Aberdeen Standard Equity Income Trust

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Retirement Strategy Fund 2060 Description Plan 3S DCP & JRA

Retirement Strategy Fund 2060 June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA ACTIVIA PROPERTIES INC REIT 0.0137% 0.0137% AEON REIT INVESTMENT CORP REIT 0.0195% 0.0195% ALEXANDER + BALDWIN INC REIT 0.0118% 0.0118% ALEXANDRIA REAL ESTATE EQUIT REIT USD.01 0.0585% 0.0585% ALLIANCEBERNSTEIN GOVT STIF SSC FUND 64BA AGIS 587 0.0329% 0.0329% ALLIED PROPERTIES REAL ESTAT REIT 0.0219% 0.0219% AMERICAN CAMPUS COMMUNITIES REIT USD.01 0.0277% 0.0277% AMERICAN HOMES 4 RENT A REIT USD.01 0.0396% 0.0396% AMERICOLD REALTY TRUST REIT USD.01 0.0427% 0.0427% ARMADA HOFFLER PROPERTIES IN REIT USD.01 0.0124% 0.0124% AROUNDTOWN SA COMMON STOCK EUR.01 0.0248% 0.0248% ASSURA PLC REIT GBP.1 0.0319% 0.0319% AUSTRALIAN DOLLAR 0.0061% 0.0061% AZRIELI GROUP LTD COMMON STOCK ILS.1 0.0101% 0.0101% BLUEROCK RESIDENTIAL GROWTH REIT USD.01 0.0102% 0.0102% BOSTON PROPERTIES INC REIT USD.01 0.0580% 0.0580% BRAZILIAN REAL 0.0000% 0.0000% BRIXMOR PROPERTY GROUP INC REIT USD.01 0.0418% 0.0418% CA IMMOBILIEN ANLAGEN AG COMMON STOCK 0.0191% 0.0191% CAMDEN PROPERTY TRUST REIT USD.01 0.0394% 0.0394% CANADIAN DOLLAR 0.0005% 0.0005% CAPITALAND COMMERCIAL TRUST REIT 0.0228% 0.0228% CIFI HOLDINGS GROUP CO LTD COMMON STOCK HKD.1 0.0105% 0.0105% CITY DEVELOPMENTS LTD COMMON STOCK 0.0129% 0.0129% CK ASSET HOLDINGS LTD COMMON STOCK HKD1.0 0.0378% 0.0378% COMFORIA RESIDENTIAL REIT IN REIT 0.0328% 0.0328% COUSINS PROPERTIES INC REIT USD1.0 0.0403% 0.0403% CUBESMART REIT USD.01 0.0359% 0.0359% DAIWA OFFICE INVESTMENT -

Finn-Ancial Times Finncap Financials & Insurance Quarterly Sector Note

finn-ancial Times finnCap Financials & Insurance quarterly sector note Q3 2020 | Issue 9 Highlights this quarter: Elevated uncertainty and volatility have been hallmarks of the last 18 months, with Brexit, the UK General Election and more recently COVID-19 all contributing to the challenges that face investors wishing to carve out solid and stable returns amid these ‘unprecedented’ times. With this is mind, and simulating finnCap’s proven Slide Rule methodology, we found the highest quality and lowest value stocks across the financials space, assessing how the make-up of these lists changed over the period January 2019 to July 2020, tracking indexed share price performance over the period as well as movements in P/E and EV/EBIT valuations. The top quartile list of Quality companies outperformed both the Value list and the FTSE All Share by rising +2.5% over the period versus -5.4% for the All Share and -14.3% for Value stocks. Furthermore, the Quality list had protection on the downside in the market crash between February and March 2020, and accelerated faster amid the market rally between late March and July 2020. From high to low (January to March), Quality moved -36.3% against the Value list at -45.5%, while a move off the lows to July was +37.4% for Quality and +34.0% for Value. There was some crossover between the Quality and Value lists, with 7 companies of the top quartile (16 companies in total) appearing in both the Quality and Value lists. This meant that a) investors could capture what we call ‘Quality at Value’ (i.e. -

