OPEC and Non-OPEC Crude Oil Production Agreement: Compliance Status

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Unconventional Gas and Oil in North America Page 1 of 24

Unconventional gas and oil in North America This publication aims to provide insight into the impacts of the North American 'shale revolution' on US energy markets and global energy flows. The main economic, environmental and climate impacts are highlighted. Although the North American experience can serve as a model for shale gas and tight oil development elsewhere, the document does not explicitly address the potential of other regions. Manuscript completed in June 2014. Disclaimer and copyright This publication does not necessarily represent the views of the author or the European Parliament. Reproduction and translation of this document for non-commercial purposes are authorised, provided the source is acknowledged and the publisher is given prior notice and sent a copy. © European Union, 2014. Photo credits: © Trueffelpix / Fotolia (cover page), © bilderzwerg / Fotolia (figure 2) [email protected] http://www.eprs.ep.parl.union.eu (intranet) http://www.europarl.europa.eu/thinktank (internet) http://epthinktank.eu (blog) Unconventional gas and oil in North America Page 1 of 24 EXECUTIVE SUMMARY The 'shale revolution' Over the past decade, the United States and Canada have experienced spectacular growth in the production of unconventional fossil fuels, notably shale gas and tight oil, thanks to technological innovations such as horizontal drilling and hydraulic fracturing (fracking). Economic impacts This new supply of energy has led to falling gas prices and a reduction of energy imports. Low gas prices have benefitted households and industry, especially steel production, fertilisers, plastics and basic petrochemicals. The production of tight oil is costly, so that a high oil price is required to make it economically viable. -

Monthly Report on Petroleum Developments in the World Markets February 2020

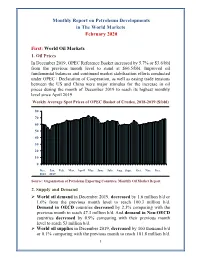

Monthly Report on Petroleum Developments in The World Markets February 2020 First: World Oil Markets 1. Oil Prices In December 2019, OPEC Reference Basket increased by 5.7% or $3.6/bbl from the previous month level to stand at $66.5/bbl. Improved oil fundamental balances and continued market stabilization efforts conducted under OPEC+ Declaration of Cooperation, as well as easing trade tensions between the US and China were major stimulus for the increase in oil prices during the month of December 2019 to reach its highest monthly level since April 2019. Weekly Average Spot Prices of OPEC Basket of Crudes, 2018-2019 ($/bbl) 80 70 60 50 40 30 20 10 0 Dec. Jan. Feb. Mar. April May June July Aug. Sept. Oct. Nov. Dec. 2018 2019 Source: Organization of Petroleum Exporting Countries, Monthly Oil Market Report. 2. Supply and Demand World oil demand in December 2019, decreased by 1.6 million b/d or 1.6% from the previous month level to reach 100.3 million b/d. Demand in OECD countries decreased by 2.3% comparing with the previous month to reach 47.3 million b/d. And demand in Non-OECD countries decreased by 0.9% comparing with their previous month level to reach 53 million b/d. World oil supplies in December 2019, decreased by 100 thousand b/d or 0.1% comparing with the previous month to reach 101.8 million b/d. 1 Non-OPEC supplies remained stable at the same previous month level of 67.2 million b/d. Whereas preliminary estimates show that OPEC crude oil and NGLs/condensates total supplies decreased by 0.6% comparing with the previous month to reach 34.5 million b/d. -

Peak Oil Demand and Long-Run Oil Prices

January 2018 Peak Oil Demand and Long-Run Oil Prices Abstract The prospect that global oil demand will gradually slow and eventually peak has created a cottage industry of executives and commentators trying to predict the point at which demand will peak. In this Energy Insight, we argue that this focus seems misplaced. The date at which oil demand will stop growing is highly uncertain and small changes in assumptions can lead to vastly different estimates. More importantly, there is little reason to believe that once it does peak, that oil demand will fall sharply. The world is likely to demand large quantities of oil for many decades to come. Rather, the significance of peak oil is that it signals a shift in paradigm – from an age of (perceived) scarcity to an age of abundance – and with it is likely to herald a shift to a more competitive market environment. This change in paradigm is also likely to pose material challenges for oil producing economies as they try both to ensure that their oil is produced and consumed, and at the same time diversify their economies fit for a world in which they can no longer rely on oil revenues to provide their main source of revenue for the indefinite future. We argue that the extent and pace of this diversification is likely to have an important bearing on oil prices over the next 20 or 30 years. It seems likely that many low-cost producers will delay the pace at which they adopt a more competitive “higher volume, lower price” strategy until they have made material progress in reforming their economies. -

