International Finance for Coal-Fired Power Plants

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Underreported Coal in Statistics a Survey-Based Solid Fuel

Applied Energy 235 (2019) 1169–1182 Contents lists available at ScienceDirect Applied Energy journal homepage: www.elsevier.com/locate/apenergy Underreported coal in statistics: A survey-based solid fuel consumption and T emission inventory for the rural residential sector in China ⁎ Liqun Penga,b,1, Qiang Zhanga, , Zhiliang Yaoc, Denise L. Mauzeralld,e, Sicong Kangb,f, Zhenyu Dug, Yixuan Zhenga, Tao Xuea, Kebin Heb a Ministry of Education Key Laboratory for Earth System Modeling, Department of Earth System Science, Tsinghua University, Beijing 100084, China b State Key Joint Laboratory of Environment Simulation and Pollution Control, School of Environment, Tsinghua University, Beijing 100084, China c School of Food and Chemical Engineering, Beijing Technology and Business University, Beijing 100048, China d Woodrow Wilson School of Public and International Affairs, Princeton University, Princeton, NJ 08544, USA e Department of Civil and Environmental Engineering, Princeton University, Princeton, NJ 08544, USA f Beijing Make Environment Co. Ltd., Beijing 100083, China g National Research Center for Environmental Analysis and Measurements, Beijing 100026, China HIGHLIGHTS • Solid fuel consumption rises with the increase in Heating Degree Days. • A transition from biofuel to coal occurs with per capita income growth. • Estimated coal consumption is 62% higher than that reported in official statistics. • An improved emission inventory of the residential sector is built in China. • Our work provides a new approach of obtaining data for other developing countries. ARTICLE INFO ABSTRACT Keywords: Solid fuel consumption and associated emissions from residential use are highly uncertain due to a lack of Rural residential reliable statistics. In this study, we estimate solid fuel consumption and emissions from the rural residential Survey sector in China by using data collected from a new nationwide field survey. -

Energy in China: Coping with Increasing Demand

FOI-R--1435--SE November 2004 FOI ISSN 1650-1942 SWEDISH DEFENCE RESEARCH AGENCY User report Kristina Sandklef Energy in China: Coping with increasing demand Defence Analysis SE-172 90 Stockholm FOI-R--1435--SE November 2004 ISSN 1650-1942 User report Kristina Sandklef Energy in China: Coping with increasing demand Defence Analysis SE-172 90 Stockholm SWEDISH DEFENCE RESEARCH AGENCY FOI-R--1435--SE Defence Analysis November 2004 SE-172 90 Stockholm ISSN 1650-1942 User report Kristina Sandklef Energy in China: Coping with increasing demand Issuing organization Report number, ISRN Report type FOI – Swedish Defence Research Agency FOI-R--1435--SE User report Defence Analysis Research area code SE-172 90 Stockholm 1. Security, safety and vulnerability Month year Project no. November 2004 A 1104 Sub area code 11 Policy Support to the Government (Defence) Sub area code 2 Author/s (editor/s) Project manager Kristina Sandklef Ingolf Kiesow Approved by Maria Hedvall Sponsoring agency Department of Defense Scientifically and technically responsible Report title Energy in China: Coping with increasing demand Abstract (not more than 200 words) Sustaining the increasing energy consumption is crucial to future economic growth in China. This report focuses on the current and future situation of energy production and consumption in China and how China is coping with its increasing domestic energy demand. Today, coal is the most important energy resource, followed by oil and hydropower. Most energy resources are located in the inland, whereas the main demand for energy is in the coastal areas, which makes transportation and transmission of energy vital. The industrial sector is the main driver of the energy consumption in China, but the transport sector and the residential sector will increase their share of consumption by 2020. -

India: Inventory of Estimated Budgetary Support and Tax Expenditures for Fossil-Fuels

