Arch Capital Group Ltd. 2015 Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Global Equity Fund Description Plan 3S DCP & JRA MICROSOFT CORP

Global Equity Fund June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA MICROSOFT CORP 2.5289% 2.5289% APPLE INC 2.4756% 2.4756% AMAZON COM INC 1.9411% 1.9411% FACEBOOK CLASS A INC 0.9048% 0.9048% ALPHABET INC CLASS A 0.7033% 0.7033% ALPHABET INC CLASS C 0.6978% 0.6978% ALIBABA GROUP HOLDING ADR REPRESEN 0.6724% 0.6724% JOHNSON & JOHNSON 0.6151% 0.6151% TENCENT HOLDINGS LTD 0.6124% 0.6124% BERKSHIRE HATHAWAY INC CLASS B 0.5765% 0.5765% NESTLE SA 0.5428% 0.5428% VISA INC CLASS A 0.5408% 0.5408% PROCTER & GAMBLE 0.4838% 0.4838% JPMORGAN CHASE & CO 0.4730% 0.4730% UNITEDHEALTH GROUP INC 0.4619% 0.4619% ISHARES RUSSELL 3000 ETF 0.4525% 0.4525% HOME DEPOT INC 0.4463% 0.4463% TAIWAN SEMICONDUCTOR MANUFACTURING 0.4337% 0.4337% MASTERCARD INC CLASS A 0.4325% 0.4325% INTEL CORPORATION CORP 0.4207% 0.4207% SHORT-TERM INVESTMENT FUND 0.4158% 0.4158% ROCHE HOLDING PAR AG 0.4017% 0.4017% VERIZON COMMUNICATIONS INC 0.3792% 0.3792% NVIDIA CORP 0.3721% 0.3721% AT&T INC 0.3583% 0.3583% SAMSUNG ELECTRONICS LTD 0.3483% 0.3483% ADOBE INC 0.3473% 0.3473% PAYPAL HOLDINGS INC 0.3395% 0.3395% WALT DISNEY 0.3342% 0.3342% CISCO SYSTEMS INC 0.3283% 0.3283% MERCK & CO INC 0.3242% 0.3242% NETFLIX INC 0.3213% 0.3213% EXXON MOBIL CORP 0.3138% 0.3138% NOVARTIS AG 0.3084% 0.3084% BANK OF AMERICA CORP 0.3046% 0.3046% PEPSICO INC 0.3036% 0.3036% PFIZER INC 0.3020% 0.3020% COMCAST CORP CLASS A 0.2929% 0.2929% COCA-COLA 0.2872% 0.2872% ABBVIE INC 0.2870% 0.2870% CHEVRON CORP 0.2767% 0.2767% WALMART INC 0.2767% -

733600137 HUM Hamilton U.S. Mid Small-Cap Financials ETF;SOI

Hamilton U.S. Mid/Small-Cap Financials ETF (HUM, HUM.U:TSX) Summary of Investment Portfolio As at March 31, 2021 % of ETF's Asset Mix Net Asset Value Net Asset Value U.S. Equities $ 45,337,253 94.02% Global Equities 3,181,073 6.60% Currency Forward Hedge* (513,777) -1.07% Cash and Cash Equivalents 338,960 0.70% Other Assets less Liabilities (121,439) -0.25% $ 48,222,070 100.00% % of ETF's Sector Mix Net Asset Value Net Asset Value Financials $ 47,831,452 99.19% Information Technology 686,874 1.43% Currency Forward Hedge* (513,777) -1.07% Cash and Cash Equivalents 338,960 0.70% Other Assets less Liabilities (121,439) -0.25% $ 48,222,070 100.00% * Positions in forward contracts are disclosed as the gain/(loss) that would be realized if the contracts were closed out on the date of this report. Hamilton U.S. Mid/Small-Cap Financials ETF (HUM, HUM.U:TSX) Summary of Investment Portfolio (continued) As at March 31, 2021 % of ETF’s Top 25 Holdings Net Asset Value Western Alliance Bancorp 3.27% Raymond James Financial Inc. 3.16% Pinnacle Financial Partners Inc. 3.09% First Horizon National Corp. 3.01% LPL Financial Holdings Inc. 2.99% Arch Capital Group Ltd. 2.93% Ares Management Corp. 2.88% Nasdaq Inc. 2.85% Ally Financial Inc. 2.83% Signature Bank 2.72% Cadence Bancorp. 2.64% Synovus Financial Corp. 2.44% Lazard Ltd. 2.27% Prosperity Bancshares Inc. 2.26% Voya Financial Inc. 2.24% WSFS Financial Corp. -

