Strategic Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

BIO-2005-MK-ONLINE (Page 1)

THE SCIENCE. THE BUSINESS. THE WORLD OF BIOPHARMACEUTICALS. 2005 MEDIA PLANNER www.biopharminternational.com THE PRINT-BASED MARKETING Display Advertising BIOPHARM The foundation of any b-to-b marketing program, print advertising allows you to BRAND touch 29,200 BPA-qualified subscribers* with your brand or product message. BioPharm International’s Build your marketing plan around the message portfolio of products allows conveyed in your print ad and utilize other channels you to reach our highly to further reinforce your message. desirable audience through multiple marketing channels. Custom Publishing Work with us to write and design a custom white paper or article Studies show integrated published as an advertorial in the pages of BioPharm. marketing is the key to successfully delivering your Insert A unique way to deliver white papers, brochures or any other collateral message to today’s buyer. material to our readers. Reinforce your message to the most important audience Polybag in your market—ask your Talk about premium placement! Send your printed piece as a ride-along advertising sales manager and readers will get the message as soon as the issue hits their desk. to design an integrated program Direct Mail utilizing the channels that best Planning a direct mail campaign to reinforce your ad message? meet your marketing objectives. Rent our list to ensure your marketing material reaches your most important audience. Post-It Note A truly unique way to send your message to our readers, Post-It Notes serve as front cover reminders about your brand. Use Post-Its to call out your ads in the issue or run 6 or 12 Post-It Notes for a truly unique campaign. -

Breaking Eroom's

Breaking Eroom’s Law Michael S. Ringel, Jack W. Scannell, Mathias Baedeker and Ulrik Schulze https://doi.org/10.1038/d41573-020-00059-3 Supplementary Box 1 | Data and analysis Breaking Eroom’s Law The count and value of NMEs relative to R&D spend comes from BCG’s New Therapeutic Drug (NTD) Database, which is also the source of BCG’s annual publication in Nat. Rev. Drug. Discov. showing trends in count and value over time.1 FDA approvals are from FDA’s Center for Drug Evaluation and Research (CDER) and Center for Biologics Evaluation and Research (CBER),2 peak sales estimates are from EvaluatePharma®,3 and R&D spend data are from BCG Value Science, inflation-adjusted using the standard global GDP-based inflator from the Economist Intelligence Unit.4 For additional details on methodology, see Schulze, Baedeker, Chen and Greber.5 Eroom’s Law is linear on a log scale through 2010, with an average increase approximately 12% per annum, or a halving of productivity approximately every seven years. If this holds true even after 2010, we would see a continuation of the linear development of the number of drugs approved per billion US$ R&D spending when using a logarithmic scale. To demonstrate that the deviation from regression after 2010 is statistically relevant we assumed the following: 1) Eroom's law is true up to 2010. 2) Eroom's law is not true between 2010 and 2018. To confirm our assumptions, we used a log-linear regression to describe the number of new molecular entities (NMEs) approved by the US FDA per billion US$ R&D spending from 1950–2010. -

Boosting Our Best Shot

NEWS FEATURE Boosting Our Best al orr a C rin Ma s by Shot ration Illust Vaccines work by training the immune system to target pathogens, but many types of shots need added substances called adjuvants to elicit a robust response. Despite the power of adjuvants, only one, called alum, is approved in the US. Charlotte Schubert looks at recent discoveries that could translate into a wider range of adjuvants and perhaps help provide future protection against diseases ranging from malaria to H1N1 ‘swine’ flu. © All rights reserved. 2009 Inc. Nature America, Max Theiler never thought it would be easy to particularly good at bumping up the immune FDA is poised to give the green light to such vanquish one of the biggest killers of his time. response. By comparison, most vaccines adjuvanted vaccines, lined up for approval in Yellow fever had already stumped a previous developed today rely on bits of microbes, such Europe, remains unclear (see sidebar). generation of microbe-hunters. And in the as short protein sequences—and they don’t For many years, researchers such as Theiler early 1900s it killed subjects who volunteered work quite so well on their own. To elicit an moved their vaccine candidates forward with for experiments in which they received bites immune response, these vaccines typically little mechanistic understanding of how they from mosquitoes, proving that the insects need a jolt from an adjuvant, a substance worked. That empirical approach is ending, transmit the disease. named from the Latin ‘adjuvans’, which says Bali Pulendran, an immunologist at the Theiler’s work was painstaking. -

Cancer Vaccines - Hope Or Hype?