FTSE Factsheet

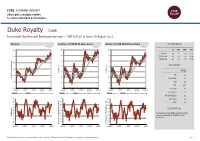

FTSE COMPANY REPORT Share price analysis relative to sector and index performance Duke Royalty DUKE Investment Banking and Brokerage Services — GBP 0.4125 at close 10 August 2021 Absolute Relative to FTSE UK All-Share Sector Relative to FTSE UK All-Share Index PERFORMANCE 10-Aug-2021 10-Aug-2021 10-Aug-2021 0.45 140 140 1D WTD MTD YTD Absolute -2.4 -1.2 -1.8 35.2 130 130 0.4 Rel.Sector -2.4 -0.5 -3.6 25.9 Rel.Market -2.8 -1.7 -3.7 20.9 120 120 0.35 VALUATION 110 110 0.3 Trailing 100 100 Relative Price Relative Price Relative 0.25 PE -ve Absolute Price (local (local currency) AbsolutePrice 90 90 EV/EBITDA -ve 0.2 80 80 PB 2.0 PCF 28.1 0.15 70 70 Div Yield 4.6 Aug-2020 Nov-2020 Feb-2021 May-2021 Aug-2021 Aug-2020 Nov-2020 Feb-2021 May-2021 Aug-2021 Aug-2020 Nov-2020 Feb-2021 May-2021 Aug-2021 Price/Sales -ve Absolute Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Net Debt/Equity 0.2 90 90 90 Div Payout -ve 80 80 80 ROE -ve 70 70 70 Share Index) Share Share Sector) Share - 60 - 60 60 DESCRIPTION 50 50 50 40 40 The Company is a globally focused investment 40 RSI RSI (Absolute) 30 30 company specialising in diversified royalty investment. -

Morningstar Report

Report as of 25 Sep 2021 Aberdeen Standard Equity Inc Trust plc , (GB0006039597) Morningstar Rating™ Peer Group Classification Last Close Last Actual NAV (23 Sep 2021) Discount Estimated Nav QQ Morningstar IT UK Equity 345.00 379.95 -9.20 379.95 Income Investment Objective Performance The fund aims to provide shareholders with an above 169 average income while also providing real growth in 146 capital and income. It will invest in a diversified 123 portfolio consisting mainly of quoted UK equities 100 which will normally comprise between 50 and 70 77 individual equity holdings. 54 2016 2017 2018 2019 2020 2021-08 -10.88 23.83 -12.55 9.46 -19.70 19.51 Fund 16.75 13.10 -9.47 19.17 -9.82 14.66 Benchmark 8.76 10.73 -10.56 18.95 -12.56 15.52 Category Management Fee Summary Management fee of 0.65% p.a. of NA on the first GBP 175m and 0.55% thereafter. No performance fee. Contract terminable on notice period of 6 months. Portfolio 31/08/2021 Asset Allocation % Long Short Net Equity Style Box™ Mkt Cap % Fund America Europe Asia Large Size Stocks 113.11 0.00 113.11 Giant 17.55 Bonds 0.00 0.00 0.00 Mid Large 18.27 Cash 0.00 13.11 -13.11 Medium 22.91 Other 0.00 0.00 0.00 Small Small 24.92 Value Blend Growth Micro 16.35 Style Average Mkt Fund Cap (Mil) Ave Mkt Cap GBP 4,115.7 <25 25-50 50-75 >75 7 Top Holdings Stock Sector Weightings % Fund World Regions % Fund Name Sector % hCyclical 66.41 Americas 2.36 BHP Group PLC r 4.54 rBasic Materials 13.25 United States 2.36 Rio Tinto PLC r 4.30 tConsumer Cyclical 14.81 Canada 0.00 CMC Markets PLC y 3.99 -

Dfs-Sofology-Decision-On-Merger.Pdf

ANTICIPATED ACQUISITION BY DFS FURNITURE PLC OF SOFOLOGY LIMITED DECISION ON RELEVANT MERGER SITUATION AND SUBSTANTIAL LESSENING OF COMPETITION ME/6706-17 The CMA’s decision on reference under section 33(1) of the Enterprise Act 2002 given on 20 November 2017. Full text of the decision published on 15 December 2017. Please note that [] indicates figures or text which have been deleted or replaced in ranges at the request of the parties for reasons of commercial confidentiality. SUMMARY 1. DFS Furniture plc (through its wholly owned subsidiary DFS Furniture Company Limited) (DFS) has agreed to acquire Sofology Limited (Sofology) (the Merger). DFS and Sofology are together referred to as the Parties. 2. The Competition and Markets Authority (CMA) believes that it is or may be the case that the Parties will cease to be distinct as a result of the Merger, that the turnover test is met and that, accordingly, arrangements are in progress or in contemplation which, if carried into effect, will result in the creation of a relevant merger situation. 3. The Parties overlap in the retail supply of upholstered living room furniture in bricks-and-mortar stores and online across the UK. 4. The CMA believes that online sales exercise some constraint on the bricks- and-mortar sales of upholstered living room furniture, although there may be limits to the competitive interaction between these two distribution channels. The CMA therefore considered competition between bricks-and-mortar retailers and competition between online retailers, both together and separately. 1 5. With regard to bricks-and-mortar competition, as the CMA could not rule out that the Parties vary some aspects of their competitive offering locally, the CMA assessed the effects of the Merger in the local areas where the Parties’ stores overlap. -

