November 1, 2011 Ms. Susan M. Cosper Technical

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Safe and Secure Distribution of Controlled Substances September 2019 About This Report

Safe and Secure Distribution of Controlled Substances September 2019 About This Report AmerisourceBergen exists within a highly AmerisourceBergen is publishing this report complex and dynamic healthcare environment. both to build on the Company’s commitment to We provide both our partners and the healthcare transparency and to provide stockholders and other system deep scale, efficiency, and value. Our wholesale stakeholders information on our efforts to ensure pharmaceutical distribution business plays a key role the safe and secure distribution of opioids and in the pharmaceutical supply chain, providing safe other controlled substances, as well as information access to thousands of important medications for on the community and associated outreach healthcare providers to serve patients with a wide programs AmerisourceBergen created and supports array of clinical needs across the healthcare spectrum. to help combat the opioid epidemic. This report supplements our efforts to communicate with The driving force behind everything we do is our stakeholders through our Corporate Citizenship Purpose - we are united in our responsibility to create Report, proxy materials, and the Fighting the Opioid healthier futures. This Purpose drives every facet of Epidemic section of our website1 and supports our our business and is more important today than ever ongoing dialogue through direct engagement. as we and the country grapple with the opioid crisis. AmerisourceBergen welcomes the opportunity AmerisourceBergen has a longstanding commitment to provide this information and the Company is to ensuring a safe and efficient pharmaceutical committed to continued transparency. supply chain. We have taken substantial steps to combat the diversion of controlled substances and fight opioid misuse and abuse. -

Name Address City Zip AMERISOURCEBERGEN CORP

Name Address City Zip AMERISOURCEBERGEN CORP 322 N 3RD ST PADUCAH 42001 AMERISOURCEBERGEN CORP 6810 SHADY OAK RD EDEN PRAIRIE 55344 AMERISOURCEBERGEN CORP 172 CAHABA VALLEY PKY PELHAM 35124 AMERISOURCEBERGEN CORP 6305 LASALLE DR LOCKBOURNE 43137 AMERISOURCEBERGEN CORP 501 PATRIOT PKWY ROANOKE 76262 AMERISOURCEBERGEN CORP 1001 W TAYLOR RD ROMEOVILLE 60446 AMERISOURCEBERGEN CORP 11200 NORTH CONGRESS AVE KANSAS CITY 64153 AMERISOURCEBERGEN CORP 5100 JAINDL BLVD BETHLEHEM 18017 AMERISOURCEBERGEN CORP 004 101 NORFOLK ST MANSFIELD 2048 AMERISOURCEBERGEN CORP 008 1325 W STRIKER AVE SACRAMENTO 95834‐1164 AMERISOURCEBERGEN CORP 012 1851 CALIFORNIA AVE CORONA 92881 AMERISOURCEBERGEN CORP 017 1765 FREMONT DR SALT LAKE CITY 84104 AMERISOURCEBERGEN CORP 020 1825 S 43RD AVE PHOENIX 85009 AMERISOURCEBERGEN CORP 024 24903 AVE KEARNY VALENCIA 91355 AMERISOURCEBERGEN CORP 026 238 SAND ISLAND ACCESS RD #M‐1 HONOLULU 96819 AMERISOURCEBERGEN CORP 032 19220 64TH AVE SOUTH KENT 98032 AMERISOURCEBERGEN CORP 037 12727 W AIRPORT BLVD SUGAR LAND 77478 AMERISOURCEBERGEN CORP 038 501 W 44TH AVE DENVER 80216 AMERISOURCEBERGEN CORP 040 1085 N SATELLITE BLVD SUWANEE 30024 AMERISOURCEBERGEN CORP 041 9900 JEB STUART PKWY GLEN ALLEN 23059 AMERISOURCEBERGEN CORP 049 ONE INDUSTRIAL PARK DR WILLIAMSTON 48895 AMERISOURCEBERGEN DRUG CO 120 TRANS AIR DR MORRISVILLE 27560 AMERISOURCEBERGEN DRUG CORP 2100 DIRECTORS ROW ORLANDO 32809‐6234 AMERISOURCEBERGEN DRUG CORP 10910 VISTA BLVD SUITE 401 ORLANDO 32829 ASD SPECIALTY HEALTHCARE ABC 345 INTERNATIONAL BLVD STE 400 BROOKS 40109 -

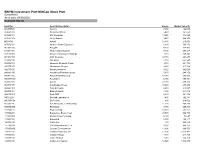

BNYM Investment Port:Midcap Stock Port (Unaudited) As of Date: 09/30/2020 Common Stocks