DrugWatch Cancer vaccines - hope or hype? ➜ Anthony Walker* There have been many false dawns in the field of cancer vaccines, but some of the new products look distinctly promising. sing vaccines that stimulate the hysteria, safety, selectivity and potency not by normal tissues. There are numer- immune system to fight cancer remain the hallmarks of a vaccine, and ous variants: subunit and anti-idiotype Uappeals to many as a natural cancer vaccines promise efficacy with vaccines and immuno-gene therapy to approach that is both safe and effective. limited – or no – side-effects. Serious name but three. Much effort has been And, judging from a recent headline adverse events have been the exception directed toward high-tech solutions in in the UK newspaper The Times in the clinical trials of experimental vac- this area, but it has become apparent – “Vaccine jab could cure lung cancer” – cines conducted to date. At the same that tumours continue to mutate as the there is clear public interest in this area. time, there have been few glimpses of disease progresses, evading the immune Even big pharma is showing signs of real benefit, with numerous false dawns system by downregulating or losing the excitement. At a partnering conference and much disappointment. expression of the target antigen. one of the more traditional majors said But there was an explosion of interest in The third group, multivalent and ultra- cancer vaccines had moved from the ‘no this field after the unravelling of mech- valent vaccines, combine several anti- strategic interest’ category to ‘watchful anisms for triggering cytotoxic T-cell gens in one formulation to overcome waiting’ – an almost seismic shift to (CTL) response about 15 years ago. -

List of Section 13F Securities

List of Section 13F Securities 1st Quarter FY 2004 Copyright (c) 2004 American Bankers Association. CUSIP Numbers and descriptions are used with permission by Standard & Poors CUSIP Service Bureau, a division of The McGraw-Hill Companies, Inc. All rights reserved. No redistribution without permission from Standard & Poors CUSIP Service Bureau. Standard & Poors CUSIP Service Bureau does not guarantee the accuracy or completeness of the CUSIP Numbers and standard descriptions included herein and neither the American Bankers Association nor Standard & Poor's CUSIP Service Bureau shall be responsible for any errors, omissions or damages arising out of the use of such information. U.S. Securities and Exchange Commission OFFICIAL LIST OF SECTION 13(f) SECURITIES USER INFORMATION SHEET General This list of “Section 13(f) securities” as defined by Rule 13f-1(c) [17 CFR 240.13f-1(c)] is made available to the public pursuant to Section13 (f) (3) of the Securities Exchange Act of 1934 [15 USC 78m(f) (3)]. It is made available for use in the preparation of reports filed with the Securities and Exhange Commission pursuant to Rule 13f-1 [17 CFR 240.13f-1] under Section 13(f) of the Securities Exchange Act of 1934. An updated list is published on a quarterly basis. This list is current as of March 15, 2004, and may be relied on by institutional investment managers filing Form 13F reports for the calendar quarter ending March 31, 2004. Institutional investment managers should report holdings--number of shares and fair market value--as of the last day of the calendar quarter as required by Section 13(f)(1) and Rule 13f-1 thereunder. -

