2010 Kazakhstan Eiti Report.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

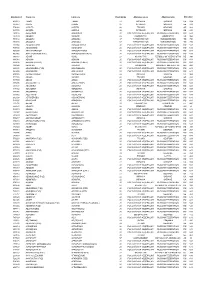

FÁK Állomáskódok

Állomáskód Orosz név Latin név Vasút kódja Államnév orosz Államnév latin Államkód 406513 1 МАЯ 1 MAIA 22 УКРАИНА UKRAINE UA 804 085827 ААКРЕ AAKRE 26 ЭСТОНИЯ ESTONIA EE 233 574066 ААПСТА AAPSTA 28 ГРУЗИЯ GEORGIA GE 268 085780 ААРДЛА AARDLA 26 ЭСТОНИЯ ESTONIA EE 233 269116 АБАБКОВО ABABKOVO 20 РОССИЙСКАЯ ФЕДЕРАЦИЯ RUSSIAN FEDERATION RU 643 737139 АБАДАН ABADAN 29 УЗБЕКИСТАН UZBEKISTAN UZ 860 753112 АБАДАН-I ABADAN-I 67 ТУРКМЕНИСТАН TURKMENISTAN TM 795 753108 АБАДАН-II ABADAN-II 67 ТУРКМЕНИСТАН TURKMENISTAN TM 795 535004 АБАДЗЕХСКАЯ ABADZEHSKAIA 20 РОССИЙСКАЯ ФЕДЕРАЦИЯ RUSSIAN FEDERATION RU 643 795736 АБАЕВСКИЙ ABAEVSKII 20 РОССИЙСКАЯ ФЕДЕРАЦИЯ RUSSIAN FEDERATION RU 643 864300 АБАГУР-ЛЕСНОЙ ABAGUR-LESNOI 20 РОССИЙСКАЯ ФЕДЕРАЦИЯ RUSSIAN FEDERATION RU 643 865065 АБАГУРОВСКИЙ (РЗД) ABAGUROVSKII (RZD) 20 РОССИЙСКАЯ ФЕДЕРАЦИЯ RUSSIAN FEDERATION RU 643 699767 АБАИЛ ABAIL 27 КАЗАХСТАН REPUBLIC OF KAZAKHSTAN KZ 398 888004 АБАКАН ABAKAN 20 РОССИЙСКАЯ ФЕДЕРАЦИЯ RUSSIAN FEDERATION RU 643 888108 АБАКАН (ПЕРЕВ.) ABAKAN (PEREV.) 20 РОССИЙСКАЯ ФЕДЕРАЦИЯ RUSSIAN FEDERATION RU 643 398904 АБАКЛИЯ ABAKLIIA 23 МОЛДАВИЯ MOLDOVA, REPUBLIC OF MD 498 889401 АБАКУМОВКА (РЗД) ABAKUMOVKA 20 РОССИЙСКАЯ ФЕДЕРАЦИЯ RUSSIAN FEDERATION RU 643 882309 АБАЛАКОВО ABALAKOVO 20 РОССИЙСКАЯ ФЕДЕРАЦИЯ RUSSIAN FEDERATION RU 643 408006 АБАМЕЛИКОВО ABAMELIKOVO 22 УКРАИНА UKRAINE UA 804 571706 АБАША ABASHA 28 ГРУЗИЯ GEORGIA GE 268 887500 АБАЗА ABAZA 20 РОССИЙСКАЯ ФЕДЕРАЦИЯ RUSSIAN FEDERATION RU 643 887406 АБАЗА (ЭКСП.) ABAZA (EKSP.) 20 РОССИЙСКАЯ ФЕДЕРАЦИЯ RUSSIAN FEDERATION RU 643 -