INDIA: INVENTORY OF ESTIMATED BUDGETARY SUPPORT AND TAX EXPENDITURES FOR FOSSIL-FUELS Energy resources and market structure India is one of the fastest growing energy markets in the world. The country is the world’s third largest coal producer owing to its large deposits. Coal is the leading primary fuel in India’s energy mix, accounting for 44% of the country’s total primary energy supply (TPES), with thermal power plants making up the majority of coal consumption. Biomass accounts for 25% of total energy use, followed by oil and natural gas, which account respectively for 22% and 7% of the country’s energy needs. Remaining energy sources, such as nuclear power and hydro-electricity, account for about 1% each. The country’s proven reserves of oil were 5.5 billion barrels as of December 2012; nonetheless, domestic production falls far short of domestic demand and the country depends heavily on imported crude oil. The state-owned coal company, Coal India Limited (CIL), retains a near monopoly of coal extraction, with over 90% of domestic coal extraction attributed to government-controlled mines. Most coal mining occurs in the states of Bihar, Chhattisgarh, Jharkhand, Madhya Pradesh, Orissa, and West Bengal. Market reforms are being implemented to bring competition and transparency to the coal sector. The government has been grappling to get an effective regulatory framework in place, which includes the loosening of regulations for the coal industry, with the objective of moving some grades of coal closer to international market prices, and allocating additional coal blocks through a transparent open bidding process. -

5Hjxodwru\ 5Hirup Lq +Xqjdu\

5HJXODWRU\ 5HIRUP LQ +XQJDU\ 5HJXODWRU\ 5HIRUP LQ WKH (OHFWULFLW\ 6HFWRU ORGANISATION FOR ECONOMIC CO-OPERATION AND DEVELOPMENT Pursuant to Article 1 of the Convention signed in Paris on 14th December 1960, and which came into force on 30th September 1961, the Organisation for Economic Co-operation and Development (OECD) shall promote policies designed: to achieve the highest sustainable economic growth and employment and a rising standard of living in Member countries, while maintaining financial stability, and thus to contribute to the development of the world economy; to contribute to sound economic expansion in Member as well as non-member countries in the process of economic development; and to contribute to the expansion of world trade on a multilateral, non-discriminatory basis in accordance with international obligations. The original Member countries of the OECD are Austria, Belgium, Canada, Denmark, France, Germany, Greece, Iceland, Ireland, Italy, Luxembourg, the Netherlands, Norway, Portugal, Spain, Sweden, Switzerland, Turkey, the United Kingdom and the United States. The following countries became Members subsequently through accession at the dates indicated hereafter: Japan (28th April 1964), Finland (28th January 1969), Australia (7th June 1971), New Zealand (29th May 1973), Mexico (18th May 1994), the Czech Republic (21st December 1995), Hungary (7th May 1996), Poland (22nd November 1996), Korea (12th December 1996) and the Slovak Republic (14th December 2000). The Commission of the European Communities takes part in the work of the OECD (Article 13 of the OECD Convention). Publié en français sous le titre : LA RÉFORME DE LA RÉGLEMENTATION DANS LE SECTEUR DE L'ÉLECTRICITÉ © OECD 2000. Permission to reproduce a portion of this work for non-commercial purposes or classroom use should be obtained through the Centre français d’exploitation du droit de copie (CFC), 20, rue des Grands-Augustins, 75006 Paris, France, tel. -

A New Geography of European Power?

A NEW GEOGRAPHY OF EUROPEAN POWER? EGMONT PAPER 42 A NEW GEOGRAPHY OF EUROPEAN POWER? James ROGERS January 2011 The Egmont Papers are published by Academia Press for Egmont – The Royal Institute for International Relations. Founded in 1947 by eminent Belgian political leaders, Egmont is an independent think-tank based in Brussels. Its interdisciplinary research is conducted in a spirit of total academic freedom. A platform of quality information, a forum for debate and analysis, a melting pot of ideas in the field of international politics, Egmont’s ambition – through its publications, seminars and recommendations – is to make a useful contribution to the decision- making process. *** President: Viscount Etienne DAVIGNON Director-General: Marc TRENTESEAU Series Editor: Prof. Dr. Sven BISCOP *** Egmont - The Royal Institute for International Relations Address Naamsestraat / Rue de Namur 69, 1000 Brussels, Belgium Phone 00-32-(0)2.223.41.14 Fax 00-32-(0)2.223.41.16 E-mail [email protected] Website: www.egmontinstitute.be © Academia Press Eekhout 2 9000 Gent Tel. 09/233 80 88 Fax 09/233 14 09 [email protected] www.academiapress.be J. Story-Scientia NV Wetenschappelijke Boekhandel Sint-Kwintensberg 87 B-9000 Gent Tel. 09/225 57 57 Fax 09/233 14 09 [email protected] www.story.be All authors write in a personal capacity. Lay-out: proxess.be ISBN 978 90 382 1714 7 D/2011/4804/19 U 1547 NUR1 754 All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise without the permission of the publishers. -