UNITED CHURCH of CHRIST, INC. SCHEDULE of INVESTMENTS June 30, 2018 Unaudited - for Information Purposes Only

THE PENSION BOARDS - UNITED CHURCH OF CHRIST, INC. SCHEDULE OF INVESTMENTS June 30, 2018 Unaudited - for information purposes only. SUMMARY OF INVESTMENTS COST VALUE STABLE VALUE INVESTMENTS Short-Term Investments $ 6,566,917 $ 6,566,917 Fixed Maturity Synthetic Guaranteed Investment Contracts 38,995,288 38,995,288 Constant Duration Synthetic Guaranteed Investment Contracts 126,234,758 126,234,758 TOTAL STABLE VALUE INVESTMENTS $ 171,796,963 $ 171,796,963 SHORT-TERM INVESTMENTS Short-term Investments $ 95,552,274 $ 95,552,274 TOTAL SHORT-TERM INVESTMENTS $ 95,552,274 $ 95,552,274 FIXED-INCOME INVESTMENTS Bonds $ 943,137,735 $ 929,127,457 Bond funds 235,065,068 238,580,280 Asset-backed & Mortgage-backed Securities 167,221,040 162,522,120 TOTAL FIXED-INCOME INVESTMENTS $ 1,345,423,843 $ 1,330,229,857 EQUITY INVESTMENTS Common stocks and equivalents $ 754,559,724 $ 1,047,247,659 Equity funds 364,289,377 398,472,808 Emerging Markets Discounted Assets 100,671,500 86,596,087 TOTAL EQUITY INVESTMENTS $ 1,219,520,601 $ 1,532,316,554 OTHER INVESTMENTS Hedge funds $ 70,137,861 $ 83,227,777 Real Assets 69,437,464 70,498,810 Participation in the United Church Funds, Inc. 38,344,068 42,641,757 TOTAL OTHER INVESTMENTS $ 177,919,393 $ 196,368,344 TOTAL INVESTMENTS $ 3,010,213,074 $ 3,326,263,992 PRINCIPAL INTEREST DESCRIPTION SERIES MATURITY COST VALUE AMOUNT RATE % SHORT-TERM INVESTMENTS MFB NI Treasury Money Market Fund $ 6,566,917 $ 6,566,917 TOTAL SHORT-TERM INVESTMENT $ 6,566,917 $ 6,566,917 FIXED MATURITY SYNTHETIC GUARANTEED INVESTMENT CONTRACTS: Asset-Backed Securities 1,155,548 AEP Texas Central Company 1.98 6/1/2021 $ 1,165,840 $ 1,144,164 1,600,000 Capital One Multi-Asset Execution Trust 1.33 6/15/2022 1,599,615 1,574,914 645,871 Carmax Auto Owner Trust 2016-1 1.61 11/16/2020 645,714 642,237 630,912 CenterPoint Energy, Inc. -