Water Resources Lifeblood of the Region

Water Resources Lifeblood of the Region 68 Central Asia Atlas of Natural Resources ater has long been the fundamental helped the region flourish; on the other, water, concern of Central Asia’s air, land, and biodiversity have been degraded. peoples. Few parts of the region are naturally water endowed, In this chapter, major river basins, inland seas, Wand it is unevenly distributed geographically. lakes, and reservoirs of Central Asia are presented. This scarcity has caused people to adapt in both The substantial economic and ecological benefits positive and negative ways. Vast power projects they provide are described, along with the threats and irrigation schemes have diverted most of facing them—and consequently the threats the water flow, transforming terrain, ecology, facing the economies and ecology of the country and even climate. On the one hand, powerful themselves—as a result of human activities. electrical grids and rich agricultural areas have The Amu Darya River in Karakalpakstan, Uzbekistan, with a canal (left) taking water to irrigate cotton fields.Upper right: Irrigation lifeline, Dostyk main canal in Makktaaral Rayon in South Kasakhstan Oblast, Kazakhstan. Lower right: The Charyn River in the Balkhash Lake basin, Kazakhstan. Water Resources 69 55°0'E 75°0'E 70 1:10 000 000 Central AsiaAtlas ofNaturalResources Major River Basins in Central Asia 200100 0 200 N Kilometers RUSSIAN FEDERATION 50°0'N Irty sh im 50°0'N Ish ASTANA N ura a b m Lake Zaisan E U r a KAZAKHSTAN l u s y r a S Lake Balkhash PEOPLE’S REPUBLIC Ili OF CHINA Chui Aral Sea National capital 1 International boundary S y r D a r Rivers and canals y a River basins Lake Caspian Sea BISHKEK Issyk-Kul Amu Darya UZBEKISTAN Balkhash-Alakol 40°0'N ryn KYRGYZ Na Ob-Irtysh TASHKENT REPUBLIC Syr Darya 40°0'N Ural 1 Chui-Talas AZERBAIJAN 2 Zarafshan TURKMENISTAN 2 Boundaries are not necessarily authoritative. -

Revision of the Quedius Fauna of Middle Asia (Coleoptera, Staphylinidae, Staphylininae)

Dtsch. Entomol. Z. 65 (2) 2018, 117–159 | DOI 10.3897/dez.65.27033 Revision of the Quedius fauna of Middle Asia (Coleoptera, Staphylinidae, Staphylininae) Maria Salnitska1, Alexey Solodovnikov2 1 Department of Entomology, St. Petersburg State University, Universitetskaya Embankment 7/9, Saint-Petersburg, Russia 2 Natural History Museum of Denmark, Zoological Museum, Universitetsparken 15, Copenhagen 2100 Denmark http://zoobank.org/B1A8523C-A463-4FC4-A0C3-072C2E78BA02 Corresponding authors: Maria Salnitska ([email protected]); Alexey Solodovnikov ([email protected]) Abstract Received 29 May 2018 Accepted 6 July 2018 Twenty eight species of the genus Quedius from Middle Asia comprising Kazakhstan, Published 31 July 2018 Kyrgyzstan, Tajikistan, Turkmenistan and Uzbekistan, are revised. Quedius altaicus Korge, 1962, Q. capitalis Eppelsheim, 1892, Q. fusicornis Luze, 1904, Q. solskyi Luze, Academic editor: 1904 and Q. cohaesus Eppelsheim, 1888 are redescribed. The following new synonymies James Liebherr are established: Q. solskyi Luze, 1904 = Q. asiaticus Bernhauer, 1918, syn. n.; Q. cohae- sus Eppelsheim, 1888 = Q. turkmenicus Coiffait, 1969, syn. n., = Q. afghanicus Coiffait, 1977, syn. n.; Q. hauseri Bernhauer, 1918 = Q. peneckei Bernhauer, 1918, syn. n., = Q. Key Words ouzbekiscus Coiffait, 1969,syn. n.; Q. imitator Luze, 1904 = Q. tschinganensis Coiffait, 1969, syn. n.; Q. novus Eppelsheim, 1892 = Q. dzambulensis Coiffait, 1967, syn. n., Staphylininae Q. pseudonigriceps Reitter, 1909 = Q. kirklarensis Korge, 1971, syn. n. Lectotypes are Staphylinini designated for Q. asiaticus Bernhauer, 1918, Q. fusicornis Luze, 1904, Q. hauseri Ber- Quedius nhauer, 1918, Q. imitator Luze, 1904, Q. novus Eppelsheim, 1892 and Q. solskyi Luze, Middle Asia 1904. For all revised species, taxonomy, distribution and bionomics are summarized. -

