Slides Presentation, Three Scenarios for a Second Automobile

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Future Mobility

FUTURE MOBILITY Sector report 29 October 2019 – 5:30 PM Automotive – Mobility - Infrastructures CASE: what will change for OEMs CASE (Connectivity, Autonomous, Sharing and Electric) will change the way consumers see mobility and will dramatically transform the industry. Quarterly results will be useful to assess short-term price reactions but, we believe, how every company is positioned in a fast- changing environment cannot be ignored for long-term returns. The industry transformation doesn’t necessarily mean “shrinking”: we believe that the overall size of the profit should rise. But a large amount of business centred on ownership models will be transacted in the future through mobility providers (i.e. services) and current incumbents may not be the winners. We initiate coverages on CNH (NEUTRAL, TP EUR10.3) that aims to be a disruptor in its sector thanks profiting from future mobility trends but it is witnessing an unpredictable AG cycle, Ferrari (BUY, TP EUR163.0) which will use the hybrid technology at its advantages and Piaggio (BUY, TP EUR3.20) where electric will support a new replacement cycle. > Regulators are forcing the transition to electric but pick-up will be slowed down by the lack of infrastructure: EU CO2 targets are forcing carmakers to introduce EVs despite they are still losing money on it and consumers are wobbling. However, slow deployment of charging infrastructure, lack in electricity storage and grids last mile capacity, constraints on battery production and recycling should limit PHEV and BEV to 16% of total registrations by 2025. We believe that electric is a perfect technology for 2 wheelers where “range anxiety” doesn’t apply Massimo Vecchio Senior Analyst and could trigger a long-awaited replacement cycle. -

List of Vehicle Owners Clubs

V765/1 List of Vehicle Owners Clubs N.B. The information contained in this booklet was correct at the time of going to print. The most up to date version is available on the internet website: www.gov.uk/vehicle-registration/old-vehicles 8/21 V765 scheme How to register your vehicle under its original registration number: a. Applications must be submitted on form V765 and signed by the keeper of the vehicle agreeing to the terms and conditions of the V765 scheme. A V55/5 should also be filled in and a recent photograph of the vehicle confirming it as a complete entity must be included. A FEE IS NOT APPLICABLE as the vehicle is being re-registered and is not applying for first registration. b. The application must have a V765 form signed, stamped and approved by the relevant vehicle owners/enthusiasts club (for their make/type), shown on the ‘List of Vehicle Owners Clubs’ (V765/1). The club may charge a fee to process the application. c. Evidence MUST be presented with the application to link the registration number to the vehicle. Acceptable forms of evidence include:- • The original old style logbook (RF60/VE60). • Archive/Library records displaying the registration number and the chassis number authorised by the archivist clearly defining where the material was taken from. • Other pre 1983 documentary evidence linking the chassis and the registration number to the vehicle. If successful, this registration number will be allocated on a non-transferable basis. How to tax the vehicle If your application is successful, on receipt of your V5C you should apply to tax at the Post Office® in the usual way. -

1230019 Ritchie Bros

Unreserved Public Auction Caorso, IT Timed auction only, see notice >> Tel: .. Fax: .. Auction location: Via Canada snc Angolo SP R, Caorso (PC), Italy facebook.com/ritchiebrositalia KOMATSU PCNLC VOLVO AG UNUSED MANITOU MRT S PRIVILEGE+ FENDT VARIO PROFI IVECO STRALIS X W/ EFFER /S KG . M rbauction.com/caorso © Copyright Ritchie Bros. Auctioneers – CAT K DOOSAN DL KOMATSU WA NEW HOLLAND WB HITACHI ZW CAT C DYNAPAC CAD BOMAG BWDH HAMM HT More items added daily! View the latest listings for this auction at rbauction.com/caorso HITACHI ZX LCN- NEW HOLLAND EC KOMATSU PCNHD KOMATSU PCNLC / HITACHI ZXLCN JCB JSN CAT D LCR JCB JSW KOMATSU PWESK More items added daily! View the latest listings for this auction at rbauction.com/caorso VOLVO ECR D KUBOTA KX KUBOTA KX HITACHI ZX USBLC CASE CXB S KOMATSU PCMR QTY OF UNUSED HITACHI ZXU YR SUNWARD SWTL CAT B More items added daily! View the latest listings for this auction at rbauction.com/caorso UNUSED — MANITOU MRT Easy S DIECI PEGASUS . DIECI PEGASUS . / & MERLO ROTO . MANITOU MTL MANITOU MVT MERLO P. / MERLO P . DIECI APOLLO . More items added daily! View the latest listings for this auction at rbauction.com/caorso / HAULOTTE HAPX / HAULOTTE HAPX / HAULOTTE HTPX JLG SJP JLG AJP / JLG SJ JLG SJ / HAULOTTE HAPX / HAULOTTE HA SPX More items added daily! View the latest listings for this auction at rbauction.com/caorso CLAAS DOMINATOR SL NEW HOLLAND T. JOHN DEERE PREMIUM UNUSED SAME EXPLORER UNUSED SAME EXPLORER UNUSED SAME -