The Furniture Industry in the United Kingdom Scenario

THE FURNITURE INDUSTRY IN THE UNITED KINGDOM SCENARIO Multiclient Research COUNTRY REPORTS September 08 – R2413.UK HOME FURNITURE UPHOLSTERY MATTRESSES OFFICE KITCHEN APPLIANCES LIGHTING All CSIL publications are available for online purchase and immediate download from: http://www.csilmilano.com http://www.worldfurnitureonline.com Reports are also available in printed form. For further information, please contact: [email protected] CSIL Milano scrl 15 corso Monforte 20122 Milano Italy tel. +39 02 796630 fax +39 02 780703 © Copyright CSIL [email protected] – www.csilmilano.com SCENARIO The furniture industry in the United Kingdom COUNTRY REPORTS Report prepared by C. Pisa HOME FURNITURE Coordinated by A. Tracogna UPHOLSTERY MATTRESSES OFFICE KITCHEN APPLIANCES LIGHTING All rights reserved. Neither this publication nor any part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise. Any such action is an infringement of the Italian Law (L.18 August 2000 n.248) and may give rise to a legal action for damages and may be prosecuted as a criminal offence. All information in this report is verified to the best of the author's and the publisher's ability. However, CSIL does not accept responsibility for any errors and/ or omissions resulting from any source and for any loss arising from reliance on it. CSIL Milano scrl 15 corso Monforte 20122 Milano Italy tel. +39 02 796630 fax +39 02 780703 © Copyright CSIL [email protected] – www.csilmilano.com The furniture industry in the United Kingdom CONTENTS 1. UNITED KINGDOM. FURNITURE INDUSTRY SUMMARY 1 2. -

The Sofa Experts Sofa The

Annual report and accounts 2017 The sofa experts sofa The DFS Furniture plc Annual report and accounts 2017 DFS is the leading retailer of living room and upholstered furniture in the UK. As the sofa experts we are able to offer our customers an unbeatable combination of great products, great service and great value. Turnover to meet some of the sofa experts team Strategic Report Financial Statements Summary of the year 1 Consolidated income statement 71 Our business 2 Consolidated statement of Chair’s statement 4 comprehensive income 72 Market overview 6 Consolidated balance sheet 73 Our business model 8 Consolidated statement of Strategy for growth 10 changes in equity 74 Strategy in action 12 Consolidated cash flow statement 75 Risks and uncertainties 16 Notes to the consolidated Chief Executive’s report 20 financial statements 76 Key performance indicators 24 Company balance sheet 95 Financial review 26 Company statement of Corporate responsibility 28 changes in equity 96 Notes to the Company Governance financial statements 97 Board of Directors 36 Shareholder information 99 Directors’ report 38 Corporate governance statement 40 Audit Committee report 47 Nomination Committee report 52 Directors’ remuneration report 54 Directors’ responsibilities statement 65 Independent auditor’s report 66 Our sofa experts DFS has been built on long-term investments in British craftsmanship, manufacturing and people. Here are just a few of the inspiring team behind our sofas: Design Manufacture Lauren Harris, Designer Michael Coleman, Upholsterer Design Studio, Long Eaton Lincoln House factory Lauren’s role at DFS ranges Michael started out as an from designing products and apprentice with us where he selecting fabrics to ultimately trained in both the traditional and creating the future looks of DFS modern methods of upholstering. -