Cancer Vaccines Edge Towards Success

DrugWatch Cancer vaccines edge towards success ➜ Richard Harrop* and Stuart Naylor* A number of cancer vaccines are now entering the final stage of clinical development. Are vaccines finally on their way to enjoying mainstream success in the oncology arena? ver the past decade, vaccina- cines that have such a safety profile such as renal cancer and melanoma, tion strategies for the treat- may be readily integrated into current yet they offer only modest benefits and O ment of cancer have been standard-of-care regimens, particularly frequently lead to toxic side-effects. investigated with renewed vigour, per- in the first-line setting where combi- In between these two approaches haps catalysed by a greater under- nation strategies prevail over lie cell-based therapies, in which whole standing of tumour immunology and monotherapies. tumour cells or cell extracts are used as the clinical successes achieved with the immunogen. While tumour-specific monoclonal antibody and cytokine- TARGETED VS NON-SPECIFIC immune responses may be induced, based therapies. However, before vac- Cancer immunotherapies can broadly the precise target(s) of the response is cines become fully integrated into the be divided into two categories: not usually known. Furthermore, arsenal of weapons currently used to tumour-specific and highly-targeted immune responses against other com- treat cancer, they must show not only products, for example vaccines or mon tissue antigens may also be efficacy but also safety and limited or antibodies that target a specific induced. Despite the lack of fine no toxicity. Recently, a number of tumour antigen, and therapies which specificity of the immune response cancer vaccines have moved into the modulate the immune system in a induced and the labour involved in the stages of development where clinical non-tumour-specific way. -

Promotion and Development Collaborations Between Established Players

Promotion and Development Collaborations Between Established Players Randall B. Sunberg Pharma and Biotech In-Licensing, Co-Development and Co-Promotion Agreements October 21-22, 2002 1 www.morganlewis.com MorganMorgan Lewis:Lewis: LifeLife SciencesSciences FocusFocus • Founded in 1873, today 1,100 lawyers in 13 offices worldwide • 175 Life Sciences professionals, including 90 with advanced degrees ranging from biochemistry to molecular genetics to immunology • Interdisciplinary coordination of transactions, IP, litigation, FDA and antitrust expertise to meet our clients’ strategic objectives • Recently ranked as the 5th leading transactional law firm in the nation by The American Lawyer "Corporate Scorecard” • Named by many Fortune 250 companies as one of their primary law firms • Recognized by corporate counsel for exceptional client service in a survey of Fortune 1000 companies • Featured prominently in the annual National Law Journal survey of “Who Defends Corporate America” 2 MorganMorgan Lewis:Lewis: RecentRecent LifeLife SciencesSciences DealsDeals • Aventis - Genta collaboration for co-development and commercialization of Genasense™ • Enzon - Elan acquisition of Abelcet® product rights and manufacturing assets • Quintiles - Eli Lilly co-promotion and marketing collaboration for Cymbalta™ • Adolor - GlaxoSmithKline development and commercialization collaboration for Alvimopan™ • Arena Pharmaceuticals - Merck drug discovery collaboration • Cephalon - Anesta stock-for-stock public company acquisition • Aventis - Millennium alliance -

How Scientist/Founders Lead Successful Biopharmaceutical

Antioch University AURA - Antioch University Repository and Archive Student & Alumni Scholarship, including Dissertations & Theses Dissertations & Theses 2008 How Scientist/Founders Lead Successful Biopharmaceutical Organizations: A Study of Three Companies Lynn Johnson Langer Antioch University - PhD Program in Leadership and Change Follow this and additional works at: http://aura.antioch.edu/etds Part of the Business Administration, Management, and Operations Commons, Medicine and Health Sciences Commons, and the Organizational Behavior and Theory Commons Recommended Citation Langer, Lynn Johnson, "How Scientist/Founders Lead Successful Biopharmaceutical Organizations: A Study of Three Companies" (2008). Dissertations & Theses. 138. http://aura.antioch.edu/etds/138 This Dissertation is brought to you for free and open access by the Student & Alumni Scholarship, including Dissertations & Theses at AURA - Antioch University Repository and Archive. It has been accepted for inclusion in Dissertations & Theses by an authorized administrator of AURA - Antioch University Repository and Archive. For more information, please contact [email protected], [email protected]. HOW SCIENTIST/FOUNDERS LEAD SUCCESSFUL BIOPHARMACEUTICAL ORGANIZATIONS: A STUDY OF THREE COMPANIES Lynn Johnson Langer A DISSERTATION Submitted to the Ph.D. in Leadership & Change Program of Antioch University in partial fulfillment of the requirements for the degree of Doctor of Philosophy May, 2008 This is to certify that the dissertation entitled: HOW SCIENTIST/FOUNDERS -