Federico Vidari Resume

FEDERICO VIDARI I use my dierent professional and personal experiences to achieve business goals. Together with a passion for work and continuous change, I practice a holistic approach to generate innovation inside and outside companies. > https://www.linkedin.com/in/federicovidari SUMMARY MY LIFE PHILOSOPHY I have been working in marketing, in particular, digital communication, since 1995. Life is what happens while you're My education Architecture Degree, Politecnico di Milano; busy making your excuses. Erasmus at TUBerlin) has provided me with a highly Simple Plan methodological, results-oriented and client-centred approach to digital design and development, from conception and planning to execution, through iterative revisions. MOST PROUD OF My experience has been consolidated through a wide range of different marketing projects. I am a skilled interlocutor with clients from all backgrounds, and a team leader able to World Citizen generate a high level of engagement in all stakeholders: Lived in Berlin and Aachen DE clients, team and suppliers. Worked in Rio de Janeiro, Berlin, Aachen, Modena, Imola. I am an expert about Business Design and Transformation, Branding, Communication and Digital Strategy, UX/UI Design, Ecommerce, Email Marketing, Social Media Marketing, Social Maserati & Ferrari websites Selling, Sales enablement and digital coaching. Delivered in a complex stakeholders I am Adjunct Professor of Communication MetaDesign and environment Service Design at Politecnico di Milano. % Next Level Fest Organized a Music Festival -

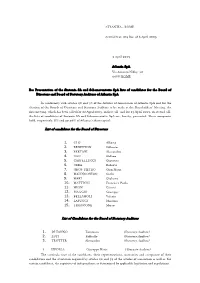

Presentation of the Sintonia SA and Schemaventotto Spa Lists of Candidates for the Board of Directors and Board of Statutory Auditors of Atlantia Spa

ATLANTIA - ROME Arrival Prot. 015 Res. of 6 April 2009 2 April 2009 Atlantia SpA Via Antonio Nibby, 20 00161 ROME Re: Presentation of the Sintonia SA and Schemaventotto SpA lists of candidates for the Board of Directors and Board of Statutory Auditors of Atlantia SpA In conformity with articles 20 and 30 of the Articles of Association of Atlantia SpA and for the election of the Boards of Directors and Statutory Auditors to be made at the Shareholders’ Meeting, the first meeting, which has been called for 22 April 2009, in first call, and for 23 April 2009, in second call, the lists of candidates of Sintonia SA and Schemaventotto SpA are, hereby, presented. These companies hold, respectively, 8% and 30.06% of Atlantia’s share capital; List of candidates for the Board of Directors 1. CLO’ Alberto 2. BENETTON Gilberto 3. BERTANI Alessandro 4. CAO Stefano 5. CASTELLUCCI Giovanni 6. CERA Roberto 7. GROS-PIETRO Gian Maria 8. MALINCONICO Carlo 9. MARI Giuliano 10. MATTIOLI Francesco Paolo 11. MION Gianni 12. PIAGGIO Giuseppe 13. BELLAMOLI Valerio 14. LAPUCCI Massimo 15. TRONCONE Marco List of Candidates for the Board of Statutory Auditors 1. DI TANNO Tommaso (Statutory Auditor) 2. LUPI Raffaello (Statutory Auditor) 3. TROTTER Alessandro (Statutory Auditor) 1. CIPOLLA Giuseppe Maria (Alternate Auditor) The curricula vitae of the candidates, their representations, warranties and acceptance of their candidature and the attestation required by articles 20 and 32 of the articles of association as well as, for certain candidates, the requisites of independence as determined by applicable legislation and regulations. -

