The Airline Business, Second Edition

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

![Contents [Edit] Africa](https://docslib.b-cdn.net/cover/9562/contents-edit-africa-79562.webp)

Contents [Edit] Africa

Low cost carriers The following is a list of low cost carriers organized by home country. A low-cost carrier or low-cost airline (also known as a no-frills, discount or budget carrier or airline) is an airline that offers generally low fares in exchange for eliminating many traditional passenger services. See the low cost carrier article for more information. Regional airlines, which may compete with low-cost airlines on some routes are listed at the article 'List of regional airlines.' Contents [hide] y 1 Africa y 2 Americas y 3 Asia y 4 Europe y 5 Middle East y 6 Oceania y 7 Defunct low-cost carriers y 8 See also y 9 References [edit] Africa Egypt South Africa y Air Arabia Egypt y Kulula.com y 1Time Kenya y Mango y Velvet Sky y Fly540 Tunisia Nigeria y Karthago Airlines y Aero Contractors Morocco y Jet4you y Air Arabia Maroc [edit] Americas Mexico y Aviacsa y Interjet y VivaAerobus y Volaris Barbados Peru y REDjet (planned) y Peruvian Airlines Brazil United States y Azul Brazilian Airlines y AirTran Airways Domestic y Gol Airlines Routes, Caribbean Routes and y WebJet Linhas Aéreas Mexico Routes (in process of being acquired by Southwest) Canada y Allegiant Air Domestic Routes and International Charter y CanJet (chartered flights y Frontier Airlines Domestic, only) Mexico, and Central America y WestJet Domestic, United Routes [1] States and Caribbean y JetBlue Airways Domestic, Routes Caribbean, and South America Routes Colombia y Southwest Airlines Domestic Routes y Aires y Spirit Airlines Domestic, y EasyFly Caribbean, Central and -

Delivering Excellent Service Quality in Low Cost Aviation

MASTER THESIS IMM – International Marketing & Management DELIVERING EXCELLENT SERVICE QUALITY IN LOW COST AVIATION A Process Perspective on the Passenger Market in Copenhagen Airport December 2009 Rasmus Lindstrøm Jensen Advisor: Jesper Clement COPENHAGEN BUSINESS SCHOOL Preface The following thesis is composed on the basis of empirical data collected at Norwegian, Cimber Sterling and six individual airline passengers. I would like to thank Lone Koch (Vice President of Product Management, Cimber Sterling ) and Johan Bisgaard Larsen (Marketing Manager, Norwegian - CPH ) for the kindness and dedication. They contributed with precious information in devising the problem statement and further made the execution of the questionnaire survey possible. Further, I would like to thank Adam Høyer ( Co+Hoegh ), Christoffer Casparij ( Væksthus Sjælland ), Lene Susgaard Henriksen ( Novo Nordisk ), Morten Kaaber ( Muuto New Nordic ), Ditte Clément ( CBS ) and Line Lundø ( CBS ) for contributing with valuable information in the focus group interview. Finally, I would like to thank my advisor Jesper Clement for being a committed and pleasant advisor and sparring partner throughout the entire process. Since the number of pages in thesis exceeds 80 pages a calculation of the magnitude has been made to keep the record straight. The calculation are based on the assumption that one normal page corresponds to 2275 characters and one figure corresponds to 800 characters. Thus the actual number of pages is calculated; (169.675 + (800*16)/2275 = 80,2 pages). Consequently, the thesis keeps within the specified boundaries. Copenhagen, December 2009 Rasmus Lindstrøm Jensen Executive Summary This thesis explores the concept of service quality and customer satisfaction with low cost airlines in Copenhagen Airport. -

Peculiarities of Development of the Low-Cost Airlines in Russian and Norwegian Context

