Definitive Information Statement of May Month Day FORM TYPE Month Day Fiscal Year Annual Meeting Registration of Securities Secondary License Type, If Applicable

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Securities and Exchange Commission Sec Form 17-A, As Amended

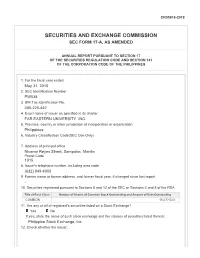

CR05708-2019 SECURITIES AND EXCHANGE COMMISSION SEC FORM 17-A, AS AMENDED ANNUAL REPORT PURSUANT TO SECTION 17 OF THE SECURITIES REGULATION CODE AND SECTION 141 OF THE CORPORATION CODE OF THE PHILIPPINES 1. For the fiscal year ended May 31, 2019 2. SEC Identification Number PW538 3. BIR Tax Identification No. 000-225-442 4. Exact name of issuer as specified in its charter FAR EASTERN UNIVERSITY, INC. 5. Province, country or other jurisdiction of incorporation or organization Philippines 6. Industry Classification Code(SEC Use Only) 7. Address of principal office Nicanor Reyes Street, Sampaloc, Manila Postal Code 1015 8. Issuer's telephone number, including area code (632) 849-4000 9. Former name or former address, and former fiscal year, if changed since last report - 10. Securities registered pursuant to Sections 8 and 12 of the SRC or Sections 4 and 8 of the RSA Title of Each Class Number of Shares of Common Stock Outstanding and Amount of Debt Outstanding COMMON 16,477,023 11. Are any or all of registrant's securities listed on a Stock Exchange? Yes No If yes, state the name of such stock exchange and the classes of securities listed therein: Philippine Stock Exchange, Inc. 12. Check whether the issuer: (a) has filed all reports required to be filed by Section 17 of the SRC and SRC Rule 17.1 thereunder or Section 11 of the RSA and RSA Rule 11(a)-1 thereunder, and Sections 26 and 141 of The Corporation Code of the Philippines during the preceding twelve (12) months (or for such shorter period that the registrant was required to file such reports) Yes No (b) has been subject to such filing requirements for the past ninety (90) days Yes No 13. -

Diversification Strategies of Large Business Groups in the Philippines

Philippine Management Review 2013, Vol. 20, 65‐82. Diversification Strategies of Large Business Groups in the Philippines Ben Paul B. Gutierrez and Rafael A. Rodriguez* University of the Philippines, College of Business Administration, Diliman, Quezon City 1101, Philippines This paper describes the diversification strategies of 11 major Philippine business groups. First, it reviews the benefits and drawbacks of related and unrelated diversification from the literature. Then, it describes the forms of diversification being pursued by some of the large Philippine business groups. The paper ends with possible explanations for the patterns of diversification observed in these Philippine business groups and identifies directions for future research. Keywords: related diversification, unrelated diversification, Philippine business groups 1 Introduction This paper will describe the recent diversification strategies of 11 business groups in the Philippines. There are various definitions of business groups but in this paper, these are clusters of legally distinct firms with a managerial relationship, usually by virtue of common ownership. The focus on business groups rather than on individual firms has to do with the way that business firms in the Philippines are organized and managed. Businesses that are controlled and managed by essentially the same set of principal owners are often organized as separate corporations, not as separate divisions within the same firm, as is often the case in American corporations like General Electric, Procter and Gamble, or General Motors (Echanis, 2009). Moreover, studies on emerging markets have pointed out that business groups often occupy dominant positions in the business landscape in markets like India, Korea, Indonesia, Thailand, and the Philippines (Khanna & Palepu, 1997; Khanna & Yafeh, 2007). -

