Annual Report 2015 for the Year Ended March 31, 2015

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Disaster Management of India

DISASTER MANAGEMENT IN INDIA DISASTER MANAGEMENT 2011 This book has been prepared under the GoI-UNDP Disaster Risk Reduction Programme (2009-2012) DISASTER MANAGEMENT IN INDIA Ministry of Home Affairs Government of India c Disaster Management in India e ACKNOWLEDGEMENT The perception about disaster and its management has undergone a change following the enactment of the Disaster Management Act, 2005. The definition of disaster is now all encompassing, which includes not only the events emanating from natural and man-made causes, but even those events which are caused by accident or negligence. There was a long felt need to capture information about all such events occurring across the sectors and efforts made to mitigate them in the country and to collate them at one place in a global perspective. This book has been an effort towards realising this thought. This book in the present format is the outcome of the in-house compilation and analysis of information relating to disasters and their management gathered from different sources (domestic as well as the UN and other such agencies). All the three Directors in the Disaster Management Division, namely Shri J.P. Misra, Shri Dev Kumar and Shri Sanjay Agarwal have contributed inputs to this Book relating to their sectors. Support extended by Prof. Santosh Kumar, Shri R.K. Mall, former faculty and Shri Arun Sahdeo from NIDM have been very valuable in preparing an overview of the book. This book would have been impossible without the active support, suggestions and inputs of Dr. J. Radhakrishnan, Assistant Country Director (DM Unit), UNDP, New Delhi and the members of the UNDP Disaster Management Team including Shri Arvind Sinha, Consultant, UNDP. -

Synthesis Report

MEGA DISASTER IN A RESILIENT SOCIETY The Great East Japan (Tohoku Kanto) Earthquake and Tsunami of 11th March 2011 SYNTHESIS AND INITIAL OBSERVATIONS International Environment and Disaster Management Graduate School of Global Environmental Studies Kyoto University 25th March 2011 About this Report This report is published on 25th of March 2011, two weeks after the Great East Japan [Tohoku-Kanto] Earthquake and Tsunami. The aim of the report is to synthesize certain existing data with basic situation analysis. The disaster has posed a major challenge to the disaster risk reduction community, which needs to be discussed in future over the course of time. Assistance of Yukiko Takeuchi for providing information, and Kumiko Fujita and Yuta suda in translating parts of the Japanese information is acknowledged. Team Members (Kyoto University) Sunil Parashar Noralene Uy Huy Nguyen Glenn Fernandez Farah Mulyasari Jonas Joerin Rajib Shaw Contact Details Rajib Shaw Associate Professor International Environment and Disaster Management Laboratory, KYOTO UNIVERSITY Yoshida Honmachi, Sakyo-Ku, Kyoto 606-8501, Japan Tel/Fax: 81-75-753-5708 E-mail: [email protected] Web: http://www.iedm.ges.kyoto-u.ac.jp/ Disclaimer The views expressed in this report are the views of the team members and do not necessarily reflect the views or policies of the research field for International Environment & Disaster Management (IEDM) or the Graduate School of Global Environment Studies (GSGES), or Kyoto University, or the organizations, or the countries cited. The report is a compilation from available sources, which are acknowledged. IEDM does not guarantee the accuracy of the data included in this volume and accept no responsibility for any consequences of their use. -