Fintech Monthly Market Update | July 2021

Fintech Monthly Market Update JULY 2021 EDITION Leading Independent Advisory Firm Houlihan Lokey is the trusted advisor to more top decision-makers than any other independent global investment bank. Corporate Finance Financial Restructuring Financial and Valuation Advisory 2020 M&A Advisory Rankings 2020 Global Distressed Debt & Bankruptcy 2001 to 2020 Global M&A Fairness All U.S. Transactions Restructuring Rankings Advisory Rankings Advisor Deals Advisor Deals Advisor Deals 1,500+ 1 Houlihan Lokey 210 1 Houlihan Lokey 106 1 Houlihan Lokey 956 2 JP Morgan 876 Employees 2 Goldman Sachs & Co 172 2 PJT Partners Inc 63 3 JP Morgan 132 3 Lazard 50 3 Duff & Phelps 802 4 Evercore Partners 126 4 Rothschild & Co 46 4 Morgan Stanley 599 23 5 Morgan Stanley 123 5 Moelis & Co 39 5 BofA Securities Inc 542 Refinitiv (formerly known as Thomson Reuters). Announced Locations Source: Refinitiv (formerly known as Thomson Reuters) Source: Refinitiv (formerly known as Thomson Reuters) or completed transactions. No. 1 U.S. M&A Advisor No. 1 Global Restructuring Advisor No. 1 Global M&A Fairness Opinion Advisor Over the Past 20 Years ~25% Top 5 Global M&A Advisor 1,400+ Transactions Completed Valued Employee-Owned at More Than $3.0 Trillion Collectively 1,000+ Annual Valuation Engagements Leading Capital Markets Advisor >$6 Billion Market Cap North America Europe and Middle East Asia-Pacific Atlanta Miami Amsterdam Madrid Beijing Sydney >$1 Billion Boston Minneapolis Dubai Milan Hong Kong Tokyo Annual Revenue Chicago New York Frankfurt Paris Singapore Dallas -

Weekend News Summary

Weekend News Summary THE SUNDAY TIMES INDICES THIS MORNING Current (%) 1W% Change Sirius seeks light at end of the tunnel: Work continued at Sirius Value Change* Minerals’ Woodsmith mine in North Yorkshire, even as shares in the FTSE 100 7,415.0 -0.2% 1.1% company fell to new lows amid fears over its future. The company so DAX 30 12,383.8 0.02% -0.7% far has completed just over a mile of a planned 23-mile tunnel to take CAC 40 5,647.2 0.1% -0.9% polyhalite deposits from its site near Whitby to Teesside for export as DJIA** 26,820.3 - -0.4% fertiliser. S&P 500** 2,961.8 - -1.0% Clipper Logistics delivers warning with higher profit: A logistics NASDAQ Comp.** 7,939.6 - -2.2% company that processes online orders for retailers including John Nikkei 225 21,755.8 -0.6% -0.9% Lewis and Boohoo.com has posted a strong increase in annual Hang Seng 40 26,092.3 0.5% -1.8% earnings but warned of potential trading turbulence in the year Shanghai Comp 2,905.2 -0.9% -2.5% ahead. Kospi 2,063.1 0.6% -2.0% Fosun ‘discussing bid’ for Thomas Cook brand name: The Chinese BSE Sensex 38,642.5 -0.5% 2.1% company that was working on a rescue deal for Thomas Cook before S&P/ASX 200 6,688.3 -0.4% -0.2% it collapsed is interested in buying the brand name of the 178-year- Current Values as at 10:15 BST, *%Chg from Friday Close, ** As on Friday Close old tour operator. -

ASLIT Investor Update Presentation

Aberforth Partners LLP Presentation to ASLIT Investors May 2021 14 Melville Street ‐ Edinburgh EH3 7NS Tel 0131 220 0733 ‐ Fax 0131 220 0735 [email protected] ‐ www.aberforth.co.uk Aberforth Partners LLP is authorised and regulated by the Financial Conduct Authority Aberforth Unit Trust Managers Limited is authorised and regulated by the Financial Conduct Authority Aberforth Partners update . Over 30 years of value investing ─ We remain committed to the self‐imposed ceiling on the business ─ AUM capped at c.1.5% of the NSCI (XIC)’s market cap ─ Unchanged ownership structure, collegiate approach, investment focus . A consistent process as the partnership continues its natural evolution ─ Sonya Kim joined as an investment manager on 1 March 2021 ─ The investment managers’ biographies are included in the appendix . Alignment of interests through the managers’ significant holdings . UK Stewardship Code 2020 – updated report available on our website Aberforth Partners LLP 1 Performance – periods to 30 April CAGR 16 months to Total Return %YTD1 YearApril 2021 *Launch **Inception FTSE All‐Share 9.7 25.9 ‐1.1 3.6 3.6 FTSE 250 (XIC) 12.2 41.2 2.7 5.8 5.8 FTSE SmallCap (XIC) 23.4 69.5 25.5 8.2 8.2 NSCI (XIC) 16.9 55.9 11.9 6.9 6.9 ASLIT Total Assets 22.8 55.1 ‐1.9 3.2 2.4 ASLIT ORD NAV 31.5 83.3 ‐2.8 3.4 2.5 ASLIT ORD share price 22.0 85.8 ‐5.4 ‐0.5 ‐ ASLIT ZDP share price 3.2 5.2 2.8 2.9 ‐ *Excludes the effects of launch costs **Inception date for ASLIT was 30/06/2017 . -

