The History of Handelsbanken

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

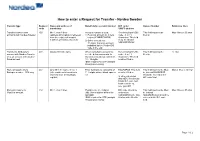

How to Enter a Request for Transfer - Nordea Sweden

How to enter a Request for Transfer - Nordea Sweden Transfer type Request Name and address of Beneficiary’s account number BIC code / Name of banker Reference lines code beneficiary SWIFT address Transfer between own 400 Min 1, max 4 lines Account number is used: Receiving bank’s BIC This field must not be Max 4 lines x 35 char accounts with Nordea Sweden (address information is retrieved 1) Personal account no = pers code - 8 or 11 filled in from the register of account reg no (YYMMDDXXXX) characters. This field numbers of Nordea, Sweden) 2) Other account nos = must be filled in 11 digits. Currency account NDEASESSXXX indicated by the 3-letter ISO code in the end Transfer to third party’s 401 Always fill in the name When using bank account no., Receiving bank’s BIC This field must not be 12 char account with Nordea Sweden see the below comments. In code - 8 or 11 filled in or to an account with another Sweden account nos consist of characters. This field Swedish bank 10 - 15 digits. must be filled in IBAN required for STP (straight through processing) Domestic payments to 402 Only fill in the name in line 1 Enter bankgiro no consisting of BGABSESS. This field This field must not be filled Max 4 lines x 35 char Bankgiro number - SEK only (other address information is 7 - 8 digits without blank spaces must be filled in. in. Instead BGABSESS retrieved from the Bankgiro etc should be entered in the register) In other currencies BIC code field than SEK: Receivning banks BIC code and bank account no. -

Chronology, 1963–89

Chronology, 1963–89 This chronology covers key political and economic developments in the quarter century that saw the transformation of the Euromarkets into the world’s foremost financial markets. It also identifies milestones in the evolu- tion of Orion; transactions mentioned are those which were the first or the largest of their type or otherwise noteworthy. The tables and graphs present key financial and economic data of the era. Details of Orion’s financial his- tory are to be found in Appendix IV. Abbreviations: Chase (Chase Manhattan Bank), Royal (Royal Bank of Canada), NatPro (National Provincial Bank), Westminster (Westminster Bank), NatWest (National Westminster Bank), WestLB (Westdeutsche Landesbank Girozentrale), Mitsubishi (Mitsubishi Bank) and Orion (for Orion Bank, Orion Termbank, Orion Royal Bank and subsidiaries). Under Orion financings: ‘loans’ are syndicated loans, NIFs, RUFs etc.; ‘bonds’ are public issues, private placements, FRNs, FRCDs and other secu- rities, lead managed, co-managed, managed or advised by Orion. New loan transactions and new bond transactions are intended to show the range of Orion’s client base and refer to clients not previously mentioned. The word ‘subsequently’ in brackets indicates subsequent transactions of the same type and for the same client. Transaction amounts expressed in US dollars some- times include non-dollar transactions, converted at the prevailing rates of exchange. 1963 Global events Feb Canadian Conservative government falls. Apr Lester Pearson Premier. Mar China and Pakistan settle border dispute. May Jomo Kenyatta Premier of Kenya. Organization of African Unity formed, after widespread decolonization. Jun Election of Pope Paul VI. Aug Test Ban Take Your Partners Treaty. -