BNYM Investment Port:MidCap Stock Port (Unaudited) As of date: 09/30/2020 Common Stocks Identifier Security Description Shares Market Value ($) 002535300 Aaron's 7,450 422,043 00404A109 Acadia Healthcare 5,480 161,550 004498101 ACI Worldwide 13,250 346,223 00508Y102 Acuity Brands 9,470 969,255 BD845X2 Adient 12,480 216,278 00737L103 Adtalem Global Education 6,800 166,872 00766T100 AECOM 4,170 174,473 018581108 Alliance Data Systems 7,130 299,317 01973R101 Allison Transmission Holdings 7,110 249,845 00164V103 AMC Networks 10,710 264,644 023436108 Amedisys 2,760 652,547 025932104 American Financial Group 3,310 221,704 03073E105 AmerisourceBergen 2,220 215,162 042735100 Arrow Electronics 5,620 442,069 04280A100 Arrowhead Pharmaceuticals 5,670 244,150 045487105 Associated Banc-Corp 47,940 605,003 05329W102 Autonation 6,980 369,451 05368V106 Avient 23,030 609,374 053774105 Avis Budget Group 10,600 278,992 05464C101 Axon Enterprise 2,410 218,587 062540109 Bank of Hawaii 4,830 244,012 06417N103 Bank OZK 6,630 141,352 090572207 Bio-Rad Laboratories 1,480 762,881 09073M104 Bio-Techne 880 218,002 05550J101 BJs Wholesale Club Holdings 11,270 468,269 09227Q100 Blackbaud 3,750 209,363 103304101 Boyd Gaming 18,350 563,162 105368203 Brandywine Realty Trust 93,500 966,790 11120U105 Brixmor Property Group 6,300 73,647 117043109 Brunswick 8,150 480,117 12685J105 Cable One 300 565,629 127190304 CACI International, Cl. A 3,980 848,377 12769G100 Caesars Entertainment 11,890 666,553 133131102 Camden Property Trust 11,390 1,013,482 134429109 Campbell Soup 4,440 -

Generics Breakout Welcome

Generics Breakout Welcome David Picard Senior Vice President, Global Generic Pharmaceuticals Discussion Agenda • CERTIO Enhancements • American Health Packaging Alan Ratliff, Director, Supplier Trade o Kyle Pudenz, Senior Vice President, o Manufacturer and Data Services Relations • Generic Sourcing • Stable Supply Initiative o Chris Doerr, Vice President, Global o Heather Ryan, Senior Manager, Drug Shortage Generic Sourcing Solutions • Q&A SM • SureSupply o Heather Odenwelder, Senior Director, Category Management o Charles Hartenstine, Senior Director, Category Management CERTIO 2020 AmerisourceBergen Switzerland Kyle Pudenz Senior Vice President, Manufacturer and Data Services CERTIO® 2020 Evolving the CERTIO solution to address key business challenges. Further Supply Chain Integration Support Proactive Communication Easier to Use Project Overview Working with key stakeholders to address your business needs CERTIO 2020 Kickoff CERTIO Champions Sessions December 14 2019 Unique CERTIO Champions 108+ 9 Engaged CERTIO Users November Enhanced CERTIO 9 Dashboards 90+ CERTIO 2020 Launch CERTIO® 2020 and Beyond Continuing to shape your preferred supply chain solution • Launching November 9, 2020 o No change in current functionality Contact Upcoming training opportunities o [email protected] • Platform Evolution 2021 o Product Oversight o Failure to Supply o …and more! Special thanks to our CERTIO® Champions! Manufacturer Partners AmerisourceBergen Ajanta Lannett Global Generics Leadership Alembic Lupin Category Management Apotex Mallinckrodt -

ABCDEF LAST UPDATED: 05/28/2014 This Reflects the Last Date of Any Changes Made to the List

