An Overview of Power Sector of Bangladesh

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Bangladesh, Year 2019: Update on Incidents According to the Armed Conflict Location & Event Data Project (ACLED)

BANGLADESH, YEAR 2019: Update on incidents according to the Armed Conflict Location & Event Data Project (ACLED) compiled by ACCORD, 29 June 2020 Number of reported incidents with at least one fatality Number of reported fatalities National borders: GADM, November 2015b; administrative divisions: GADM, November 2015a; China/India border status: CIA, 2006; geodata of disputed borders: GADM, November 2015b; Natural Earth, undated; incident data: ACLED, 20 June 2020; coastlines and inland waters: Smith and Wessel, 1 May 2015 BANGLADESH, YEAR 2019: UPDATE ON INCIDENTS ACCORDING TO THE ARMED CONFLICT LOCATION & EVENT DATA PROJECT (ACLED) COMPILED BY ACCORD, 29 JUNE 2020 Contents Conflict incidents by category Number of Number of reported fatalities 1 Number of Number of Category incidents with at incidents fatalities Number of reported incidents with at least one fatality 1 least one fatality Protests 930 1 1 Conflict incidents by category 2 Riots 405 107 122 Development of conflict incidents from 2010 to 2019 2 Violence against civilians 257 184 195 Battles 99 43 63 Methodology 3 Strategic developments 15 0 0 Conflict incidents per province 4 Explosions / Remote 7 2 2 violence Localization of conflict incidents 4 Total 1713 337 383 Disclaimer 6 This table is based on data from ACLED (datasets used: ACLED, 20 June 2020). Development of conflict incidents from 2010 to 2019 This graph is based on data from ACLED (datasets used: ACLED, 20 June 2020). 2 BANGLADESH, YEAR 2019: UPDATE ON INCIDENTS ACCORDING TO THE ARMED CONFLICT LOCATION & EVENT DATA PROJECT (ACLED) COMPILED BY ACCORD, 29 JUNE 2020 Methodology GADM. Incidents that could not be located are ignored. -

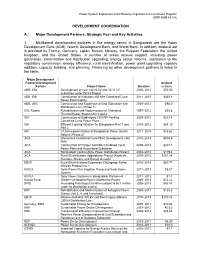

Development Coordination

Power System Expansion and Efficiency Improvement Investment Program (RRP BAN 42378) DEVELOPMENT COORDINATION A. Major Development Partners: Strategic Foci and Key Activities 1. Multilateral development partners in the energy sector in Bangladesh are the Asian Development Bank (ADB), Islamic Development Bank, and World Bank. In addition, bilateral aid is provided by France, Germany, Japan, Kuwait, Norway, the Russian Federation, the United Kingdom, and the United States. A number of areas receive support, including power generation, transmission and distribution upgrading, energy sector reforms, assistance to the regulatory commission, energy efficiency, rural electrification, power plant upgrading capacity addition, capacity building, and planning. Financing by other development partners is listed in the table. Major Development PartnersDevelopment Amount Partner Project Name Duration (million) ADB, KfW Development of new 132/33 kV and 33/11 kV 2006–2012 $53.00 substation under DESA Project ADB, IDB Construction of Ashuganj 450 MW Combined Cycle 2011–2015 $365.4 Power Plant (North) ADB, JBIC Construction and Expansion of Grid Substation with 2005–2012 $94.0 Distribution Line (Phase 1) CIS, Russia Rehabilitation and Modernization of Ghorashal 1997–2012 $30.8 Thermal Power Station Unit 1 and 2 IDA Construction of Siddhirganj 335 MW Peaking 2009–2015 $253.4 Combined Cycle Power Plant IDA Efficient Lighting Initiative for Bangladesh Part 1 and 2009–2012 $34.10 Part 2 IDA TA for Implementation of Bangladesh Power Sector 2011–2015 $16.62 Reform -

