2013-11-18-PH-S-EMP.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Diversification Strategies of Large Business Groups in the Philippines

Philippine Management Review 2013, Vol. 20, 65‐82. Diversification Strategies of Large Business Groups in the Philippines Ben Paul B. Gutierrez and Rafael A. Rodriguez* University of the Philippines, College of Business Administration, Diliman, Quezon City 1101, Philippines This paper describes the diversification strategies of 11 major Philippine business groups. First, it reviews the benefits and drawbacks of related and unrelated diversification from the literature. Then, it describes the forms of diversification being pursued by some of the large Philippine business groups. The paper ends with possible explanations for the patterns of diversification observed in these Philippine business groups and identifies directions for future research. Keywords: related diversification, unrelated diversification, Philippine business groups 1 Introduction This paper will describe the recent diversification strategies of 11 business groups in the Philippines. There are various definitions of business groups but in this paper, these are clusters of legally distinct firms with a managerial relationship, usually by virtue of common ownership. The focus on business groups rather than on individual firms has to do with the way that business firms in the Philippines are organized and managed. Businesses that are controlled and managed by essentially the same set of principal owners are often organized as separate corporations, not as separate divisions within the same firm, as is often the case in American corporations like General Electric, Procter and Gamble, or General Motors (Echanis, 2009). Moreover, studies on emerging markets have pointed out that business groups often occupy dominant positions in the business landscape in markets like India, Korea, Indonesia, Thailand, and the Philippines (Khanna & Palepu, 1997; Khanna & Yafeh, 2007). -

February 19, 2011 February 15, 2014

februarY 15, 2014 hawaii filiPino ChroniCle 1 ♦ FEBRUARY 15,19, 20142011 ♦ OPINION HAWAII-FILIPINO NEWS LEGAL NOTES Driverless Cars? ConGen torres, maYor hints of Possible Yes, almost Just CalDwell leaD traDe ComPromise on arounD the Corner mission to the PhiliPPines immiGration PRESORTED HAWAII FILIPINO CHRONICLE STANDARD 94-356 WAIPAHU DEPOT RD., 2ND FLR. U.S. POSTAGE WAIPAHU, HI 96797 PAID HONOLULU, HI PERMIT NO. 9661 2 hawaii filiPino ChroniCle februarY 15, 2014 EDITORIALS FROM THE PUBLISHER or hopeless romantics, February Publisher & Executive Editor The Mega Rich as 14th is one of the most antici- Charlie Y. Sonido, M.D. pated days of the year. It’s a day Publisher & Managing Editor Role Models that’s set aside to celebrate the Chona A. Montesines-Sonido ill Gates and Warren Buffet are household names in powerful human emotion called Associate Editors F love. When you think about it, Dennis Galolo the U.S. The multi-billionaires are rich, powerful and we should be showing our love Edwin Quinabo influential. But how many of us know of the late to those closest to us every day and not just Corliss Lamont, a Harvard graduate born of Wall Contributing Editor on special occasions like Valentine’s. On that note, Happy Belinda Aquino, Ph.D. Street wealth who championed the causes of poor B Valentine’s Day to all of you! Creative Designer people his entire life? Or Maud Younger (1870- Our cover story for this issue—“The 10 Wealthiest People Junggoi Peralta 1936), who despite coming from a wealthy family in San Francisco, in the Philippines” according to Forbes Magazine, was written worked for five years as a waitress to learn about working class Photography by our Philippine correspondent Gregory Garcia. -

WT/DS396/R WT/DS403/R Page A-1 ANNEX a FIRST WRITTEN

WT/DS396/R WT/DS403/R Page A-1 ANNEX A FIRST WRITTEN SUBMISSIONS OF THE PARTIES Contents Page Annex A-1 Executive summary of the first written submission of the European Union A-2 Annex A-2 Executive summary of the first written submission of the United States A-10 Annex A-3 Executive summary of the first written submission of the Philippines A-18 WT/DS396/R WT/DS403/R Page A-2 ANNEX A-1 EXECUTIVE SUMMARY OF THE FIRST WRITTEN SUBMISSION OF THE EUROPEAN UNION I. INTRODUCTION 1. The present dispute concerns a blatant violation of Article III:2 first and second sentences. For many decades, the Philippines have applied lower internal taxes to domestically produced distilled spirits than to like or directly competitive and substitutable distilled spirits imported from the European Union (the "EU") and other WTO Members. Regrettably, over the past years, the discrimination against imported distilled spirits has even worsened, as the tax differential between domestic products and imported products has progressively widened. 2. The Filipino authorities have in several occasions publicly acknowledged the WTO-incompatibility of the measures at dispute. In fact, in the past years, several draft bills were proposed to reform the Excise Tax Regime. Some of these draft bills envisaged the creation of a single tax structure for all alcohol products, based on alcohol content rather than on the raw materials used. These proposals met however the strong resistance from the local spirits industry and were never approved. 3. The Filipino market for spirits is currently estimated to amount to ca. -