ABCDEF LAST UPDATED: 05/28/2014 This reflects the last date of any changes made to the list. Authorized Distributors Below is a list of Roxane Laboratories, Inc. (RLI) Authorized Distributors. These distributors have met RLI's requirements to distribute RLI's products. Authorized Distributors listed below are approved to distribute the entire RLI product line provided that they have the appropriate licenses. AmerisourceBergen Drug Corp AmerisourceBergen Drug Corp 172 Cahaba Valley Pkwy PELHAM AL AmerisourceBergen Drug Corp 1825 S 43rd Ave STE B PHOENIX AZ AmerisourceBergen Drug Corp 1851 California Ave CORONA CA AmerisourceBergen Drug Corp 1325 W Striker Ave SACRAMENTO CA AmerisourceBergen Drug Corp 24903 Avenue Kearny VALENCIA CA AmerisourceBergen Drug Corp 501 W 44th Ave DENVER CO AmerisourceBergen Drug Corp 2100 Directors Row ORLANDO FL AmerisourceBergen Drug Corp 1085 N Satellite Blvd SUWANEE GA AmerisourceBergen Drug Corp 238 Sand Island Access Rd #M1 HONOLULU HI AmerisourceBergen Drug Corp 1001 W TAYLOR RD ROMEOVILLE IL AmerisourceBergen Drug Corp 322 N 3RD St PADUCAH KY AmerisourceBergen Drug Corp 101 Norfolk St MANSFIELD MA AmerisourceBergen Drug Corp One Industrial Park Dr WILLIAMSTON MI AmerisourceBergen Drug Corp 6810 Shady Oak Rd EDEN PRAIRIE MN AmerisourceBergen Drug Corp 11200 N CONGRESS AVE KANSAS CITY MO AmerisourceBergen Drug Corp 8190 Lackland Rd SAINT LOUIS MO AmerisourceBergen Drug Corp 6300 St Louis St MERIDIAN MS AmerisourceBergen Drug Corp 8605 Ebenezer Church Rd RALEIGH NC AmerisourceBergen Drug Corp 100 Friars -

Women in Leadership 2018 a Status Report on Women Leaders in Corporate Boardrooms and Executive Offices

Women in Leadership 2018 A Status Report on Women Leaders in Corporate Boardrooms and Executive Offices The Forum of Executive Women Philadelphia, PA 2018–2019 About The Forum of Executive Women Board of Directors Founded in 1977, The Forum of Executive Women is a membership organization of more than 450 women of significant influence Officers across the Greater Philadelphia region. The Forum’s membership Margaret A. McCausland consists of individuals holding the senior-most positions in President the corporations, nonprofit organizations and public sector entities that drive our regional economy and community. Lisa Detwiler Vice President The Forum’s members are executive women working together Katherine Hatton to increase the number of women in leadership roles, expand Secretary their impact and influence, and position them to drive positive change in the region. We have served as the catalyst for a Shannon Breuer multitude of initiatives that have sparked critical conversations Treasurer in executive suites, boardrooms and public policy arenas. Forum programs and initiatives include symposiums, CEO At-Large Directors Roundtables, a Public Sector Leadership Conversation Series, and Committee Chairs publication of research reports, and outreach promoting the value Jeanne S. Barnum of gender diversity on boards and in executive suites. A robust Yelena M. Barychev mentoring program with diverse initiatives enhances The Forum’s Emily V. Biscardi commitment to building the pipeline of our next generation of Teresa Bryce Bazemore women leaders in the tri-state Greater Philadelphia region. Joan F. Chrestay Diane M. Connor Tanuja M. Dehne Nancy O’Mara Ezold The Forum of Executive Women Debra Fickler 1231 Highland Avenue Amy S. -

Sotrovimab Access Guide

Access & Reimbursement Information for Sotrovimab June 2021 AUTHORIZED USE Sotrovimab is authorized for use under an Emergency Use Authorization (EUA) for the treatment of mild-to-moderate coronavirus disease 2019 (COVID-19) in adults and pediatric patients (12 years of age and older weighing at least 40 kg) with positive results of direct SARS-CoV-2 viral testing, and who are at high risk for progression to severe COVID-19, including hospitalization or death. LIMITATIONS OF AUTHORIZED USE • Sotrovimab is not authorized for use in patients: who are hospitalized due to COVID-19, OR who require oxygen therapy due to COVID-19, OR who require an increase in baseline oxygen flow rate due to COVID-19 (in those on chronic oxygen therapy due to underlying non-COVID-19 related comorbidity). • Benefit of treatment with sotrovimab has not been observed in patients hospitalized due to COVID-19. SARS-CoV-2 monoclonal antibodies may be associated with worse clinical outcomes when administered to hospitalized patients with COVID-19 requiring high flow oxygen or mechanical ventilation. Sotrovimab is not FDA-approved and is authorized only for the duration of the declaration that circumstances exist justifying the authorization of the emergency use of sotrovimab under section 564(b)(1) of the Act, 21 U.S.C. § 360bbb-3(b)(1), unless the authorization is terminated or revoked sooner. Please see Important Safety Information, most current Fact Sheet for Healthcare Providers and Fact Sheet for Patients, Parents, and Caregivers, and FDA Letter of Authorization -

