Decouple Or Degrowth: Integrated Thinking Needed to Transform Systemic Risks Into Sources of Low Carbon Growth CDP Japan 500 Climate Change Report 2013

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

ED-7311-20.Pdf

EIAJ ED-7311-20 - 1 - EIAJ ED-7311-20 - 2 - EIAJ ED-7311-20 - 3 - EIAJ ED-7311-20 - 4 - EIAJ ED-7311-20 - 5 - EIAJ ED-7311-20 - 6 - EIAJ ED-7311-20 - 7 - EIAJ ED-7311-20 - 8 - EIAJ ED-7311-20 - 9 - EIAJ ED-7311-20 - 10 - EIAJ ED-7311-20 - 11 - EIAJ ED-7311-20 - 12 - EIAJ ED-7311-20 - 13 - EIAJ ED-7311-20 - 14 - EIAJ ED-7311-20 - 15 - EIAJ ED-7311-20 - 16 - EIAJ ED-7311-20 - 17 - EIAJ ED-7311-20 - 18 - EIAJ ED-7311-20 - 19 - EIAJ ED-7311-20 - 20 - EIAJ ED-7311-20 - 21 - EIAJ ED-7311-20 - 22 - EIAJ ED-7311-20 - 23 - EIAJ ED-7311-20 - 24 - EIAJ ED-7311-20 - 25 - EIAJ ED-7311-20 - 26 - EIAJ ED-7311-20 - 27 - EIAJ ED-7311-20 - 28 - EIAJ ED-7311-20 - 29 - EIAJ ED-7311-20 - 30 - EIAJ ED-7311-20 - 31 - EIAJ ED-7311-20 - 32 - EIAJ ED-7311-20 - 33 - EIAJ ED-7311-20 - 34 - EIAJ ED-7311-20 - 35 - EIAJ ED-7311-20 - 36 - EIAJ ED-7311-20 - 37 - EIAJ ED-7311-20 - 38 - EIAJ ED-7311-20 - 39 - EIAJ ED-7311-20 - 40 - EIAJ ED-7311-20 - 41 - EIAJ ED-7311-20 - 42 - EIAJ ED-7311-20 - 43 - EIAJ ED-7311-20 - 44 - EIAJ ED-7311-20 - 45 - EIAJ ED-7311-20 - 46 - EIAJ ED-7311-20 - 47 - EIAJ ED-7311-20 - 48 - EIAJ ED-7311-20 - 49 - EIAJ ED-7311-20 - 50 - EIAJ ED-7311-20 - 51 - EIAJ ED-7311-20 - 52 - EIAJ ED-7311-20 - 53 - EIAJ ED-7311-20 - 54 - EIAJ ED-7311-20 - 55 - EIAJ ED-7311-20 - 56 - EIAJ ED-7311-20 - 57 - EIAJ ED-7311-20 - 58 - EIAJ ED-7311-20 - 59 - EIAJ ED-7311-20 - 60 - EIAJ ED-7311-20 - 61 - EIAJ ED-7311-20 - 62 - EIAJ ED-7311-20 - 63 - EIAJ ED-7311-20 - 64 - EIAJ ED-7311-20 - 65 - EIAJ ED-7311-20 - 66 - EIAJ ED-7311-20 - 67 - EIAJ ED-7311-20 - 68 - EIAJ -

Disaster Management of India

DISASTER MANAGEMENT IN INDIA DISASTER MANAGEMENT 2011 This book has been prepared under the GoI-UNDP Disaster Risk Reduction Programme (2009-2012) DISASTER MANAGEMENT IN INDIA Ministry of Home Affairs Government of India c Disaster Management in India e ACKNOWLEDGEMENT The perception about disaster and its management has undergone a change following the enactment of the Disaster Management Act, 2005. The definition of disaster is now all encompassing, which includes not only the events emanating from natural and man-made causes, but even those events which are caused by accident or negligence. There was a long felt need to capture information about all such events occurring across the sectors and efforts made to mitigate them in the country and to collate them at one place in a global perspective. This book has been an effort towards realising this thought. This book in the present format is the outcome of the in-house compilation and analysis of information relating to disasters and their management gathered from different sources (domestic as well as the UN and other such agencies). All the three Directors in the Disaster Management Division, namely Shri J.P. Misra, Shri Dev Kumar and Shri Sanjay Agarwal have contributed inputs to this Book relating to their sectors. Support extended by Prof. Santosh Kumar, Shri R.K. Mall, former faculty and Shri Arun Sahdeo from NIDM have been very valuable in preparing an overview of the book. This book would have been impossible without the active support, suggestions and inputs of Dr. J. Radhakrishnan, Assistant Country Director (DM Unit), UNDP, New Delhi and the members of the UNDP Disaster Management Team including Shri Arvind Sinha, Consultant, UNDP. -