Cover Book Final.Cdr

TOP 100 ASIA’S BEST EMPLOYER BRANDS PRASAD MEDURY Managing Director, Odgers Berndtson India Private Limited DR. HARISH MEHTA Founder & Executive Chairman of Onward Technologies Ltd (OTL). Founding Member of NASSCOM DR. SANJAY MUTHAL Executive Director, Insist Executive Search TOP 100 ASIA’S BEST EMPLOYER BRANDS One of most competitive IT-BPM Firms in the Philippines GLOBAL INTEGRATED Global Integrated Contact Facilities, Inc. (GICF) is a medium-scale, diversied IT-BPM CONTACT FACILITIES INC. solutions company that caters to domestic and international B2B and B2C organizations in high-growth industry sectors. Established in 2015, and backed by domain and functional experts with an average industry tenure of over 15 years, GICF serves as a business catalyst that brings strong value propositions across its stakeholder partnerships– through targeted, exible, and economical solutions that strive to secure and sustain enterprise- wide success objectives no matter the stage of a client’s business lifecycle. GICF and its leaders have been privileged to forge client relationships with international and domestic top-tier MNCs, large-scale businesses, and SMEs with operations across North America, Europe, and the Asia Pacic– managing variedly scaled IT-BPM projects that are simple-to-complex in nature. GICF maintains its brand promise ‘YOUR VISION, OUR SOLUTION’ as manifested in its innovative approach to addressing dynamic shifts within the IT-BPM industry and specic to the vertical and domain areas specic to every client engagement. Gcash is the Philippines' rst and leading mobile money wallet. Through the GCash App, customers can easily purchase prepaid airtime; pay bills at over 400 partner billers nationwide; send and receive money anywhere in the Philippines; pay using QR codes at MYNT (GLOBE FINTECH over 50,000 partner merchants; and invest money at money market funds through the INNOVATIONS, INC.) convenience of their smartphone. -

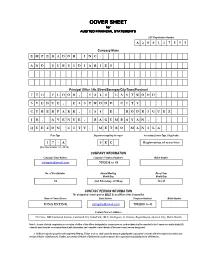

COVER SHEET for AUDITED FINANCIAL STATEMENTS

COVER SHEET for AUDITED FINANCIAL STATEMENTS SEC Registration Number A 2 0 0 1 1 7 5 9 5 Company Name EMPERADORINC. ANDSUBSIDIARIES Principal Office ( No./Street/Barangay/City/Town)Province) 7TH FLOOR, 1880 EASTWOOD AVENUE,EASTWOODCITY CYBERPARK, 188 E. RODRIGUEZ JR.AVENUE,BAGUMBAYAN, QUEZONCITY,METROMANILA Form Type Department requiring the report Secondary License Type, If Applicable 1 7 - A S E C Registration of securities (For December 31, 2015) COMPANY INFORMATION Company's Email Address Company's Telephone Number/s Mobile Number [email protected] 7092038 to 41 No. of Stockholders Annual Meeting Fiscal Year Month/Day Month/Day 24 3rd Monday of May 12/31 CONTACT PERSON INFORMATION The designated contact person MUST be an Officer of the Corporation Name of Contact Person Email Address Telephone Number/s Mobile Number DINA INTING [email protected] 7092038 to 41 Contact Person's Address 7th Floor, 1880 Eastwood Avenue, Eastwood City CyberPark, 188 E. Rodriguez, Jr. Avenue, Bagumbayan, Quezon City, Metro Manila Note 1: In case of death, resgination or cessation of office of the officer designated as contact person, such incident shall be reported to the Commission within thirty (30) calendar days from the occurrence thereof with information and complete contact details of the new contact person designated. 2: All Boxes must be properly and completely filled-up. Failure to do so shall cause the delay in updating the corporation's records with the Commission and/or non- receipt of Notice of Deficiencies. Further, non-receipt of Notice of Deficiencies shall not excuse the corporation from liability for its deficiencies. -

