Unpublished Decision Memorandum

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Overview of Coal Mining Industry in India

GOVT. OF INDIA OVERVIEW OF COAL MINING INDUSTRY IN INDIA FUTURE PROSPECTS AND POSSIBILITIES PARTHA S. BHATTACHARYYA CHAIRMAN, COAL INDIA LIMITED 05-07Th. JUNE 2007 CONTENT SN TOPIC SLIDE No. 1 Background 1-6 2 Nationalisation of Coal Industry 7-11 3 Turn around of CIL 12-15 4 X Plan performance 16-19 5 Demand and production projections 20-25 6 THRUST AREAS 26 A New Strategy 27-38 B Beneficiation of Non-coking coal 39-41 C Clean coal technologies 42-45 D Coal Videsh 46 % SHARE OF COMMERCIAL PRIMARY ENERGY RESOURCES - INDIA NUCLEAR 2% HYDRO 2% NATURAL GAS 9% COAL 51% OIL 36% 1 A.CIL :COAL PRODUCING SUBSIDIARIES 1 8 EASTERN COALFIELDS LTD. (1) 5 4 3 BHARAT COKING COAL LTD. (2) CENTRAL COALFIELDS LTD. (3) NORTHERN COALFIELDS LTD. (4) WESTERN COALFIELDS LTD. (5) SOUTH EASTERN COALFIELDS LTD.(6) MAHANADI COALFIELDS LTD. (7) NORTH EASTERN COALFIELDS. (8) ( A UNIT UNDER CIL(HQ) ) 2 PLANNING & DESIGN INSTITUTE COAL 7 LIGNITE CENTRAL MINE PLANNING & DESIGN INSTITUTE (CMPDIL) 6 B.SINGARENI COLLIERIES CO. LTD. (9) 9 10 C.NEYVELI LIGNITE CORPORATION (10) 2 INDIAN COAL RESOURCES – 2007 (Bill T) 33.2 222 Coking Non-Coking TOTAL RESOURCE – 255.2 3 COAL RESERVES IN INDIA (As on 1.1.2007) (Billion T) TYPE OF COAL PROVED INDICATED INFERRED TOTAL Prime Coking 4.6 0.7 0.0 5.3 Medium Coking 11.8 11.6 1.9 25.3 Semi Coking 0.5 1.0 0.2 1.7 Non coking 80.6 105.6 35.8 222.0 TOTAL 97.9 119.0 38.3 255.2 Lignite 4.3 12.7 20.1 37.1 4 Proved resource is around 10% of world’s proved reserves CHARACTERISTICS OF INDIAN COAL DEPOSITS 1. -

India: Inventory of Estimated Budgetary Support and Tax Expenditures for Fossil-Fuels

INDIA: INVENTORY OF ESTIMATED BUDGETARY SUPPORT AND TAX EXPENDITURES FOR FOSSIL-FUELS Energy resources and market structure India is one of the fastest growing energy markets in the world. The country is the world’s third largest coal producer owing to its large deposits. Coal is the leading primary fuel in India’s energy mix, accounting for 44% of the country’s total primary energy supply (TPES), with thermal power plants making up the majority of coal consumption. Biomass accounts for 25% of total energy use, followed by oil and natural gas, which account respectively for 22% and 7% of the country’s energy needs. Remaining energy sources, such as nuclear power and hydro-electricity, account for about 1% each. The country’s proven reserves of oil were 5.5 billion barrels as of December 2012; nonetheless, domestic production falls far short of domestic demand and the country depends heavily on imported crude oil. The state-owned coal company, Coal India Limited (CIL), retains a near monopoly of coal extraction, with over 90% of domestic coal extraction attributed to government-controlled mines. Most coal mining occurs in the states of Bihar, Chhattisgarh, Jharkhand, Madhya Pradesh, Orissa, and West Bengal. Market reforms are being implemented to bring competition and transparency to the coal sector. The government has been grappling to get an effective regulatory framework in place, which includes the loosening of regulations for the coal industry, with the objective of moving some grades of coal closer to international market prices, and allocating additional coal blocks through a transparent open bidding process. -