FY2008 Results Meeting

FY200FY20088 ResultsResults MeetingMeeting FY2008 : Year ended March 31, 2009 May 14, 2009 Ryosan Company, Limited Code : 8140 / Stock listings: Tokyo Stock Exchange (First Section) URL : http://www.ryosan.co.jp/eng/ Notice This presentation contains forward-looking statements regarding business performance, which may differ substantially from actual results, depending on certain risks and uncertainties, the most significant of which are listed below. z Economic conditions in key markets (Japan and the rest of Asia), rapid changes in consumption patterns and supply-demand balance for products z Sharp fluctuations in the ¥/$ exchange rate z Substantial fluctuation in prices in capital markets Consolidated results for FY 2008 FY2007 FY2008 FY2009(Forecasts) Of Total Of Total % Chg. YoY Of Total % Chg. YoY ¥ 100 million% ¥ 100 million%% ¥ 100 million %% Net sales 2,860 2,208 (22.8) 1,700 (23.0) Gross margin 251 8.8 196 8.9 (22.1) 149 8.8 (24.1) SG&A expenses 144 5.0 134 6.1 (6.8) 115 6.8 (14.7) Operating income 107 3.8 61 2.8 (42.8) 34 2.0 (44.7) Ordinary income 112 3.9 72 3.3 (35.6) 38 2.2 (47.7) Net income 67 2.4 39 1.8 (41.8) 22 1.3 (43.9) Earnings per share ¥187.15 ¥111.83 (¥75) ¥63.83 (¥48) 1 Segment results for FY2008 Unit : ¥ 100 million FY2007 FY2008 FY2009(Forecasts) OP OP OP Margin Margin % Chg. YoYMargin % Chg. YoY % % Sales 1,489 1,169 (21.5) 808 (30.9) Semiconductors Operating income 724.9% 48 4.2%(32.7) 28 3.5% (42.7) Electronic Sales 1,031 759 (26.4) 584 (23.1) Components Operating income 444.3 28 3.7 (35.9) 22 3.8 (22.1) -

Published on 7 October 2016 1. Constituents Change the Result Of

The result of periodic review and component stocks of TOPIX Composite 1500(effective 31 October 2016) Published on 7 October 2016 1. Constituents Change Addition( 70 ) Deletion( 60 ) Code Issue Code Issue 1810 MATSUI CONSTRUCTION CO.,LTD. 1868 Mitsui Home Co.,Ltd. 1972 SANKO METAL INDUSTRIAL CO.,LTD. 2196 ESCRIT INC. 2117 Nissin Sugar Co.,Ltd. 2198 IKK Inc. 2124 JAC Recruitment Co.,Ltd. 2418 TSUKADA GLOBAL HOLDINGS Inc. 2170 Link and Motivation Inc. 3079 DVx Inc. 2337 Ichigo Inc. 3093 Treasure Factory Co.,LTD. 2359 CORE CORPORATION 3194 KIRINDO HOLDINGS CO.,LTD. 2429 WORLD HOLDINGS CO.,LTD. 3205 DAIDOH LIMITED 2462 J-COM Holdings Co.,Ltd. 3667 enish,inc. 2485 TEAR Corporation 3834 ASAHI Net,Inc. 2492 Infomart Corporation 3946 TOMOKU CO.,LTD. 2915 KENKO Mayonnaise Co.,Ltd. 4221 Okura Industrial Co.,Ltd. 3179 Syuppin Co.,Ltd. 4238 Miraial Co.,Ltd. 3193 Torikizoku co.,ltd. 4331 TAKE AND GIVE. NEEDS Co.,Ltd. 3196 HOTLAND Co.,Ltd. 4406 New Japan Chemical Co.,Ltd. 3199 Watahan & Co.,Ltd. 4538 Fuso Pharmaceutical Industries,Ltd. 3244 Samty Co.,Ltd. 4550 Nissui Pharmaceutical Co.,Ltd. 3250 A.D.Works Co.,Ltd. 4636 T&K TOKA CO.,LTD. 3543 KOMEDA Holdings Co.,Ltd. 4651 SANIX INCORPORATED 3636 Mitsubishi Research Institute,Inc. 4809 Paraca Inc. 3654 HITO-Communications,Inc. 5204 ISHIZUKA GLASS CO.,LTD. 3666 TECNOS JAPAN INCORPORATED 5998 Advanex Inc. 3678 MEDIA DO Co.,Ltd. 6203 Howa Machinery,Ltd. 3688 VOYAGE GROUP,INC. 6319 SNT CORPORATION 3694 OPTiM CORPORATION 6362 Ishii Iron Works Co.,Ltd. 3724 VeriServe Corporation 6373 DAIDO KOGYO CO.,LTD. 3765 GungHo Online Entertainment,Inc. -

