Investor Presentation for the Merger(3.0MB)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Impact of Specialization in Gynecology and Obstetrics Departments On

Adachi et al. Health Economics Review 2013, 3:31 http://www.healtheconomicsreview.com/content/3/1/31 RESEARCH Open Access Impact of specialization in gynecology and obstetrics departments on pregnant women’s choice of maternity institutions Yoshimi Adachi1*, Hiroyasu Iso1, Junyi Shen2, Kanami Ban3, On Fukui4, Hiroyuki Hashimoto5, Takako Nakashima6, Kenichiro Morishige7 and Tatuyoshi Saijo8 Abstract In April 2008, specialization in gynecology and obstetrics departments was introduced in the Sennan area of Osaka prefecture in Japan that aimed at solving the problems of regional provisions of obstetrics services (e.g., shortage of obstetricians, overworking of obstetricians, and provision of specialist maternity services for high-risk pregnancies). Under this specialization, the gynecology and obstetrics departments in two city hospitals were combined and reconstructed into two centers, i.e., the gynecological care center in Kaizuka City Hospital and the prenatal care center in Izumisano City Hospital. This paper investigates to what extent and how this specialization affected pregnant women’s choices of the prenatal care center and other maternity institutions. We used birth certificate data of 15,927 newborns from the Sennan area between April 1, 2007 and March 30, 2010, for Before and After Analysis to examine changes in pregnant women’s choices of maternity institutions before and after the specialization was instituted. Our results indicated that this specialization scheme was, to some extent, successful on the basis of providing maternity services for high-risk pregnancies at the prenatal care center (i.e., Izumisano City Hospital) and having created a positive effect by pregnant women to other facilities in the nearby area. -

Investor Presentation -Appendix- (Ended Jun. 2017)

nd Period Fiscal Period22 ended June 30, 2017 * Fractions of the stated amounts are cut off and those of the ratios and years are rounded off unless otherwise indicated. Therefore, the aggregation of the figures Index stated hereupon are not necessarily identical to the total. 1. FINANCIAL HIGHLIGHTS • Overview of financial results • Portfolio overview - Office in Osaka area 2 34 for the fiscal period ended June 30, 2017 (22nd Period) 4 • Portfolio overview - Office in Osaka area 3 35 • 22nd Period financial results – Comparison to previous period 5 • Portfolio overview – TK interest and others 36 • 22nd Period financial results – Comparison to initial forecasts 6 • Newly acquired assets 37 • 22nd Period financial results – • Disposed assets 41 Breakdown of change from previous period 7 • Balance sheet 8 5. FINANCING STRATEGY • Income statement 9 • Major financing- related figures and investment corporation bonds 43 2. FORECASTS FOR THE 23RD AND 24TH FISCAL PERIOD • Financial status 44 • Forecasts for the 23rd and 24th fiscal period 11 • Lender composition and maturity ladder (as of end of Jun. 2017) 45 • Breakdown of change from previous period 12 • Outstanding borrowings (as of end of Jun. 2017) 46 3. RESULTS FOR THE 22ND FISCAL PERIOD • Lender composition and maturity ladder (as of end of Jul. 2017) 47 • Occupancy 14 • Outstanding borrowings (as of end of Jul. 2017) 48 • Portfolio operation 15 6. MARKET ENVIRONMENT • Occupancy by property 16 • Office market data 1 (Tokyo 23 districts) 51 • Revisions and gaps in rents 17 • Office market data 2 (Tokyo 23 districts) 52 • Surveys on tenants’ satisfaction 18 • Office market data 3 (Osaka) 53 • Initiatives in Properties in Portfolio 19 • Office market data 4 (Osaka) 54 4. -

Cross-Regional Perinatal Healthcare Systems: Efforts in Greater Kansai Area, Japan