SEB Fund 1 AR 31122019 Final Post BM

Annual Report SEB Fund 1 Status: 31 December 2019 R.C.S K 49 Notice The sole legally binding basis for the purchase of units of the Fund described in this report is the latest valid Sales Prospectus with its terms of contract. Table of Contents Page Additional Information to the Investors in Germany 2 Organisation 3 General Information 5 Management Report 9 Schedule of Investments: SEB Fund 1 - SEB Asset Selection Fund 10 SEB Fund 1 - SEB Europe Index Fund 14 SEB Fund 1 - SEB Global Fund 24 SEB Fund 1 - SEB Global Chance / Risk Fund 33 SEB Fund 1 - SEB Norway Focus Fund 39 SEB Fund 1 - SEB Sustainability Fund Europe 41 SEB Fund 1 - SEB Sustainability Nordic Fund 46 SEB Fund 1 - SEB US All Cap 48 Combined Statement of Operations 50 Combined Statement of Changes in Net Assets 54 Combined Statement of Net Assets 58 Statistical Information 62 Notes to the Financial Statements 74 Audit Report 81 Risk Disclosure (unaudited) 84 Remuneration Disclosure (unaudited) 86 1 Additional Information to the Investors in Germany As at 31 December 2019 Units in circulation: The following Sub-Funds are publicly approved for distribution in Germany: • SEB Fund 1 - SEB Asset Selection Fund • SEB Fund 1 - SEB Global Fund • SEB Fund 1 - SEB Global Chance / Risk Fund • SEB Fund 1 - SEB Sustainability Fund Europe • SEB Fund 1 - SEB Sustainability Nordic Fund The following Sub-Funds are not distributed in Germany: • SEB Fund 1 - SEB Europe Index Fund • SEB Fund 1 - SEB Norway Focus Fund • SEB Fund 1 - SEB US All Cap The information disclosed above is as at 31 December 2019 and this may change after the year end. -

Svenska Handelsbanken AB

OFFERING CIRCULAR Svenska Handelsbanken AB (publ) (Incorporated as a public limited liability banking company in The Kingdom of Sweden) U.S.$50,000,000,000 Euro Medium Term Note Programme for the issue of Notes with a minimum maturity of one month On 26th June, 1992 Svenska Handelsbanken AB (publ) (the “Issuer” or the “Bank”) entered into a U.S.$1,500,000,000 Euro Medium Term Note Programme (the “Programme”) and issued an offering circular on that date describing the Programme. This Offering Circular supersedes any previous offering circular and supplements therein prepared in connection with the Programme. Any Notes (as defined below) issued under the Programme on or after the date of this Offering Circular are issued subject to the provisions described herein. This does not affect any Notes already in issue. Under the Programme, the Bank may from time to time issue Notes (the “Notes”), which expression shall include Notes (i) issued on a senior preferred basis as described in Condition 3 (“Senior Preferred Notes”), (ii) issued on a senior non-preferred basis as described in Condition 4 (“Senior Non-Preferred Notes”), (iii) issued on a subordinated basis and which rank on any voluntary or involuntary liquidation (Sw. likvidation) or bankruptcy (Sw. konkurs) of the Bank as described in Condition 5 (“Subordinated Notes”) and (iv) issued on a subordinated basis with no fixed maturity and which rank on any voluntary or involuntary liquidation (Sw. likvidation) or bankruptcy (Sw. konkurs) of the Bank as described in Condition 6 (“Additional Tier 1 Notes”). The Outstanding Principal Amount (as defined in Condition 2) of each Series (as defined below) of Additional Tier 1 Notes will be subject to Write Down (as defined in Condition 2) if the Common Equity Tier 1 Capital Ratio (as defined in Condition 2) of the Bank and/or the Handelsbanken Group (as defined Condition 2) is less than the relevant Trigger Level (as defined in Condition 2). -

Alternative Index Weighting Strategies on the Swedish Stock Market

Alternative Index Weighting Strategies on the Swedish Stock Market William Appelgren Johanna Trost [email protected] [email protected] Stockholm School of Economics Department of Finance Spring 2014 Tutor: Michael Halling Abstract The Market-Capitalization index reweighting has since long had the role as the conventional tool for passive investments through its simplicity and CAPM framework conformance. Nowadays, alternative index reweightings are getting increased traction in the light of market-capitalization criticism and suggested risk-return improvements and possibilities of desired characteristics. This study sets to examine four alternative index reweightings; the Minimum Variance, the Equal Weights, the Equal Risk Contribution and the Risk-Weighted Alpha reweighting methods, as well as compare these indices to the benchmark Market-Capitalization weighted index over a number of quantitative measures. The stock universe chosen is the OMXS30 constituents of the NASDAQ OMX Stockholm Stock Exchange and the study also discusses the feasibility of introducing the alternative methods to the exchange. The study shows that all computed alternative methods beat the benchmark in terms of risk-adjusted return, as well as return in absolute measures. Index weight characteristics over time, especially as an effect of short-selling constraints, do however impact the weightings significantly and with regards to feasibility do not all alternative indices show on definite prevalence over the Market-Capitalization index for the examined data set and time period. Possible improvements of the data collection, method decisions and tools for analysis are also discussed as a reference for further studies. The findings of the study conclude in not being able to reject the proposal of an alternative index launch on the Swedish stock market. -