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Brage Nord Open Research Archive Logistics and transport BE303E 003 Peculiarities of development of the low-cost airlines in Russian and Norwegian context by Elena Toramanyan Spring, 2007 Abstract E. Toramanyan, Master thesis ABSTRACT Low-cost flights per se become more and more popular in the world airline industry, while in Russia the first low-cost carrier has recently appeared. The purpose of this paper is to investigate the phenomenon of low-cost carriers, peculiarities of the development of the low-cost airlines in the context of Russian Federation and Norway. In order to cover the topic, deep literature review and qualitative research were carried out. In the paper, I attempted to follow history, analyze reasons for low-cost flights, advantages and disadvantages of low-cost carriers, scrutinize perspectives and peculiarities of the low-cost airline market in Russia and Norway, and analyze future opportunities. Under these circumstances, case study method and interviews as primary information sources and reports and articles written by airline experts as secondary sources were used. Two companies were under the research: Sky Express – a Russian low-cost airline company launched the market this year, and a Norwegian low-cost airline company, a member of European Low Fares Airline Association, Norwegian Air Shuttle. Deep literature review concerning low-cost airlines and empirical findings showed that the phenomenon of low fares has its peculiarities on a particular market. In order to understand the role of context regarding the research question, I tried to find similarities and to reveal differences in the activities of two companies with the help of PESTE analysis. -

EVAIR Safety Bulletin No 4

Cooperative Network Design EVAIR Safety Bulletin No 4 Summer Seasons 2006-2009 Evolution EUROCONTROL EVAIR_bulletin04.indd 1 15/02/10 14:15 EUROCONTROL VOLUNTARY ATM INCIDENT Data providers REPORTING (EVAIR) The number of EVAIR ATM incident data providers among commer- cial airlines has been increasing year on year. By the end of 2009, 63 SUMMER SEASONS 2006-2009 EVOLUTION airlines were providing ATM incident reports to EVAIR. The airlines which contribute to EVAIR account for 50% of the overall European EXECUTIVE SUMMARY air traffic. The statistics in the EVAIR Safety Bulletin No 4 cover the summer Main trends periods (April - September) 2006 to 2009. The statistics are based Eight main ATM contributors are used as the basis for monitoring: on the ATM/CNS incident reports collected manually and ACAS RAs collected automatically from one Mode-S radar station. The 1. Mistakes; main data providers are commercial airlines and ANSPs providing 2. Spoken Communication; feedback to airlines’ incident reports and the ACAS RAs from the 3. Operational Communication; Mode-S radar station. 4. Traffic and Airspace problems; 5. Traffic Information; Data collection 6. Lapses; Through the manual data provision (commercial airlines and feed- 7. ATC Clearance; back from ANSPs) EVAIR collected approximately 1500 reports for 8. Coordination. the summer seasons from 2006 to 2009. For the same period, 2637 valid ACAS RAs were collected automatically from the Mode S radar During the summer periods 2006-2009 in absolute figures, Mistakes station. with 27%, Spoken communication with 19%, Operational Communi- cation and Traffic information with 11% each make almost 70% of the The number of reports EVAIR collects has grown each year. -

Airline Schedules

Airline Schedules This finding aid was produced using ArchivesSpace on January 08, 2019. English (eng) Describing Archives: A Content Standard Special Collections and Archives Division, History of Aviation Archives. 3020 Waterview Pkwy SP2 Suite 11.206 Richardson, Texas 75080 [email protected]. URL: https://www.utdallas.edu/library/special-collections-and-archives/ Airline Schedules Table of Contents Summary Information .................................................................................................................................... 3 Scope and Content ......................................................................................................................................... 3 Series Description .......................................................................................................................................... 4 Administrative Information ............................................................................................................................ 4 Related Materials ........................................................................................................................................... 5 Controlled Access Headings .......................................................................................................................... 5 Collection Inventory ....................................................................................................................................... 6 - Page 2 - Airline Schedules Summary Information Repository: -

Industry Monitor the EUROCONTROL Bulletin on Air Transport Trends

Issue N°141. 31/05/12 Industry Monitor The EUROCONTROL bulletin on air transport trends European flights declined by 2.7% in April. EUROCONTROL statistics and forecasts 1 May update of the two-year flight forecast is for a Other statistics and forecasts 2 downward revision of 0.4 percentage points to 1.7% fewer flights in 2012 than in 2011. The Passenger airlines 3 outlook for 2013 is for 1.6% growth. Cargo 6 ACI reported overall passenger traffic at Financial results of airlines 7 European airports to be up 3.4% in 1Q12 on Environment 7 1Q11 whereas aircraft movements decreased by 1.7%. Airports 8 Oil 8 European airlines selected in this bulletin recorded €1.7 billion operating losses during Aircraft Manufacturing 9 1Q12, a 17% increase on the same period a year Economy 9 ago. Regulation 9 Oil prices reduced to €79 per barrel on 31 May, Fares 9 dropping 15% from April. EUROCONTROL statistics and forecasts European flights declined by 2.7% in April compared with the same month last year and were similar to April 2009 levels. Strikes in Portugal, but mainly in France resulted in circa 5,000 flight cancellations. With the exception of charter and low-cost, both up 3% and 1.2% respectively on April 2011, other market segments were down circa 4% (see Figure 1) (EUROCONTROL, May). Based on preliminary data for delay from all causes, 36% of flights were delayed on departure in April, resulting in a 3 percentage point increase on April 2011. Analysis of the causes of delay shows a notable increase in reactionary delay. -