Conferences and Lectures Cross-Regional Perinatal Healthcare Systems: Efforts in Greater Kansai Area, Japan JMAJ 53(2): 86–90, 2010 1 Noriyuki SUEHARA* Fukui Kyoto Shiga Introduction Hyogo Aiming to create a society in which any woman can give birth without any sense of anxiety, Japan’s Ministry of Health, Labour and Welfare Osaka Mie (MHLW) has been promoting the establishment Nara and systemization of general perinatal medical Tokushima centers nationwide since 1996. Wakayama In Osaka Prefecture, Neonatal Mutual Coop- erative System (NMCS) was established in 1977, and then Obstetric & Gynecologic Cooperative System (OGCS) in 1978. This illustrates that sys- 100km temization of perinatal healthcare is in progress in Osaka. Under OGCS, six hospitals (namely Osaka Medical Center and Research Institute for Maternal and Child Health, Osaka City General Hospital, Takatsuki General Hospital, Aizenbashi Hospital, Kansai Medical University Hirakata Hospital, and Yodogawa Christian Hospital) are designated as Base Hospitals, plus, nine other facilities are designated as Sub-base Hospitals. These hospitals play a large role in the Osaka’s regional perinatal healthcare system. In 1999, Osaka Council on Perinatal Health- Tokyo care Strategies was established, and in December of that year Osaka Medical Center and Research 500 km Institute for Maternal and Child Health was des- ignated as the general perinatal medical center for Osaka Prefecture. Subsequently, four addi- fectural Government formulated Guideline for tional hospitals (Takatsuki General Hospital, Improving the Perinatal Emergency Medical Aizenbashi Hospital, Kansai Medical University System, and 13 regional perinatal medical centers Hirakata Hospital, and Osaka University Hospi- were approved. Furthermore, Osaka Prefecture tal) were designated as general perinatal medical Guidelines for Prioritizing Perinatal Healthcare centers, serving as core facilities for perinatal Functions were drawn up in December 2008 based healthcare system in Osaka. -

Essentials for Living in Osaka (English)

~Guidebook for Foreign Residents~ Essentials for Living in Osaka (English) Osaka Foundation of International Exchange October 2018 Revised Edition Essentials for Living in Osaka Table of Contents Index by Category ⅠEmergency Measures ・・・1 1. Emergency Telephone Numbers 2. In Case of Emergency (Fire, Sudden Sickness and Crime) Fire; Sudden Illness & Injury etc.; Crime Victim, Phoning for Assistance; Body Parts 3. Precautions against Natural Disasters Typhoons, Earthquakes, Collecting Information on Natural Disasters; Evacuation Areas ⅡHealth and Medical Care ・・・8 1. Medical Care (Use of medical institutions) Medical Care in Japan; Medical Institutions; Hospital Admission; Hospitals with Foreign Language Speaking Staff; Injury or Sickness at Night or during Holidays 2. Medical Insurance (National Health Insurance, Nursing Care Insurance and others) Medical Insurance in Japan; National Health Insurance; Latter-Stage Elderly Healthcare Insurance System; Nursing Care Insurance (Kaigo Hoken) 3. Health Management Public Health Center (Hokenjo); Municipal Medical Health Center (Medical Care and Health) Ⅲ Daily Life and Housing ・・・16 1. Looking for Housing Applying for Prefectural Housing; Other Public Housing; Looking for Private Housing 2. Moving Out and Leaving Japan Procedures at Your Old Residence Before Moving; After Moving into a New Residence; When You Leave Japan 3. Water Service Application; Water Rates; Points of Concern in Winter 4. Electricity Electricity in Japan; Application for Electrical Service; Payment; Notice of the Amount of Electricity Used 5. Gas Types of Gas; Gas Leakage; Gas Usage Notice and Payment Receipt 6. Garbage Garbage Disposal; How to Dispose of Other Types of Garbage 7. Daily Life Manners for Living in Japan; Consumer Affairs 8. When You Face Problems in Life Ⅳ Residency Management System・Basic Resident Registration System for Foreign Nationals・Marriage・Divorce ・・・27 1. -

Storm Warning (Bofu-Keiho / 暴 風警報) Or an Emergency Warning (Tokubetsu-Keiho / 特別警報)