7/7/2020 FAQ Regarding Upcoming Commercial Remdesivir Allocation

7/7/2020 FAQ Regarding Upcoming Commercial Remdesivir Allocation On June 29, 2020, the Department of Health and Human Services (HHS) announced an agreement with Gilead Sciences to secure 500,000 treatment courses of commercial remdesivir for American hospitals through September 2020. In contrast to the previous donated supply of remdesivir, this supply will be purchased by American hospitals. On Friday July 3, 2020, the HHS Office of the Assistant Secretary for Preparedness and Response (HHS/ASPR) announced further details on the upcoming allocation process, as summarized in the following figure: On Monday July 6, 2020, representative members of the Society of Infectious Diseases Pharmacists (SIDP) met with ASPR and AmerisourceBergen (sole distributor of remdesivir) to clarify frequently asked questions regarding this upcoming process. Frequently Asked Questions • What price should American hospitals expect to pay for commercial remdesivir when ordering from AmerisourceBergen? Most American hospitals should expect to pay the wholesale acquisition cost (WAC) of $520 per 100 mg vial of remdesivir. For a typical 5-day course of remdesivir (total of 6 vials), this would equate to $3,120 per course. The government price of $390 per vial is applicable to federal agencies that directly purchase drugs, such as the Veterans’ Affairs, Indian Health Services, Department of Defense, the Coast Guard and the Federal Bureau of Prisons, once on the Federal Supply Schedule, and will not apply to most American hospitals. • Per ASPR, state level allocations of commercial remdesivir will be based on American hospitals reporting data on suspected or confirmed COVID-19 cases every 2 weeks via the TeleTracking portal. -

President's Message Inside 4Q2019

Inside 4Q2019 2.......Template.for.Disaster 8.......Past.Events 3.......ACC.News 15.....Sponsors.for.2019 4.......Choice.of.Law.and.Covenants.. 16.....New.and.Returning.Members Not.to.Compete 18.....Upcoming.ACCGP.Events 5.......Member.Spotlight 18.....Chapter.Leadership 6.......Aileen.Schwartz.Forges.Relationships,.. Inspires.Change 7.......Association.of.Corporate.. Counsel’sTop.10.30-Somethings FOCUS President’s Message Peter A. Prinsen I am advised by our Membership Chair, Speaking of 2020, I’m thrilled CLE Institute on December Mike Eckhardt from Wawa, that the Greater to report that we have had an 10th, Morgan Lewis’ sponsor- Philadelphia Chapter’s membership is now at overwhelming response to our ship of Pro Bono efforts with over 1,600 members. Not only is the number 2020 sponsorship opportunities. Philadelphia VIP on December of our Chapter members outstanding, but the Like last year, we have been 11th and culminating with level of your involvement and commitment to oversubscribed in virtually all sponsorship our Annual Holiday Party and Board the Chapter is extraordinary as well. This year levels. Despite being oversubscribed, we Installation on December 12th at the we will have put on over 80 programs ranging continue to work hard to find opportunities Racquet Club of Philadelphia. from our Meet your Counterparts Programs for our sponsors to “squeeze them in” so that I am truly humbled to have been your to our In-House Counsel Conference (where they can enjoy the benefit of sponsorship of President for 2019. For 2020, the Chapter over 600 of you attended and participated in this fine Chapter. -