Downloadable Annual Report Yes

CR02058-2016 SECURITIES AND EXCHANGE COMMISSION SEC FORM 17-A, AS AMENDED ANNUAL REPORT PURSUANT TO SECTION 17 OF THE SECURITIES REGULATION CODE AND SECTION 141 OF THE CORPORATION CODE OF THE PHILIPPINES 1. For the fiscal year ended Dec 31, 2015 2. SEC Identification Number 167423 3. BIR Tax Identification No. 000-477-103 4. Exact name of issuer as specified in its charter MEGAWORLD CORPORATION 5. Province, country or other jurisdiction of incorporation or organization Metro Manila 6. Industry Classification Code(SEC Use Only) 7. Address of principal office 28th Floor, The World Centre, 330 Sen. Gil Puyat Avenue, Makati City Postal Code 1227 8. Issuer's telephone number, including area code (632) 8678826 to 40 9. Former name or former address, and former fiscal year, if changed since last report N/A 10. Securities registered pursuant to Sections 8 and 12 of the SRC or Sections 4 and 8 of the RSA Title of Each Class Number of Shares of Common Stock Outstanding and Amount of Debt Outstanding Common 32,239,445,872 Preferred 6,000,000,000 11. Are any or all of registrant's securities listed on a Stock Exchange? Yes No If yes, state the name of such stock exchange and the classes of securities listed therein: Philippine Stock Exchange, Common Shares 12. Check whether the issuer: (a) has filed all reports required to be filed by Section 17 of the SRC and SRC Rule 17.1 thereunder or Section 11 of the RSA and RSA Rule 11(a)-1 thereunder, and Sections 26 and 141 of The Corporation Code of the Philippines during the preceding twelve (12) months (or for such shorter period that the registrant was required to file such reports) Yes No (b) has been subject to such filing requirements for the past ninety (90) days Yes No 13. -

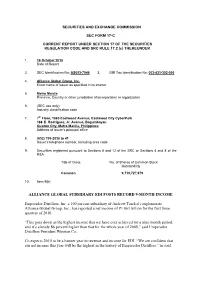

Alliance Global Subsidiary Edi Posts Record 9-Month Income

SECURITIES AND EXCHANGE COMMISSION SEC FORM 17-C CURRENT REPORT UNDER SECTION 17 OF THE SECURITIES REGULATION CODE AND SRC RULE 17.2 (c) THEREUNDER 1. 18 October 2010 Date of Report 2. SEC Identification No: AS093-7946 3. BIR Tax Identification No: 003-831-302-000 4. Alliance Global Group, Inc. Exact name of issuer as specified in its charter 5. Metro Manila Province, Country or other jurisdiction of incorporation or organization 6. (SEC use only) Industry classification code 7. 7th Floor, 1880 Eastwood Avenue, Eastwood City CyberPark 188 E. Rodriguez, Jr. Avenue, Bagumbayan Quezon City, Metro Manila, Philippines Address of issuer’s principal office 8. (632) 709-2038 to 41 Issuer’s telephone number, including area code 9. Securities registered pursuant to Sections 8 and 12 of the SRC or Sections 4 and 8 of the RSA: Title of Class No. of Shares of Common Stock Outstanding Common 9,719,727,979 10. Item 9(b) ALLIANCE GLOBAL SUBSIDIARY EDI POSTS RECORD 9-MONTH INCOME Emperador Distillers, Inc. a 100 percent subsidiary of Andrew Tan-led conglomerate Alliance Global Group, Inc., has reported a net income of P1.061 billion for the first three quarters of 2010. “This goes down as the highest income that we have ever achieved for a nine-month period, and it’s already 86 percent higher than that for the whole year of 2009,” said Emperador Distillers President Winston Co. Co expects 2010 to be a banner year in revenue and income for EDI. “We are confident that our net income this year will be the highest in the history of Emperador Distillers,” he said. -