“Power Finance Corporation - Investors Interaction Meet”

“Power Finance Corporation - Investors Interaction Meet” May 31, 2018 MANAGEMENT: TEAM OF POWER FINANCE CORPORATION:- - Mr. Rajeev Sharma - Chairman and Managing Director - Mr. D. Ravi - Director (Commercial) - Mr. C. Gangopadhyay - Director (Project) - Shri Sitaram Pareek - Independent Director Page 1 of 23 Power Finance Corporation May 31, 2018 Speaker: Good Afternoon, Ladies and Gentlemen. On behalf of Power Finance Corporation, we feel honored and privileged to welcome you all to this Investors Interaction Meet. The company recently announced its financial results for the year 2017-18 and has been successful in maintaining its growth trajectory. PFC is always aiming to connect with its investor and build a strong and enduring positive relationship with the investment community. With this objective, today’s event has been organized to discuss PFC’s current performance and future outlook with the current and prospective investors. On the desk in the center is Chairman and Managing Director -- Shri Rajeev Sharma along with the other directors. To my immediate left is Shri DRavi – Director, Commercial. Next to him is Shri C Gangopadhyay – Director, Projects. To my extreme left is Shri Sitaram Pareek – Independent Director and beside him is Shri N.B. Gupta – Director, Finance. They are all in front of you to give a brief insight of PFC’s performance during the financial year 2017-18. They will also present to you a roadmap for the forthcoming year. I request Shri Rajeev Sharma -- Chairman and Managing Director to address the gathering. Rajeev Sharma: Thank you very much for sparing your valuable time to be present here during this interaction. -

Detailed Advertisement for Recruitment of Company Secretary in E6, E7 and E8 Grades in Executive Cadre

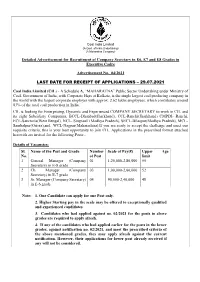

Coal India Limited (A Govt. of India Undertaking) (A Maharatna Company) Detailed Advertisement for Recruitment of Company Secretary in E6, E7 and E8 Grades in Executive Cadre Advertisement No. 04/2021 LAST DATE FOR RECEIPT OF APPLICATIONS – 29.07.2021 Coal India Limited (CIL) - A Schedule A, “MAHARATNA” Public Sector Undertaking under Ministry of Coal, Government of India, with Corporate Hqrs at Kolkata, is the single largest coal producing company in the world with the largest corporate employer with approx. 2.62 lakhs employees, which contributes around 83% of the total coal production in India. CIL is looking for Enterprising, Dynamic and Experienced COMPANY SECRETARY to work in CIL and its eight Subsidiary Companies, BCCL-Dhanbad(Jharkhand), CCL-Ranchi(Jharkhand) CMPDI- Ranchi, ECL-Sanctoria(West Bengal), NCL- Singrauli (Madhya Pradesh), SECL-Bilaspur(Madhya Pradesh), MCL- Sambalpur(Orissa),and WCL-Nagpur(Maharashtra).If you are ready to accept the challenge and meet our requisite criteria, this is your best opportunity to join CIL. Applications in the prescribed format attached herewith are invited for the following Posts:- Details of Vacancies: Sl. Name of the Post and Grade Number Scale of Pay(₹) Upper Age No. of Post limit 1 General Manager (Company 01 1,20,000-2,80,000 55 Secretary) in E-8 grade 2 Ch. Manager (Company 03 1,00,000-2,60,000 52 Secretary) in E-7 grade 3 Sr. Manager (Company Secretary) 04 90,000-2,40,000 48 in E-6 grade Note- 1. One Candidate can apply for one Post only. 2. Higher Starting pay in the scale may be offered to exceptionally qualified and experienced candidates. -