UCS TIGHT OIL.Indd

The Truth about Tight Oil Don Anair Amine Mahmassani Methane from Unconventional Oil Extraction Poses Significant Climate Risks July 2013 Since 2010, “tight oil”—oil extracted from hard- to-access deposits using horizontal drilling and hydraulic fracturing (fracking)—has dramatically changed the US oil industry, reversing decades of declining domestic oil production and reducing US oil imports (EIA 2015a). In 2015, tight oil comprised more than half of US oil produc- 10,000 feet to reach sedimentary rock and then sideways or tion, bringing total production close to 10 million barrels per horizontally for a mile or more. Next, a mixture of water, day—a peak not seen since the 1970s (see Figure 1). But this sand, and chemicals is pumped at high pressure into the wells sudden expansion has also led to an increase of global warm- to create fractures in the rocks, which frees the oil and gas ing emissions due, in large part, to methane—an extremely potent heat-trapping gas that is found in larger concentra- tions in tight oil regions. Although most of the emissions associated with the con- sumption of oil are a result of burning the finished fuel (for example, in a car or truck), the emissions from extracting, transporting, and refining oil add, on average, 35 percent to a fuel’s life cycle emissions. These “upstream” emissions can- not be overlooked when seeking to mitigate emissions from oil use overall. Recent scientific evidence highlights major gaps in our knowledge of these large and rising sources of global warming pollution (Caulton et al. -

Welcome to the 11Th Edition of Energy Perspectives! This Is An

Welcome to the 11th edition of Energy Perspectives! This is an independent report that informs Equinor’s strategy and offers a fact-based contribution to the energy transition debate. This year’s edition is an update of the edition from November last year, and with a lot happening on the global arena the last 6 months, there is a lot to consider when looking 30 years ahead. As always, this report and its data and conclusions would be impossible without the excellent work of many of my colleagues, to whom I extend my appreciation and gratitude. You are the best! 1 Covid19 is not over. In a global perspective, we are still dealing with its impact and the enormous effects it has on people, societies, economies, and markets. We are not through it yet. And we might have to live with recurring infection spikes, especially in parts of the world that do not get sufficient access to vaccines. Recurring lockdowns entailed that energy demand, and in particular oil demand due to its use as a transport fuel, was hit hard. Recovery is in the making, and faster than many feared, but oil demand, as an example, is still not back to pre-Covid19-levels. The map shows how the pandemic has affected economies across the globe, with almost all countries pink or red, that is, with negative economic development. Industrialised countries are on their way out of recession while disabling the virus, but the uncertainty is still high in many emerging economies. 2 We are seeing signs of recovery. Thanks to the development and rollout of vaccines and massive public spending to stimulate demand, there are signs that the situation is being brought under control so that we can live with the virus more like we do with normal flus. -

U.S.-Canada Cross- Border Petroleum Trade

U.S.-Canada Cross- Border Petroleum Trade: An Assessment of Energy Security and Economic Benefits March 2021 Submitted to: American Petroleum Institute 200 Massachusetts Ave NW Suite 1100, Washington, DC 20001 Submitted by: Kevin DeCorla-Souza ICF Resources L.L.C. 9300 Lee Hwy Fairfax, VA 22031 U.S.-Canada Cross-Border Petroleum Trade: An Assessment of Energy Security and Economic Benefits This report was commissioned by the American Petroleum Institute (API) 2 U.S.-Canada Cross-Border Petroleum Trade: An Assessment of Energy Security and Economic Benefits Table of Contents I. Executive Summary ...................................................................................................... 4 II. Introduction ................................................................................................................... 6 III. Overview of U.S.-Canada Petroleum Trade ................................................................. 7 U.S.-Canada Petroleum Trade Volumes Have Surged ........................................................... 7 Petroleum Is a Major Component of Total U.S.-Canada Bilateral Trade ................................. 8 IV. North American Oil Production and Refining Markets Integration ...........................10 U.S.-Canada Oil Trade Reduces North American Dependence on Overseas Crude Oil Imports ..................................................................................................................................10 Cross-Border Pipelines Facilitate U.S.-Canada Oil Market Integration...................................14 -