Equity Research; Post “Brexit” What Should Work

Equity Research; Post “Brexit” what should work Post “Brexit” what should work Research Report Report Date “There are decades where nothing happens; and there are weeks when decades happen”; Lenin th 19 July 2016 Broadly the dust is now settling. What is the early impact of “Brexit”…so far? Analyst i) Weak sterling “low for longer” due to lower interest rate support, Ravi Lockyer MSc Llb less confidence in the UK’s prospects outside of the EU. We expect Collins Sarri Statham the Bank of England will lower Base Rate to 0.25% on the 4th August Investments Ltd 2016. Finally we see the Brexit “shock” as only slightly slowing UK GDP in 2016. STG has settled well below the long term trend support at US$1.50 (31 year lows). This helps FTSE100 earnings. Source ONS ii) A possible UK constitutional crisis as the government moves towards Article 50 but without a solution for Scotland and Northern Ireland. iii) The drivers of the UK consumer, the property market and wage growth could be more sluggish as Brexit “shock” is absorbed. iv) The UK government is looking at stimulus measures, more infrastructure spending & specific actions for weaker industrial areas. In this currency sensitive environment, broad groupings have emerged:- i) “Winners” - “large cap” UK multi-national beneficiaries of the UK devaluation due to overseas revenue exposure. This list comprises a spectrum of oil & gas majors, pharmaceuticals, HSBC and Standard Chartered, a range of exporters such as BATS, Imperial, Diageo, Rolls Royce. The primary reason is USD or EUR dividends. ii) “Losers” have been UK insurers (due to EU pass-porting risks), housebuilders (UK property concerns), the UK centric retail banks, publicans, airline and travel companies (weaker UK demand for short haul travel), large retailers (costs in Euros/ USD linked currencies). -

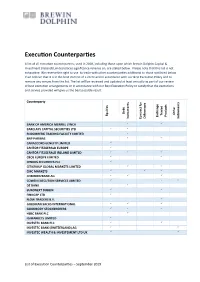

Execu on Counterpar

Execu�on Counterpar�es A list of all execu�on counterpar�es, used in 2018, including those upon which Brewin Dolphin Capital & Investment (Ireland) Limited places significance reliance on, are stated below. Please note that this list is not exhaus�ve. We reserve the right to use to trade with other counterpar�es addi�onal to those not listed below if we believe that it is in the best interest of a client and in accordance with our Best Execu�on Policy and to remove any venues from the list. The list will be reviewed and updated at least annually as part of our review of best execu�on arrangements or in accordance with our Best Execu�on Policy to sa�sfy that the execu�ons and service provided will give us the best possible result. r s Counterparty s s t t o e s e f n n s t c g d r e e e t c t n n e e c � b e a i d h a e r du t r h a e t o rum r rum D c qu O r t t n T x ff E s s i P E o n n D C I I BANK OF AMERICA MERRILL LYNCH BARCLAYS CAPITAL SECURITIES LTD BLOOMBERG TRADING FACILITY LIMITED BNP PARIBAS CANACCORD GENUITY LIMITED CANTOR FITZGERALD EUROPE CANTOR FITZGERALD IRELAND LIMITED CBOE EUROPE LIMITED CENKOS SECURITIES PLC CITIGROUP GLOBAL MARKETS LIMITED CMC MARKETS COMMERZBANK AG COWEN EXECUTION SERVICES LIMITED DZ BANK EURONEXT DUBLIN FINNCAP LTD FLOW TRADERS B.V.