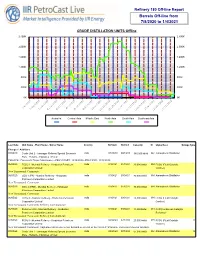

Barrels Off-Line from 7/8/2020 to 1/4/2021

Refinery 180 Off-line Report Barrels Off-line from 7/8/2020 to 1/4/2021 CRUDE DISTILLATION UNITS Offline 2,400K 2,400K 2,000K 2,000K 1,600K 1,600K 1,200K 1,200K 800K 800K 400K 400K 0K 0K 7/8/2020 9/1/2020 7/19/20207/30/20208/10/20208/21/2020 9/12/20209/23/202010/4/2020 11/6/2020 12/9/2020 10/15/202010/26/2020 11/17/202011/28/2020 12/20/202012/31/2020 Australia Central Asia Middle East North Asia South Asia Southeast Asia Last Date Unit Name - Plant Name - Owner Name Country TA Start TA End Capacity St Utype Desc Outage Type Changes / Additions 07/08/20 Crude Unit 2 - Jamnagar Refinery Special Economic India 07/20/20 08/18/20 380,000 bbl/d GU Atmospheric Distillation Zone - Reliance Industries Limited CHANGE: Comments: Major Maintenance--PREVSTART: 10/14/2020--PREVEND: 11/12/2020 06/05/20 FCCU I - Mumbai Refinery - Hindustan Petroleum India 01/04/21 01/15/21 20,000 bbl/d MH FCCU (Fluid Catalytic Corporation Limited Cracker) New Turnaround: Comments: 06/05/20 CDU 1 (FR) - Mumbai Refinery - Hindustan India 01/04/21 03/04/21 80,000 bbl/d MH Atmospheric Distillation Petroleum Corporation Limited New Turnaround: Comments: 06/05/20 CDU 2 (FRE) - Mumbai Refinery - Hindustan India 01/04/21 01/15/21 70,000 bbl/d MH Atmospheric Distillation Petroleum Corporation Limited New Turnaround: Comments: 06/05/20 FCCU II - Mumbai Refinery - Hindustan Petroleum India 01/04/21 03/04/21 28,000 bbl/d MH FCCU (Fluid Catalytic Corporation Limited Cracker) New Turnaround: Comments: Refinery wide shutdown 06/05/20 Reformer Unit - Mumbai Refinery - Hindustan India 01/04/21 03/04/21 11,000 bbl/d MH CCR(Continuous Catalytic Petroleum Corporation Limited Reformer) New Turnaround: Comments: Refinery wide shutdown 07/08/20 FCCU I - Mumbai Refinery - Hindustan Petroleum India 04/26/20 07/18/20 20,000 bbl/d MH FCCU (Fluid Catalytic U Corporation Limited Cracker) New Turnaround: Comments: Unplanned derate due to low demand as a result of the Covid-19 Pandemic and issue in reactor internals. -

Reduction of Greenhouse Gas Emissions from the Oil Refining and Petrochemical Industry Reference Number: PH3/8 Date Issued: June 1999

The reduction of greenhouse gas emission from the oil refining and petrochemical industry Report Number PH3/8 June 1999 This document has been prepared for the Executive Committee of the Programme. It is not a publication of the Operating Agent, International Energy Agency or its Secretariat. Title: The reduction of greenhouse gas emissions from the oil refining and petrochemical industry Reference number: PH3/8 Date issued: June 1999 Other remarks: Background to the Study The IEA Greenhouse Gas R&D programme (IEA GHG) is systematically evaluating the cost and potential for reducing emissions of greenhouse gases arising from anthropogenic activities, especially the use of fossil fuels. Greenhouse gases are produced from a variety of industrial activities. The main sources, not related to power generation, are those energy intensive industries, which chemically or physically transform materials from one state to another. During these processes, many greenhouse gases (carbon dioxide, methane, nitrous oxide) are released. One notable example is oil refining and petrochemicals where considerable amounts of greenhouse gases are produced. Relatively little attention has been focused on the abatement/mitigation of greenhouse gas emissions from the industrial sector. This study is the second in a series looking at greenhouse gas abatement/mitigation options for energy intensive industries. Carbon dioxide, methane and other hydrocarbons are emitted during the refining of oil, production of petrochemicals and the storage of feedstocks and products. The purpose of this study is to consider the abatement/mitigation options in the oil refining and petrochemicals industry. The study was carried out by AEA Technology of the United Kingdom. -

Annual Report 2014

Annual Report 2014 for the year ended March 31, 2014 AcceleratingAccelerating thethe PacePace ofof ReformReform toto RealizeRealize OurOur GoalsGoals President, Chief Executive Offi cer KEIZO MORIKAWA The Cosmo Oil Group is actively in crude oil development, petrochem- engaged in carrying out its fi ve-year icals, and renewable energy. The Medium-Term Management Plan Cosmo Oil Group is driven by its launched in April 2013. In order to mission to fulfi ll the diverse needs of build a robust operating platform society by ensuring the stable supply and transition to a new business of energy. With this as our guiding structure, the Group is working to light, we will embark on a new jour- regain profi tability in the refi ning ney to become a vertically integrated and marketing sector while accelerat- global energy company from a ing the pace at which it expands its long-term perspective. business portfolio, including activities Disclaimer: FORWARD-LOOKING STATEMENTS Certain statements made and information contained herein constitute “forward-looking information” (within the meaning of applicable Japanese securities legislation). Such statements and information (together, “forward looking statements”) relate to future events or the Company’s future performance, business prospects or opportunities. Forward-looking statements include, but are not limited to, statements with respect to estimates of reserves and or resources, future production levels, future capital expenditures and their allocation to exploration and development activities, future drilling and other exploration and development activities, ultimate recovery of reserves or resources and dates by which certain areas will be explored, devel- oped or reach expected operating capacity, that are based on forecasts of future results, estimates of amounts not yet determinable and assumptions of management. -