Usef-I Q2 2021

Units Cost Market Value U.S. EQUITY FUND-I U.S. Equities 88.35% Domestic Common Stocks 10X GENOMICS INC 5,585 868,056 1,093,655 1ST SOURCE CORP 249 9,322 11,569 2U INC 301 10,632 12,543 3D SYSTEMS CORP 128 1,079 5,116 3M CO 11,516 2,040,779 2,287,423 A O SMITH CORP 6,897 407,294 496,998 AARON'S CO INC/THE 472 8,022 15,099 ABBOTT LABORATORIES 24,799 2,007,619 2,874,948 ABBVIE INC 17,604 1,588,697 1,982,915 ABERCROMBIE & FITCH CO 1,021 19,690 47,405 ABIOMED INC 9,158 2,800,138 2,858,303 ABM INDUSTRIES INC 1,126 40,076 49,938 ACACIA RESEARCH CORP 1,223 7,498 8,267 ACADEMY SPORTS & OUTDOORS INC 1,036 35,982 42,725 ACADIA HEALTHCARE CO INC 2,181 67,154 136,858 ACADIA REALTY TRUST 1,390 24,572 30,524 ACCO BRANDS CORP 1,709 11,329 14,749 ACI WORLDWIDE INC 6,138 169,838 227,965 ACTIVISION BLIZZARD INC 13,175 839,968 1,257,422 ACUITY BRANDS INC 1,404 132,535 262,590 ACUSHNET HOLDINGS CORP 466 15,677 23,020 ADAPTHEALTH CORP 1,320 39,475 36,181 ADAPTIVE BIOTECHNOLOGIES CORP 18,687 644,897 763,551 ADDUS HOMECARE CORP 148 13,034 12,912 ADOBE INC 5,047 1,447,216 2,955,725 ADT INC 3,049 22,268 32,899 ADTALEM GLOBAL EDUCATION INC 846 31,161 30,151 ADTRAN INC 892 10,257 18,420 ADVANCE AUTO PARTS INC 216 34,544 44,310 ADVANCED DRAINAGE SYSTEMS INC 12,295 298,154 1,433,228 ADVANCED MICRO DEVICES INC 14,280 895,664 1,341,320 ADVANSIX INC 674 15,459 20,126 ADVANTAGE SOLUTIONS INC 1,279 14,497 13,800 ADVERUM BIOTECHNOLOGIES INC 1,840 7,030 6,440 AECOM 5,145 227,453 325,781 AEGLEA BIOTHERAPEUTICS INC 287 1,770 1,998 AEMETIS INC 498 6,023 5,563 AERSALE CORP -

Appendix D - Securities Held by Funds October 18, 2017 Annual Report of Activities Pursuant to Act 44 of 2010 October 18, 2017

Report of Activities Pursuant to Act 44 of 2010 Appendix D - Securities Held by Funds October 18, 2017 Annual Report of Activities Pursuant to Act 44 of 2010 October 18, 2017 Appendix D: Securities Held by Funds The Four Funds hold thousands of publicly and privately traded securities. Act 44 directs the Four Funds to publish “a list of all publicly traded securities held by the public fund.” For consistency in presenting the data, a list of all holdings of the Four Funds is obtained from Pennsylvania Treasury Department. The list includes privately held securities. Some privately held securities lacked certain data fields to facilitate removal from the list. To avoid incomplete removal of privately held securities or erroneous removal of publicly traded securities from the list, the Four Funds have chosen to report all publicly and privately traded securities. The list below presents the securities held by the Four Funds as of June 30, 2017. 1345 AVENUE OF THE A 1 A3 144A AAREAL BANK AG ABRY MEZZANINE PARTNERS LP 1721 N FRONT STREET HOLDINGS AARON'S INC ABRY PARTNERS V LP 1-800-FLOWERS.COM INC AASET 2017-1 TRUST 1A C 144A ABRY PARTNERS VI L P 198 INVERNESS DRIVE WEST ABACUS PROPERTY GROUP ABRY PARTNERS VII L P 1MDB GLOBAL INVESTMENTS L ABAXIS INC ABRY PARTNERS VIII LP REGS ABB CONCISE 6/16 TL ABRY SENIOR EQUITY II LP 1ST SOURCE CORP ABB LTD ABS CAPITAL PARTNERS II LP 200 INVERNESS DRIVE WEST ABBOTT LABORATORIES ABS CAPITAL PARTNERS IV LP 21ST CENTURY FOX AMERICA INC ABBOTT LABORATORIES ABS CAPITAL PARTNERS V LP 21ST CENTURY ONCOLOGY 4/15 -

Investing in Financials

BARON F I R S T Q U A R T E R 2 0 1 6 INSIGHT Investing in Financials Michael Baron, VP, Research Analyst; Josh Saltman, VP, Research Analyst; Jose Barria, Research Analyst The Financials sector has lagged significantly since the 2007-08 financial Baron has a long and successful history of utilizing its bottom-up, crisis. As of March 31, 2016, the category was down 14% since its research-driven, long-term investment approach in the Financials October 9, 2007 peak, compared with the broader market as measured sector. As with all of our investments, Baron looks for financial by the Russell 3000 Index, which increased 59%. Many financial companies that have significant long-term growth opportunities, companies experienced subdued profitability and growth in the sustainable competitive advantages, and strong management teams, aftermath of the crisis as a result of heightened regulation, fines, and at an attractive valuation. We believe this investment style and the historically low interest rates. Most recently, credit risk in the energy sector’s relative value have allowed us to discover many potentially space has weighed on the sector. The decreasing likelihood of near-term successful investments in Financials. U.S. Federal Reserve rate hikes has not helped either. Opportunities in Banks and Insurance While their stock prices lag, financial company fundamentals and the economy continue to improve. Most financial institutions have paid Although traditional banks and insurance companies comprise a large back government loans and some are increasing share buybacks and weight in the Financials index, Baron tends not to invest in these dividend payments, reflecting greater financial soundness and stability. -