1 Determinants for Seat Capacity Distribution in EU and US, 1990-2009

Determinants for seat capacity distribution in EU and US, 1990-2009. Pere SUAU-SANCHEZ*1; Guillaume BURGHOUWT 2; Xavier FAGEDA 3 1Department of Geography, Universitat Autònoma de Barcelona, Edifici B – Campus de la UAB, 08193 Bellaterra, Spain E-mail: [email protected] 2Airneth, SEO Economic Research, Roetersstraat 29, 1018 WB Amsterdam, The Netherlands E-mail: [email protected] 3Department of Economic Policy, Universitat de Barcelona, Av.Diagonal 690, 08034 Barcelona, Spain E-mail: [email protected] *Correspondance to: Pere SUAU-SANCHEZ Department of Geography, Universitat Autònoma de Barcelona, Edifici B – Campus de la UAB, 08193 Bellaterra, Spain E-mail: [email protected] Telephone: +34 935814805 Fax: +34 935812100 1 Determinants for seat capacity distribution in EU and US, 1990-2009. Abstract Keywords: 2 1. Introduction Air traffic is one of the factors influencing and, at the same time, showing the position of a city in the world-city hierarchy. There is a positive correlation between higher volumes of air passenger and cargo flows, urban growth and the position in the urban hierarchy of the knowledge economy (Goetz, 1992; Rodrigue, 2004; Taylor, 2004; Derudder and Witlox, 2005, 2008; Bel and Fageda, 2008). In relation to the configuration of mega-city regions, Hall (2009) remarks that it is key to understand how information moves in order to achieve face-to-face communication and, over long distances, it will continue to move by air, through the big international airports (Shin and Timberlake, 2000). This paper deals with the allocation of seat capacity among all EU and US airports over a period of 20 years. -

The Undisputed Leader in World Travel CONTENTS

Report & Accounts 1996-97 ...the undisputed leader in world travel CONTENTS Highlights of the year 1 Chairman’s Statement 2 THE NEXT Chief Executive’s Statement 5 Board Members 8 The Board and Board Committees DECADEIN FEBRUARY 1997 and the Report of the Remuneration Committee 10 British Airways celebrated 10 years of privatisation, with a Directors’ Report 14 renewed commitment to stay at the forefront of the industry. Report of the Auditors on Corporate Governance matters 17 Progress during the last decade has been dazzling as the airline Operating and Financial established itself as one of the most profitable in the world. Review of the year 18 Statement of Directors’ responsibilities 25 Report of the Auditors 25 Success has been built on a firm commitment to customer service, cost control and Group profit and loss account 26 the Company’s ability to change with the times and new demands. Balance sheets 27 As the year 2000 approaches, the nature of the industry and Group cash flow statement 28 competition has changed. The aim now is to create a new Statement of total recognised British Airways for the new millennium, to become the undisputed gains and losses 29 leader in world travel. Reconciliation of movements in shareholders’ funds 29 This involves setting a new direction for the Company with a Notes to the accounts 30 new Mission, Values and Goals; introducing new services and Principal investments 54 products; new ways of working; US GAAP information 55 new behaviours; a new approach to The launch of privatisation spelt a Five year summaries 58 service style and a brand new look. -