Annual Report 2015 PETROCHEMICAL BUSINESS WIND POWER GENERATION BUSINESS

What sets COSMO Energy Group apart? OIL EXPLORATION AND PRODUCTION BUSINESS PETROLEUM BUSINESS • The Cosmo Oil Company spun off its oil E&P business • Crude oil production volume: 38,031 barrels/day Total Refi ning Capacity (Barrels/day) Marketing Structure by Petroleum Products Features and established Cosmo Energy Exploration & • Crude Reserves Estimate: Total proved and probable • Chiba Refi nery 220,000 Petroleum Product SSs Companies Overseas in Japan in Japan Export Production Co., Ltd. reserves: 167.6 million barrels • Yokkaichi Refi nery 132,000 LP gas © • Announced details of an oil reserves assessment • Reserves-to-production ratio of total proved and • Sakai Refi nery 100,000 • Signed a memorandum of agreement in relation to probable reserves: Approx. 26 years Gasoline © v Total 452,000 strategic comprehensive cooperation with Compañía • New Hail Oil Field: Production scheduled to com- Naphtha © Española de Petróleos, S.A.U. (CEPSA), a major mence from the second half of fi scal 2016. The • Established a joint organization called Keiyo Seisei JV G.K. Kerosene © © integrated oil company based in Spain new Hail Oil Field is expected to produce roughly with TonenGeneral Sekiyu K.K. in January 2015 in order to Jet fuel © v • Cosmo Energy Exploration & Production sold part of the same amount as the other current existing oil increase effi ciency and optimize operations at respective Diesel fuel © © refi neries in Chiba. its stake in the newly established Cosmo Abu Dhabi fi elds of Abu Dhabi Oil Company. Heavy fuel oil A © • Took steps to strengthen competitiveness and decided to Energy Exploration & Production Co., Ltd. -

JCCP NEWS No. 103 February 2009

JCCP NEWS Newsletter of Japan Cooperation Center, Petroleum Topics No. 103 February 2009 H.E. Dr. Maitha Al-Shamsi, In this issue: UAE Minister of State, Topics Visits Japan H.E. Dr. Maitha Al-Shamsi Visits Japan 1 Visits to SE Asia and the Middle East by Mr. Sase 5 Signing Ceremony with QP 11 “Maintenance & Safety Management” for Saudi Aramco 13 JCCP Participants Surpass 18,000 18 Personnel Exchange Programs CPJ on “Refinery Computerization” (CDB OGI) 19 CPJ on “Energy Saving” (LUKOIL) 22 CPO on “Upgrading Process of Heavy Oil” in Colombia and TC Program in Brazil 26 CPO on “HRM” for Kuwait & UAE 29 TC Program in Russia & Azerbaijan 35 TC Program in Iran, Kuwait, Saudi Arabia, Bahrain 38 Dr. Al-Shamsi at JCCP, with Mr. Masataka Sase, Executive Director of JCCP Participant’s Voice 42 JCCP Regular Courses Completed October – December 2008 44 As part of the FY2008 JCCP VIP Invitation Program, JCCP has Technical Cooperation invited H.E. Dr. Maitha Al-Shamsi, UAE Minister of State, to Japan, 18th Saudi-Japan Joint Symposium 46 from November 15 to 21, 2008. Project on In-SAR Technology Before being appointed to Minister of State and Research Advisor at Application in Saudi Arabia 48 UAE University in February 2008, Dr. Al-Shamsi has held prominent Study on Improving Reactor positions at the university. She assumed the positions of Deputy Vice Efficiency in Iran 50 Chancellor in 1990, Vice Chancellor in 2000, and Assistant Provost SQU-Japan Projects Introduced in SQU’s Newsletter 51 for Research in 2004. In these capacities, she actively promoted the Announcement development of higher education in UAE and has made a significant Personnel Changes 52 number of achievements in that area. -