1332:Xtks Nippon Suisan Kaisha Ltd 3 4 1 1334:Xtks Maruha Nichiro Holdings Inc. 3 4 1 1377:Xtks Sakata Seed Corp. 3 5 2 1414:Xtks SHO-BOND Holdings Co

Symbol Code Description Current Rating New rating Diff 1332:xtks Nippon Suisan Kaisha Ltd 3 4 1 1334:xtks Maruha Nichiro Holdings Inc. 3 4 1 1377:xtks Sakata Seed Corp. 3 5 2 1414:xtks SHO-BOND Holdings Co. Ltd 3 6 3 1766:xtks TOKEN Corp. 3 6 3 1801:xtks Taisei Corp. 3 5 2 1803:xtks Shimizu Corp. 3 4 1 1808:xtks Haseko Corp. 3 4 1 1812:xtks Kajima Corp. 3 5 2 1820:xtks Nishimatsu Construction Co. Ltd 3 6 3 1824:xtks Maeda Corp. 3 6 3 1833:xtks Okumura Corp. 3 6 3 1860:xtks Toda Corp. 3 5 2 1861:xtks Kumagai Gumi Co. Ltd 3 8 5 1865:xtks Asunaro Aoki Construction Co. Ltd 3 6 3 1870:xtks Yahagi Construction Co. Ltd 3 4 1 1881:xtks NIPPO Corp. 3 6 3 1883:xtks Maeda Road Construction Co. Ltd 3 6 3 1911:xtks Sumitomo Forestry Co Ltd 3 4 1 1924:xtks PanaHome Corp. 3 4 1 1925:xtks Daiwa House Industry Co. Ltd 3 4 1 1928:xtks Sekisui House Ltd 3 4 1 1934:xtks YURTEC Corp. 3 6 3 1945:xtks Tokyo Energy & Systems Inc. 3 4 1 1961:xtks Sanki Engineering Co. Ltd 3 4 1 1963:xtks JGC Corporation 3 4 1 1968:xtks Taihei Dengyo Kaisha Ltd 3 4 1 1969:xtks Takasago Thermal Engineering Co. Ltd 3 4 1 1973:xtks NEC Networks & System Integration Corp. 3 5 2 1979:xtks Taikisha Ltd 3 4 1 1983:xtks TOSHIBA PLANT SYSTEMS & SERVICES Corp. -

Synthesis Report

MEGA DISASTER IN A RESILIENT SOCIETY The Great East Japan (Tohoku Kanto) Earthquake and Tsunami of 11th March 2011 SYNTHESIS AND INITIAL OBSERVATIONS International Environment and Disaster Management Graduate School of Global Environmental Studies Kyoto University 25th March 2011 About this Report This report is published on 25th of March 2011, two weeks after the Great East Japan [Tohoku-Kanto] Earthquake and Tsunami. The aim of the report is to synthesize certain existing data with basic situation analysis. The disaster has posed a major challenge to the disaster risk reduction community, which needs to be discussed in future over the course of time. Assistance of Yukiko Takeuchi for providing information, and Kumiko Fujita and Yuta suda in translating parts of the Japanese information is acknowledged. Team Members (Kyoto University) Sunil Parashar Noralene Uy Huy Nguyen Glenn Fernandez Farah Mulyasari Jonas Joerin Rajib Shaw Contact Details Rajib Shaw Associate Professor International Environment and Disaster Management Laboratory, KYOTO UNIVERSITY Yoshida Honmachi, Sakyo-Ku, Kyoto 606-8501, Japan Tel/Fax: 81-75-753-5708 E-mail: [email protected] Web: http://www.iedm.ges.kyoto-u.ac.jp/ Disclaimer The views expressed in this report are the views of the team members and do not necessarily reflect the views or policies of the research field for International Environment & Disaster Management (IEDM) or the Graduate School of Global Environment Studies (GSGES), or Kyoto University, or the organizations, or the countries cited. The report is a compilation from available sources, which are acknowledged. IEDM does not guarantee the accuracy of the data included in this volume and accept no responsibility for any consequences of their use. -