Investor Guide ‘19

INVESTOR GUIDE ‘19 IN ASSOCIATION WITH GOVERNMENT REGIONAL CENTER OF ALMATY REGION FOR DEVELOPMENT OF ALMATY REGION Dear friends! One of the key factors of investment attractiveness is macroeconomic, social and political stability. Almaty region is one of the largest regions in Kazakhstan with huge natural potential and a favorable geographical position for transit opportunities, which provides sufficient possibilities for partnership and business development. All the necessary conditions for the implementation of joint business initiatives with domestic and foreign partners are provided. We are interested in building mutually beneficial relations, in attracting innovative projects using the latest accomplishments and effective technologies. Sincerely, the Governor of Almaty region Amandyk Batalov ALMATY REGION East Kazakhstan region Alakol Karagandy lake region e Sarkand district Alakol district Balkhash lak Karatal Aksu district district Balkhash Eskeldy district TALDYKORGAN district China TEKELI Koksu district Panfilov Ile Kerbulak district district district Kapshagay lake Zhambyl Uigur KAPSHAGAY district region Enbekshikazakh district Zhambyl ALMATY district Talgar Kegen Raimbek district dictrict district Karasay district Kyrgyzstan Area Structure Lakes 223 911 km² 17 districts Balkhash - 16 400 km² 3 cities Alakol - 2 200 km² Population Regional Center Major rivers 2 mln. people Taldykorgan Ili, Aksu, Koksu, Lepsy, Karatal TRANSIT POTENTIAL ТРАНЗИТНЫЙ ПОТЕНЦИАЛ Almaty region has a unique transport and logistics potential: 5 road crossing -

Access to Drinking Water and Sanitation in the Republic of Kazakhstan

Committee for Water Resources Ministry of Agriculture of the Republic of Kazakhstan UNDP Project National Plan for Integrated Water Resources Management and Water Efficiency in Kazakhstan RepORT AcceSS TO DrinkinG WATer and SaniTATION in THE RepuBLic OF KAZakHSTan January 2006 Foreword Supplying population of the Republic of Kazakhstan with adequate quality drinking water is one of the priority directions of the social-economic development of the country. For Kazakhstan the Millennium Development Goals are the long-term goals, which are closely related to the National Development Strategy “Kazakhstan-2030”. The problem of supply of population with drinking water is reflected in such national documents as the Conception of the Water Economic and Political Sector Development of the Republic of Kazakhstan until 2010, the Strategy for Industrial and Innovation Development of the Republic of Kazakhstan for 2003-2015, as well as the Water Code of the Republic of Kazakhstan. Kazakhstan carries out a systematic work on water supply and sanitation in the framework of the sectoral Program “Drinking water” and the National Program on Development of Rural Territories. Under these programs the construction and reconstruction of the water supply systems in urban and rural areas is carried out. For the next 10 years of the program implementation 115 billion tenge are planned to be allocated from the republican budget. At the same time the factors inhibitory to stable and successful programme implementation are the following: a high level of deterioration of water supply networks and units, insufficient development and equipment of the water pipes traffic departments, as well as insufficiency in reliable official data on the accessibility of drinking water to population of Kazakhstan. -