Table of Contents

A periodic pubblication from the Italian Trade Volume 12 Issue1 .it italian trade 1 Table of contents 22. CREDITS EDITORIALS 24. “Italy and Miami: a long lasting bond of friendship”: a message from Tomas Regalado, Mayor of the City of Miami 26. “The US Southeast, a thriving market for Italian companies”: a message from Gloria Bellelli, Consul General of Italy in Miami 28. “The United States of America, a strategic market for Italian food industry”: a message from Gian Domenico Auricchio, President of Assocamerestero 30. “25 years supporting Italy and its businesses”: a message from Gianluca Fontani, President of Italy-America Chamber of Commerce Southeast SPECIAL EDITORIAL CONTRIBUTIONS 32. “Andrea Bocelli, when simplicity makes you the greatest”, interview with Andrea Bocelli, Italian classical crossover tenor, recording artist, and singer-songwriter. 40. “Santo Versace, Style is the Man!”, interview with Santo Versace, President of Gianni Versace Spa 47. “Italians in Miami: a unique-of-its-kind community”, by Antonietta Di Pietro Italian Instructor in the Department of Modern Languages at Florida International University 53. “Italy and the US: a strong relationship” by Andrea Mancia e Simone Bressan, Journalists and Bloggers THE “MADE IN ITALY AMBASSADOR AWARD” WINNERS 58. “Buccellati, a matter of generations”, interview with Andrea Buccellati, President and Creative Director of Buccellati Spa 63. “The Made in Italy essence” interview with Dario Snaidero, CEO of Snaidero USA INTRODUCING “THE BEST OF ITALY GALA NIGHT” 69. “The Best of Italy Gala Night” Program THE PROTAGONISTS OF “THE BEST OF ITALY GALA NIGHT” 76. “Alfa Romeo, Return of a legend”, by Alfa Romeo 82. -

Amac Aerospace and Pininfarina Present An

MAY 2019/PRESS RELEASE AMAC AEROSPACE AND PININFARINA PRESENT AN INNOVATIVE CABIN CONCEPT FOR THE AIRBUS A350-900 A new way to live and enjoy the on-board experience leveraging on the 360° Pininfarina design expertise and on AMAC Aerospace unique completion capabilities. Turin, May 20, 2019 – Imagine entering in a luxury hotel This concept is expressed in the cabin lounge by a unique lounge, enjoying a drink and then relaxing on comfortable open space sculptured by a flowing band that gives life couches surrounded by the green. Imagine having dinner to different environments. The welcoming area is furnished gazing at the sunset on the ocean and then watching a movie with a wet bar to receive guests. Following the band, the on a giant screen. Now open your eyes: you are on board traveler finds the relaxing area conceived as a cocoon on an Airbus A350-900. characterized by an intimate atmosphere: embracing sofas facing a transparent giant screen allowing either to project or AMAC Aerospace and Pininfarina present at EBACE an to enjoy the view. The lounge is completed by a dining area innovative cabin concept for the Airbus A350-900 aimed conceived both to eat and to hold meetings and a chaise- to innovate the onboard experience. The inspiration came long green space dedicated to personal relaxing moments. from the eclectic Pininfarina design expertise ranging for the nautical to the architectural interior design with the AMAC Aerospace competencies lie in bespoke conceiving, goal to create a comfortable and enjoyable space able to production and installation of the most discerning cabins make you forget to be on a jet. -

Electric Vehicle Infrastructure for the Monterey Bay Area the Associa� on of Monterey Bay Area Governments August 2013

