Weekend News Summary

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Retirement Strategy Fund 2060 Description Plan 3S DCP & JRA

Retirement Strategy Fund 2060 June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA ACTIVIA PROPERTIES INC REIT 0.0137% 0.0137% AEON REIT INVESTMENT CORP REIT 0.0195% 0.0195% ALEXANDER + BALDWIN INC REIT 0.0118% 0.0118% ALEXANDRIA REAL ESTATE EQUIT REIT USD.01 0.0585% 0.0585% ALLIANCEBERNSTEIN GOVT STIF SSC FUND 64BA AGIS 587 0.0329% 0.0329% ALLIED PROPERTIES REAL ESTAT REIT 0.0219% 0.0219% AMERICAN CAMPUS COMMUNITIES REIT USD.01 0.0277% 0.0277% AMERICAN HOMES 4 RENT A REIT USD.01 0.0396% 0.0396% AMERICOLD REALTY TRUST REIT USD.01 0.0427% 0.0427% ARMADA HOFFLER PROPERTIES IN REIT USD.01 0.0124% 0.0124% AROUNDTOWN SA COMMON STOCK EUR.01 0.0248% 0.0248% ASSURA PLC REIT GBP.1 0.0319% 0.0319% AUSTRALIAN DOLLAR 0.0061% 0.0061% AZRIELI GROUP LTD COMMON STOCK ILS.1 0.0101% 0.0101% BLUEROCK RESIDENTIAL GROWTH REIT USD.01 0.0102% 0.0102% BOSTON PROPERTIES INC REIT USD.01 0.0580% 0.0580% BRAZILIAN REAL 0.0000% 0.0000% BRIXMOR PROPERTY GROUP INC REIT USD.01 0.0418% 0.0418% CA IMMOBILIEN ANLAGEN AG COMMON STOCK 0.0191% 0.0191% CAMDEN PROPERTY TRUST REIT USD.01 0.0394% 0.0394% CANADIAN DOLLAR 0.0005% 0.0005% CAPITALAND COMMERCIAL TRUST REIT 0.0228% 0.0228% CIFI HOLDINGS GROUP CO LTD COMMON STOCK HKD.1 0.0105% 0.0105% CITY DEVELOPMENTS LTD COMMON STOCK 0.0129% 0.0129% CK ASSET HOLDINGS LTD COMMON STOCK HKD1.0 0.0378% 0.0378% COMFORIA RESIDENTIAL REIT IN REIT 0.0328% 0.0328% COUSINS PROPERTIES INC REIT USD1.0 0.0403% 0.0403% CUBESMART REIT USD.01 0.0359% 0.0359% DAIWA OFFICE INVESTMENT -

Parker Review

Ethnic Diversity Enriching Business Leadership An update report from The Parker Review Sir John Parker The Parker Review Committee 5 February 2020 Principal Sponsor Members of the Steering Committee Chair: Sir John Parker GBE, FREng Co-Chair: David Tyler Contents Members: Dr Doyin Atewologun Sanjay Bhandari Helen Mahy CBE Foreword by Sir John Parker 2 Sir Kenneth Olisa OBE Foreword by the Secretary of State 6 Trevor Phillips OBE Message from EY 8 Tom Shropshire Vision and Mission Statement 10 Yvonne Thompson CBE Professor Susan Vinnicombe CBE Current Profile of FTSE 350 Boards 14 Matthew Percival FRC/Cranfield Research on Ethnic Diversity Reporting 36 Arun Batra OBE Parker Review Recommendations 58 Bilal Raja Kirstie Wright Company Success Stories 62 Closing Word from Sir Jon Thompson 65 Observers Biographies 66 Sanu de Lima, Itiola Durojaiye, Katie Leinweber Appendix — The Directors’ Resource Toolkit 72 Department for Business, Energy & Industrial Strategy Thanks to our contributors during the year and to this report Oliver Cover Alex Diggins Neil Golborne Orla Pettigrew Sonam Patel Zaheer Ahmad MBE Rachel Sadka Simon Feeke Key advisors and contributors to this report: Simon Manterfield Dr Manjari Prashar Dr Fatima Tresh Latika Shah ® At the heart of our success lies the performance 2. Recognising the changes and growing talent of our many great companies, many of them listed pool of ethnically diverse candidates in our in the FTSE 100 and FTSE 250. There is no doubt home and overseas markets which will influence that one reason we have been able to punch recruitment patterns for years to come above our weight as a medium-sized country is the talent and inventiveness of our business leaders Whilst we have made great strides in bringing and our skilled people. -