Class Cancellation due to Weather Warnings: Storm Warning (Bofu-keiho / 暴 風警報) or an Emergency Warning (Tokubetsu-keiho / 特別警報) At the moment, a typhoon is approaching Japan. Classes will be cancelled if any of the above warnings are issued. You can confirm the details of when class cancellation may occur according to areas and municipalities where warnings have been issued, and when the warning has been lifted on the following homepage or the table below. Kwansei Gakuin University Website Undergraduate: http://www.kwansei.ac.jp/a_affairs/a_affairs_000850.html Graduate : http://www.kwansei.ac.jp/a_affairs/a_affairs_002656.html Nishinomiya-Uegahara and Kobe-Sanda Warning/Strike Lifted Nishinomiya-Seiwa Campus Campus By 6:00 am All classes held as usual 1st period class cancelled By 8:00 am Both 2nd-5th period class held as usual Undergraduate 1st & 2nd period classes cancelled By 10:30 am All classes and Graduate 3rd - 5th period classes held as usual cancelled School 1st - 3rd period classes cancelled By 12:00 pm 4th - 5th period classes held as usual Any time after 12:00 pm All classes cancelled 1st - 5th period classes cancelled Graduate By 3:00 pm 6th – 7th period classes held as usual School only Any time after 3:00 pm All classes cancelled Areas Municipalities Hanshin Kobe, Amagasaki, Nishinomiya, Ashiya, Itami, Takarazuka, Kawanishi, Sanda, Inagawa Hokuban Tanba Nishiwaki, Sasayama, Tanba, Taka-cho Harima Nantobu Akashi, Kakogawa, Miki, Takasago, Ono, Kasai, Kato, Inami-cho, Harima-cho Osaka Osaka city Kita Osaka Toyonaka, Ikeda, Suita, Takatsuki, Ibaraki, Minoh, Settsu, Torimoto-cho, Toyono-cho, Nose-cho Tobu Osaka Moriguchi, Hirakata, Yao, Neyagawa, Daito, Kashiwara, Kadoma, Higashi Osaka, Shijonawate, Katano Minami Kawachi Tondabayashi, Kawachinagano, Matsubara, Habikino, Fujiidera, Osaka Sayama, Taishi-cho, Kanan-cho, Chihaya Asaka-mura Senshu Sakai, Kishiwada, Izumiotsu, Kaizuka, Izumisano, Izumi, Takaishi, Sennan, Hannan, Tadaoka-cho, Kumatori-cho, Tajiri-cho, Misaki-cho 8 September 2015 Organization for Academic Affairs Kwansei Gakuin University . -

Shibuya City Industry and Tourism Vision

渋谷区 Shibuya City Preface Preface In October 2016, Shibuya City established the Shibuya City Basic Concept with the goal of becoming a mature international city on par with London, Paris, and New York. The goal is to use diversity as a driving force, with our vision of the future: 'Shibuya—turning difference into strength'. One element of the Basic Concept is setting a direction for the Shibuya City Long-Term Basic Plan of 'A city with businesses unafraid to take risks', which is a future vision of industry and tourism unique to Shibuya City. Each area in Shibuya City has its own unique charm with a collection of various businesses and shops, and a great number of visitors from inside Japan and overseas, making it a place overflowing with diversity. With the Tokyo Olympic and Paralympic Games being held this year, 2020 is our chance for Shibuya City to become a mature international city. In this regard, I believe we must make even further progress in industry and tourism policies for the future of the city. To accomplish this, I believe a plan that further details the policies in the Long-Term Basic Plan is necessary, which is why the Industry and Tourism Vision has been established. Industry and tourism in Shibuya City faces a wide range of challenges that must be tackled, including environmental improvements and safety issues for accepting inbound tourism and industry. In order to further revitalize the shopping districts and small to medium sized businesses in the city, I also believe it is important to take on new challenges such as building a startup ecosystem and nighttime economy. -

PORTS of OSAKA PREFECTURE

Port and Harbor Bureau, Osaka Prefectural Government PORTS of OSAKA PREFECTURE Department of General Affairs / Department of Project Management 6-1 Nagisa-cho, Izumiotsu City 595-0055 (Sakai-Semboku Port Service Center Bldg. 10F) TEL: 0725-21-1411 FAX: 0725-21-7259 Department of Planning 3-2-12 Otemae, Chuo-ku, Osaka 540-8570(Annex 7th floor) TEL: 06-6941-0351 (Osaka Prefectural Government) FAX: 06-6941-0609 Produced in cooperation with: Osaka Prefecture Port and Harbor Association, Sakai-Semboku Port Promotion Council, Hannan Port Promotion Council Osaka Prefectural Port Promotion Website: http://www.osakaprefports.jp/english/ Port of Sakai-Semboku Japan’s Gateway to the World. With the tremendous potential and vitality that befit the truly international city of Osaka, Port of Hannan Seeking to become a new hub for the international exchange of people, From the World to Osaka, from Osaka to the Future goods and information. Starting from The sea is our gateway to the world – The sea teaches us that we are part of the world. Port of Nishiki Port of Izumisano Osaka Bay – Japan’s marine gateway to the world – is now undergoing numerous leading projects that Osaka Bay, will contribute to the future development of Japan, including Kansai International Airport Expansion and the Phoenix Project. Exchange for Eight prefectural ports of various sizes, including the Port of Sakai-Semboku (specially designated Port of Ozaki Port of Tannowa major port) and the Port of Hannan (major port), are located along the 70 kilometers of coastline the 21st Century extending from the Yamato River in the north to the Osaka-Wakayama prefectural border in the south. -