US Vegan Climate

US Vegan Climate ETF Schedule of Investments April 30, 2021 (Unaudited) Shares Security Description Value COMMON STOCKS - 99.4% Administrative and Support and Waste Management and Remediation Services - 13.4% 1,675 Accenture plc - Class A $ 485,700 233 Allegion plc 31,311 107 Booking Holdings, Inc. (a) 263,870 293 Broadridge Financial Solutions, Inc. 46,479 317 Equifax, Inc. 72,666 352 Expedia Group, Inc. 62,033 70 Fair Isaac Corporation (a) 36,499 729 Fidelity National Financial, Inc. 33,257 214 FleetCor Technologies, Inc. (a) 61,572 782 Global Payments, Inc. 167,841 961 IHS Markit, Ltd. 103,384 5,607 Mastercard, Inc. - Class A 2,142,210 425 Moody's Corporation 138,852 212 MSCI, Inc. 102,983 3,091 PayPal Holdings, Inc. (a) 810,738 491 TransUnion 51,354 8,745 Visa, Inc. - Class A 2,042,482 6,653,231 Construction - 0.9% 890 DR Horton, Inc. 87,478 1,956 Johnson Controls International plc 121,937 705 Lennar Corporation - Class A 73,038 19 NVR, Inc. (a) 95,344 682 PulteGroup, Inc. 40,320 396 Sunrun, Inc. (a) 19,404 437,521 Finance and Insurance - 14.1% 1,735 Aflac, Inc. 93,222 40 Alleghany Corporation (a) 27,159 797 Allstate Corporation 101,060 969 Ally Financial, Inc. 49,855 1,588 American Express Company 243,520 2,276 American International Group, Inc. 110,272 314 Ameriprise Financial, Inc. 81,138 657 Anthem, Inc. 249,259 596 Aon plc - Class A 149,858 1,025 Arch Capital Group, Ltd. (a) 40,703 496 Arthur J. -

Financial Services Fund

SCHEDULE OF INVESTMENTS (Unaudited) June 30, 2020 FINANCIAL SERVICES FUND SHARES VALUE SHARES VALUE COMMON STOCKS† - 99.9% Taubman Centers, Inc. 450 $ 16,992 Park Hotels & Resorts, Inc. 1,650 16,318 REITs - 30.1% Macerich Co.1 1,374 12,325 American Tower Corp. — Class A 474 $ 122,548 Crown Castle International Corp. 566 94,720 Total REITs 2,230,982 Prologis, Inc. 998 93,143 BANKS - 25.4% Equinix, Inc. 126 88,490 JPMorgan Chase & Co. 1,968 185,110 Digital Realty Trust, Inc. 496 70,487 Bank of America Corp. 6,585 156,394 SBA Communications Corp. 225 67,032 Citigroup, Inc. 2,218 113,340 Public Storage 339 65,051 Wells Fargo & Co. 4,313 110,413 AvalonBay Communities, Inc. 334 51,650 Morgan Stanley 2,038 98,435 Equity Residential 875 51,468 Goldman Sachs Group, Inc. 477 94,265 Simon Property Group, Inc. 743 50,806 U.S. Bancorp 2,210 81,372 Welltower, Inc. 975 50,456 Truist Financial Corp. 2,040 76,602 Alexandria Real Estate Equities, Inc. 307 49,811 PNC Financial Services Group, Inc. 695 73,121 Realty Income Corp. 823 48,968 Bank of New York Mellon Corp. 1,695 65,512 Weyerhaeuser Co. 2,045 45,931 State Street Corp. 833 52,937 Invitation Homes, Inc. 1,574 43,332 First Republic Bank 440 46,636 Essex Property Trust, Inc. 187 42,855 Northern Trust Corp. 564 44,748 Healthpeak Properties, Inc. 1,547 42,635 HDFC Bank Ltd. ADR 931 42,323 Boston Properties, Inc. 464 41,936 M&T Bank Corp. -