Portfolio of Investments

PORTFOLIO OF INVESTMENTS Variable Portfolio – Partners International Value Fund, September 30, 2020 (Unaudited) (Percentages represent value of investments compared to net assets) Investments in securities Common Stocks 97.9% Common Stocks (continued) Issuer Shares Value ($) Issuer Shares Value ($) Australia 4.2% UCB SA 3,232 367,070 AMP Ltd. 247,119 232,705 Total 13,350,657 Aurizon Holdings Ltd. 64,744 199,177 China 0.6% Australia & New Zealand Banking Group Ltd. 340,950 4,253,691 Baidu, Inc., ADR(a) 15,000 1,898,850 Bendigo & Adelaide Bank Ltd. 30,812 134,198 China Mobile Ltd. 658,000 4,223,890 BlueScope Steel Ltd. 132,090 1,217,053 Total 6,122,740 Boral Ltd. 177,752 587,387 Denmark 1.9% Challenger Ltd. 802,400 2,232,907 AP Moller - Maersk A/S, Class A 160 234,206 Cleanaway Waste Management Ltd. 273,032 412,273 AP Moller - Maersk A/S, Class B 3,945 6,236,577 Crown Resorts Ltd. 31,489 200,032 Carlsberg A/S, Class B 12,199 1,643,476 Fortescue Metals Group Ltd. 194,057 2,279,787 Danske Bank A/S(a) 35,892 485,479 Harvey Norman Holdings Ltd. 144,797 471,278 Demant A/S(a) 8,210 257,475 Incitec Pivot Ltd. 377,247 552,746 Drilling Co. of 1972 A/S (The)(a) 40,700 879,052 LendLease Group 485,961 3,882,083 DSV PANALPINA A/S 15,851 2,571,083 Macquarie Group Ltd. 65,800 5,703,825 Genmab A/S(a) 1,071 388,672 National Australia Bank Ltd. -

UNO Template

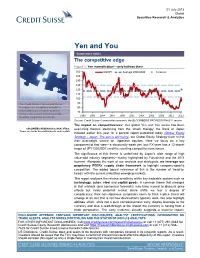

01 July 2013 Global Securities Research & Analytics Yen and You Connections Series The competitive edge Figure 1: Yen 'normalisation'—only halfway there 160 USDJPY Average 1990-2008 Forecast 150 140 130 120 110 100 The Credit Suisse Connections Series 90 leverages our exceptional breadth of 80 macro and micro research to deliver 70 incisive cross-sector and cross-border 1990 1992 1994 1997 1999 2001 2004 2006 2008 2011 2013 thematic insights for our clients. Source: Credit Suisse Commodities research, the BLOOMBERG PROFESSIONAL™ service The impact on competitiveness: Our global Yen and You series has been SECURITIES RESEARCH & ANALYTICS examining themes stemming from the 'shock therapy' the Bank of Japan Please see inside for contributors to each section initiated earlier this year. In a parallel report published today (Global Equity Strategy - Japan: The sun is still rising), our Global Equity Strategy team revisit their overweight stance on Japanese equities. Here we focus on a key component of that view—a structurally weak yen (our FX team has a 12-month target of JPY120/USD1) and the resulting competitiveness issues. The significance of this theme is underlined by Japan's wide range of high value-add industry segments—starkly highlighted by Fukushima and the 2011 tsunami. Alongside the work of our analysts and strategists, we leverage our proprietary PEERs supply chain framework to highlight company-specific competition. The added topical relevance of this is the number of 'head-to- heads' with the current embattled emerging markets. This report analyses the relative sensitivity within key tradeable sectors such as technology, autos, steel and capital goods. -