Sca Annual Report 2019 2019 Introduction

SCA ANNUAL REPORT 2019 SCA ANNUAL REPORT 2019 INTRODUCTION Europe’s largest private forest owner SCA is Europe’s largest private forest owner with 2.6 million hectares of forest in Northern Sweden and 30,000 hectares in Estonia and Latvia. Based on this unique resource, SCA has developed an industry that generates the greatest possible value in and from the forest. 2.6 million hectares of forest land Pulp mill SCA ANNUAL REPORT 2019 SCA ANNUAL REPORT Sawmills Publication paper mills Kraftliner mills SCA’s forest holdings Estonia Latvia 2 Cover: SCA’s large forest holding is a unique asset that forms the basis for the company’s value chain. This is SCA Contents Introduction 3 This is SCA 4 The year at a glance Forest 6 President's message SCA owns a total of 2.6 million 8 Value chain hectares of forest in Northern 10 The green cycle Sweden, an area nearly the size of Belgium, and 30,000 hectares in 12 Forest and climate Estonia and Latvia. SCA’s unique 14 Vibrant local communities forest asset is a growing resource 16 Trends that provides access to high- quality forest raw materials while capturing a net of more than 10% Strategy and operations 18 Strategy of Sweden’s fossil CO2 emissions. 22 Forest Wood 28 Wood SCA is one of Europe’s leading 32 Pulp suppliers of wood-based products 36 Paper for the wood industry and building materials trade, with an annual pro- 42 Renewable energy duction capacity of 2.2 million m3 44 Logistics of solid-wood products. -

Interim Report January – September 2020 Q3

Interim Report January – September 2020 Q3 Financial summary Third quarter First nine months • Net sales amounted to EUR 27k (0) • Net sales amounted to EUR 126k (21k) • Operating loss (EBIT) increased to EUR 4,790k • Operating loss (EBIT) increased to EUR 7,291k (748k) driven by listing costs (3,490k) driven by listing costs • Loss after tax amounted to EUR 4,730k (815k) • Loss after tax amounted to EUR 7,127k (3,602k) • Basic and diluted loss per Class A share amounted to EUR 0.10 (0.02) • Basic and diluted loss per Class A share amounted to EUR 0.16 (0.08) • Liquid funds as at end of the period amounted to EUR 90.5m • Cash flow from operating activities amounted to EUR -1,824k (-3,014k) • No interest-bearing debt at end of the period Figures within parentheses refer to the preceding year. Significant events • Enlisted Inselspital Bern, the largest In the third quarter of 2020 university hospital in Switzerland, to be the lead hospital in our upcoming RefluxStop™ • Completed listing on Nasdaq First North Premier Growth Market raising SEK 1.1 Registry clinical trial to be focused primarily billion, with trading of Implantica's Swedish in Germany and Switzerland. Depository Receipts commencing on September 21, 2020. The offering was After the end of the period substantially oversubscribed. • Exercised overallotment option raising an additional SEK 165 million. • Increased our shareholder base with highly reputable shareholders such as Swedbank • Implantica’s RefluxStop™ trial showed Robur Ny Teknik, Handelsbanken Fonder, exceptional three-year follow-up results. TIN Fonder, Skandia and Nordea Investment None of the 47 patients in the study were in Management. -