Program on Topics of Executive Communication and Advanced Persuasion

The 7th Annual Philadelphia The Pennsylvania Diversity Council presents Diversity & Inclusion 2.0: Aligning Purpose, People & Performance September 1, 2016 8:30am - 3:00pm Hilton Philadelphia City Avenue 4200 City Avenue Philadelphia, Pennsylvania 19131 HELPING MORE PEOPLE ACHIEVE THEIR DREAM OF HOMEOWNERSHIP At Radian, we are committed to helping people achieve their dream of homeownership. For nearly 40 years, we have been working diligently with our lending partners to find innovative solutions to make this dream a reality for more deserving homebuyers. To learn more or to partner with Radian, please visit radian.biz. Radian is proud to support the 7th Annual Philadelphia Diversity & Leadership Conference. www.radian.biz 877.723.4261 Visit our new homebuyer website at AchieveTheDream.com to see how we are helping first-time homebuyers navigate the process with ease! © 2016 Radian Guaranty Inc. WELCOME FROM THE NATIONAL DIVERSITY COUNCIL DENNIS KENNEDY ANGELES VALENCIANO Founder & Chairman CEO National Diversity Council National Diversity Council We are truly honored to welcome you to the 7th Annual Philadelphia Diversity & Leadership Conference. As the country faces ever-changing demographics, new opportunities have risen for organizations to create a diverse and inclusive environment in order to foster innovation and leadership excellence. The purpose of today’s event is to ensure companies possess the tools they need for success by sharing diversity and inclusion best practices and essential leadership skills. The Diversity & Leadership Conference is comprised of an opening awards breakfast, several breakout panel sessions, and awards luncheon. Throughout the conference, speakers will openly discuss topics relating to the event theme of “Diversity & Inclusion 2.0: Aligning Purpose, People, and Performance.” We will also have the honor of recognizing several influential business executives who have exemplified leadership excellence and championed diversity and inclusion throughout their careers. -

Comcast Technology Center Opens

Press Contact: Marlene K. Sahms T 610.755.6930 [email protected] FOR IMMEDIATE RELEASE Comcast Technology Center Opens Philadelphia, PA (July 24, 2018) — Newmark Knight Frank (NKF) released its second-quarter 2018 office reports for the greater Philadelphia region. The reports detail no slowdown in activity for Southeastern Pennsylvania, while the delivery of the Comcast Technology Center results in the Philadelphia Central Business District (CBD) recording over 1.0 million square feet of positive absorption. Both Delaware's suburban submarkets and the Southern New Jersey market struggle with rising vacancy. Southeastern Pennsylvania recorded 709,719 square feet of positive absorption for the first half of the year and surpassed 2017’s year-end absorption by 148,000 square feet. Overall vacancy decreased 60 basis points quarter-over- quarter to 14.0 percent. USSC Group’s expansion into 300,000-square-foot at 101 Gordon Drive, located in the Exton/Malvern submarket, accounted for most of the quarter’s 355,000 square feet of absorption. On the downside, some suburban tenants decided to shed excess space, which pushed year-over-year sublease availability up 10 basis points to 2.0 percent. In the Fort Washington submarket, T-Mobile relocated and downsized from 45,000 square feet at 500 Virginia Drive to 24,112 square feet at 475 Virginia Drive. Transamerica, located in the Exton/Malvern submarket, outsourced a number of business line jobs to a third-party provider, downsizing from 90,300 square feet at 300 Eagleview Boulevard to 9,500 square feet at 350 Eagleview Boulevard. During the second quarter, pharmaceutical distributer AmerisourceBergen announced that it planned to keep its headquarters in Conshohocken. -

Amerisourcebergen Customer Huddle December 2, 2020

AmerisourceBergen Customer Huddle December 2, 2020 During the call, please submit questions via the Skype window. Both audio and visuals are available through the Skype Meeting Broadcast link and are accessible via any browser, either PC or mobile. Today’s Speakers Keyvan Nekouei Alexis Rose Sr. Director, Account Vice President, Experience & Clinical Health Systems Services During the call, please submit questions via the Skype Q&A window. Both audio and visuals are available through the Skype Meeting Broadcast link and are accessible via any browser, either PC or mobile. COVID-19 Updates COVID-19 Therapies NDC # ABC Item # Commercially Government Product Manufacturer (if commercially (if commercially Available? Allocated? available) available) Veklury (remdesivir) Gilead Sciences YES NO 61958-2901-02 10251685 Eli Lilly and Bamlanivimab NO YES N/A N/A Company Eli Lilly and 2mg: 0002-4182-30 2mg: 10251952 Olumiant (baricitinib) YES NO Company 1mg: 0002-4732-30 1mg: 10252013 Regeneron Casirivimab and Pharmaceuticals, NO YES N/A N/A Imdevimab Inc. 4 12/02/2020 CONFIDENTIAL COVID-19 Therapies Resources FDA Approval Additional Info regarding Healthcare Providers Patient Fact FDA Authorization Product OR EUA product access, dosage, Fact Sheet Sheet Letter Announcement clinical data Veklury Healthcare Providers FDA Authorization FDA Approval Patient Support Veklury Website (remdesivir) Resources Letter Patient Fact Sheet (ENG) EUA Healthcare Providers FDA Authorization Bamlanivimab Bamlanivimab Website Announcement Fact Sheet Letter Patient Fact