Government of India Ministry of Micro, Small and Medium Enterprises

GOVERNMENT OF INDIA MINISTRY OF MICRO, SMALL AND MEDIUM ENTERPRISES LOK SABHA UNSTARRED QUESTION NO. 4232 TO BE ANSWERED ON 07.01.2019 PUBLIC PROCUREMENT POLICY 4232. SHRI ADHALRAO PATIL SHIVAJIRAO: SHRI SHRIRANG APPA BARNE: SHRI KUNWAR PUSHPENDRA SINGH CHANDEL: DR. SHRIKANT EKNATH SHINDE: SHRI ANANDRAO ADSUL: SHRI VINAYAK BHAURAO RAUT: Will the Minister of MICRO, SMALL AND MEDIUM ENTERPRISES be pleased to state: (a) the details of the total annual procurement of goods and services by each Public Sector Enterprise (PSE) in the year 2014-15, 2015-16, 2016-17 and 2017-18; (b) the quantity of calculated value of goods and services procured under Public Procurement Policy Order, 2012 during the said period in each PSE; (c) the status of procurement under this policy from MSMEs owned by SC/ST and non-SC/STs during the said period by each PSE; (d) whether the public procurement policy is not being complied with by many Government departments/PSEs; and (e) if so, the details thereof and the reasons therefor along with corrective steps taken/being taken by the Government in this regard? ANSWER MINISTER OF STATE (INDEPENDENT CHARGE) FOR MICRO, SMALL AND MEDIUM ENTERPRISES (SHRI GIRIRAJ SINGH) (a) to (e): The details of annual procurement of goods & services by the Central Public Sector Enterprise (CPSE) as per information provided by Department of Public Enterprises (DPE) are as under: Year No. of Total Procurement Procurement from MSEs CPSEs Procurement From MSEs owned by SC/ST (Rs. in Crore) (Rs. in Crore) Entrepreneur (Rs. in Crore) 2014-15 133 131766.86 15300.57 59.37 2015-16 132 279167.15 12566.15 50.11 2016-17 142 245785.31 25329.44 400.87 2017-18 169 280785.49 24226.51 442.52 Ministry of MSME has taken several measures for effective implementation of the Public Procurement Policy. -

Western Coalfields Limited

WESTERN COALFIELDS LIMITED (A SUBSIDIARY OF COAL INDIA LIMITED) STANDING ORDERS IN RESPECT OF W.C.L. NAGPUR Government of India (1) MINISTRY OF LABOUR Registered OFFICE OF THE CHIEF LABOUR COMMISSIONER (C) NEW DELHI No. IE. 5/6/91-IS, I Dated the 19th February, 1993 To 1. The Chairman-cum-Mg.Director 8. The General Secretary M/s Western Coalfields Ltd. Chhindwara Zila Koyla Khadan Coal Estate, Civil Lines Karmachari Sangh, P.O. Nagpur 440001 Parasia, Distt. Chhindwara (MP) 2. The General Secretary 9. The General Secretary Rashtriya Koyla Khadan mazdoor Sangh Koyla Khadan Karmachari Congress (INTUC), Adv. Bobde Building, AIR P.O. Pathakhera, Distt:Betul(MP) Square, Civil Lines, Nagpur-440 001 10. The General Secretary 3. The General Secretary MP Koyla Khadan Mazdoor Samyukta Khadan Mazdoor Sangh Panchayat Union, Western Coalfields (AITUC), Parwana Memorial 44, Koyla Shramik Fedn. (HMS) 116, Kingsway, Nagpur Sulbha Niwas, Sindi Khana Geneshpeth, Nagpur 4. The General Secretary Lal Zenda Coal Mines Mazdoor Union 11. The General Secretary (CITU), PO: Ganjipeth, Nagpur Wardha Valley Colliery Workers Union, Chadrapur,Western Coalfields 5. The General Secretary Shramik Fedn. (HMS) Sindi Khana, Western Coalfields Koyla Shramik GaneshPeth, Nagpur. Federation (HMS), 116, Sulbha Niwas, Sindi Khana, Ganeshpeth,Nagpur 12. The General Secretary Rashtriya Vidarbha Coal Employees 6. The General Secretary Union, mazdoor Karyalay Bharatiya Koyla Khadan mazdoor Jatpura Gate Chandrapur (MS) Sangh, (BMS), at and PO Parasia Vishwakarma Bhavan 13. The General Secretary Distt: Chhindwara (MP) Indian National Mines Overman Sirdar/Shitfirers Association, 7. The General Secretary P.O. Babupeth, Distt. Chandrapur Koyla Shramik Sabha Western Coalfields limited Federation (HMS), 116, Sulbha Niwas Sindikhana, Ganeshpeth, Nagpur Subject: IE (S.Os) Act, 1946 – appeal under section 6(1) preferred by the Management union of Western Coalfields Limited, Nagpur. -