Annual Report 2014

ANNUAL REPORT 2014 Dress €99 Blazer €19.99 H&M SPRING 2015 MODERN ESSENTIALS SELECTED BY DAVID BECKHAM SPRING 2015 Shirt €19.99 H&M SPRING 2014 Sweater € 19.95 — H&M ANNUAL REPORT 2014 — Contents H&M IN WORDS AND PICTURES This is H&M 8 CEO letter 10 2014 in brief 12 Our brands 16 Sustainable development 36 Our employees 42 Expansion 46 History 54 H&M IN FIGURES Administration report, including proposed distribution of earnings 60 Group income statement 66 Consolidated statement of comprehensive income 66 Group balance sheet 67 Group changes in equity 68 Group cash flow statement 69 Parent company income statement 70 Parent company statement of comprehensive income 70 Parent company balance sheet 71 Parent company changes in equity 72 Parent company cash flow statement 73 Notes to the financial statements 74 Signing of the annual report 90 Auditor’s report 91 Corporate governance report, including information about the board of directors 92 Auditor’s statement on the corporate governance report 104 Five year summary 106 The H&M share 107 Financial information and contact details 108 H&M’s annual accounts and consolidated accounts for the financial year 2013/14 comprise pages 60–90. — THIS IS H&M — Fashion and quality at the best price H&M is a leading global fashion company with strong values and a clear business concept. H&M has a passion for fashion, a belief in people and a desire to always exceed customers’ expectations – and to do so in a sustainable way. H&M’s busi- ness concept is to offer fashion and quality at the best price. -

PDF Press Release Notice of AGM Investor 2021

Press release Stockholm, March 30, 2021 Notice of Investor AB’s Annual General Meeting on May 5, 2021 Investor AB (publ) summons to the Annual General Meeting (the “Meeting”) on Wednesday, May 5, 2021. Due to covid-19, the Meeting is only conducted by advance voting. Information on the resolutions passed at the Meeting will be disclosed on May 5, 2021, as soon as the outcome of the advance voting has been confirmed. Shareholders can submit questions to [email protected] up to and including April 25, 2021, with written response from the Company no later than on April 30, 2021. A pre-recorded interview with the Chair of the Board, Jacob Wallenberg, and the President, Johan Forssell, where they together discuss the fiscal year 2020 and answer a number of questions received, will be available on Investor's website, www.investorab.com, on May 3, 2021. In addition, the Chair of the Board and the President will be available to answer questions at a live conference call on May 3, 2021, via Investor’s website, www.investorab.com. Registration and notification A shareholder who wishes to participate in the Meeting must • be recorded as a shareholder in the share register prepared by Euroclear Sweden AB concerning the circumstances on Tuesday, April 27, 2021, and • notify its intention to participate by casting its advance vote in accordance with the instructions under the heading Advance voting below so that the advance voting form is received by Euroclear Sweden AB no later than Tuesday, May 4, 2021. To be entitled to participate in the Meeting a shareholder whose shares are registered in the name of a nominee must, in addition to providing notification of participation, register its shares in its own name so that the shareholder is recorded 1(4) in the share register on Tuesday, April 27, 2021. -

Svenska Handelsbanken

Annual Report 2001 Svenska Handelsbanken THE ANNUAL GENERAL MEETING OF SVENSKA HANDELSBANKEN will be held at the Grand Hôtel, Vinterträdgården, Royal entrance, Stallgatan 4, Stockholm, at 10.00 a.m. on Tuesday, 23 April 2002. NOTICE OF ATTENDANCE AT ANNUAL GENERAL MEETING Shareholders wishing to attend the Meeting must: • be entered in the Register of Shareholders kept by VPC AB (Swedish Central Securities Depository and Clearing Organisation), on or before Friday, 12 April 2002, and • give notice of attendance to the Chairman's Office at the Head Office of the Bank, Kungsträdgårdsgatan 2, SE-106 70 Stockholm, telephone +46 8 701 19 84, or via the Internet www.handelsbanken.se/bolagsstamma (Swedish only), by 3 p.m. on Wednesday, 17 April 2002. In order to be entitled to take part in the Meeting, any share- holders whose shares are nominee-registered must also request a temporary entry in the register of shareholders kept by the VPC. Shareholders must notify the nominee about this well before 12 April 2002, when this entry must have been effected. DIVIDEND The Board of Directors recommends that the record day for the dividend be Friday, 26 April 2002. If the Annual General Meeting votes in accordance with this recommendation, the VPC expects to be able to send the dividend to shareholders on Thursday, 2 May 2002. PUBLICATION DATES FOR INTERIM REPORTS January–March 22 April 2002 January–June 20 August 2002 January–September 22 October 2002 Svenska Handelsbanken AB (publ) Registered no. 502007-7862 www.handelsbanken.se Contents HIGHLIGHTS OF THE YEAR 2 THE GROUP CHIEF EXECUTIVE’S COMMENTS.......... -