Gulf Asia Bulletin.Indd

A 2 I N r b P 0 s O e u R 1 s s l I 3 u 6 e l L e GULF ASIA a e r t c i h n Asia’s presence in the Gulf region has to the IMF 2011 rankings. This growth politics, economics and security relating in recent years expanded beyond the PZ YLÅLJ[LK PU H Z[YVUNLY HUK TVYL to the GCC states as well as other traditional areas of trade and investment, visible presence in the Gulf region, not countries of the region including Iran and to an increasingly wide range of only in energy-related trade but also Iraq. We believe that we are well placed areas including energy security and across a growing number of sectors. to contribute to the understanding of RUV^SLKNLIHZLKPUK\Z[YPLZ9LÅLJ[PUN The Kingdom of Saudi Arabia remains both short-term and long-term strategic [OL L_WHUZPVU VM (ZPH»Z PUÅ\LUJL the biggest economy in the Gulf region. issues relating to GCC-Asia relations. the Gulf Research Center (GRC) has Japan has been the largest investor from extended its focus to studying the Gulf- Asia into the Kingdom between 2009 This GCC-Asia bulletin, which is to be Asia relationship in-depth. and 2010, with China, Malaysia, and produced bi-annually, seeks to address Republic of Korea following. Historically, [OLJ\YYLU[PUMVYTH[PVUKLÄJP[PU[OLHYLH Among the areas of interest for GRC Japan’s investments were almost of GCC-Asia relations through analytical are international relations and energy exclusively targeted towards the power/ and incisive articles. -

Energy Security of APEC Economies and Changing Downstream Oil Environment

Energy Security of APEC Economies and Changing Downstream Oil Environment APEC Energy Working Group August 2018 APEC Project: EWG 05 2016S Produced by Dr Ken Koyama, Mr. Ichiro Kutani, Mr Takashi Matsumoto and Mr Tadashi Yoshida Asia Pacific Energy Research Centre (APERC) Institute of Energy Economics, Japan Inui Building, Kachidoki 11F, 1-13-1 Kachidoki Chuo-ku, Tokyo 104-0054 Japan Tel: (813) 5144-8551 Fax: (813) 5144-8555 Email: [email protected] (administration) Website: http://aperc.ieej.or.jp/ For Asia-Pacific Economic Cooperation Secretariat 35 Heng Mui Keng Terrace Singapore 119616 Tel: (65) 68919 600 Fax: (65) 68919 690 Email: [email protected] Website: www.apec.org ©2018 APEC Secretariat APEC#218-RE-01.10 ISBN: 978-981-11-8392-8 ii Foreword Energy security is the talk of the town whenever petroleum prices increase or decrease rapidly. In recent years, the increase in non-OPEC crude oil production by key players such as Russia and the United States has triggered a decline in crude oil prices. In response, OPEC attempted to encourage cooperation from non-OPEC economies to stabilize the oil prices. In addition, OPEC is shifting from selling crude oil to producing value-added products, as well as participating in refinery construction projects in consuming economies in order to secure a stable crude oil market. In contrast, on the demand side, the construction of refineries is falling short of the growth in oil demand while petroleum product trading is expanding globally, particularly in developing Asia. This research is jointly conducted by Strategy Research Unit of IEEJ and Asia Pacific Energy Research Centre (APERC) to identify new policy actions and concepts of oil security that can lead to the improvement of oil security in APEC economies. -

Energy Security of APEC Economies and Changing Downstream Oil Environment Michael Ochoada Sinocruz Chrisnawan Anditya Luis Camacho Beas