Renewable Project Environmental Review Report - Wind

Prepared For: Consultancy Contract C26157REV/JPNS- 2013-02-01 Kazakhstan Renewable Energy Financing Facility (KazREFF) - Strategic Environmental Review Renewable Project Environmental Review Report - Wind June 2014 ERM Japan Ltd. The Landmark Tower Yokohama 19th Floor, 2-2-1 Minatomirai, Nishi-ku YOKOHAMA 220-8119 Japan www.erm.com The world's leading sustainability consultancy Contents 1.0 INTRODUCTION 1 2.0 RESOURCE AVAILABILITY AND POTENTIAL 2 2.1 RESOURCE AVAILABILITY 2 2.2 RESOURCE POTENTIAL 6 2.3 TRANSMISSION CAPACITY AND CONSTRAINTS 6 2.3.1 Existing Conditions 7 2.3.2 Anticipated Development 10 2.4 EXISTING PROJECTS 11 2.5 KNOWN PROPOSED PROJECTS 11 3.0 AVAILABLE AND PRACTICAL TECHNOLOGIES 14 3.1 COMPONENTS 14 3.1.1 Met Mast/Towers 15 3.1.2 Wind Turbines and Foundations 16 3.1.3 Support Buildings 17 3.1.4 Access Roads 18 3.2 GRID CONNECTIVITY 18 3.3 SITE DESIGN AND CONFIGURATION 20 3.3.1 Wind Farm Layouts 22 3.3.2 Construction 23 3.3.3 Commissioning, Operation, and Maintenance 24 3.3.4 Decommissioning 24 3.4 DEVELOPMENT COSTS 25 3.5 SUPPLY CHAIN IN KAZAKHSTAN 25 4.0 ENVIRONMENTAL AND SOCIAL CONSTRAINTS 27 The world's leading sustainability consultancy 5.0 KAZREFF PROJECT APPRAISAL - ENVIRONMENTAL AND SOCIAL PERFORMANCE REQUIREMENTS 31 5.1 EBRD REQUIREMENTS 31 5.1.1 Category A 32 5.1.2 Category B 33 5.2 KAZAKHSTAN REQUIREMENTS 33 5.3 KAZREFF APPRAISAL PROCESS 35 5.3.1 Initial Screening 36 5.3.2 Documentation Review and Approval/Feedback 36 6.0 APPENDICES 38 The world's leading sustainability consultancy 1.0 INTRODUCTION This Renewable Project Environmental Review (RPER) Report for Wind in Kazakhstan is one of four separate reports (other RPER reports were prepared for solar photovoltaic, small hydropower, and biogas) that have been prepared by Environmental Recourses Management (ERM) for the European Bank for Reconstruction and Development (EBRD). -

Assessment of the Tourist Recreation Capacity of Lake Alakol Basin

GeoJournal of Tourism and Geosites Year XIII, vol. 30, no. 2 supplement, 2020, p.875-879 ISSN 2065-1198, E-ISSN 2065-0817 DOI 10.30892/gtg.302spl13-517 ASSESSMENT OF THE TOURIST RECREATION CAPACITY OF LAKE ALAKOL BASIN Zhandos T. MUKAYEV* Shakarim University, Department of Science Disciplines, Glinki 20a st, 071412, Semey Kazakhstan, e-mail: [email protected] Zhanar O. OZGELDINOVA L. N. Gumilyev Eurasian National University, Department of Physical and Economical Geography, 2 Mirzoyanst, 010008, Nur-Sultan Kazakhstan, e-mail: [email protected] Kulchikhan M. JANALEYEVA L. N. Gumilyev Eurasian National University, Department of Physical and Economical Geography, 2 Mirzoyanst, 010008, Nur-Sultan Kazakhstan, e-mail: [email protected] Nurgul YE. RAMAZANOVA L. N. Gumilyev Eurasian National University, Department of Physical and Economical Geography, 2 Mirzoyanst, 010008, Nur-Sultan Kazakhstan, e-mail: [email protected] Altyn A. ZHANGUZHINA L. N. Gumilyev Eurasian National University, Department of Physical and Economical Geography, 2 Mirzoyanst, 010008, Nur-Sultan Kazakhstan, e-mail: [email protected] Citation: Mukayev, T.Zh., Ozgeldinova, O.Zh., Janaleyeva, M.K., Ramazanova, Ye.N., & Zhanguzhina, A.A. (2020). ASSESSMENT OF THE TOURIST RECREATION CAPACITY OF LAKE ALAKOL BASIN. GeoJournal of Tourism and Geosites, 30(2spl), 875–879. https://doi.org/10.30892/gtg.302spl13-517 Abstract: This article proposes criteria for a component-wise integrated assessment of the recreational attractiveness of the landscapes of the Alakol Lake basin. This methodology is based on a component-wise landscape assessment, which consists of the main indicators that make up the landscape: topography, climate, water bodies, and soil and vegetation cover. -