Speaker Bios 2Nd FDA/PQRI Conference on Advancing Product Quality

Speaker Bios 2nd FDA/PQRI Conference on Advancing Product Quality Professor Bertil Abrahamsson, Ph.D. Dr. Abrahamsson has a broad experience of industrial drug development from more than 25 years of work with Astra and AstraZeneca. During this period he has had various line and project management positions. Presently he is a Senior Principal Scientist with emphasis on biopharmaceutics., In this role he is leading biopharmaceutics research and product development support on a global basis. In addition, as one of the most senior scientists in AZ Pharmaceutical Development he is also a member of the local as well as the extended global leadership teams. Dr. Abrahamsson is an internationally recognised scientist and he has published more than 80 papers in the area of oral biopharmaceutics and drug delivery. He is presently an adjunct Professor in Biopharmaceutics at Uppsala University. He initiated and is currently leading a major european private public partnership project in oral biopharmaceutics area ( http://www.orbitoproject.eu). Ilgaz Akseli, Ph.D., MBA Dr. Akseli is a Senior Associate Director in the Pharmaceutical Development department in Boehringer-Ingelheim Pharmaceuticals, Ridgefield, CT. He is the head of the Formulation Material Profiling and Computational Modeling Labs. Two labs are in the global level and his team is guiding and supporting the formulation and process development for drug candidates in assigned therapeutic areas. Dr. Akseli earned his BSc degree in Mechanical Engineering with a focus on Design of Powder Compaction. He has two MSc degrees; one is in Materials Science and Engineering from University College London with a focus on Metal Powder Compaction and the other degree is in Business Management from London School of Economics with a focus on Lean Six Sigma implementations in the Pharmaceutical Industry. -

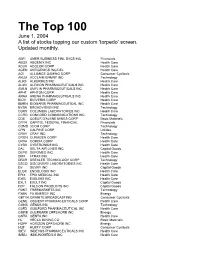

The Bottom 99

The Top 100 June 1, 2004 A list of stocks topping our custom 'torpedo’ screen. Updated monthly. ABFI AMER BUSINESS FINL SVCS INC Financials ABGX ABGENIX INC Health Care ADLR ADOLOR CORP Health Care AGEN ANTIGENICS INC/DEL Health Care AGI ALLIANCE GAMING CORP Consumer Cyclicals AKLM ACCLAIM ENMNT INC Technology ALKS ALKERMES INC Health Care ALXN ALEXION PHARMACEUTICALS INC Health Care AMLN AMYLIN PHARMACEUTICALS INC Health Care APHT APHTON CORP Health Care ARNA ARENA PHARMACEUTICALS INC Health Care BIOV BIOVERIS CORP Health Care BMRN BIOMARIN PHARMACEUTICAL INC Health Care BVSN BROADVISION INC Technology CBRX COLUMBIA LABORATORIES INC Health Care CCRD CONCORD COMMUNICATIONS INC Technology CDE COEUR D'ALENE MINES CORP Basic Materials CFFN CAPITOL FEDERAL FINANCIAL Financials COMS 3COM CORP Technology CPN CALPINE CORP Utilities CRAY CRAY INC Technology CRGN CURAGEN CORP Health Care CRXA CORIXA CORP Health Care CYBX CYBERONICS INC Health Care DAL DELTA AIR LINES INC Capital Goods DEPO DEPOMED INC Health Care DMX I-TRAX INC Health Care DRXR DREXLER TECHNOLOGY CORP Technology DSCO DISCOVERY LABORATORIES INC Health Care DV DEVRY INC Capital Goods ELGX ENDOLOGIX INC Health Care EPIX EPIX MEDICAL INC Health Care EXEL EXELIXIS INC Health Care EXLT EXULT INC Capital Goods FCP FALCON PRODUCTS INC Capital Goods FMKT FREEMARKETS INC Technology FXEN FX ENERGY INC Energy GBTVK GRANITE BROADCASTING Consumer Cyclicals GENE OSCIENT PHARMACEUTICALS CORP Health Care GGNS GENUS INC Technology GLFD GUILFORD PHARMACEUTICAL INC Health Care GMRK GULFMARK OFFSHORE -