Ngo Documents 2013-08-14 00:00:00 Coal India Investor Brief High Risk

High risk, low return COAL INDIA LTD’s shareholder value is threatened by poor corporate governance, faulty reserve estimations, regulatory risk and macro-economic issues. Introduction Coal India Limited is the world’s largest coal miner, with a production of 435 million metric tons (MT) in 2011 -201 2. There is significant pressure on CIL to deliver annual production growth rates in excess of 7%. The company has a 201 7 production target of 61 5 MT.[1 ] Coal India’s track record raises questions over its ability to deliver this rate of growth. In addition, serious governance issues are likely to impact CIL’s financial performance. These pose a financial and reputational risk to CIL, its shareholders and lenders, while macro- economic issues in the Indian energy economy pose a long term threat to Coal India. • CIL’s attempts to access new mining areas are facing widespread opposition from local communities and environmental groups. With its reliance on open-pit mining, access to new mines are essential for CIL to achieve production targets. G • CIL has grown reliant on shallow, open pit mining for 90% of its production, and has lost in-house expertise on deep mining techniques. N I • CIL has a record of poor corporate governance, manifested in rampant corruption, poor worker safety and repeated legal violations. This has, in the last year alone, led to penalties and F closure notices for over 50 mines, threatening both its financial performance and reputation. E I • CIL’s financial performance has been affected by directives from majority shareholder Government of India to keep coal prices artifically low.[2] According to one estimate, this cost R CIL $1 .75 billion in the 201 2-1 3 financial year alone.[3] The government has also taken away coal blocks allocated to CIL and given them to private players.[4] B • Changing economics of coal power in India; renewable energies are becoming cost- competitive even as coal faces increased regulatory scrutiny and public opposition. -

A Review of the Three Waves of International Relations Small State Literature

Pacific Dynamics: Vol 5 (1) 2021 Journal of Interdisciplinary Research http://pacificdynamics.nz Creative Commons Attribution 4.0 ISSN: 2463-641X DOI : http://dx.doi.org/10.26021/10639 Breaking the paradigm(s): A review of the three waves of international relations small state literature Jeffrey Willis* Independent Researcher Abstract Mainstream international relations (IR) literature has long treated small states as marginal actors who exist on the periphery of global affairs. For many years, scholars have struggled to conclusively define the category of small statehood. Additionally, IR’s privileging of the theoretical paradigms of realism and neorealism when analyzing small state issues, has meant that, until recently, small states have been conceptualized as actors that struggle to make proactive foreign policy choices on their own terms. Despite this, small states, and particularly small island states in the Pacific region, appear to have many opportunities to engage in vibrant foreign policy endeavours in the present day. This article offers a review of small state IR literature, with a particular focus on small state foreign policy issues. It begins by reviewing the various approaches to defining small statehood, before turning to a review of how small state issues have been treated in broader IR. It posits that the small state IR literature can usefully be broken down into three distinct time periods— 1959–1979, 1979–1992, and 1992–present—and reviews the literature within that framework, drawing out the theoretical through lines -

