of the South Coast, South Africa. Environmental Management An amendment application was undertaken to change the well completion status Programme Block 11B/12B, described in the programme. -

Flower Route Map 2014 LR

K o n k i e p en w R31 Lö Narubis Vredeshoop Gawachub R360 Grünau Karasburg Rosh Pinah R360 Ariamsvlei R32 e N14 ng Ora N10 Upington N10 IAi-IAis/Richtersveld Transfrontier Park Augrabies N14 e g Keimoes Kuboes n a Oranjemund r Flower Hotlines O H a ib R359 Holgat Kakamas Alexander Bay Nababeep N14 Nature Reserve R358 Groblershoop N8 N8 Or a For up-to-date information on where to see the Vioolsdrif nge H R27 VIEWING TIPS best owers, please call: Eksteenfontein a r t e b e e Namakwa +27 (0)79 294 7260 N7 i s Pella t Lekkersing t Brak u West Coast +27 (0)72 938 8186 o N10 Pofadder S R383 R383 Aggeneys Flower Hour i R382 Kenhardt To view the owers at their best, choose the hottest Steinkopf R363 Port Nolloth N14 Marydale time of the day, which is from 11h00 to 15h00. It’s the s in extended ower power hour. Respect the ower Tu McDougall’s Bay paradise: Walk with care and don’t trample plants R358 unnecessarily. Please don’t pick any buds, bulbs or N10 specimens, nor disturb any sensitive dune areas. Concordia R361 R355 Nababeep Okiep DISTANCE TABLE Prieska Goegap Nature Reserve Sun Run fels Molyneux Buf R355 Springbok R27 The owers always face the sun. Try and drive towards Nature Reserve Grootmis R355 the sun to enjoy nature’s dazzling display. When viewing Kleinzee Naries i R357 i owers on foot, stand with the sun behind your back. R361 Copperton Certain owers don’t open when it’s overcast. -

Sponsored by the Department of Science and Technology Volume

Volume 26 Number 3 • August 2015 Sponsored by the Department of Science and Technology Volume 26 Number 3 • August 2015 CONTENTS 2 Reliability benefit of smart grid technologies: A case for South Africa Angela Masembe 10 Low-income resident’s preferences for the location of wind turbine farms in the Eastern Cape Province, South Africa Jessica Hosking, Mario du Preez and Gary Sharp 19 Identification and characterisation of performance limiting defects and cell mismatch in photovoltaic modules Jacqui L Crozier, Ernest E van Dyk and Frederick J Vorster 27 A perspective on South African coal fired power station emissions Ilze Pretorius, Stuart Piketh, Roelof Burger and Hein Neomagus 41 Modelling energy supply options for electricity generations in Tanzania Baraka Kichonge, Geoffrey R John and Iddi S N Mkilaha 58 Options for the supply of electricity to rural homes in South Africa Noor Jamal 66 Determinants of energy poverty in South Africa Zaakirah Ismail and Patrick Khembo 79 An overview of refrigeration and its impact on the development in the Democratic Republic of Congo Jean Fulbert Ituna-Yudonago, J M Belman-Flores and V Pérez-García 90 Comparative bioelectricity generation from waste citrus fruit using a galvanic cell, fuel cell and microbial fuel cell Abdul Majeed Khan and Muhammad Obaid 100 The effect of an angle on the impact and flow quantity on output power of an impulse water wheel model Ram K Tyagi CONFERENCE PAPERS 105 Harnessing Nigeria’s abundant solar energy potential using the DESERTEC model Udochukwu B Akuru, Ogbonnaya