1St-Year STUDENT's GUIDE

ASFENDIYAROV KAZAKH NATIONAL MEDICAL UNIVERSITY 1st-year STUDENT’S GUIDE Almaty 2018 Dear first-year students! I congratulate you on the significant event in your life - you have become medical students! Today, Asfendiyarov Kazakh National Medical University - the oldest medical university of the country – gladly welcomes you to its big family. You have chosen one of the most difficult, but at the same time, the most interesting specialty - medicine. I wish you to succeed in your studies, keep interest and love of your chosen profession throughout your life, become a highly qualified specialist for the benefit of the national health care and rise to eminence in your profession. KazNMU was founded in 1930. The first rector of the university was a prominent state and public figure, a doctor, a well-known scientist, a talented teacher, Professor Sanzhar Dzhafarovich Asfendiyarov, who made a significant contribution to the development of science and education in Kazakhstan. Our University is named after this great person. In 2001, by the Decree of the President of the Republic of Kazakhstan dated July 5, 2001, No. 648 “On granting special status to the individual state higher educational institutions", S.Asfendiyarov Kazakh State Medical University was awarded a special status - the status of the National University. Good luck, dear first-year students! Rector, Professor Nurgozhin T.S. 2 Mission – is the formation of a new generation of medical workers with the level of professional training, technological skills and competitiveness that meet modern priorities and future challenges of Kazakhstani and world health of the 21st century. Vision: KazNMU is the leader of modern medical and pharmaceutical education, science and clinical practice in Kazakhstan and Central Asia. -

Volume of the Works of Potential Supplier (Provision of Services) for the Last Eight Years

Volume of the works of potential supplier (provision of services) for the last eight years The name of services The name and contact The place and year of data of customers service provision Conducting technical The Kazakh Scientific Eskeldi district, supervision during the work Research and Design March, 2007 on major overhaul of the Institute of road and “Taldykorgan - Tekeli” transport problems Highway km.0-12. «DORTRANS» Eskeldi district Mob.: 244-65-21 Conducting technical The Kazakh Scientific Karasay district, supervision during the work Research and Design Sepember, 2007 on major overhaul of the Institute of road and “Kaskelen-Lime Plant” transport problems Highway km.0-18. «DORTRANS» Karasay district Mob.: 244-65-21 Conducting technical The State Institution "The Karasay district, supervision during the work Department of passenger March, 2008 on major overhaul of transport and highways of the “Kaskelen - Lime Plant” Almaty region" Highway km.0-18. Karasay district Mob.: 272019 Conducting technical The State Institution "The Karasay district, supervision during the work Department of passenger March, 2008 on major overhaul of transport and highways of «the entrance to the tract Almaty region" Maralsay» Highway km.0-7,5. Mob.: 272019 Karasay district Conducting technical The State Institution "The Sarkand district, supervision during the work Department of passenger August, 2008 on major overhaul of transport and highways of the bridge on “ the entrance Almaty region" to the Kokterek v.” Highway Mob.: 272019 Sarkand district Conducting technical The State Institution "The Sarkand district, supervision during the work Department of passenger on major overhaul of transport and highways of August, 2008 «The entrance to the Abay Almaty region" v.» Highway km.0-3. -

Meadow Vegetation of the Zhetysu Alatau Mountains

Dimeyeva et al.: Meadow vegetation - 375 - MEADOW VEGETATION OF THE ZHETYSU ALATAU MOUNTAINS DIMEYEVA, L. A.1* – SITPAYEVA, G. T.1 – USSEN, K.2 – ORLOVSKY, L.3 – ABLAIKHANOV, E.4 – ISLAMGULOVA, A. F.1 – ZHANG, Y.5 – ZHANG, J.5 – SULEIMENOVA, N. S.2 1Institute of Botany and Phytointroduction, Almaty, 050040, Kazakhstan 2Department of Ecology, Kazakh National Agrarian University, Almaty, Kazakhstan 3Ben-Gurion University of Negev, Sede Boqer, Israel 4Al-Farabi Kazakh National University, Almaty, Kazakhstan 5Xinjiang Institute of Ecology and Geography, Chinese Academy of Sciences, Urumqi, China *Corresponding author e-mail: [email protected] (phone: +7-727-3947642, fax: +7-727-3948040) (Received 28th Apr 2016; accepted 22nd Jul 2016) Abstract. The Zhetysu (Junggar) Alatau mountain system consists of mainly two parallel, high mountain ranges: the northern and the southern. The natural border between the ranges is the Koksu river and the Boro Tala river (located in China). Climate conditions, water resources, soil cover, altitudinal zonality of plant cover vary in the northern and the southern ranges (macro slopes). The aim of the research was to give phytocoenotic characteristic of meadow vegetation, to determine the ecological-physiognomic types of meadows, to identify the species composition of natural communities and indicators of anthropogenic influence. Meadow vegetation inhabits a wide altitudinal range from piedmont deserts and low-hill terrains to subalpine and alpine belts, with a high degree of species and phytocoenotic diversity. -