Private Higher Education Institutions Faculty-Student Ratio: AY 2017-18

Table 11. Private Higher Education Institutions Faculty-Student Ratio: AY 2017-18 Number of Number of Faculty/ Region Name of Private Higher Education Institution Students Faculty Student Ratio 01 - Ilocos Region The Adelphi College 434 27 1:16 Malasiqui Agno Valley College 565 29 1:19 Asbury College 401 21 1:19 Asiacareer College Foundation 116 16 1:7 Bacarra Medical Center School of Midwifery 24 10 1:2 CICOSAT Colleges 657 41 1:16 Colegio de Dagupan 4,037 72 1:56 Dagupan Colleges Foundation 72 20 1:4 Data Center College of the Philippines of Laoag City 1,280 47 1:27 Divine Word College of Laoag 1,567 91 1:17 Divine Word College of Urdaneta 40 11 1:4 Divine Word College of Vigan 415 49 1:8 The Great Plebeian College 450 42 1:11 Lorma Colleges 2,337 125 1:19 Luna Colleges 1,755 21 1:84 University of Luzon 4,938 180 1:27 Lyceum Northern Luzon 1,271 52 1:24 Mary Help of Christians College Seminary 45 18 1:3 Northern Christian College 541 59 1:9 Northern Luzon Adventist College 480 49 1:10 Northern Philippines College for Maritime, Science and Technology 1,610 47 1:34 Northwestern University 3,332 152 1:22 Osias Educational Foundation 383 15 1:26 Palaris College 271 27 1:10 Page 1 of 65 Number of Number of Faculty/ Region Name of Private Higher Education Institution Students Faculty Student Ratio Panpacific University North Philippines-Urdaneta City 1,842 56 1:33 Pangasinan Merchant Marine Academy 2,356 25 1:94 Perpetual Help College of Pangasinan 642 40 1:16 Polytechnic College of La union 1,101 46 1:24 Philippine College of Science and Technology 1,745 85 1:21 PIMSAT Colleges-Dagupan 1,511 40 1:38 Saint Columban's College 90 11 1:8 Saint Louis College-City of San Fernando 3,385 132 1:26 Saint Mary's College Sta. -

February 19, 2011 February 15, 2014

februarY 15, 2014 hawaii filiPino ChroniCle 1 ♦ FEBRUARY 15,19, 20142011 ♦ OPINION HAWAII-FILIPINO NEWS LEGAL NOTES Driverless Cars? ConGen torres, maYor hints of Possible Yes, almost Just CalDwell leaD traDe ComPromise on arounD the Corner mission to the PhiliPPines immiGration PRESORTED HAWAII FILIPINO CHRONICLE STANDARD 94-356 WAIPAHU DEPOT RD., 2ND FLR. U.S. POSTAGE WAIPAHU, HI 96797 PAID HONOLULU, HI PERMIT NO. 9661 2 hawaii filiPino ChroniCle februarY 15, 2014 EDITORIALS FROM THE PUBLISHER or hopeless romantics, February Publisher & Executive Editor The Mega Rich as 14th is one of the most antici- Charlie Y. Sonido, M.D. pated days of the year. It’s a day Publisher & Managing Editor Role Models that’s set aside to celebrate the Chona A. Montesines-Sonido ill Gates and Warren Buffet are household names in powerful human emotion called Associate Editors F love. When you think about it, Dennis Galolo the U.S. The multi-billionaires are rich, powerful and we should be showing our love Edwin Quinabo influential. But how many of us know of the late to those closest to us every day and not just Corliss Lamont, a Harvard graduate born of Wall Contributing Editor on special occasions like Valentine’s. On that note, Happy Belinda Aquino, Ph.D. Street wealth who championed the causes of poor B Valentine’s Day to all of you! Creative Designer people his entire life? Or Maud Younger (1870- Our cover story for this issue—“The 10 Wealthiest People Junggoi Peralta 1936), who despite coming from a wealthy family in San Francisco, in the Philippines” according to Forbes Magazine, was written worked for five years as a waitress to learn about working class Photography by our Philippine correspondent Gregory Garcia. -