Annual and Sustainability Report 2018

Annual and Sustainability Report 2018 We build for a better society. B Skanska Annual and Sustainability Report 2018 Operations Skanska’s operations consist of Construction and Project Development, including Residential Development, Commercial Property Development and, until 2018, Infrastructure Development. Business units within these streams collaborate in various ways, creating operational and financial synergies that generate increased value. Residential Commercial Property Infrastructure Construction Development Development Development 1 Constructs and renovates build- Develops new residential projects, Develops customer-focused office Secures and manages the value ings, infrastructure and homes, including single and multi-family buildings, shopping centers and of Skanska’s existing public- along with facilities manage- housing, built by the Construction logistics properties built by the private partnership (PPP) assets. ment and other related services. business stream. Construction business stream. 1 As of January 1, 2019, Infrastructure Development is no longer a business stream and is reported in Central on a separate line. Well diversified, Percentage of total revenue in 2018 with a leading market position Skanska’s diversification across various business streams with operations in eleven countries and several market segments strengthens the Group’s 40% SwedenSweden competitive standing and ensures FinlandFinland Norway a balanced and diversified risk profile. USA 38% Denmark United Kingdom Poland Czech Republic SlovakiaSlovakia Hungary 22% Romania Green revenue in 2018 Green market value in 2018 Green financing in 2018 Percentage of total Construction revenue Percentage of Commercial Property Percentage of total central debt 3 that is that is Green and Deep green, as defined Development market value from Green Green, according to the Skanska Green by the Skanska Color Palette™ 2. -

List of PRA-Regulated Banks

LIST OF BANKS AS COMPILED BY THE BANK OF ENGLAND AS AT 2nd December 2019 (Amendments to the List of Banks since 31st October 2019 can be found below) Banks incorporated in the United Kingdom ABC International Bank Plc DB UK Bank Limited Access Bank UK Limited, The ADIB (UK) Ltd EFG Private Bank Limited Ahli United Bank (UK) PLC Europe Arab Bank plc AIB Group (UK) Plc Al Rayan Bank PLC FBN Bank (UK) Ltd Aldermore Bank Plc FCE Bank Plc Alliance Trust Savings Limited FCMB Bank (UK) Limited Allica Bank Ltd Alpha Bank London Limited Gatehouse Bank Plc Arbuthnot Latham & Co Limited Ghana International Bank Plc Atom Bank PLC Goldman Sachs International Bank Axis Bank UK Limited Guaranty Trust Bank (UK) Limited Gulf International Bank (UK) Limited Bank and Clients PLC Bank Leumi (UK) plc Habib Bank Zurich Plc Bank Mandiri (Europe) Limited Hampden & Co Plc Bank Of Baroda (UK) Limited Hampshire Trust Bank Plc Bank of Beirut (UK) Ltd Handelsbanken PLC Bank of Ceylon (UK) Ltd Havin Bank Ltd Bank of China (UK) Ltd HBL Bank UK Limited Bank of Ireland (UK) Plc HSBC Bank Plc Bank of London and The Middle East plc HSBC Private Bank (UK) Limited Bank of New York Mellon (International) Limited, The HSBC Trust Company (UK) Ltd Bank of Scotland plc HSBC UK Bank Plc Bank of the Philippine Islands (Europe) PLC Bank Saderat Plc ICBC (London) plc Bank Sepah International Plc ICBC Standard Bank Plc Barclays Bank Plc ICICI Bank UK Plc Barclays Bank UK PLC Investec Bank PLC BFC Bank Limited Itau BBA International PLC Bira Bank Limited BMCE Bank International plc J.P.