Investing in Energy Efficiency to Reduce Climate Change

Project Report Investing in energy efficiency to reduce climate change National Center for Energy Saving and Energy Efficiency, The National Party Concerned Slide 2 The reason: Memorandum of Understanding between UNECE and the National Party Concerned Project № ECE-INT-04-318 Slide 3 Action Plan calls for the preliminary works execution including the following: •Website building; • National Energy Policy Data for the purposes of regional studies; • Case Study. Slide 4 www.energy-effect.kz , 1.National Project website Content: - Briefly about Kazakhstan; - About the Project; - Summary and the Project objectives; - Purpose; - Events; - Public-Private Partnership based Investment Fund ; - Kazakhstan as the Project member; - National Coordinator (NC); - National Institutions Concerned (NIC). - News - Activities in the field of Energy Efficiency and Renewable Energy in Kazakhstan; -Institutional Structure in Power Supply, Thermal Energy and Gas sectors; -Brief description of Power Sector; - Kazakhstan Energy Policy; -Kazakhstan Energy Efficiency and Renewable Energy Policy; -Investment Programs and Projects; -Legislation and investment climate in Energy Efficiency and Renewable Energy. Slide 5 National Project website Performance: Concept and Structure were developed English and Russian versions are created Specific Projects realized by Ministries and Agencies, private structures of the Republic of Kazakhstan were inserted to the National Project website. Slide 6 2. National Energy Policy Data National Energy Policy Data was realized and submitted -

Updated 02.03.2021

Updated 02.03.2021 #1 Archandra caspia was recorded (as Parndra) for Turkmenia (Kopet-Dag) and for Transcaspean Iran (Gorgan) - (Araujo-Arigony, 1977) on the base of Lameere (1902): "habite a Transcaucasie, le nord de la Perse et la Turcomanie." The records were regarded by A.Semenov (1902) as wrong. Archandra Lameere, 1912 was regarded as a genus by A.Santo-Silva (2001). #2 According to Svacha (1987), Callipogon and Ergates belong to different tribes. #3 Ergates faber was recorded for Central Russia (two districts of Mordovia: Ichalki and Bolshie Berezniaki) by Z.A. Timraleev (2007). According to personal communication by M.Rejzek (15.10.2004): “Ergates faber was really described in 1761 and published in Fauna Svecia [in fact 1760](not in Systema Naturae, ed. 12, as written by many authors such as Aurivillius in Catalogus coleopterorum, Plavilstshikov (1936) or Villiers (1978). If you have a look at Systema Naturae ed. 12: 622, you will see that Linnaeus himself refers to “Fn. Svec.”. Bily & Mehl (Fauna Scandinavica) already wrote 1761.” Ergates faber m. hartigi Demelt, 1963 and E.f. ssp. alkani Demelt, 1968 were regarded by Villiers (1978) as aberrations of females. #4 Prinobius is a separate genus, according to Villiers (1978). According to Vives (2000), Macrotoma Serv.,1832-June is a junitor homonym of Macrotoma Laporte,1832-April (Diptera) and a new name was proposed: Prinobiini Vives, 2000. Macrotoma Serv.,1832 was maintained by D.Heffern et al., 2006, so Prinobiini is superfluous. According to Sama (1994): Prinobius myardi Muls., 1842 = Prionus scutellaris Germ., 1817 nec Olivier, 1795 (Pyrodes).