“Power Finance Corporation - Investors Interaction Meet”

“Power Finance Corporation - Investors Interaction Meet” May 31, 2018 MANAGEMENT: TEAM OF POWER FINANCE CORPORATION:- - Mr. Rajeev Sharma - Chairman and Managing Director - Mr. D. Ravi - Director (Commercial) - Mr. C. Gangopadhyay - Director (Project) - Shri Sitaram Pareek - Independent Director Page 1 of 23 Power Finance Corporation May 31, 2018 Speaker: Good Afternoon, Ladies and Gentlemen. On behalf of Power Finance Corporation, we feel honored and privileged to welcome you all to this Investors Interaction Meet. The company recently announced its financial results for the year 2017-18 and has been successful in maintaining its growth trajectory. PFC is always aiming to connect with its investor and build a strong and enduring positive relationship with the investment community. With this objective, today’s event has been organized to discuss PFC’s current performance and future outlook with the current and prospective investors. On the desk in the center is Chairman and Managing Director -- Shri Rajeev Sharma along with the other directors. To my immediate left is Shri DRavi – Director, Commercial. Next to him is Shri C Gangopadhyay – Director, Projects. To my extreme left is Shri Sitaram Pareek – Independent Director and beside him is Shri N.B. Gupta – Director, Finance. They are all in front of you to give a brief insight of PFC’s performance during the financial year 2017-18. They will also present to you a roadmap for the forthcoming year. I request Shri Rajeev Sharma -- Chairman and Managing Director to address the gathering. Rajeev Sharma: Thank you very much for sparing your valuable time to be present here during this interaction. -

Presentation Satellite Suveillanc

ENVIRONMENT DIVISION COAL INDIA LTD HEADQUARTERS LAND RECLAMATION • Opencast mining method necessitates excavation of land. • This initially leads to degradation of land. • Coal India, tries to bring back the lost greenery by continuous afforestation and other reclamation activities. • The mine reclamation is being monitored by advanced techniques i.e. Satellite Surveillance SATELLITESATELLITE SURVEILLANCESURVEILLANCE OFOF OPENCASTOPENCAST MINESMINES OBJECTIVES SATELLITE SURVEILLANCE To have practical idea about Areas of backfilled zone Plantation status / Social Forestry Position of OB Dumps – Internal / External Active Mining Area Water bodies Land Use Classes viz. waste land, agricultural land & forest land. Status of Settlement / Resettlement To assess the remedial measures required for land reclamation / restoration. To utilize the reclaimed land for larger socio-economic benefits in a planned way. Procedures: Satellite Data: Procurement of RESOURCESAT (LISS-IV) data from NRSA, Hyderabad (Government of India Undertaking). Collateral Data: Procurement of Ancillary Data related to concerned OCP from coal company. Satellite Data Processing: Data processed using ERDAS image processing software. Information stored on GIS Platform for temporal analysis. Ground Truthing: Selective ground verification of land use classes to be validated in each project. Report Finalisation: Report finalised and uploaded in websites of CIL, CMPDIL & concerned subsidiary. Basic Data Data Source Secondary Data Topographical Maps Pre-processing, -