Istoxx® Mutb Japan Momentum 300 Index

ISTOXX® MUTB JAPAN MOMENTUM 300 INDEX Components1 Company Supersector Country Weight (%) Z HOLDINGS Technology Japan 0.69 M3 Health Care Japan 0.65 KOEI TECMO HOLDINGS Technology Japan 0.65 MENICON Health Care Japan 0.59 CAPCOM Technology Japan 0.58 FUJITEC Industrial Goods & Services Japan 0.56 Ibiden Co. Ltd. Industrial Goods & Services Japan 0.56 NIPPON PAINT HOLDINGS Chemicals Japan 0.56 RENESAS ELECTRONICS Technology Japan 0.55 JEOL Industrial Goods & Services Japan 0.55 INTERNET INTV.JAPAN Technology Japan 0.53 JSR Corp. Chemicals Japan 0.52 NET ONE SYSTEMS Technology Japan 0.51 Fujitsu Ltd. Technology Japan 0.51 Bank of Kyoto Ltd. Banks Japan 0.51 Hokuhoku Financial Group Inc. Banks Japan 0.51 FUJITSU GENERAL Personal & Household Goods Japan 0.50 Iyo Bank Ltd. Banks Japan 0.50 Kyushu Financial Group Banks Japan 0.50 77 Bank Ltd. Banks Japan 0.49 COCOKARA FINE INC. Retail Japan 0.49 TOSHIBA TEC Industrial Goods & Services Japan 0.48 JCR PHARMACEUTICALS Health Care Japan 0.48 MONOTARO Retail Japan 0.48 COSMOS PHARM. Retail Japan 0.48 Tokyo Electron Ltd. Technology Japan 0.48 Nomura Research Institute Ltd. Technology Japan 0.48 Olympus Corp. Health Care Japan 0.47 SUNDRUG Retail Japan 0.47 Chiba Bank Ltd. Banks Japan 0.47 NEC NETWORKS & SY.INTG. Technology Japan 0.47 Nomura Holdings Inc. Financial Services Japan 0.47 TOKYO OHKA KOGYO Technology Japan 0.47 PENTA-OCEAN CONSTRUCTION Construction & Materials Japan 0.47 FUYO GENERAL LEASE Financial Services Japan 0.46 FUJI Industrial Goods & Services Japan 0.46 Hachijuni Bank Ltd. -

Portfolio of Investments

PORTFOLIO OF INVESTMENTS CTIVP® – Lazard International Equity Advantage Fund, March 31, 2020 (Unaudited) (Percentages represent value of investments compared to net assets) Investments in securities Common Stocks 96.4% Common Stocks (continued) Issuer Shares Value ($) Issuer Shares Value ($) Australia 6.4% Legrand SA 131,321 8,375,908 AGL Energy Ltd. 880,686 9,216,678 L’Oreal SA 104,607 27,073,419 Aristocrat Leisure Ltd. 728,775 9,443,206 Orange SA 949,535 11,496,452 ASX Ltd. 162,820 7,642,885 Peugeot SA 1,014,598 13,209,331 BHP Group Ltd. 471,264 8,549,345 Schneider Electric SE 553,434 46,777,833 CIMIC Group Ltd. 332,784 4,713,315 STMicroelectronics NV 400,446 8,608,225 CSL Ltd. 166,037 30,097,798 Total SA 1,095,152 41,264,011 Fortescue Metals Group Ltd. 4,669,354 28,614,857 Total 209,274,345 (a),(b) IDP Education Ltd. 447,152 3,487,548 Germany 4.2% Inghams Group Ltd. 1,200,179 2,405,115 Adidas AG 22,586 5,014,708 Magellan Financial Group Ltd. 729,823 19,356,167 Allianz SE, Registered Shares 319,746 54,451,936 Regis Resources Ltd. 1,318,187 2,929,557 Continental AG 32,324 2,304,645 Santos Ltd. 4,606,425 9,460,470 Dialog Semiconductor PLC(c) 82,878 2,154,248 (c) Saracen Mineral Holdings Ltd. 3,513,246 7,900,242 Hugo Boss AG 273,602 6,848,821 Technology One Ltd. 897,813 4,336,750 MTU Aero Engines AG 74,698 10,801,095 Total 148,153,933 SAP SE 91,344 10,198,367 Austria 0.2% Siemens Healthineers AG 179,517 6,939,504 OMV AG 81,189 2,221,890 Total 98,713,324 Raiffeisen Bank International AG 111,223 1,599,856 Hong Kong 3.9% Total 3,821,746 CK Hutchison Holdings Ltd. -