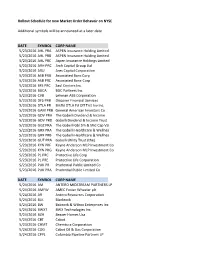

Rollout Schedule for New Market Order Behavoir on NYSE Additional

Rollout Schedule for new Market Order Behavoir on NYSE Additional symbols will be announced at a later date DATE SYMBOL CORP NAME 5/23/2016 AHL PRA ASPEN Insurance Holding Limited 5/23/2016 AHL PRB ASPEN Insurance Holding Limited 5/23/2016 AHL PRC Aspen Insurance Holdings Limited 5/23/2016 ARH PRC Arch Capital Group Ltd 5/23/2016 ARU Ares Capital Corporation 5/23/2016 ASB PRB Associated Banc Corp 5/23/2016 ASB PRC Associated Banc-Corp 5/23/2016 BFS PRC Saul Centers Inc. 5/23/2016 BGCA BGC Partners Inc. 5/23/2016 CVB Lehman ABS Corporation 5/23/2016 DFS PRB Discover Financial Services 5/23/2016 DTLA PR Brkfld DTLA Fd Off Trst Inv Inc. 5/23/2016 GAM PRB General American Investors Co 5/23/2016 GDV PRA The Gabelli Dividend & Income 5/23/2016 GDV PRD Gabelli Dividend & Income Trust 5/23/2016 GGZ PRA The Gabelli Gbl Sm & Mid Cap Val 5/23/2016 GRX PRA The Gabelli Healthcare & Wellnes 5/23/2016 GRX PRB The Gabelli Healthcare & Wellnes 5/23/2016 GUT PRA Gabelli Utility Trust (the) 5/23/2016 KYN PRF Kayne Anderson MLP Investment Co 5/23/2016 KYN PRG Kayne Anderson MLP Investment Co 5/23/2016 PL PRC Protective Life Corp 5/23/2016 PL PRE Protective Life Corporation 5/23/2016 PUK PR Prudential Public Limited Co 5/23/2016 PUK PRA Prudrntial Public Limited Co DATE SYMBOL CORP NAME 5/24/2016 AM ANTERO MIDSTREAM PARTNERS LP 5/24/2016 AMFW AMEC Foster Wheeler plc 5/24/2016 AR Antero Resources Corporation 5/24/2016 BLK Blackrock 5/24/2016 BW Babcock & Wilcox Enterprises Inc 5/24/2016 BWXT BWX Technologies Inc. -

Baron Funds® December 31, 2020 Quarterly Report

Baron Funds® December 31, 2020 Quarterly Report “Ron, when I first met you 35 years ago, you business in 1982. Our Firm now manages that only 1 of 19 analysts who had published a were investing in wireless telephones. $50 billion of assets. Further, since 1992, we research report with a sell recommendation on ‘Wow! That’s a pretty far out idea,’ have earned more than $47 billion realized and Tesla had met Elon Musk; only 3 had visited its I thought.” After beginning a recent phone call unrealized profits for our clients. Baron Capital Fremont factory; none had visited its huge to me with that comment, Chuck no longer has an insignificant book value. facility in Reno...which we visited 3 times!...and Mathewsontoldmehewascallingto no one I knew had read either Elon’s biography Although Chuck called to congratulate us on congratulate us on our Tesla investment. or “The Last Days of Night,” an historical fiction Tesla, he had previously been skeptical about Chuck Mathewson. Chairman Emeritus book about Nikola Tesla that was a really fun Tesla’s prospects. That was also the case for International Game Technology and Chairman read. The last was a book my wife, Judy, insisted most of my friends, clients and my contacts in Emeritus Baron Funds. December 2020. I read. I finished it in two nights. After extensive the media. To say nothing of the executives of diligence...that is ongoing nine years later...we In 1970, I began my career as a Wall Street businesses that manufacture cars with internal invested $372 million in Tesla shares, securities analyst. -

FACTS™ Trust Impact Assessments Available for the Following Alphabetically Listed Companies