Market Recap

MARKET RECAP 02 August 2018 PSEi Value Turnover (US$) Net Foreign Flow (US$) PHI:US (PLDT ADR) US$ 1.00 7,759.55 (-1.004%) 92,842,039.63 (4,550,407.74 25.32 (+1.36%) = 1,346.01 53.115 Market Recap • Philippine share prices sank on mounting trade war fears after the US warned it was looking at more than doubling threatened tariffs on a range of Chinese imports. • The benchmark PSEi tumbled 78.67 points or 1.004% to close at 7,759.55. The broader All Shares index fell 34.84 points or 0.75% to 4,644.68 at the closing bell. • Donald Trump's Trade Representative Robert Lighthizer confirmed earlier reports that the White House was considering hiking levies to 25% from the announced 10% on $200-bil of Chinese goods. • Lighthizer’s statement comes after separate reports said the two sides were looking to restart talks to avert a trade war between the world's top two economies that could hammer global growth. • In response to earlier reports that the US was considering the move, Chinese foreign ministry spokesman Geng Shuang warned Wednesday that "blackmail and pressure from the US side will never work on China". • The latest developments come as Washington considers imposing tariffs on $16-bil of goods in the coming weeks, having already targeted imports worth $34-bil last month. • Investors are left guessing about how the crisis will play out, with some worrying that with both sides digging in there could be more pain down the line, but others are saying Trump is playing tough as a negotiating tactic. -

COVER SHEET for Audited Financial Statements

COVER SHEET for Audited Financial Statements SEC Registration Number A2001-17595 COMPANY NAME EMPERADOR INC. AND SUBSIDIARIES PRINCIPAL OFFICE ( No./Street/Barangay/City/Town)Province) 7TH FLOOR, 1880 EASTWOOD AVENUE,EASTWOODCITY CYBERPARK, 188 E. RODRIGUEZ JR.AVENUE,BAGUMBAYAN QUEZONCITY,METROMANILA Form Type Department requiring the report Secondary License Type, If Applicable Certificate of Permit to Offer 1 7 - A S E C Securities for Sale (for December 31, 2018) COMPANY INFORMATION Company's Email Address Company's Telephone Number/s Mobile Number [email protected] 709-2038 to 41 N/A No. of Stockholders Annual Meeting Fiscal Year Month/Day Month/Day 160 3rd Monday of May DECEMBER 31 CONTACT PERSON INFORMATION The designated contact person MUST be an Officer of the Corporation Name of Contact Person Email Address Telephone Number/s Mobile Number DINA INTING [email protected] 709-2038 to 41 N/A Contact Person's Address 7th Floor, 1880 Eastwood Avenue, Eastwood City Cyberpark, 188 E. Rodriguez Jr. Avenue, Bagumbayan, Quezon City Note 1: In case of death, resgination or cessation of office of the officer designated as contact person, such incident shall be reported to the Commission within thirty (30) calendar days from the occurrence thereof with information and complete contact details of the new contact person designated. 2: All Boxes must be properly and completely filled-up. Failure to do so shall cause the delay in updating the corporation's records with the Commission and/or non-receipt of Notice of Deficiencies. Further, non-receipt of Notice of Deficiencies shall not excuse the corporation from liability for its deficiencies. -

The Art of Success

ANNUAL REPORT 2013 The Art of Success THE ART FINANCIAL HIGHLIGHTS OF SUCCESS 1 123,379 37,107 32,406 23,055 102,134 20,494 5,837 6,584 14,743 17,218 22,167 66,291 3,136 13,910 9,497 11,607 44,495 2,588 12,898 6,909 10 11 12 13 10 11 12 13 10 11 12 13 REVENUES EBITDA NET INCOME (In Million Pesos) (In Million Pesos) (In Million Pesos) Attributable to: Non-controlling Interest Owners of AGI ANNUAL REPORT 2 2013 MESSAGE FROM THE CHAIRMAN AGI’s total here is no single formula for success in business. Making it good revenues for in a highly competitive business arena requires considerable Tcreativity—creativity in making decisions that matter, creativity in 2013 grew planning projects that will make a difference, and creativity in managing by a hefty people effectively to allow them to live up to their potential. I am happy and proud to note that our leaders in Alliance Global Group, Inc. (AGI) 20.8 percent to not only have the requisite creativity to fulfill this mandate, but passion P123.38 billion and expertise to succeed in our line of businesses as well. Our numbers for 2013 speak for us in this regard. from P102.13 billion the The year 2013 was definitely a challenging one for the Philippines, as the country had to deal with a few strong typhoons and a huge previous year. earthquake. Despite these natural calamities, however, the country was able to register a gross domestic product (GDP) growth of 7.2 percent at the end of the year, even higher than the 6.8 percent growth rate in 2012. -

Duterte Leads the Pack, Race Heats Up!