Travel Information Örnsköldsvik Airport

w v TRAVEL INFORMATION TO AND FROM OER ÖRNSKÖLDSVIK AIRPORT // OVERVIEW Two airlines fly to Örnsköldsvik AirLeap fly from Stockholm Arlanda and BRA-Braathens fly from 1 Stockholm Bromma. 32 flights a week on average Many connections possible via 2 Stockholm’s airports. Örnsköldsvik is located 25 km from the airport, only 20 minutes 3 with Airport taxi or rental car. Book your travel via Air Leap (LPA) www.airleap.se BRA-Braathens Regional 4 Airlines (TF) www.flygbra.se CONNECTIONS WITH 2 AIRLINES GOOD CONNECTIONS good flight connections is essential for good business relationships and Örnsköldsvik Airport fulfills that requirement. As of 2 February, two airlines operate the airport, Air Leap and BRA – Braathens Regional Airlines. Air Leap (IATA code LPA) operates between Örnsköldsvik and Stockholm Arlanda Airport (ARN) and BRA (IATA code TF) between Örnsköldsvik och Stockholm Bromma Airport (BMA). Together the airlines offer on average 32 flights per week, in each direction. air leap operate Saab2000 with 50 Finnair is also a member of ”One minutes flight time to Örnsköldsvik. World Alliance” which gives bene- At Arlanda you find Air Leap at Termi- fits for its members and One World nal 3, with walking distance to Termi- members when travelling on flights nal 2 (SkyTeam, One World airlines) connected to the Finnair Network. and to Terminal 5 (Star Alliance air- Enclosed is a list of some of the lines). Tickets for connecting flights more common connections that are need to be purchased separately and currently possible with one ticket checked luggage brought through and checked in baggade to your customs at Arlanda and checked-in final destination. -

Bombardier Business Aircraft and Are Not Added to This Report

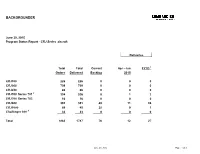

BACKGROUNDER June 30, 2015 Program Status Report - CRJ Series aircraft Deliveries Total Total Current Apr - Jun FYTD 1 Orders Delivered Backlog 2015 CRJ100 226 226 0 0 0 CRJ200 709 709 0 0 0 CRJ440 86 86 0 0 0 CRJ700 Series 701 2 334 326 8 1 2 CRJ700 Series 705 16 16 0 0 0 CRJ900 391 351 40 11 24 CRJ1000 68 40 28 0 1 Challenger 800 3 33 33 0 0 0 Total 1863 1787 76 12 27 June 30, 2015 Page 1 of 3 Program Status Report - CRJ Series aircraft CRJ700 CRJ700 CRJ700 CRJ700 Customer Total Total CRJ100 CRJ100 CRJ200 CRJ200 CRJ440 CRJ440 Series 701 Series 701 Series 705 Series 705 CRJ900 CRJ900 CRJ1000 CRJ1000 Orders Delivered Backlog Ordered Delivered Ordered Delivered Ordered Delivered Ordered Delivered Ordered Delivered Ordered Delivered Ordered Delivered Adria Airways 12 11 1 0 0 5 5 0 0 0 0 0 0 7 6 0 0 AeroLineas MesoAmericanas 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 Air Canada 56 56 0 24 24 17 17 0 0 0 0 15 15 0 0 0 0 Air Dolimiti 5 5 0 0 0 5 5 0 0 0 0 0 0 0 0 0 0 Air Littoral 19 19 0 19 19 0 0 0 0 0 0 0 0 0 0 0 0 Air Nostrum 81 56 25 0 0 35 35 0 0 0 0 0 0 11 11 35 10 Air One 10 10 0 0 0 0 0 0 0 0 0 0 0 10 10 0 0 Air Wisconsin 64 64 0 0 0 64 64 0 0 0 0 0 0 0 0 0 0 American Airlines 54 30 24 0 0 0 0 0 0 0 0 0 0 54 30 0 0 American Eagle 47 47 0 0 0 0 0 0 0 47 47 0 0 0 0 0 0 Arik Air 7 5 2 0 0 0 0 0 0 0 0 0 0 4 4 3 1 Atlantic Southeast (ASA) 57 57 0 0 0 45 45 0 0 12 12 0 0 0 0 0 0 Atlasjet 3 3 0 0 0 0 0 0 0 0 0 0 0 3 3 0 0 Austrian arrows 4 13 13 0 0 0 13 13 0 0 0 0 0 0 0 0 0 0 BRIT AIR 49 49 0 20 20 0 0 0 0 15 15 0 0 0 0 14 14 British European 4 4 0 0 0 4 4 0 0 0 0 0 0 0 0 0 0 China Eastern Yunnan 6 6 0 0 0 6 6 0 0 0 0 0 0 0 0 0 0 China Express 28 18 10 0 0 0 0 0 0 0 0 0 0 28 18 0 0 Cimber Air 2 2 0 0 0 2 2 0 0 0 0 0 0 0 0 0 0 COMAIR 130 130 0 110 110 0 0 0 0 20 20 0 0 0 0 0 0 DAC AIR 2 2 0 0 0 2 2 0 0 0 0 0 0 0 0 0 0 Delta Connection 168 168 0 0 0 94 94 0 0 30 30 0 0 44 44 0 0 Delta Air Lines 40 40 0 0 0 0 0 0 0 0 0 0 0 40 40 0 0 Estonian Air 3 3 0 0 0 0 0 0 0 0 0 0 0 3 3 0 0 The Fair Inc. -