KPMG Equity Capital Markets Review H1 2018

Equity Capital Markets Half Year Review H1 2018 kpmg.com/uk/equitycapitalmarkets 1 Equity Capital Markets review – H1 2018 H1 2018: Equity Capital Markets review H1 2018 snapshot The first half of 2018 ended strongly generating positive momentum in equity issuance especially in the UK where volumes were up. Overall, however, global ECM volumes were slightly lower versus H2 2017, continuing a trend seen since H1 2017 Overall, global equity issuance was slightly lower in H1 2018 versus H2 2017 Global Europe UK Funds raised Funds raised Funds raised (£000m) (£000m) (£000m) 25 400 125 20 issuance 100 300 15 75 200 10 50 100 5 25 0 Total ECM 0 0 H1 H2 H1 H2 H1 H1 H2 H1 H2 H1 H1 H2 H1 H2 H1 2016 2016 2017 2017 2018 2016 2016 2017 2017 2018 2016 2016 2017 2017 2018 IPOs Right Issues Placings Germany and the UK lead European ECM in H1 Largest 3 European and UK IPOs £20.1bn Siemens Healthineers AG £3.7bn highlights DWS Group GmbH £19.2bn & Co. KGaA £1.2bn Adyen BV European ECM European ECM £4.4bn £834m A very active half year for AIM IPOs beating H1 2017 and offsetting lower Main Market volumes Main Market AIM Funds raised Funds raised (£000m) No. deals (£000m) No. deals 41 IPOs 8 40 1.5 50 16% decrease on H1 2017 6 30 1.2 40 0.9 30 4 20 0.6 20 2 10 0.3 10 £4.3bn Funds Raised 0 0 0.0 0 H1 H2 H1 H2 H1 H1 H2 H1 H2 H1 44% decrease on H1 2017 2016 2016 2017 2017 2018 2016 2016 2017 2017 2018 Deal value Focus # Deals IPO UK IPO Key sectors Strong aftermarket performance of UK IPOs in H1 2018 Financial Services Main Market AIM £1,409m raised (13 deals) -

Herbert Smith Freehills Boosts London Corporate Capability with Ecm Partner Hire

HERBERT SMITH FREEHILLS BOOSTS LONDON CORPORATE CAPABILITY WITH ECM PARTNER HIRE 23 June 2020 | London Firm news Leading global law firm Herbert Smith Freehills has hired Michael Jacobs to join its market leading Global Corporate practice as an Equity Capital Markets partner in London. Michael joins the firm from Allen & Overy where he was a partner. He returns to London from Hong Kong, where he has spent the last three years. Michael is an equity capital markets specialist and has represented listed companies, underwriters and investors on initial public offerings, secondary offerings and other strategic equity transactions. He also regularly advises listed corporates on the equity capital markets implications of public and private M&A transactions and restructurings. Prior to relocating to Hong Kong, Michael acted on the initial public offerings of Worldpay, Virgin Money, Hastings Insurance, Neinor Homes and The Gym Group and secondary capital raises by companies including Great Portland Estates, Sirius Minerals, Ophir Energy, Capitec Bank, GKN, Vedanta Energy and the recapitalisation and consensual bail in of the Co- operative Bank. Michael is recommended by Legal 500 for equity capital markets transactions. Michael also has considerable experience across mainstream corporate finance transactions, including public and private M&A, board-level corporate advisory work, restructurings and regulatory advice for clients including advising on cross-border deals which span a wide range of sectors, including financial institutions, fintech and growth capital. His M&A experience includes advising on Banco de Sabadell’s takeover of TSB Banking Group and the acquisition of Northern Rock by Virgin Money, as well as on transactions for Ping An, Go-Jek, Discovery Capital and Roivant Sciences during his time in Hong Kong. -