Ls&Co. Bangladesh Fire Safety and Building Integrity Program

g in progress LEGEND LS&CO. BANGLADESH FIRE SAFETY AND BUILDING INTEGRITY PROGRAM g completed STATUS REPORT MARCH 2018 FIRE SAFETY(1) ELECTRICAL AUDIT BUILDING STABILITY INSPECTION factory factory housing in housing in # of workers Phase I Phase II multi- multi- employed by status of 2013 status of Status of Gravity Loading Status of Detailed POSTAL purpose factory factory (all assessment corrective corrective and Seismic Inspections Engineering Analysis status of corrective FACTORY NAME ADDRESS REGION CODE building building buildings) (annual) action status of audit action (ASCE31)(2) (DEA) action(3) Plot-246-249, Adamjee EPZ, Siddhirganj, Narayanganj Dhaka 1430 No No 2017 Complete 2017- complete complete 2017 - complete 2017 - complete In Progress Ananta Apparels Ltd 2702 Ananta Denim Technology Ltd. Kashpara, Noyabari, Kanchpur, Narayanganj Dhaka 1430 No No 4300 2015 Complete 2015 - complete complete 2015 - complete NA 2015- complete Cosmopolitan Industries Pvt. Ltd Khejur Bagan, Bara Ashulia, Savar Dhaka 1341 No No 4300 2013 Complete 2011 - complete complete 2014 - complete 2014 - complete 2015- complete Cutting Edge Industries Ltd (Washing Plant) 1612, South Salna, Salna Bazar, Gazipur Dhaka 1702 No No 495 2017 Complete 2017-complete complete 2016- complete NA NA Denimach Ltd Kewa Mouja, Ward No. 5, Sreepur, Gazipur Dhaka 1740 No No 6500 2013 Complete 2012 - complete complete 2014 - complete 2014 - complete 2015- complete Dhaka 1340 No No 5295 2017 Complete 2017- complete complete 2017 - complete 2018 - complete In Progress Denitex Ltd 9/1, Karnapara, Savar Karnaphuli Shoes Industries Ltd. (Garments Unit) Korean Export Processing Zone, Anwara, Chittagong. Chittagong 4371 No No 6111 2016 Complete 2016 - complete complete 2016 - complete 2016 - complete 2016 - complete* Kenpark Bangladesh Pvt.Ltd (Unit 1) Sector 8, Plot 31-42, Chittagong Export Processing Zone Chittagong 4223 No No 3400 2013 Complete 2012 - complete complete 2014 - complete 2014 - complete 2015- complete Lalmai Sportswear Inds. -

Feasible Micro Hydro Potentiality Exploration in Hill Tracts Of

Global Journal of Researches in Engineering Electrical and Electronics Engineering Volume 12 Issue 9 Version 1.0 Year 2012 Type: Double Blind Peer Reviewed International Research Journal Publisher: Global Journals Inc. (USA) Online ISSN: 2249-4596 & Print ISSN: 0975-5861 Feasible Micro Hydro Potentiality Exploration in Hill Tracts of Bangladesh By Khizir Mahmud, Md. Abu Taher Tanbir & Md. Ashraful Islam Chittagong University of Engineering & Technology (CUET), Bangladesh Abstract - The energy demand is expected to grow rapidly in most developing countries over the next decades. For Bangladesh, economic growth has been accelerating and it is expected that the population will grow from an estimated 162.20 million people in 2011 to 200 million by 2050, with almost half of the population living in urban areas. For meeting the expected energy demand as the population will rise and to sustain economic growth, alternative form of energy – renewable energy needs to be expanded. This paper tries to explore the possibility of finding the renewable energy mainly from micro hydro in different places of Chittagong hill tract region by thoroughly describing present condition of energy along with data collection, calculation and feasibility of power generation from July 2011 to Jan 2012. Keywords : Bangladesh hill tract region, micro hydro, renewable energy. GJRE-F Classification : FOR Code: 090608 Feas ibleMicroHydroPotentialityExplorationinHillTractsofBangladesh Strictly as per the compliance and regulations of: © 2012. Khizir Mahmud, Md. Abu Taher Tanbir & Md. Ashraful Islam. This is a research/review paper, distributed under the terms of the Creative Commons Attribution-Noncommercial 3.0 Unported License http://creativecommons.org/licenses/by-nc/3.0/), permitting all non commercial use, distribution, and reproduction in any medium, provided the original work is properly cited. -

Zila Report : Narayanganj

POPULATION & HOUSING CENSUS 2011 ZILA REPORT : NARAYANGANJ Bangladesh Bureau of Statistics Statistics and Informatics Division Ministry of Planning BANGLADESH POPULATION AND HOUSING CENSUS 2011 Zila Report: NARAYANGANJ October 2015 BANGLADESH BUREAU OF STATISTICS (BBS) STATISTICS AND INFORMATICS DIVISION (SID) MINISTRY OF PLANNING GOVERNMENT OF THE PEOPLE’S REPUBLIC OF BANGLADESH ISBN-978-984-33-8615-1 COMPLIMENTARY Published by Bangladesh Bureau of Statistics (BBS) Statistics and Informatics Division (SID) Ministry of Planning Website: www.bbs.gov.bd This book or any portion thereof cannot be copied, microfilmed or reproduced for any commercial purpose. Data therein can, however, be used and published with acknowledgement of their sources. Contents Page Message of Honorable Minister, Ministry of Planning …………………………………………….. vii Message of Honorable State Minister, Ministry of Finance and Ministry of Planning …………. ix Foreword ……………………………………………………………………………………………….. xi Preface …………………………………………………………………………………………………. xiii Zila at a Glance ………………………………………………………………………………………... xv Physical Features ……………………………………………………………………………………... xix Zila Map ………………………………………………………………………………………………… xxi Geo-code ………………………………………………………………………………………………. xxii Chapter-1: Introductory Notes on Census ………………………………………………………….. 1 1.1 Introduction ………………………………………………………………………………… 1 1.2 Census and its periodicity ………………………………………………………………... 1 1.3 Objectives ………………………………………………………………………………….. 1 1.4 Census Phases …………………………………………………………………………… 2 1.5 Census Planning …………………………………………………………………………. -