Market Indicators As at End*: August-2020

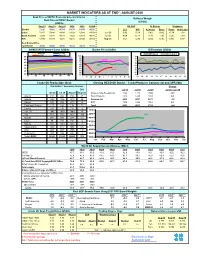

MARKET INDICATORS AS AT END*: AUGUST-2020 Spot Price of OPEC Basket & Selected Crudes Refiners' Margin Real Price of OPEC Basket (US$/b) (US$/b) Aug-18 Aug-19 Aug-20 2018 2019 2020# US Gulf N. Europe Singapore Basket 72.26 59.62 45.19 69.78 64.04 40.50 LLS WTI A. Heavy Brent Oman Arab Light Dubai 72.47 58.88 43.89 69.68 63.48 41.54 Jun-20 3.92 5.19 0.42 0.42 -0.74 1.02 North Sea Dtd 72.64 58.83 44.79 71.22 64.19 40.88 Jul-20 4.64 6.13 -1.86 1.30 1.26 1.99 WTI 67.99 54.84 42.36 65.16 57.02 38.15 Aug-20 3.67 5.30 -2.05 0.16 0.86 0.87 Real Basket Price Jun01=100 46.86 39.02 28.30 35.22 44.73 26.19 NYMEX WTI Forward Curve (US$/b) Basket Price (US$/b) Differentials (US$/b) May-20 Jun-20 WTI-Brent Brent-Dubai Jul-20 Aug-20 50 100 3 90 2 45 2018 80 1 70 40 0 60 35 2019 -1 50 30 40 -2 2020 -3 25 30 20 -4 20 10 -5 1M 3M 5M 7M 9M 11M J F M A M J J A S O N D 03 05 07 11 13 17 19 21 25 27 31 Crude Oil Production (tb/d) Closing OECD Oil Stocks - Crude/Products Commercial and SPR (Mb) Crude Oil Production (Tb/d) Production: Secondary Sources Change Diff. -

Worldwide Operations and Locations March 2019

Worldwide Operations and Locations March 2019 Kuparuk Barents Alpine Prudhoe Bay Sea Aasta Hansteen UNITED STATES – ALASKA Heidrun Norwegian Trans-Alaska Pipeline System (TAPS) CANADA Sea NORWAY Clair Alvheim Anchorage Britannia Aberdeen Stavanger Surmont UNITED KINGDOM J-Area Greater Ekosk Area Montney North Sea Calgary NORTH AMERICA London Bakken East Irish Sea EUROPE Pacic Ocean UNITED STATES – Wyoming/ LOWER 48 Caspian Uinta Basin Sea Niobrara Beijing CHINA Bartlesville JAPAN Anadarko Basin Penglai Tripoli Houston Atlantic Ocean MIDDLE EAST Permian Basin LIBYA ASIA GOM Eagle Ford Doha Gulf of Mexico Qatargas 3 Pacic Ocean QATAR Panyu CAMBODIA South China Sea Exploration MALAYSIA Block G Production Block J KBB AFRICA Natuna Sea Exploration and Production COLOMBIA Indian Ocean Kuala Lumpur Major Pipeline Corridor SINGAPORE Key Development or Program INDONESIA Jakarta Java Sea Headquarters Bayu-Undan/Darwin LNG Key Oce Location SOUTH TIMOR-LESTE Timor Sea AMERICA Athena AUSTRALIA Australia Pacic LNG Brisbane CHILE Perth World’s Largest Independent E&P Company ConocoPhillips is the world’s largest independent exploration and production (E&P) company based on production and proved reserves. 2018 Production* 2018 Proved Reserves 2018 Production* 2018 Proved Reserves by region by region 1,283 MBOED 5.3 BBOE 2018 Resources The company explores for, produces, transports and markets crude oil, 40 BBOE bitumen, natural gas, natural gas liquids and liqueed natural gas on a 5% 34% Canada 22% Alaska 20% worldwide basis. Key focus areas include safely operating producing 15% Natural Gas 8% Non OECD Alaska 23% assets, executing major development projects and exploring for new North American Asia Pacic & Natural Gas resources in promising areas. -

Future Trends in Global Oil and Gas Exploration Dr

Future Trends in Global Oil and Gas Exploration Dr. Michael C. Daly Executive Vice President Exploration, BP plc Imperial College 23 September Thank you for the invitation to speak at your conference celebrating the centenary of Oil Technology at Imperial College. It is an honour and great pleasure to be here. I have been asked to discuss the future trends of global oil and gas exploration, a subject I am deeply passionate about and have lived with for over 30 years now. Of course many factors will influence the future of exploration. However, the fundamentals of resource quality, technology and 1 geopolitics seem paramount to me. Today I will largely confine my remarks to the first of these, resource quality, which I believe to be the fundamental driver. Exploration trends will follow the industry’s perception of the “next best resource base” to explore and develop, which incorporates both the scale and quality of resource and the cost of its development. Today we are some 40 years into the deepwater era. And although we are perhaps half way through it in finding terms, deepwater exploration is a trend that will be with us for some time yet. Deepwater will likely be followed by two very different trends, both of which are beginning to emerge. Firstly, a move to the unexplored arctic frontier of ice bound continental shelves; and secondly to a re- 2 exploration of the onshore and shallow waters of the world with new images, new technology and occasionally new ideas. But before getting into this in detail, we need to understand the context of what there is to find, where it might be, and what it will take to find it. -