E V Electric Vehicle Infrastructure for the Monterey Bay Area The Associa on of Monterey Bay Area Governments August 2013 The prepara on of this document was funded by a grant awarded by the Monterey Bay Unifi ed Air Pollu on Control District (MUAPCD), as part of the AB2766 program. Project Staff Alan Romero, Monterey Bay Unifi ed Air Pollu on Control District (MBUAPCD) AMBAG Dawn Mathes, Monterey County Resource Management Agency (RMA) Paul Hierling, Planner Carl P. Holm, Monterey County RMA Cody Meyer, Planner Craig Spencer, Monterey County RMA Anais Schenk, Planner Mario Salazar, Monterey County RMA Jason Adelaars, GIS Michael Ricker, City of Salinas Ecology Ac on Veronica Lezama, San Benito Council of Piet Canin, Vice President, Transporta on Governments Group Tegan Speiser, Santa Cruz County RTC Emily Glanville, Program Specialist Michael Zeller, TAMC Monterey Bay Unifi ed Air James Wasserman, Zero Motorcycles, Plug- Pollu on Control District In America Alan Romero, Air Quality Planner III Megan Tolbert, CSU Monterey Bay EV Communi es Alliance Piet Canin, Ecology Ac on Richard Corcoran, PEV Owner Richard Schorske, CEO Teresa Buika, UC Santa Cruz Previous staff contributors Richard Schorske, EV Communi es Alliance John Doughty Randy Deshazo, Principal Planner Linda Meckel, Planner, Project Manager MBEVA Plug-In Electric Vehicle Coordina ng Council Sharon Sarris, Green Fuse Energy Kris Markey, Offi ce of Monterey County Supervisor Parker Andy Hartmann, Interna onal Brotherhood of Electrical Workers Cheryl Schmi , City of Santa Cruz For more informa on regarding this study, contact Anais Schenk at [email protected] 2 E V Electric Vehicle Infrastructure for the Monterey Bay Area Execu ve Summary.............................................................................................................................................. -

Italian Morning Sight

Italian Morning Sight 07 September 2015 Equity Research +39 02 4344 - 4389 Institutional Sales - 5101 Relative Value - 4788 Equity Derivatives - 5451 Investment Research Stock Exchanges 4 Sep 15 Last %Chg %YtD Min YtD Max YtD Technical Analysis FTSE Italy All-Share 23,072 -2.97 14.57 19,270 25,684 DJ STOXX: Daily relative performance by sector FTSE MIB 21,473 -3.18 12.94 18,123 24,031 FTSE Italy Star 23,771 -1.06 27.39 18,482 26,520 Comit 1,200.4 -1.56 15.62 1,002.9 1,323.7 Stoxx 600 353.11 -2.52 3.09 331.62 414.06 EuroStoxx 50 3,180.2 -2.75 1.08 3,007.9 3,828.8 Dow Jones Industrials 16,102 -1.66 -9.65 15,666 18,312 Nasdaq Comp 4,684 -1.05 -1.10 4,506 5,219 Nikkei 225 17,792 -2.15 1.96 16,796 20,868 Other Market Indicators 4 Sep 15 Last %Chg %YtD Min YtD Max YtD EUR/USD 1.1116 0.17 -8.14 1.0522 1.2031 USD/YEN 119.19 -0.91 -0.59 116.87 125.65 London Brent Crude Oil Index U$/BBL 50.37 2.54 -12.14 42.81 67.95 10 Yrs Bund Futures 154.89 0.58 -0.63 148.98 160.36 Source: Datastream Recommendation and target price changes Banca Carige: TP EUR 2.20 from EUR 2.30 Trevi: TP EUR 1.50 from 1.90 News Banca Carige (Buy) A restructuring story with M&A appeal Enel (Accumulate) Going-on Fiat Chrysler Automobiles (Buy) FCA likely to wait until 2016 before moving on GM Telecom Italia (Accumulate) New rumours on savings' conversion Trevi (Neutral) Feedback from H1 presentation: challenging guidance UniCredit (Neutral) Interview with Mr Ghizzoni in La Repubblica All ESN research is available on Bloomberg: “ESNR” <go> Italian Morning Sight 07 September 2015 Banca Carige Italy/Banks BANKS Banca Carige (Buy) A restructuring story with M&A appeal Buy A restructuring story with M&A appeal Recommendation unchanged Share price: EUR 1.63 The facts: We are publishing this morning a company update on Banca Carige. -

2018 Annual Report

2018 ANNUAL REPORT 2018 ANNUAL REPORT AND FORM 20-F 2 2018 | ANNUAL REPORT 2018 | ANNUAL REPORT 3 Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes No Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes No Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer,” and emerging growth company” in Rule 12b-2 of the Exchange Act. Large accelerated filer Accelerated filer Non-accelerated filer Emerging growth company If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing: U.S. -