WT/DS396/R WT/DS403/R Page A-1 ANNEX a FIRST WRITTEN

WT/DS396/R WT/DS403/R Page A-1 ANNEX A FIRST WRITTEN SUBMISSIONS OF THE PARTIES Contents Page Annex A-1 Executive summary of the first written submission of the European Union A-2 Annex A-2 Executive summary of the first written submission of the United States A-10 Annex A-3 Executive summary of the first written submission of the Philippines A-18 WT/DS396/R WT/DS403/R Page A-2 ANNEX A-1 EXECUTIVE SUMMARY OF THE FIRST WRITTEN SUBMISSION OF THE EUROPEAN UNION I. INTRODUCTION 1. The present dispute concerns a blatant violation of Article III:2 first and second sentences. For many decades, the Philippines have applied lower internal taxes to domestically produced distilled spirits than to like or directly competitive and substitutable distilled spirits imported from the European Union (the "EU") and other WTO Members. Regrettably, over the past years, the discrimination against imported distilled spirits has even worsened, as the tax differential between domestic products and imported products has progressively widened. 2. The Filipino authorities have in several occasions publicly acknowledged the WTO-incompatibility of the measures at dispute. In fact, in the past years, several draft bills were proposed to reform the Excise Tax Regime. Some of these draft bills envisaged the creation of a single tax structure for all alcohol products, based on alcohol content rather than on the raw materials used. These proposals met however the strong resistance from the local spirits industry and were never approved. 3. The Filipino market for spirits is currently estimated to amount to ca. -

1 2018 IEEE Republic of Philippines Section Report PART A

2018 IEEE Republic of Philippines Section Report PART A - SECTION SUMMARY A.1 EXECUTIVE SUMMARY IEEE Republic of Philippines Section List of Officers POSITION NAME Chairman Dr. Jennifer Dela Cruz Vice Chair (Awards & Recognition Dr. Argel Bandala Chair) Secretary Dr. Ryan Rhay Vicerra Treasurer (Conference Chair) Dr. Ryan Rhay Vicerra Auditor Dr. Susan Festin Public Relations Officer Engr. Edison Roxas Committee Member – Educational Dr. Rhandley Cajote Activities Chair Committee Member – Membership Engr. Josyl Mariela Rocamora Development Chair Committee Member – Professional Mr. Victor Gruet Activities Chair Committee Member – SIGHT Dr. Nestor Michael Tiglao Chair Committee Member – Student Mr. Neriah “BJ” Ato Activities Chair Committee Member - Newsletter Dr. Argel Bandala Editor Committee Member - Webmaster Dr. Argel Bandala Highlights IEEE Kapihan May 26,2018 IEEE Week 2018 Formation of IEEE YP Affinity Group 1 MEMBERSHIP DEVELOPMENT PROGRAMS IEEE REPUBLIC OF PHILIPPINES SECTION MEMBERSHIP (AS OF JUNE 2018) IEEE Grade Description Active Members (2018) Higher Grade Members 258 Student Members 109 TOTAL 367 IEEE Grade Description Active Members (2017) Higher Grade Members 240 Student Members 96 TOTAL 336 Summary and evidence of work done in the retention of members 6th IEEE Kapihan Dr. Jennifer Dela Cruz, Chair of IEEE PS, discussed the history of Kapihan along with the goals and objectives on why this event is happening. It was held on May 26, 2018 at Mapua University. B.3. Recognized Education Programs 6th IEEE Kapihan Members Gathering: Knowing More About Us May 26, 2018, AV2-AV3 Mapua University, Intramuros PROGRAMME 9:00 – 9:30 AM Registration 9:30 – 9:35 AM Invocation and National Anthem 9:35 – 10:15 AM Welcome and Opening Remarks Introduction of PS Officers 2018 IEEE PS Membership Status Jennifer Dela Cruz, Ph.D IEEE PS Chair, IEEE PS WIE Chair 2 10:15 – 10:30 AM General Data Protection Regulation (GDPR) Overview 10:30 – 11:00 AM Tutorials on Collabratec Engr. -

College Codes (Outside the United States)