Finn-Ancial Times Finncap Financials & Insurance Quarterly Sector Note

finn-ancial Times finnCap Financials & Insurance quarterly sector note Q3 2020 | Issue 9 Highlights this quarter: Elevated uncertainty and volatility have been hallmarks of the last 18 months, with Brexit, the UK General Election and more recently COVID-19 all contributing to the challenges that face investors wishing to carve out solid and stable returns amid these ‘unprecedented’ times. With this is mind, and simulating finnCap’s proven Slide Rule methodology, we found the highest quality and lowest value stocks across the financials space, assessing how the make-up of these lists changed over the period January 2019 to July 2020, tracking indexed share price performance over the period as well as movements in P/E and EV/EBIT valuations. The top quartile list of Quality companies outperformed both the Value list and the FTSE All Share by rising +2.5% over the period versus -5.4% for the All Share and -14.3% for Value stocks. Furthermore, the Quality list had protection on the downside in the market crash between February and March 2020, and accelerated faster amid the market rally between late March and July 2020. From high to low (January to March), Quality moved -36.3% against the Value list at -45.5%, while a move off the lows to July was +37.4% for Quality and +34.0% for Value. There was some crossover between the Quality and Value lists, with 7 companies of the top quartile (16 companies in total) appearing in both the Quality and Value lists. This meant that a) investors could capture what we call ‘Quality at Value’ (i.e. -

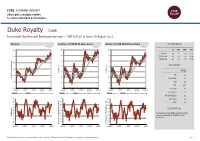

FTSE Factsheet

FTSE COMPANY REPORT Share price analysis relative to sector and index performance Duke Royalty DUKE Investment Banking and Brokerage Services — GBP 0.4125 at close 10 August 2021 Absolute Relative to FTSE UK All-Share Sector Relative to FTSE UK All-Share Index PERFORMANCE 10-Aug-2021 10-Aug-2021 10-Aug-2021 0.45 140 140 1D WTD MTD YTD Absolute -2.4 -1.2 -1.8 35.2 130 130 0.4 Rel.Sector -2.4 -0.5 -3.6 25.9 Rel.Market -2.8 -1.7 -3.7 20.9 120 120 0.35 VALUATION 110 110 0.3 Trailing 100 100 Relative Price Relative Price Relative 0.25 PE -ve Absolute Price (local (local currency) AbsolutePrice 90 90 EV/EBITDA -ve 0.2 80 80 PB 2.0 PCF 28.1 0.15 70 70 Div Yield 4.6 Aug-2020 Nov-2020 Feb-2021 May-2021 Aug-2021 Aug-2020 Nov-2020 Feb-2021 May-2021 Aug-2021 Aug-2020 Nov-2020 Feb-2021 May-2021 Aug-2021 Price/Sales -ve Absolute Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Net Debt/Equity 0.2 90 90 90 Div Payout -ve 80 80 80 ROE -ve 70 70 70 Share Index) Share Share Sector) Share - 60 - 60 60 DESCRIPTION 50 50 50 40 40 The Company is a globally focused investment 40 RSI RSI (Absolute) 30 30 company specialising in diversified royalty investment. -

Morningstar Report

Report as of 25 Sep 2021 Aberdeen Standard Equity Inc Trust plc , (GB0006039597) Morningstar Rating™ Peer Group Classification Last Close Last Actual NAV (23 Sep 2021) Discount Estimated Nav QQ Morningstar IT UK Equity 345.00 379.95 -9.20 379.95 Income Investment Objective Performance The fund aims to provide shareholders with an above 169 average income while also providing real growth in 146 capital and income. It will invest in a diversified 123 portfolio consisting mainly of quoted UK equities 100 which will normally comprise between 50 and 70 77 individual equity holdings. 54 2016 2017 2018 2019 2020 2021-08 -10.88 23.83 -12.55 9.46 -19.70 19.51 Fund 16.75 13.10 -9.47 19.17 -9.82 14.66 Benchmark 8.76 10.73 -10.56 18.95 -12.56 15.52 Category Management Fee Summary Management fee of 0.65% p.a. of NA on the first GBP 175m and 0.55% thereafter. No performance fee. Contract terminable on notice period of 6 months. Portfolio 31/08/2021 Asset Allocation % Long Short Net Equity Style Box™ Mkt Cap % Fund America Europe Asia Large Size Stocks 113.11 0.00 113.11 Giant 17.55 Bonds 0.00 0.00 0.00 Mid Large 18.27 Cash 0.00 13.11 -13.11 Medium 22.91 Other 0.00 0.00 0.00 Small Small 24.92 Value Blend Growth Micro 16.35 Style Average Mkt Fund Cap (Mil) Ave Mkt Cap GBP 4,115.7 <25 25-50 50-75 >75 7 Top Holdings Stock Sector Weightings % Fund World Regions % Fund Name Sector % hCyclical 66.41 Americas 2.36 BHP Group PLC r 4.54 rBasic Materials 13.25 United States 2.36 Rio Tinto PLC r 4.30 tConsumer Cyclical 14.81 Canada 0.00 CMC Markets PLC y 3.99 -