Detailed Advertisement for Recruitment of Company Secretary in E6, E7 and E8 Grades in Executive Cadre

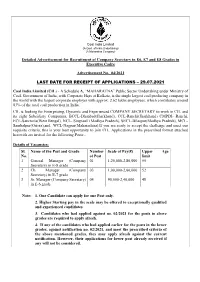

Coal India Limited (A Govt. of India Undertaking) (A Maharatna Company) Detailed Advertisement for Recruitment of Company Secretary in E6, E7 and E8 Grades in Executive Cadre Advertisement No. 04/2021 LAST DATE FOR RECEIPT OF APPLICATIONS – 29.07.2021 Coal India Limited (CIL) - A Schedule A, “MAHARATNA” Public Sector Undertaking under Ministry of Coal, Government of India, with Corporate Hqrs at Kolkata, is the single largest coal producing company in the world with the largest corporate employer with approx. 2.62 lakhs employees, which contributes around 83% of the total coal production in India. CIL is looking for Enterprising, Dynamic and Experienced COMPANY SECRETARY to work in CIL and its eight Subsidiary Companies, BCCL-Dhanbad(Jharkhand), CCL-Ranchi(Jharkhand) CMPDI- Ranchi, ECL-Sanctoria(West Bengal), NCL- Singrauli (Madhya Pradesh), SECL-Bilaspur(Madhya Pradesh), MCL- Sambalpur(Orissa),and WCL-Nagpur(Maharashtra).If you are ready to accept the challenge and meet our requisite criteria, this is your best opportunity to join CIL. Applications in the prescribed format attached herewith are invited for the following Posts:- Details of Vacancies: Sl. Name of the Post and Grade Number Scale of Pay(₹) Upper Age No. of Post limit 1 General Manager (Company 01 1,20,000-2,80,000 55 Secretary) in E-8 grade 2 Ch. Manager (Company 03 1,00,000-2,60,000 52 Secretary) in E-7 grade 3 Sr. Manager (Company Secretary) 04 90,000-2,40,000 48 in E-6 grade Note- 1. One Candidate can apply for one Post only. 2. Higher Starting pay in the scale may be offered to exceptionally qualified and experienced candidates. -

Ngo Documents 2013-08-14 00:00:00 Coal India Investor Brief High Risk

High risk, low return COAL INDIA LTD’s shareholder value is threatened by poor corporate governance, faulty reserve estimations, regulatory risk and macro-economic issues. Introduction Coal India Limited is the world’s largest coal miner, with a production of 435 million metric tons (MT) in 2011 -201 2. There is significant pressure on CIL to deliver annual production growth rates in excess of 7%. The company has a 201 7 production target of 61 5 MT.[1 ] Coal India’s track record raises questions over its ability to deliver this rate of growth. In addition, serious governance issues are likely to impact CIL’s financial performance. These pose a financial and reputational risk to CIL, its shareholders and lenders, while macro- economic issues in the Indian energy economy pose a long term threat to Coal India. • CIL’s attempts to access new mining areas are facing widespread opposition from local communities and environmental groups. With its reliance on open-pit mining, access to new mines are essential for CIL to achieve production targets. G • CIL has grown reliant on shallow, open pit mining for 90% of its production, and has lost in-house expertise on deep mining techniques. N I • CIL has a record of poor corporate governance, manifested in rampant corruption, poor worker safety and repeated legal violations. This has, in the last year alone, led to penalties and F closure notices for over 50 mines, threatening both its financial performance and reputation. E I • CIL’s financial performance has been affected by directives from majority shareholder Government of India to keep coal prices artifically low.[2] According to one estimate, this cost R CIL $1 .75 billion in the 201 2-1 3 financial year alone.[3] The government has also taken away coal blocks allocated to CIL and given them to private players.[4] B • Changing economics of coal power in India; renewable energies are becoming cost- competitive even as coal faces increased regulatory scrutiny and public opposition. -