FACTS™ Trust Impact Assessments Available for the Following Alphabetically Listed Companies (Updated October 2010) 1st Source Corporation AECOM Technology Corporation Allergan, Inc. 3M Company Aeropostale, Inc. ALLETE, Inc. 3PAR Inc. AeroVironment, Inc. Alliance Data Systems Corporation 99 Cents Only Stores Aetna Alliant Energy Corporation A. O. Smith Corporation Affiliated Managers Group, Inc. Alliant Techsystems Inc. A. Schulman, Inc. Affymetrix, Inc. Allied Nevada Gold Corp. AAON, Inc. AFLAC Incorporated Allied World Assurance Holdings, Ltd. AAR Corp. Aga Medical Holdings, Inc Allos Therapeutics, Inc. Aaron's, Inc. AGCO Corporation Allscripts Healthcare Solutions Inc Abaxis, Inc. Agilent Technologies Inc. Alnylam Pharmaceuticals, Inc. Abbott Laboratories AGL Resources Inc. Alon USA Energy, Inc. Abercrombie & Fitch Co. Air Methods Corporation Alpha Natural Resources, Inc. ABIOMED, Inc. Air Products & Chemicals, Inc. Alphatec Holdings, Inc. ABM Industries, Inc. Aircastle Limited Altera Corporation AboveNet, Inc. Airgas, Inc. Altria Group, Inc. Abraxis Bioscience, Inc. AirTran Holdings, Inc. AMAG Pharmaceuticals, Inc. Acacia Research Corporation AK Steel Holding Corporation Amazon.com, Inc. Acadia Realty Trust Akamai Technologies, Inc. AMB Property Corporation Accenture Plc Alaska Air Group, Inc. AMCOL International Corporation Accuray Incorporated Alaska Communications Systems Group, Inc Amedisys, Inc. ACI Worldwide Inc Albany International Corp. AMERCO Acme Packet, Inc. Albemarle Corporation Ameren Corporation Acorda Therapeutics Inc. Alberto-Culver Company Activision Blizzard, Inc. American Axle & Manufact. Holdings, Inc. Alcoa Inc. Actuant Corporation Alexander & Baldwin, Inc. American Campus Communities, Inc. Acuity Brands, Inc. Alexander's, Inc. American Capital Agency Corp. Acxiom Corporation American Capital Ltd. ADC Telecommunications Alexandria Real Estate Equities, Inc. American Eagle Outfitters Administaff, Inc. Alexion Pharmaceuticals, Inc. Adobe Systems Incorporated Align Technology, Inc. -

New Covenant Growth Fund

SCHEDULE OF INVESTMENTS (Unaudited) March 31, 2020 New Covenant Growth Fund Market Value Market Value Description Shares ($ Thousands) Description Shares ($ Thousands) COMMON STOCK — 96.0% COMMON STOCK (continued) Bosnia and Herzegovina — 0.0% IMAX * 2,244 $ 20 RenaissanceRe Holdings Ltd. 248 $ 37 Intelsat * 8,389 13 – Interpublic Group of Cos Inc/The 8,487 137 Canada — 0.1% Iridium Communications * 366 8 Lululemon Athletica Inc * 1,014 192 – John Wiley & Sons Inc, Cl A 236 9 Cayman Islands — 0.0% Liberty Broadband, Cl A * 113 12 Herbalife * 1,088 31 Lions Gate Entertainment, Cl A * 7,278 44 – Ireland — 1.0% Live Nation Entertainment Inc * 181 8 Accenture PLC, Cl A 11,297 1,844 Match Group * 703 46 Jazz Pharmaceuticals PLC * 616 62 Meredith 1,401 17 Mallinckrodt * 13,812 27 MSG Networks * 2,988 31 Medtronic PLC 19,976 1,801 New York Times, Cl A 1,515 47 NortonLifeLock 13,065 245 Nexstar Media Group, Cl A 455 26 Perrigo Co PLC 211 10 Omnicom Group Inc 10,137 557 Scholastic 1,266 32 3,989 – Shenandoah Telecommunications 1,286 63 Puerto Rico — 0.0% Sirius XM Holdings 7,153 35 Popular Inc 1,507 53 – Spotify Technology SA * 608 74 Switzerland — 0.0% Sprint Corp * 2,200 19 Garmin Ltd 1,092 82 Take-Two Interactive Software Inc * 830 98 – TechTarget * 1,986 41 United Kingdom — 0.2% TEGNA 3,052 33 Aon PLC 2,921 482 T-Mobile US Inc * 2,824 237 Healthpeak Properties 9,384 224 Twitter Inc * 7,369 181 706 – Verizon Communications Inc 62,462 3,356 United States — 94.7% ViacomCBS, Cl B 1,000 14 Communication Services — 8.3% Walt Disney Co/The 26,709