Fintech Monthly Market Update | July 2021

Fintech Monthly Market Update JULY 2021 EDITION Leading Independent Advisory Firm Houlihan Lokey is the trusted advisor to more top decision-makers than any other independent global investment bank. Corporate Finance Financial Restructuring Financial and Valuation Advisory 2020 M&A Advisory Rankings 2020 Global Distressed Debt & Bankruptcy 2001 to 2020 Global M&A Fairness All U.S. Transactions Restructuring Rankings Advisory Rankings Advisor Deals Advisor Deals Advisor Deals 1,500+ 1 Houlihan Lokey 210 1 Houlihan Lokey 106 1 Houlihan Lokey 956 2 JP Morgan 876 Employees 2 Goldman Sachs & Co 172 2 PJT Partners Inc 63 3 JP Morgan 132 3 Lazard 50 3 Duff & Phelps 802 4 Evercore Partners 126 4 Rothschild & Co 46 4 Morgan Stanley 599 23 5 Morgan Stanley 123 5 Moelis & Co 39 5 BofA Securities Inc 542 Refinitiv (formerly known as Thomson Reuters). Announced Locations Source: Refinitiv (formerly known as Thomson Reuters) Source: Refinitiv (formerly known as Thomson Reuters) or completed transactions. No. 1 U.S. M&A Advisor No. 1 Global Restructuring Advisor No. 1 Global M&A Fairness Opinion Advisor Over the Past 20 Years ~25% Top 5 Global M&A Advisor 1,400+ Transactions Completed Valued Employee-Owned at More Than $3.0 Trillion Collectively 1,000+ Annual Valuation Engagements Leading Capital Markets Advisor >$6 Billion Market Cap North America Europe and Middle East Asia-Pacific Atlanta Miami Amsterdam Madrid Beijing Sydney >$1 Billion Boston Minneapolis Dubai Milan Hong Kong Tokyo Annual Revenue Chicago New York Frankfurt Paris Singapore Dallas -

UK Equity Capital Markets Update – Winter 2019

Stimulating hope Equity Capital Markets update Winter 2019 Financial Advisory This Equity Capital Markets update contains commentary on: recent UK stockmarket performance; levels of equity market issuance and macroeconomic considerations; how to select IPO advisers; and a case study of Deloitte’s involvement in the recent IPO of Helios Towers. Stimulating hope | Contents Contents Welcome 04 Market performance 06 UK IPOs in 2019 10 Equity issuance and macroeconomic considerations 12 ECM hot topic: Selecting IPO advisers 18 Case study: IPO of Helios Towers on London Stock Exchange 23 Deloitte Equity Capital Markets 26 About this report: This report contains data sourced from Deloitte’s Q3 2019 CFO Survey, Deloitte’s Autumn 2019 European CFO survey, FactSet, Dealogic, company admission documents, press releases and London Stock Exchange statistics. Unless stated otherwise, IPO and secondary fundraisings relate to completed transactions by companies admitted to either the Main Market or AIM and all market data is as at 14 November 2019. The issuance of GDRs and convertibles have also been excluded. All commentary is provided by Deloitte ECM Partners. © 2019 Deloitte LLP. All rights reserved. 3 Stimulating hope| Welcome Welcome to Deloitte’s 7th Equity Capital Markets update Amidst continuing uncertainty, global equity markets have delivered strong gains so far in 2019. US and certain European indices are currently trading at or around all-time highs, supported by more accommodative monetary policy and central bank adjustments in the face of economic data continuing to point to a deceleration in global economic growth. The FTSE 100 is 8.4% higher than at the start of this year and, while investors still await a final resolution of the UK’s exit from the EU, the more domestically focused FTSE 250 similarly has performed strongly in 2019. -