APEC Oil and Gas Security Studies Series 14 APEC OilAPEC and Oil Gas and Security Gas Security Studies Studies Energy Security of APEC Economies and Changing Downstream Oil Environment Michael Ochoada Sinocruz Chrisnawan Anditya Luis Camacho Beas Energy Security of APEC Economies and Changing Downstream Oil Environment Yoshikazu Kobayashi Tomoko Matsumoto APEC Energy Working Group EWG 05 2016S Produced by Series Asia Pacific Energy Research Centre (APERC) Institute of Energy Economics, Japan Inui Building, Kachidoki 11F, 1-13-1 Kachidoki August 201814 Chuo-ku, Tokyo 104-0054 Japan Tel: (813) 5144-8551 Fax: (813) 5144-8555 E-mail: [email protected] (administration) Website: http://aperc.ieej.or.jp/ For APEC Energy Working Group 2018 Asia-Pacific Economic Cooperation Secretariat 35 Heng Mui Keng Terrace Singapore 119616 Tel: (65) 68919 600 Fax: (65) 68919 690 Email: [email protected] Website: www.apec.org © 2018 APEC Secretariat APEC#218-RE-01.10 ISBN: 978-981-11-8392-8 Photographs credited by APERC APEC Oil and Gas Security Studies Series 14 APEC OilAPEC and Oil Gas and Security Gas Security Studies Studies Energy Security of APEC Economies and Changing Downstream Oil Environment Michael Ochoada Sinocruz Chrisnawan Anditya Luis Camacho Beas Energy Security of APEC Economies and Changing Downstream Oil Environment Yoshikazu Kobayashi Tomoko Matsumoto APEC Energy Working Group EWG 05 2016S Produced by Series Asia Pacific Energy Research Centre (APERC) Institute of Energy Economics, Japan Inui Building, Kachidoki 11F, 1-13-1 Kachidoki August -

Decouple Or Degrowth: Integrated Thinking Needed to Transform Systemic Risks Into Sources of Low Carbon Growth CDP Japan 500 Climate Change Report 2013

Decouple or degrowth: integrated thinking needed to transform systemic risks into sources of low carbon growth CDP Japan 500 Climate Change Report 2013 6 November 2013 Scoring partner and report writer The evolution of CDP With great pleasure, CDP announced an exciting change this year. Over ten years ago CDP pioneered the only global disclosure system for companies to report their environmental impacts and strategies to investors. In that time, and with your support, CDP has accelerated climate change and natural resource issues to the boardroom and has moved beyond the corporate world to engage with cities and governments. The CDP platform has evolved significantly, supporting multinational purchasers to build more sustainable supply chains. It enables cities around the world to exchange information, take best practice action and build climate resilience. We assess the climate performance of companies and drive improvements through shareholder engagement. Our offering to the global marketplace has expanded to cover a wider spectrum of the earth’s natural capital, specifically water and forests, alongside carbon, energy and climate. For these reasons, we have outgrown our former name of the Carbon Disclosure Project and rebranded to CDP. Many of you already know and refer to us in this way. Our rebrand denotes our progress as we continue to catalyze action and respond to business, finance, investment and environmental needs globally. We now have a bolder, more dynamic look and logo that reflects the scale of the work we must undertake in the coming years to move the markets ahead of where they would otherwise be on these issues and realize truly sustainable economies. -

Transparency Report 2015

KPMG AZSA LLC Transparency Report 2015 As at 30 June 2015 © 2015 KPMG AZSA LLC, a limited liability audit corporation incorporated under the Japanese Certified Public Accountants Law and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Transparency Report 2015 Content Message from the Managing Partner 3 1. Who we are 4 1.1 Our business 4 1.2 Our strategy 4 2. Our structure and governance 4 2.1 Legal structure 4 2.2 Name and ownership 4 2.3 Governance structure 5 3. System of quality control 5 3.1 Tone at the top – the foundation of audit quality 7 3.1.1 Leadership responsibilities for quality and risk management 8 3.2 Association with the right clients 8 3.2.1 Acceptance and continuance of clients and engagements 8 3.2.2 Prospective client and engagement evaluation process 8 3.2.3 Continuance process 9 3.2.4 Client portfolio management 9 3.3 Clear standards and robust audit tools 9 3.3.1 Audit methodology and tools 10 3.3.2 Independence, integrity, ethics and objectivity 11 3.4 Recruitment, development and assignment of appropriately qualified personnel 13 3.4.1 Recruitment 13 3.4.2 Personal development 14 3.4.3 Performance evaluation and compensation 14 3.4.4 Partner admissions 14 3.4.5 Assignment 15 3.5 Commitment to technical excellence and quality service delivery 15 3.5.1 Technical training 15 3.5.2 Accreditation and licensing 16 3.5.3 Access to specialist networks 16 3.5.4 Consultation 16 3.5.5 Developing business understanding and industry knowledge 17 3.6 Performance of effective and efficient audits 17 3.6.1 KPMG Audit Process 17 3.6.2 Client confidentiality, information security and data privacy 20 3.7 Commitment to continuous improvement 21 3.7.1 Monitoring 21 3.8.2 Client feedback 22 4.