Pierre Cremieux October 2020 CV (English)

PIERRE-YVES CREMIEUX, PH.D. President Office: 617 425 8135 111 Huntington Avenue Fax: 617 425 8001 14th Floor [email protected] Boston, MA 02199 Pierre-Yves Cremieux, President of Analysis Group, has a broad range of expertise in health economics, antitrust, statistics, and labor economics. He has consulted to numerous clients in the United States and Canada and testified in bench and jury trials, arbitrations, and administrative proceedings. Dr. Cremieux has served as an expert and supported other experts in both litigation and non-litigation matters on antitrust issues; general commercial claims; contractual disputes; and a number of labor- related matters in a variety of industries, including high tech, pharmaceuticals, biotech, financial products, consumer products, and commodities. He has assessed the evaluation of damages on a class-wide basis in some of the largest class action matters in recent years. His scientific research in antitrust economics, class certification, health economics, and statistics has been published in numerous peer-reviewed journals, including the George Mason Law Review, the American Bar Association Economics Committee Newsletter, The Review of Economics and Statistics, the Journal of Health Economics, Industrial and Labor Relations Review, the Journal of Clinical Oncology, and The American Journal of Managed Care. Dr. Cremieux’s research has been cited in leading media outlets including The Wall Street Journal and Forbes. Dr. Cremieux has frequently presented at leading legal, health care, and economics seminars on topics such as antitrust, class certification, health economics, and statistics, in both the United States and Canada. He has also been invited to teach courses on economics, statistics, health care, and antitrust at various schools including McGill University, Boston University, Harvard Medical School, and the Yale School of Management. -

How Scientist/Founders Lead Successful

HOW SCIENTIST/FOUNDERS LEAD SUCCESSFUL BIOPHARMACEUTICAL ORGANIZATIONS: A STUDY OF THREE COMPANIES Lynn Johnson Langer A DISSERTATION Submitted to the Ph.D. in Leadership & Change Program of Antioch University in partial fulfillment of the requirements for the degree of Doctor of Philosophy May, 2008 This is to certify that the dissertation entitled: HOW SCIENTIST/FOUNDERS LEAD SUCCESSFUL BIOPHARMACEUTICAL ORGANIZATIONS: A STUDY OF THREE COMPANIES prepared by Lynn Johnson Langer is approved in partial fulfillment of the requirements for the degree of Doctor of Philosophy in Leadership & Change. Approved by: ______________________________________________________________________ Alan E. Guskin, Ph.D., Chair date ______________________________________________________________________ Jon Wergin, Ph.D., Committee Member date ______________________________________________________________________ Mitch Kusy, Ph.D., Committee Member date ______________________________________________________________________ Alice Sapienza, DBA, External Reader date Copyright 2008 Lynn Johnson Langer All rights reserved Acknowledgements I arrive at this place in my journey to becoming a scholar supported in love and friendship by so many people. I must thank first and foremost my husband, Eric Langer, who has supported me in many ways, but particularly with my education. I thank my daughter, Julia Annemarie, my study partner. We shout across the hall to each other, complaining and laughing about all the work. I thank her for her support and the opportunity to be a role model. She never once complained about the plays and events I missed because I was away at a residency. I thank my son, Adam and his wife, Megan who through their lives, remind me to follow my dreams. I thank my son, Benjamin, who shows me that through hard work, we can accomplish great things.