Maligayang Pasko at Manigong Bagong Taon ! DUTERTE LEADS THE PACK, RACE HEATS UP! ⦿ POE disqualified for second time ⦿ MAR to DUTERTE: “Suntukan na lang” ⦿ DUTERTE to MAR: “Lets have a gun duel!” The 2016 Philippine presi- the pack besting his oppo- dential race is almost nents. reaching its crescendo and But some say the surveys boiling point as protago- are flawed and defective. nists step up their respec- tive campaign, exchanging Reports from Manila say Rodrigo Duterte Grace Poe Mar Roxas barbs and brickbats to woo Mar Roxas and Duterte are from slapping, to a boxing among voters with the fire voters. animatedly engaged in a bout and a gun duel. provided by the controver- See related stories word war that has culmi- sial and foul mouthed Da- Latecomer Rodrigo Duterte, This has provided some on Page 3 nated to physical challenges vao city Mayor Duterte. according to surveys, leads form of entertainment Ramos tells Duterte, Roxas: Andrew Tan’s Emperador buys Spain’s Fundador Act like global leaders By: Tina Arceo-Dumlao By: Gil Cabacungan LISTED liquor company world’s largest brandy Emperador Inc. owned by company and makes the Former President Fidel V. they would not only be tycoon Andrew L. Tan has Tan-led firm one of the Ramos said that if Mar Rox- compared to past Philip- acquired Fundador Pedro largest foreign investors in as and Rodrigo Duterte pine Presidents but they Domecq, Spain’s largest Jerez, the brandy capital of want to be President, they would also be compared and oldest brandy, in an “all Spain. -

Walang Ilaw, May Bangka

Libre dito ang INQUIRER LIBRE Digital Edition www.inquirer.net/apps VOL. 13 NO. 63 • FEBRUARY 21-23, 2014 The best things in life are Libre Lord, salamat po sa mapagkalinga at mababait na Lolo at Lola. Sila po ang tumatayong pangalawang mga magulang na- ming magkakapatid habang ang aming mga magulang ay nagtra- trabaho sa ibang bayan. Sana po ay maging malakas at masigla pa sila, walang mga karamdaman. Bi- gyan N’yo pa po sila ng mahabang buhay. Amen. (Brian Ben Coronel) PANAGBENGA NA! HIGANTENG paru-paro at dambuhalang mga bulaklak ang pinagkakaabalahan ng mga kabataang ito bilang paghahanda sa pagdiriwang ng Panagebnga ngayong weekend sa Baguio City, na taun-taong dinadagsa ng mga turista. EV ESPIRITU EARTH HOUR 2014 Walang ilaw, may bangka Ni Camille Anne M. Arcilla Layunin ng proyektong “Ban- (WWF) hinihimok ang mga in- ding makalikom ng pondo sa pa- cas for the Philippines” na dibidwal, pamayanan at nego- mamagitan ng Internet para sa ALIBAN sa pagpatay ng ilaw, hihigitan na ng makalikom ng $24,000 bago syo na magpatay ng di-mahala- sari-saring proyekto, kabilang Earth Hour ang 60-minutong kampanya sa ang Earth Hour ngayong taon, gang ilaw bilang sagisag ng ang pagbibigay ng bangkang yari pagpapanatili sa kalikasan at lilikom na ng na nakatakda sa Marso 29 mula pakikiisa sa pagpapanatili sa sa fiberglass sa mga lugar na M 8:30 hanggang 9:30 ng gabi. planeta. tinamaan ni Yolanda. Nakatala pondo upang tulungan ang mga mangingisda na nawa- Sa kampanyang Earth Hour May kaugnay pang kampa- ang mga programa sa http:// lan ng kabuhayan dahil sa Superbagyong “Yolanda.” ng World Wide Fund for Nature nyang Earth Hour Blue na nais earthhourblue.crowdonomic.com.