COLLEGE CODES (OUTSIDE THE UNITED STATES) ACT CODE COLLEGE NAME COUNTRY 7143 ARGENTINA UNIV OF MANAGEMENT ARGENTINA 7139 NATIONAL UNIVERSITY OF ENTRE RIOS ARGENTINA 6694 NATIONAL UNIVERSITY OF TUCUMAN ARGENTINA 7205 TECHNICAL INST OF BUENOS AIRES ARGENTINA 6673 UNIVERSIDAD DE BELGRANO ARGENTINA 6000 BALLARAT COLLEGE OF ADVANCED EDUCATION AUSTRALIA 7271 BOND UNIVERSITY AUSTRALIA 7122 CENTRAL QUEENSLAND UNIVERSITY AUSTRALIA 7334 CHARLES STURT UNIVERSITY AUSTRALIA 6610 CURTIN UNIVERSITY EXCHANGE PROG AUSTRALIA 6600 CURTIN UNIVERSITY OF TECHNOLOGY AUSTRALIA 7038 DEAKIN UNIVERSITY AUSTRALIA 6863 EDITH COWAN UNIVERSITY AUSTRALIA 7090 GRIFFITH UNIVERSITY AUSTRALIA 6901 LA TROBE UNIVERSITY AUSTRALIA 6001 MACQUARIE UNIVERSITY AUSTRALIA 6497 MELBOURNE COLLEGE OF ADV EDUCATION AUSTRALIA 6832 MONASH UNIVERSITY AUSTRALIA 7281 PERTH INST OF BUSINESS & TECH AUSTRALIA 6002 QUEENSLAND INSTITUTE OF TECH AUSTRALIA 6341 ROYAL MELBOURNE INST TECH EXCHANGE PROG AUSTRALIA 6537 ROYAL MELBOURNE INSTITUTE OF TECHNOLOGY AUSTRALIA 6671 SWINBURNE INSTITUTE OF TECH AUSTRALIA 7296 THE UNIVERSITY OF MELBOURNE AUSTRALIA 7317 UNIV OF MELBOURNE EXCHANGE PROGRAM AUSTRALIA 7287 UNIV OF NEW SO WALES EXCHG PROG AUSTRALIA 6737 UNIV OF QUEENSLAND EXCHANGE PROGRAM AUSTRALIA 6756 UNIV OF SYDNEY EXCHANGE PROGRAM AUSTRALIA 7289 UNIV OF WESTERN AUSTRALIA EXCHG PRO AUSTRALIA 7332 UNIVERSITY OF ADELAIDE AUSTRALIA 7142 UNIVERSITY OF CANBERRA AUSTRALIA 7027 UNIVERSITY OF NEW SOUTH WALES AUSTRALIA 7276 UNIVERSITY OF NEWCASTLE AUSTRALIA 6331 UNIVERSITY OF QUEENSLAND AUSTRALIA 7265 UNIVERSITY -

Securities and Exchange Commission Sec Form 17-A, As Amended

CR05818-2018 SECURITIES AND EXCHANGE COMMISSION SEC FORM 17-A, AS AMENDED ANNUAL REPORT PURSUANT TO SECTION 17 OF THE SECURITIES REGULATION CODE AND SECTION 141 OF THE CORPORATION CODE OF THE PHILIPPINES 1. For the fiscal year ended May 31, 2018 2. SEC Identification Number PW538 3. BIR Tax Identification No. 000-225-442 4. Exact name of issuer as specified in its charter FAR EASTERN UNIVERSITY, INC. 5. Province, country or other jurisdiction of incorporation or organization Philippines 6. Industry Classification Code(SEC Use Only) 7. Address of principal office Nicanor Reyes Street, Sampaloc, Manila Postal Code 1015 8. Issuer's telephone number, including area code (632) 849-4000 9. Former name or former address, and former fiscal year, if changed since last report - 10. Securities registered pursuant to Sections 8 and 12 of the SRC or Sections 4 and 8 of the RSA Title of Each Class Number of Shares of Common Stock Outstanding and Amount of Debt Outstanding COMMON 16,477,023 11. Are any or all of registrant's securities listed on a Stock Exchange? Yes No If yes, state the name of such stock exchange and the classes of securities listed therein: Philippine Stock Exchange, Inc. 12. Check whether the issuer: (a) has filed all reports required to be filed by Section 17 of the SRC and SRC Rule 17.1 thereunder or Section 11 of the RSA and RSA Rule 11(a)-1 thereunder, and Sections 26 and 141 of The Corporation Code of the Philippines during the preceding twelve (12) months (or for such shorter period that the registrant was required to file such reports) Yes No (b) has been subject to such filing requirements for the past ninety (90) days Yes No 13. -