G20 Subsidies to Oil, Gas and Coal Production

G20 subsidies to oil gas and coal production: India Vibhuti Garg and Ken Bossong Argentina Australia Brazil Canada China France Germany India Indonesia Italy Japan Korea (Republic of) Mexico Russia Saudi Arabia This country study is a background paper for the report Empty promises: G20 subsidies South Africa to oil, gas and coal production by Oil Change International (OCI) and the Overseas Turkey Development Institute (ODI). It builds on research completed for an earlier report The fossil United Kingdom fuel bailout: G20 subsidies to oil, gas and coal exploration, published in 2014. United States For the purposes of this country study, production subsidies for fossil fuels include: national subsidies, investment by state-owned enterprises, and public finance.A brief outline of the methodology can be found in this country summary. The full report provides a more detailed discussion of the methodology used for the country studies and sets out the technical and transparency issues linked to the identification of G20 subsidies to oil, gas and coal production. The authors welcome feedback on both this country study and the full report to improve the accuracy and transparency of information on G20 government support to fossil fuel production. A Data Sheet with data sources and further information for India’s production subsidies is available at: http://www.odi.org/publications/10073-g20-subsidies-oil-gas-coal-production-india priceofoil.org Country Study odi.org November 2015 Background remained substantial at $11 billion in 2014–15 (MoPNG, India has substantial fossil fuel reserves, including 61 2015b). Similar consumer subsidies of approximately billion tonnes of coal, 5.7 billion barrels of oil and 1.4 $12 billion in 2012–13 existed in the electricity sector. -

Western Coalfields Limited (A Govt

Western Coalfields Limited (A Govt. of India Undertaking) (A MINIRATNA Company) NOTIFICATION FOR ENGAGEMENT OF DOCTORS ON TEMPORARY CONTRACT BASIS Notification No: WCL/2021/EE/1418 Western Coalfields Limited (WCL)- A Schedule B, “MINIRATNA” Public Sector Undertaking under Ministry of Coal, Government of India, is one of the eight Subsidiary Companies of Coal India Limited. It has mining operation spread over the states of Maharashtra (in Nagpur, Chandrapur & Yeotmal Districts) and Madhya Pradesh (in Betul and Chhindawara Districts) with total manpower of 38,097 employees. The coal production target for FY 2021-22 for WCL is 60 MT. The Company is a major source of supplies of coal to the industries located in Western India in the States of Maharashtra, Madhya Pradesh, Gujrat and also in Southern India of state of Karnataka. A large numbers of Power Houses under Maharashtra, Madhya Pradesh, Gujrat, Karnataka - Electricity Boards are major consumers of its coal along with cement, steel, chemical, fertilizer, paper and brick industries in these states. Western Coalfields Limited is looking for dedicated and enterprising doctors to work in its subsidiaries/ coalfield Areas Hospitals/Dispensaries on temporary contract basis. If you are ready to accept the challenge and meet our requisite criteria, this is your best opportunity to work in WCL. Details of requirement at Western Coalfields Limited : Sl. Category of Doctor Number of Monthly Consolidated No. Post Honorarium 1. Doctors with MBBS qualification 09 Rs. 90,000 /- Doctors with MBBS plus 2. 24 Rs. 1,25,000 /- Specialization Vacancies at Western Coalfields Limited : There are total 33 vacancies of General Duty Medical Officers and Specialist. -