Shibuya City 渋

渋谷区 Shibuya City Chapter 1 1Shibuya City Urban Characteristics Shibuya City Urban Characteristics and Roles The Present In consideration of plans for the industry and tourism sectors to make Shibuya City a mature, international city, it is important to first identify its current urban characteristics. With this in mind, the Japan Power Cities index (Mori Memorial Foundation) was used for analysis. Japan Power Cities analyzes the main cities 1 of Japan including the 23 wards of Tokyo in the six functions of city power The Present of Shibuya City (Economy & Business, Research and Development, Cultural Interaction, Daily Life & Livability, Environment, and Accessibility) and 83 indicators identifying the Industry and Tourism strengths and weaknesses of cities. In the total score for the 23 wards of Tokyo, the survey ranks Shibuya City in fifth place overall, fourth place in the functions of Economy & Business, Cultural Interaction, and Accessibility, and fifth place in Daily Life & Livability, whereas it ranks low in ninth place for Research & Development (see figure at top and table at bottom of p. 9). Furthermore, when narrowing down the viewpoints for industry and tourism and looking at the deviation scores in each indicator group, groups such as Business Vitality, Business Environment, and Financial Affairs in Economy & Business are ranked highly as shown in the figure on the top of page ten. Even among these areas, indicators such as Ratio of New Businesses and Density of Flexible Workplaces are strong (see table on bottom of p. 10). Also, as shown in the figure in the middle of page ten, in Cultural Interaction, groups such as Volume of Interaction, Volume of Communication, and Intangible Resources are strengths. -

Section 5 Initiatives to Promote National Resilience (PDF:906.2KB)

“Creating regional disaster management capabilities”: TOHATSU Co., Ltd. TOHATSU develop and manufacture portable fire pumps that are “small, lightweight and compact.” They are also used by Japanese fire brigades. The portable fire pump enables quick fire-extinguishing activities at a fire site at the end of a path inaccessible to fire engines and helps improve the disaster risk reduction capabilities of the region. Raindrops or snowflakes Weather radars are used to observe globally via the use of a The larger the droplet or snowflake, the rotating antenna stronger the emitted radio wave. The frequency changes depending on the movement of the droplets or snowflakes. Weather radar “Easy-to-assemble safe and secure toilet booth of storage type for disasters”: Kawahara Technical Research Co., Ltd. Kawahara Technical Research have developed a public private toilet booth that is mostly made of paper and can be easily assembled. Biological agents placed in a septic tank reduce the risk of infectious diseases. The public private toilet booth is lightweight and able to assemble easily, even by two women, without using tools. Section 5: Initiatives to Promote National Resilience 5-1 Decision of the National Resilience Annual Plan for 2019 The government reviewed the National Resilience Basic Plan (Decided at the cabinet meeting on December 14, 2018) and decided the first Annual Plan, “National Resilience Annual Plan for 2019” (hereinafter referred to as “Annual Plan 2019”) on June 11, 2019. The Annual Plan 2019 includes the following national resilience efforts to be implemented in FY2019: Major measures, such as embankment maintenance and improvement of earthquake resistance of houses, disaster 100 prevention and mitigation measures for small- and medium-sized enterprises, new support measures to eliminate utility poles, enhancing key performance indicators and introducing benchmark indicators to appropriately determine progress, etc. -

July 27, 2005 for Immediate Release New City Residence Investment

July 27, 2005 For Immediate Release New City Residence Investment Corporation 1-10-6 Roppongi, Minato-ku, Tokyo Tetsuya Fujita, Executive Officer (Securities Code: 8965) Inquiries: CBRE Residential Management K.K. Yoetsu Takizawa, General Manager Planning & Administration TEL: +81-3-6229-3860 Notice Concerning the Proposed Acquisition of Investment Asset New City Residence Investment Corporation (“NCRI” or “the Investment Corporation”) today announced its plan to acquire the following investment asset. 1. Acquisition Details (1) Trust Beneficiary Interest in Real Estate Property Trust Asset (Millions of yen) Projected Acquisition Price Property Name (Note 1) 1 New City Residence Shinjyuku Gyoen I 3,140 2 New City Residence Sasazuka 3,050 3 New City Residence Takanawadai 1,180 4 New City Residence Nihonbashi Ningyocho IV 842 5 New City Residence Shinjyuku Gyoen II 580 6 New City Residence Ginza East IV 510 7 New City Residence Jiyugaoka 1,470 8 New City Residence Mejiro East 1,080 9 New City Residence Iriya 675 10 Park Terrace Ichikawa 620 11 Park Terrace Shioyaki 310 12 Park Terrace Horie 193 Total 13,650 Notes: 1. The projected acquisition price is exclusive of property tax, urban planning tax, consumption tax, and local consumption tax. Figures less than million yen are rounded. 2. The current names of properties 1 through 9 identified in the table above are Duo Scala Shinjuku Gyoen, Duo Scala Sasazuka II, Duo Scala Takanawadai, Dynafort Nihonbashi II, Park Terrace Shinjuku, Duo Scala Irifune, Duo Scala Jiyugaoka, Land Stage Mejiro, and Iriya Amflat III, respectively. The Investment Corporation intends to change the names of each building to those identified in the above table shortly after acquisition. -