Piaggio Mp3 Range the Piaggio Mp3 Range Grows and Is Completed Stability and Ease of Riding Combined with Agility, Brilliant

PIAGGIO MP3 RANGE THE PIAGGIO MP3 RANGE GROWS AND IS COMPLETED STABILITY AND EASE OF RIDING COMBINED WITH AGILITY, BRILLIANT PERFORMANCE AND REDUCED CONSUMPTION. TOP SHELF SAFETY AND COMFORT AS ALWAYS FOR THE THREE- WHEELED PATRIARCH OF THE CATEGORY AND BEST SELLER FOR MORE THAN 10 YEARS YOURBAN ALSO UPDATED TO COMPLY WITH EURO 4 EMISSIONS STANDARDS, THE MOST COMPACT AND CITY PIAGGIO MP3 MODEL Piaggio MP3 is the world's first 3-wheel scooter, the concrete response to the demand for easy-to-handle, extremely safe city vehicles to get about in the city or reach the city centre from the ever growing suburbs. The two front wheels and the exclusive patented suspension system, conceived and developed by Piaggio before any other global manufacturer, combine the safety of a car with the simplicity and practicality of a scooter and the fun of a motorcycle with dynamic riding on corners. This is why Piaggio MP3 is able to satisfy a truly global demand: from drivers looking for a more practical yet safe alternative to the experienced motorcyclist able to appreciate the advantages and technical features of a vehicle that has, on its own, created a new market segment of which it is the undisputed leader. “Two wheels ahead of the rest”: a definition which not only indicates the peculiar characteristic of Piaggio MP3, but also suggests technological superiority that the revolutionary Piaggio Group “three wheeler” has managed to affirm. Two front wheels to travel in total safety in any weather or road surface conditions and at the same time have fun riding just as on a conventional two-wheeled vehicle. -

KWD Webranking Italy 2013 EN

IN COLLABORATION WITH lundquist. KWD WEBRANKING 2013 ITALY THE RESEARCH IN NUMBERS KWD Webranking is the most in-depth analysis of online nancial and corporate communications in Europe th th 17 EUROPEAN EDITION AND 12 ITALIAN EDITION THE “BLACK SHEEP” 40 ITALIAN COMPANIES EXCLUDED Spotlight on best practice and companies investing in their LESS THAN 25 POINTS IN THE 2012 RANKING online communications THE BEST IN 2013 TOP 10 IN 2013 BEST IMPROVERS ITALIAN AVERAGE 11 88.8 Eni +9.9 Mondadori 22 86.1 Telecom Italia 42.2 POINTS OUT OF 100 +9.3 Campari 33 80.5 Hera -2 POINTS 73.5 Snam 44 VS 2012 +5.5 Prysmian 55 71.3 Pirelli & C. 66 68.5 Terna +5.3 Eni 66.8 UniCredit 77 ONLY +4.1 Igd 88 63.5 Generali 1 COMPANY OUT OF 3 99 63.3 Mondadori IMPROVED 1010 62 Piaggio & C. ITS SCORE NEW WEBSITES BREMBO FIAT SPA CAMPARI LUXOTTICA CNH INDUSTRIAL PIAGGIO & C. FINMECCANICA ST MICROELECTRONICS ITALIAN COMPANIES DOING WELL IN DISCLOSURE Italian companies are doing well in the presentation of the “ company, nancial results and governance, information“ usually found inside nancial reports. Sustainability, employer branding and social media are the weakest areas. Joakim Lundquist, Head of KWD in Italy POSITIVE NEGATIVE PRESENTATION OF THE COMPANY SUSTAINABILITY 98% Present their history 25% Do not present sustainability information other than the code of ethics PRESENTATION OF FINANCIAL RESULTS EMPLOYER BRANDING 100% Have reports, documents 21% Do not present the company and presentations in English to potential candidates GOVERNANCE SOCIAL MEDIA 95% Include information 55% Do not include any social media concerning their AGM accounts on their website TECHNOLOGY VSVS STORIES INNOVATIONS TO BE TOLD Italian companies rely on technology to close the gap with “ “ European companies but corporate website is not used effectively to communicate identity and future vision.