Result of Star Rating Base Year 2018-19

STAR RATING OF UNDERGROUND MINES FOR THE YEAR 2018-19 Annexure-A Type STAR RATING Name of the Coal India FINAL MARKS % Sl. Name of the Coal Mine of AWARDED BY Subsidiary / Company STAR RATING. Mine CCO 1 Shyamsunderpur Colliery UG Eastern Coalfield Limited 94 FIVE STAR EASTERN COAL FIELDS 2 JHANJRA PROJECT COLLIERY UG 92 FIVE STAR LIMITED 3 Sreerampur-1 Incline UG SCCL 92 FIVE STAR South Eastern Coalfields 4 Churcha Mine RO UG 91 FIVE STAR Limited Coal India Limited 5 Adriyala Shaft Project(ALP) UG SCCL 87 FOUR STAR 6 BAHERABANDH UG MINE UG SECL 87 FOUR STAR 7 Katkona 1&2 UG SECL 87 FOUR STAR EASTERN COALFIELD 8 SHANKARPUR COLLIERY UG 87 FOUR STAR LIMITED EASTERN COALFIELDS 9 KUMARDHUBI COLLIERY UG 86 FOUR STAR LIMITED 10 Badjna Colliery UG Eastern coal limited 85 FOUR STAR 11 KAPILDHARA UGP UG SECL 85 FOUR STAR 12 Khandra Colliery UG E.C.L 85 FOUR STAR WESTERN COALFIELDS 13 SHOBHAPUR UG 85 FOUR STAR LIMITED Eastern Coalfields 14 Dhemomain pit colliery UG 84 FOUR STAR Limited 15 Godavarikhani - 7 LEP UG SCCL 84 FOUR STAR 16 SHEETALDHARA-KURJA UGP UG SECL 84 FOUR STAR 17 SODEPUR (R) COLLIERY UG Eastern coalfields Limited 84 FOUR STAR Eastern Coalfields 18 Bahula Colliery UG 83 FOUR STAR Limited 19 BANKOLA UG ECL 83 FOUR STAR WESTERN COALFIELDS 20 SAONER MINE NO 1 UG 83 FOUR STAR LIMITED WESTERN COALFIELDS 21 SARNI MINE UG 83 FOUR STAR LIMITED Western coalfields 22 Silewara Colliery UG 83 FOUR STAR Limited 23 Singhal under ground mine UG Secl 83 FOUR STAR 24 Sreerampur-3 & 3A Incline UG SCCL 83 FOUR STAR 25 Tawa UG WCL 83 FOUR STAR 26 Tilaboni Colliery UG ECL 83 FOUR STAR Western Coalfields 27 Adasa mine UG 82 FOUR STAR limited Eastern Coalfields 28 Chinakuri Mine No. -

WESTERN COALFIELDS LIMITED Environment Department

WESTERN COALFIELDS LIMITED Environment Department Proposal No. IA/MH/CMIN/20125/2010 Project Name: Kamptee Deep OC Coal Mine Project Proposal submission date: 09.04.2019 Information /Clarification on EDS raised on 20.04.2019 Sl.No Particulars Submission 1 Annual Coal Production Environmental Clearance of Inder UG to OC Expansion Mining from two mines project for a production capacity of 1.20 MTPA in an area of 463.80 separately ha was accorded by MOEF & CC vide letter no.J-11015/35/2010- IA-II(M) dated 06.02.2013. Annual Coal Production details vis-à-vis EC capacity (for last 5 years) is as follows: Sl.No Year EC Capacity Production (in MTPA) (in MT) 1 2014-15 1.20 0.13 2 2015-16 1.20 0.78 3 2016-17 1.20 0.80 4 2017-18 1.20 0.75 5 2018-19 1.20 0.72 Environmental Clearance of Expansion of Kamptee Deep OC coal mine project for capacity of 1.50 MTPA (normative), 2.0 MTPA (peak) in ML area of 667.65 ha was accorded by MOEF & CC vide letter no.J-11015/287/2010-IA-II(M) dated 11.05.2015. Annual Coal Production details vis-à-vis EC capacity (for last 5 years) is as follows: Sl. Year EC Production No Capacity (in MT) (in MTPA) 1 2014-15 1.5 1.14 2 2015-16 2.0 0.92 3 2016-17 2.0 0.95 4 2017-18 2.0 0.52 5 2018-19 2.0 0.61 2 Details of Consent to Inder UG to OC Expansion Mining project : Consent to Operate operate granted by MPCB vide letter no BO/JD (APC)/UAN no.