Cover Book Final.Cdr

TOP 100 ASIA’S BEST EMPLOYER BRANDS PRASAD MEDURY Managing Director, Odgers Berndtson India Private Limited DR. HARISH MEHTA Founder & Executive Chairman of Onward Technologies Ltd (OTL). Founding Member of NASSCOM DR. SANJAY MUTHAL Executive Director, Insist Executive Search TOP 100 ASIA’S BEST EMPLOYER BRANDS One of most competitive IT-BPM Firms in the Philippines GLOBAL INTEGRATED Global Integrated Contact Facilities, Inc. (GICF) is a medium-scale, diversied IT-BPM CONTACT FACILITIES INC. solutions company that caters to domestic and international B2B and B2C organizations in high-growth industry sectors. Established in 2015, and backed by domain and functional experts with an average industry tenure of over 15 years, GICF serves as a business catalyst that brings strong value propositions across its stakeholder partnerships– through targeted, exible, and economical solutions that strive to secure and sustain enterprise- wide success objectives no matter the stage of a client’s business lifecycle. GICF and its leaders have been privileged to forge client relationships with international and domestic top-tier MNCs, large-scale businesses, and SMEs with operations across North America, Europe, and the Asia Pacic– managing variedly scaled IT-BPM projects that are simple-to-complex in nature. GICF maintains its brand promise ‘YOUR VISION, OUR SOLUTION’ as manifested in its innovative approach to addressing dynamic shifts within the IT-BPM industry and specic to the vertical and domain areas specic to every client engagement. Gcash is the Philippines' rst and leading mobile money wallet. Through the GCash App, customers can easily purchase prepaid airtime; pay bills at over 400 partner billers nationwide; send and receive money anywhere in the Philippines; pay using QR codes at MYNT (GLOBE FINTECH over 50,000 partner merchants; and invest money at money market funds through the INNOVATIONS, INC.) convenience of their smartphone. -

Corazon S. De La Paz- Bernardo

CORAZON S. DE LA PAZ- BERNARDO PROFESSIONAL CAREER . Consultant, Office of the Chairman, Social Security Commission August 1, 2008 to present . President and CEO, Social Security System August 2001 to July 31, 2008 . Vice Chairperson, Social Security Commission August 2001 to July 31, 2008 September 2004 to December . President, International Social Security Association 2010 . Chairman and Senior Partner, Joaquin Cunanan & Company/ July 1, 1981 to June 30, 2001 (PricewaterhouseCoopers – Philippines) . Member of the Board, Price Waterhouse World Firm Limited 1992 to 1995 EDUCATIONAL ATTAINMENT . Master in Business Administration, Cornell University 1965 Fulbright Grantee and University of the East Scholar . Bachelor of Business Administration, University of the East 1960 Magna Cum Laude . Certified Public Accountant 1962 First Place, 1960 Philippine CPA Board Examination . Rizal High School, Class Salutatorian 1956 PROFESSIONAL/OTHER AFFILIATIONS Board Member: . ASEAN Social Security Association 2001 to July 2008 . Philippine Social Security Association 2001 to July 2008 . Ayala Land Inc. 2006 to April 2010 President: . Social Security System 2001 to July 2008 . Cornell Club of the Philippines 1997 to 2001 . Philippine Fulbright Scholars Associations, Inc. 1995 to 2001 . Management Association of the Philippines (MAP) 1994 . Financial Executives Institute of the Philippines (FINEX) 1985 . Philippine Institute of Certified Public Accountants (PICPA) 1978 and 1979 . Association of The Outstanding Women in Nation's Service (TOWNS) 1986 to 1987 Awardees . Rizal High School Alumni Association 1989 and 1990 1 Chairman: . ISSA Committee on Management Review October 2001 to 2004 Appointed during the ISSA General Assembly in Stockholm 1994 . MAP Foundation, Inc. 1990 to 2001 . Committee on US-ASEAN Affairs, Philippine Chamber of Commerce & Industry . -