NEWS RELEASE June 15, 2021

925 North Eldridge Parkway Houston, TX 77079 Media Relations: 281-293-1149 www.conocophillips.com/media NEWS RELEASE June 15, 2021 ConocoPhillips to Host Market Update June 30 HOUSTON – ConocoPhillips (NYSE: COP) will host a virtual market update on Wednesday, June 30 beginning at 9:00 a.m. Central time. The meeting will feature presentations by ConocoPhillips executives, including Chairman and Chief Executive Officer Ryan Lance. A live webcast of the meeting will be made available on the ConocoPhillips Investor Relations website, www.conocophillips.com/investor. The event will be archived and available for replay later that day. The presentation, along with a transcript, will also be available on the Investor Relations website. --- # # # --- About ConocoPhillips Headquartered in Houston, Texas, ConocoPhillips had operations and activities in 15 countries, $84 billion of total assets, and approximately 10,300 employees at March 31, 2021. Production excluding Libya averaged 1,488 MBOED for the three months ended March 31, 2021, and proved reserves were 4.5 BBOE as of Dec. 31, 2020. For more information, go to www.conocophillips.com. Contacts Media Dennis Nuss 281-293-1149 [email protected] Investor Relations 281-293-5000 [email protected] CAUTIONARY STATEMENT FOR THE PURPOSES OF THE "SAFE HARBOR" PROVISIONS OF THE PRIVATE SECURITIES LITIGATION REFORM ACT OF 1995 This news release contains forward-looking statements as defined under the federal securities laws. Forward-looking statements relate to future events and anticipated results of operations, business strategies, and other aspects of our operations or operating results. Words and phrases such as “anticipate," “estimate,” “believe,” “budget,” “continue,” “could,” “intend,” “may,” “plan,” “potential,” “predict," “seek,” “should,” “will,” “would,” “expect,” “objective,” “projection,” “forecast,” “goal,” “guidance,” “outlook,” “effort,” “target” and other similar words can be used to identify forward-looking statements. -

The Economic Impact of Oil Prices by Rurik Krymm

The Economic Impact of Oil Prices by Rurik Krymm During the last three months of 1973, the tax-paid costs of typical grades of crude petroleum in the main producing areas of the world, around the Persian Gulf, were roughly quadrupled, rising for typical Iranian and Arabian Ugh t crudes from about $1.85 per barrel in September 1973 to more than $7.00 by 1 January 1974, or from approximately $13.30 to more than $50.00per ton. Since the cost of production represents an insignificantly small fraction of the new cost level (less than 2%) and subject to complex adjustments reflecting varying qualities of crude oils and advantages of geographical location, the producing countries may expect to receive a minimum average revenue of $50.00 per ton of crude oil produced on their territory instead of $12.50. If we ignore the purchases which carried the prices of relatively small amounts of oil to the $100-$ 150range, this figure of $50.00per ton with future adjustments for inflation represents a probable guide line for future cost estimates. The change affects exports of close to 1.4 billion tons of oil and consequently involves an immediate shift of financial resources of close to 60 billion dollars per year from the oil-consuming to the oil-producing countries. Tables 1, 2 and 3 give an idea of the distribution of this burden by main geographical regions and of its possible evolution over the next seven years. The figures involved are so large that comparisons have been made by some authors with the reparations proposals advanced by the Allies at the end of the First World War. -

OPEC Annual Statistical Bulletin 2019 1 Contents

2019 OPEC Annual Statistical Bulletin Organization of the Petroleum Exporting Countries 1965 – 2019 th edition 54 Team for the preparation of the OPEC Annual Statistical Bulletin Secretary General Editorial Team Chairman of the Editorial Board Head, Public Relations and Information Department Mohammad Sanusi Barkindo Hasan Hafidh Director, Research Division Editor Ayed S. Al-Qahtani Maureen MacNeill, Mathew Quinn Project Leader Coordinator, Design and Production Head, Data Services Department Carola Bayer Adedapo Odulaja Senior Production Assistant Coordinator, Statistics Team Diana Lavnick Hossein Hassani Graphic Designer Statistics Team Tara Starnegg Pantelis Christodoulides, Klaus Stöger, Mohammad Sattar, Mihni Mihnev, Justinas Pelenis, Ksenia Gutman Coordinator, IT Development Team Mohamed Mekerba IT Development Team Vedran Hrgovcic, Zairul Arifin Online Annual Statistical Bulletin 2019: asb.opec.org Download now: Smart App for OPEC Annual Statistical Bulletin iOS Android Questions on data Data queries: [email protected]. Advertising The OPEC Annual Statistical Bulletin now accepts advertising. For details, please contact the Head, PR and Information Department, at the following address: Organization of the Petroleum Exporting Countries Helferstorferstrasse 17, A-1010 Vienna, Austria Tel: +43 1 211 12/0 Fax: +43 1 216 43 20 Advertising: [email protected] Website: www.opec.org Photographs Courtesy OPEC. © 2019 Organization of the Petroleum Exporting Countries ISSN 0475-0608 Contents Foreword 5 Key messages 6 Tables Page Page Section