Your Guide Directors' Remuneration in FTSE 250 Companies

Your guide Directors’ remuneration in FTSE 250 companies The Deloitte Academy: Promoting excellence in the boardroom October 2018 Contents Overview from Mitul Shah 1 1. Introduction 4 2. Main findings 8 3. The current environment 12 4. Salary 32 5. Annual bonus plans 40 6. Long term incentive plans 52 7. Total compensation 66 8. Malus and clawback 70 9. Pensions 74 10. Exit and recruitment policy 78 11. Shareholding 82 12. Non-executive directors’ fees 88 Appendix 1 – Useful websites 96 Appendix 2 – Sample composition 97 Appendix 3 – Methodology 100 Your guide | Directors’ remuneration in FTSE 250 companies Overview from Mitul Shah It has been a year since the Government announced its intention to implement a package of corporate governance reforms designed to “maintain the UK’s reputation for being a ‘dependable and confident place in which to do business’1, and in recent months we have seen details of how these will be effected. The new UK Corporate Governance Code, to take effect for accounting periods beginning on or after 1 January 2019, includes some far reaching changes, and the year ahead will be a period of review and change for many companies. Remuneration committees must look at how best to adapt to an expanded remit around workforce remuneration, as well as a greater focus on how judgment is used to ensure that pay outcomes are justified and supported by performance. Against this backdrop, 2018 has been a mixed year in the FTSE 250 executive pay environment. In terms of pay outcomes, the picture is relatively stable. Overall pay levels have fallen for FTSE 250 chief executives and we have seen continued momentum in companies adopting executive alignment features such as holding periods, as well as strengthening shareholding guidelines for executives. -

ASLIT Investor Update Presentation

Aberforth Partners LLP Presentation to ASLIT Investors May 2021 14 Melville Street ‐ Edinburgh EH3 7NS Tel 0131 220 0733 ‐ Fax 0131 220 0735 [email protected] ‐ www.aberforth.co.uk Aberforth Partners LLP is authorised and regulated by the Financial Conduct Authority Aberforth Unit Trust Managers Limited is authorised and regulated by the Financial Conduct Authority Aberforth Partners update . Over 30 years of value investing ─ We remain committed to the self‐imposed ceiling on the business ─ AUM capped at c.1.5% of the NSCI (XIC)’s market cap ─ Unchanged ownership structure, collegiate approach, investment focus . A consistent process as the partnership continues its natural evolution ─ Sonya Kim joined as an investment manager on 1 March 2021 ─ The investment managers’ biographies are included in the appendix . Alignment of interests through the managers’ significant holdings . UK Stewardship Code 2020 – updated report available on our website Aberforth Partners LLP 1 Performance – periods to 30 April CAGR 16 months to Total Return %YTD1 YearApril 2021 *Launch **Inception FTSE All‐Share 9.7 25.9 ‐1.1 3.6 3.6 FTSE 250 (XIC) 12.2 41.2 2.7 5.8 5.8 FTSE SmallCap (XIC) 23.4 69.5 25.5 8.2 8.2 NSCI (XIC) 16.9 55.9 11.9 6.9 6.9 ASLIT Total Assets 22.8 55.1 ‐1.9 3.2 2.4 ASLIT ORD NAV 31.5 83.3 ‐2.8 3.4 2.5 ASLIT ORD share price 22.0 85.8 ‐5.4 ‐0.5 ‐ ASLIT ZDP share price 3.2 5.2 2.8 2.9 ‐ *Excludes the effects of launch costs **Inception date for ASLIT was 30/06/2017 . -

The IPO Review EQ Boardroom, Equiniti the IPO REVIEW

The IPO Review EQ Boardroom, Equiniti THE IPO REVIEW Introduction “I am delighted to present our IPO round-up for 2018. Decisions on whether or not to list had to be taken against a political as well as a financial context, especially by UK boards. With concerns about disruptions to trade, investors have been apprehensive, especially in the latter part of the year. However, we have also seen outstandingly successful listings which have captured investors’ imaginations and turned well-served customers into enthusiastic shareholders. Such successes demonstrate that sophisticated and liquid markets like London cannot be distracted from opportunities to invest in strong and forward-looking enterprises. Overseas companies looking to list are coming to London in ever greater numbers, attracted by our ready capital, transparency and regulatory standards. In this way London continues to help power the global economy and in turn we at Equiniti are proud to help power the London market. As the largest provider of shareholder services in the UK we count the majority of FTSE 100 companies as clients and with our record of helping companies to list, we look forward to swelling their ranks.” Paul Matthews CEO, EQ Boardroom 02 THE IPO REVIEW Contents 02 Introduction 04 Executive Summary 05 Sector Analysis Highlights of Main 06 Market Listings 07 Highlights of AIM Listings The Battle to Attract 08 International Tech IPOs 09 2018 vs 2017 10 Outlook 2019 03 THE IPO REVIEW Executive Summary With global free trade under Stout-hearted retailers also listed Overall the year was down on pressure and the meaning in the year; ignoring the script 2017 in both the number of of Brexit foggier than ever, and raising money to expand listings and the money raised.