The Name of a Financial Institution JCN Address Telephone As of October

As of October 1, 2020 Business The name of JCN Address Telephone category a financial institution Bank Holding 1-9-2, Ohtemachi, Chiyoda-ku, Tokyo 100- Sony Financial Holdings Inc. 4010401053410 03-5290-6500 company 0004 Total 25 Hokuhoku Financial Group, 1-2-26 Tsutsumicho-dori, Toyama City 1230001004554 076-423-7331 companies Inc. 930-8637 1-5-5, Ohtemachi, Chiyoda-ku, Tokyo 100- Mizuho Financial Group, Inc. 9010001081419 03-5224-1111 8176 Sumitomo Mitsui Financial 1-1-2, Marunouchi, Chiyoda-ku, Tokyo 2010001081053 03-3282-8111 Group, Inc. 100-0005 Sumitomo Mitsui Trust 1-4-1,Marunouchi,Chiyoda-ku,Tokyo 100- 9010001139555 03-6256-6000 Holding, Inc. 8233 Mitsubishi UFJ Financial 2-7-1, Marunouchi, Chiyoda-ku, Tokyo 4010001073486 03-3240-8111 Group, Inc. 100-8330 Resona Holdings, Inc. 5010601039654 1-5-65, Kiba, Koto-ku, Tokyo 135-8581 03-6704-3111 Yamaguchi Financial Group, 4-2-36,Takezaki- 5250001007270 083-223-5511 Inc. cho,Shimonoseki,Yamaguchi 750-8603 Fukuoka Financial Group, 2-13-1, Ohtemon, Chuo-ku,Fukuoka,810- 9290001028986 092-723-2502 Inc. 8693 JAPAN POST HOLDINGS 2-3-1 Ohtemachi, Chiyoda-ku, Tokyo 100- 5010001112697 03-3477-0111 Co, Ltd 8791 Mebuki Financial Group,Inc. 1060001007582 2-7-2,Yaesu,Chuo-ku,Tokyo 104-0028 029-233-1151 3-1-24 Chuo Aoba-ku, Sendai, Miyagi 980- FIDEA Holdings Co.Ltd 4370001018694 022-290-8800 8800 18-14 Chayamachi, Kita-ku, Osaka 530- Senshu Ikeda Holdings,Inc 1120001140303 06-4802-0181 0013 7-1 Kameicho, Takamatsu, Kagawa 760- TOMONY Holdings, Inc. 5470001011928 087-812-0102 0050 2-1-1 Ichibancho, Aoba-ku, Sendai, Miyagi Jimoto Holdings, Inc. -

Company Response Status and Score Company Response Status and Score

2017 Company response status and score Company response status and score Key to response status: AQ Answered questionnaire AQ (NP) Answered questionnaire but response not made public AQ (SA) Company is either a subsidiary or has merged during the reporting process; see Company in parenthesis for further information AQ (L) Answered questionnaire after submission deadline DP Declined to participate NR No response RV Responded voluntarily 1 Score levels: The levels build consecutively from Disclosure to Leadership. A threshold of 75% in a lower level has to be passed before a company is scored for the next level. For more information, please see our Introduction to Scoring. A Leadership A- B Management B- C Awareness C- D Disclosure D- F: Failure to provide sufficient information to CDP to be evaluated for this purpose 2 Company Response Status Ticker Country HQ CDP Band and Score Consumer Discretionary ABC-Mart, Inc. NR 2670 JP Japan Failure to disclose (F) AccorHotels DP AC FP France Failure to disclose (F) Adastria Co., Ltd. NR 2685 JP Japan Failure to disclose (F) adidas AG AQ ADS GR Germany Leadership (A-) Advance Auto Parts Inc NR AAP US USA Failure to disclose (F) Aisin Seiki Co., Ltd. AQ (NP) 7259 JP Japan Awareness (C) AKSA AKRILIK KIMYA SANAYII A.S. DP AKSA TI Turkey Failure to disclose (F) Anta Sports Products Ltd NR 2020 HK Hong Kong Failure to disclose (F) Aoyama Trading Co., Ltd. NR 8219 JP Japan Failure to disclose (F) 1 Companies that respond voluntarily to CDP are not scored unless they request this service.