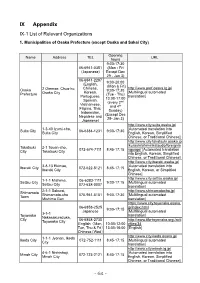

IX Appendix IX-1 List of Relevant Organizations

IX Appendix IX-1 List of Relevant Organizations 1. Municipalities of Osaka Prefecture (except Osaka and Sakai City) Opening Name Address TEL URL hours 9:00-17:30 06-6941-0351 (Mon - Fri (Japanese) Except Dec 29 - Jan 3) 06-6941-2297 9:00-20:00 (English, (Mon & Fri) Chinese, http://www.pref.osaka.lg.jp/ Osaka 2 Otemae, Chuo-ku, 9:00-17:30 Korean, [Multilingual automated Prefecture Osaka City (Tue - Thu) Portuguese, translation] 13:00-17:00 Spanish, (every 2nd Vietnamese, and 4th Filipino, Thai, Sunday) Indonesian, (Except Dec Nepalese and 29- Jan 3) Japanese) http://www.city.suita.osaka.jp/ 1-3-40 Izumi-cho, [Automated translation into Suita City 06-6384-1231 9:00-17:30 Suita City English, Korean, Simplified Chinese, or Traditional Chinese] http://www.city.takatsuki.osaka.jp /kurashi/shiminkatsudo/foreignla Takatsuki 2-1 Touen-cho, 072-674-7111 8:45-17:15 nguage/ [Automated translation City Takatsuki City into English, Korean, Simplified Chinese, or Traditional Chinese] http://www.city.ibaraki.osaka.jp/ 3-8-13 Ekimae, [Automated translation into Ibaraki City 072-622-8121 8:45-17:15 Ibaraki City English, Korean, or Simplified Chinese] http://www.city.settsu.osaka.jp/ 1-1-1 Mishima, 06-6383-1111 Settsu City 9:00-17:15 [Multilingual automated Settsu City 072-638-0007 translation] 2-1-1 Sakurai, http://www.shimamotocho.jp/ Shimamoto Shimamoto-cho 075-961-5151 9:00-17:30 [Multilingual automated Town Mishima Gun translation] https://www.city.toyonaka.osaka. 06-6858-2525 jp/index.html 9:00-17:15 Japanese [Multilingual automated 3-1-1 Toyonaka -

Title a Study on the Pollen Stratigraphy of the Osaka Group

A Study on the Pollen Stratigraphy of the Osaka Group, Title Pliocene-Pleistocene Deposits in the Osaka Basin Author(s) Tai, Akiko Memoirs of the Faculty of Science, Kyoto University. Series of Citation geology and mineralogy (1973), 39(2): 123-165 Issue Date 1973-02-28 URL http://hdl.handle.net/2433/186585 Right Type Departmental Bulletin Paper Textversion publisher Kyoto University MpMolRs oF THE FAauLTy oF ScmNcE, KyoTo UrglvERsl ry, SERIEs oF GEoL. & MINERAL., Vol. XXXIX, No. 2, pp. 12•3-1as, Feb. 28, 1973 A Study on the Pollen Stratigraphy of the AOsaka Group, Pliocene•Pleistocene Deposits inA the Osaka Basin By Akiko TAi' (Received Sept. 30, 1972) Abstract From the view point of the pollen stratigraphy, the Osaka group, the typical Pliocene-Pleistocene deposits distributed in the Kinki district, Central Japan, is divided into Metasequaia Zone below and Fagzas Zone above. Those divisions correspond with the stratigraphical units, that is, the Lower formation and the Upper formation of the Osaka group respectively. The former zone is character- ized by the decrease of the Tertiary type tree pollen and the increase of the coniferous tree pollen which are present in Japanese Islands, and further it is subdivided into A-D subzones ascendingly. The marine beds of the latter are characterized by the high percentage of Fagus pollen, and a spectmm obtained from tlie fresh water bed shows the po11en composition consisting of cool-temperate to cold climate. Basing upon the compositional oscillation of the pollen diagram in regard to lithofacies changes, Fagus zone is subdivided into E-H subzones.