Community Students • Faculty • Officers • Personnel • Alumni Silangan

Reporting milestones about and for the April-May 2012 UE Vol. 2, No. 2 COMMUNITY Students • Faculty • Officers www.UE.edu.ph • Personnel • Alumni Silangan UE Nutrition-Dietetics Team Wins 1st Prize in National Nutrition Council Recipe Contest A TEAM OF UE NUTRITION and Dietetics students along with The Winning Nutrition Team: their faculty member-coach won (from left) Ms. the 1st Prize in a National Capital G. Maglalang, A. Region-level recipe development Besana, A. Bautista contest recently. and R. A. Gianan Specifically, in line with the celebration of the 38th National Nutrition Month Celebration in July (whose theme is “Pagkain ng Gulay Araw-Araw Itong Ihain”), the National Nutrition Council NCR Regional Office conducted a Regional Recipe Development Contest last April 27 at the San Juan Elementary School Gymnasium. The contest was aimed to develop low-cost, easy-to-prepare and nutritious vegetable dishes. Each recipe should use just five 2nd-year student Rose Ann Gianan, the Mandaluyong City government, other prize-winning concoctions, major ingredients and should be with faculty member Geraldine M. whose “Vegetable with Pineapple in a recipe book for distribution prepared in less than 30 minutes. Maglalang as their coach. The UE Coconut Sauce” was adjudged 3rd to the beneficiaries of the national About 35 recipes were submitted team prepared “Sweet Potato, Tofu Place; and consolation prize-winners government’s Pantawid Pamilya by different schools, universities and Snow Peas in Pineapple Sauce,” Manila Doctors College and Centro program. The recipe book will also and local government units. Recipes which garnered the contest-best Escolar University. -

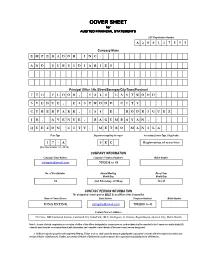

COVER SHEET for AUDITED FINANCIAL STATEMENTS

COVER SHEET for AUDITED FINANCIAL STATEMENTS SEC Registration Number A 2 0 0 1 1 7 5 9 5 Company Name EMPERADORINC. ANDSUBSIDIARIES Principal Office ( No./Street/Barangay/City/Town)Province) 7TH FLOOR, 1880 EASTWOOD AVENUE,EASTWOODCITY CYBERPARK, 188 E. RODRIGUEZ JR.AVENUE,BAGUMBAYAN, QUEZONCITY,METROMANILA Form Type Department requiring the report Secondary License Type, If Applicable 1 7 - A S E C Registration of securities (For December 31, 2015) COMPANY INFORMATION Company's Email Address Company's Telephone Number/s Mobile Number [email protected] 7092038 to 41 No. of Stockholders Annual Meeting Fiscal Year Month/Day Month/Day 24 3rd Monday of May 12/31 CONTACT PERSON INFORMATION The designated contact person MUST be an Officer of the Corporation Name of Contact Person Email Address Telephone Number/s Mobile Number DINA INTING [email protected] 7092038 to 41 Contact Person's Address 7th Floor, 1880 Eastwood Avenue, Eastwood City CyberPark, 188 E. Rodriguez, Jr. Avenue, Bagumbayan, Quezon City, Metro Manila Note 1: In case of death, resgination or cessation of office of the officer designated as contact person, such incident shall be reported to the Commission within thirty (30) calendar days from the occurrence thereof with information and complete contact details of the new contact person designated. 2: All Boxes must be properly and completely filled-up. Failure to do so shall cause the delay in updating the corporation's records with the Commission and/or non- receipt of Notice of Deficiencies. Further, non-receipt of Notice of Deficiencies shall not excuse the corporation from liability for its deficiencies.