Air Transport Industry Analysis Report

Annual Analyses of the EU Air Transport Market 2016 Final Report March 2017 European Commission Annual Analyses related to the EU Air Transport Market 2016 328131 ITD ITA 1 F Annual Analyses of the EU Air Transport Market 2013 Final Report March 2015 Annual Analyses of the EU Air Transport Market 2013 MarchFinal Report 201 7 European Commission European Commission Disclaimer and copyright: This report has been carried out for the Directorate General for Mobility and Transport in the European Commission and expresses the opinion of the organisation undertaking the contract MOVE/E1/5-2010/SI2.579402. These views have not been adopted or in any way approved by the European Commission and should not be relied upon as a statement of the European Commission's or the Mobility and Transport DG's views. The European Commission does not guarantee the accuracy of the information given in the report, nor does it accept responsibility for any use made thereof. Copyright in this report is held by the European Communities. Persons wishing to use the contents of this report (in whole or in part) for purposes other than their personal use are invited to submit a written request to the following address: European Commission - DG MOVE - Library (DM28, 0/36) - B-1049 Brussels e-mail (http://ec.europa.eu/transport/contact/index_en.htm) Mott MacDonald, Mott MacDonald House, 8-10 Sydenham Road, Croydon CR0 2EE, United Kingdom T +44 (0)20 8774 2000 F +44 (0)20 8681 5706 W www.mottmac.com Issue and revision record StandardSta Revision Date Originator Checker Approver Description ndard A 28.03.17 Various K. -

Hva Er Rovatferd?

Hovedoppgave for mastergradsstudiet i samfunnsøkonomi Hva er rovatferd? Eksempler fra norsk luftfart Harald Evensen Mai 2006 Økonomisk institutt Universitetet i Oslo i Forord Det er de store endringene i flymarkedet, og den spesielle konkurransesituasjonen, som gjorde at jeg ønsket å skrive om dette temaet. De fleste av oss har merket at det er billigere å fly til Bergen i dag, enn hva tilfellet var for kun noen få år siden. Jeg håper denne oppgaven kan være med på å belyse hva som har skjedd i det norske flymarkedet, og hvilke former konkurransen har tatt de siste åtte årene, etter åpningen av Oslo Lufthavn Gardermoen. Min veileder, Professor Tore Nilssen ved Økonomisk institutt ved Universitetet i Oslo, har vært til stor hjelp både når det gjelder å konsentrere oppgaven rundt ett tema – rovatferd – og å komme med konkrete tilbakemeldinger som har gjort innhold og språk bedre. Jeg vil også benytte anledningen til å takke min kjæreste, Kari, som har lest korrektur og passet på at jeg ikke har sittet og furtet for lenge de gangen det har gått trått med oppgaven. Oslo, 2. mai 2006 Harald Evensen ii Innhold Forord………………………………………………………………………………......... i 1. Innledning………………………………………………………………………... 1 2. Luftfartsmarkedet i Norge……………………………………………………… 3 2.1 Beskrivelse av markedet………………………………………………….. 3 2.2 Kampen mot Color Air…………………………………………………… 7 2.3 Braathens gir opp…………………………………………………………. 9 2.4 Bonusavtaler og storkundeavtaler………………………………………… 11 2.4.1 Bonusavtaler………………………………………………………. 11 2.4.2 Storkundeavtaler………………………………………………….. 12 2.5 Konkurranse på nytt………………………………………………………. 13 2.6 Rovatferd mot en liten konkurrent?............................................................. 15 2.7 Sunn konkurranse?....................................................................................... 17 3. Rovatferd………………………………………………………………………… 19 3.1 Hva er rovatferd? Definisjoner og utdypning………………………….....