G20 Subsidies to Oil, Gas and Coal Production

G20 subsidies to oil gas and coal production: India Vibhuti Garg and Ken Bossong Argentina Australia Brazil Canada China France Germany India Indonesia Italy Japan Korea (Republic of) Mexico Russia Saudi Arabia This country study is a background paper for the report Empty promises: G20 subsidies South Africa to oil, gas and coal production by Oil Change International (OCI) and the Overseas Turkey Development Institute (ODI). It builds on research completed for an earlier report The fossil United Kingdom fuel bailout: G20 subsidies to oil, gas and coal exploration, published in 2014. United States For the purposes of this country study, production subsidies for fossil fuels include: national subsidies, investment by state-owned enterprises, and public finance.A brief outline of the methodology can be found in this country summary. The full report provides a more detailed discussion of the methodology used for the country studies and sets out the technical and transparency issues linked to the identification of G20 subsidies to oil, gas and coal production. The authors welcome feedback on both this country study and the full report to improve the accuracy and transparency of information on G20 government support to fossil fuel production. A Data Sheet with data sources and further information for India’s production subsidies is available at: http://www.odi.org/publications/10073-g20-subsidies-oil-gas-coal-production-india priceofoil.org Country Study odi.org November 2015 Background remained substantial at $11 billion in 2014–15 (MoPNG, India has substantial fossil fuel reserves, including 61 2015b). Similar consumer subsidies of approximately billion tonnes of coal, 5.7 billion barrels of oil and 1.4 $12 billion in 2012–13 existed in the electricity sector. -

Lilliputian States in Digital Affairs and Cyber Security

Software Manufacturer Liability LIINA ARENG LILLIPUTIAN STATES IN DIGITAL AFFAIRS AND CYBER SECURITY Tallinn Paper No. 4. 2014 Previously in This Series No. 1 Kenneth Geers “Pandemonium: Nation States, National Security, and the Internet” (2014) No. 2 Liis Vihul “The Liability of Software Manufacturers for Defective Products” (2014) No. 3 Hannes Krause “NATO on Its Way Towards a Comfort Zone in Cyber Defence” (2014) Disclaimer This publication is a product of the NATO Cooperative Cyber Defence Centre of Excellence (the Centre). It does not necessarily reflect the policy or the opinion of the Centre or NATO. The Centre may not be held responsible for any loss or harm arising from the use of information contained in this publication and is not responsible for the content of the external sources, including external websites referenced in this publication. Digital or hard copies of this publication may be produced for internal use within NATO and for personal or educational use when for non-profit and non-commercial purpose, provided that copies bear a full citation. Please contact [email protected] with any further queries. Roles and Responsibilities in Cyberspace The theme of the 2014 Tallinn Papers is ‘Roles and Responsibilities in Cyberspace’. Strategic developments in cyber security have often been frustrated by role assignment, whether in a domestic or international setting. The difficulty extends well beyond the formal distribution of roles and responsibilities between organisations and agencies. Ascertaining appropriate roles and responsibilities is also a matter of creating an architecture that is responsive to the peculiar challenges of cyberspace and that best effectuates strategies that have been devised to address them. -

Normative Power Europe in a Changing World: a Discussion

Normative Power Europe in a Changing World: A Discussion André Gerrits (ed.) December 2009 NETHERLANDS INSTITUTE OF INTERNATIONAL RELATIONS CLINGENDAEL CIP-Data Koninklijke bibliotheek, The Hague Gerrits, André (ed.) Normative Power Europe in a Changing World: A Discussion / A. Gerrits (ed.), L. Aggestam, I. Manners, T. Romanova, A. Toje, Y. Wang – The Hague, Netherlands Institute of International Relations Clingendael. Clingendael European Papers No. 5 ISBN 978-90-5031-148-9 Desk top publishing by Cheryna Abdoel Wahid Netherlands Institute of International Relations Clingendael Clingendael European Studies Programme Clingendael 7 2597 VH The Hague Phone number +31(0)70 - 3245384 Telefax +31(0)70 - 3282002 P.O. Box 93080 2509 AB The Hague E-mail: [email protected] Website: http://www.clingendael.nl The Netherlands Institute of International Relations Clingendael is an independent institute for research, training and public information on international affairs. It publishes the results of its own research projects and the monthly ‘Internationale Spectator’ and offers a broad range of courses and conferences covering a wide variety of international issues. It also maintains a library and documentation centre. © Netherlands Institute of International Relations Clingendael. All rights reserved. No part of this book may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of the copyright holders. Clingendael