NO PLACE for CRITICISM Bangladesh Crackdown on Social Media Commentary WATCH

HUMAN RIGHTS NO PLACE FOR CRITICISM Bangladesh Crackdown on Social Media Commentary WATCH No Place for Criticism Bangladesh Crackdown on Social Media Commentary Copyright © 2018 Human Rights Watch All rights reserved. Printed in the United States of America ISBN: 978-1-6231-36017 Cover design by Rafael Jimenez Human Rights Watch defends the rights of people worldwide. We scrupulously investigate abuses, expose the facts widely, and pressure those with power to respect rights and secure justice. Human Rights Watch is an independent, international organization that works as part of a vibrant movement to uphold human dignity and advance the cause of human rights for all. Human Rights Watch is an international organization with staff in more than 40 countries, and offices in Amsterdam, Beirut, Berlin, Brussels, Chicago, Geneva, Goma, Johannesburg, London, Los Angeles, Moscow, Nairobi, New York, Paris, San Francisco, Sydney, Tokyo, Toronto, Tunis, Washington DC, and Zurich. For more information, please visit our website: http://www.hrw.org MAY 2018 ISBN: 978-1-6231-36017 No Place for Criticism Bangladesh Crackdown on Social Media Commentary Summary ........................................................................................................................... 1 Information and Communication Act ......................................................................................... 3 Punishing Government Critics ...................................................................................................4 Protecting Religious -

ENVIRONMENTAL ASSESSMENT of WORLD BANK Public Disclosure Authorized FINANCED 2 X 150 MW GAS TURBINE POWER PLANT at SIDDHIRGANJ

POWER CELL, POWER DIVISION MINISTRY OF POWER, ENERGY AND MINERAL RESOURCES GOVERNMENT OF BANGLADESH ENVIRONMENTAL ASSESSMENT OF WORLD BANK Public Disclosure Authorized FINANCED 2 x 150 MW GAS TURBINE POWER PLANT AT SIDDHIRGANJ VOL. I REVISED Public Disclosure Authorized Public Disclosure Authorized FINAL REPORT VOLUME 1: MAIN REPORT Public Disclosure Authorized Bureau of Research, Testing and Consultation (BRTC) Bangladesh University of Engineering & Technology (BUET), Dhaka Dec -2fJO7 POWER CELL, POWER DIVISION MINISTRY OF POWER, ENERGY AND MINERAL RESOURCES GOVERNMENT OF BANGLADESH ENVIRONMENTAL ASSESSMENT OF WORLD BANK FINANCED 2 x 150 MW GAS TURBINE POWER PLANT AT SIDDHIRGANJ FINAL REPORT (Revised December 2007) VOLUME 1: MAIN REPORT Bureau of Research, Testing and Consultation (BRTC) Bangladesh University of Engineering & Technology (BUET), Dhaka December 2007 Executive Summary INTRODUCTION In order to increase the capacity of electricity production, the Ministry of Power, Energy and Mineral Resources, GOB has planned to establish a 2x1 50 MW Gas Turbine Peaking Power Plant at Siddhirga~ljwith the financial assistance of the World Bank. According to the Bangladesh Environment Conservation Rules 1997 (GOB, 1997), construction of a power plant project falls under the RED category. Initial Environmental Examination (IEE) followed by Environmental Impact Assessment (EIA) including Environmental Management Plan are required for these types of projects for getting environmental clearance from the Department of Environment (DOE). According to the World Bank (1999) operational policy OP 4.01, this project is classified as an Environmental Category A project, requiring an Environmental Assessment for the construction and operation of the project with recommendations for appropriate mitigation and management measures. Since a detailed environmental assessment of the proposed project is being carried out, the DOE has exempted the IEE of the project in response to the request by the Electricity Generation Company of Bangladesh Limited (EGCB). -

Ashuganj 400 MW Combined Cycle Power Plant (East)

Environmental Impact Assessment (Annex 16-Part 2) May 2016 Bangladesh: Power System Expansion and Efficiency Improvement Investment Program (Tranche 3) Ashuganj 400 MW Combined Cycle Power Plant (East) Prepared by Ashuganj Power Station Company Limited (APSCL) for the Asian Development Bank. This is an updated version of the draft EIA posted in October 2015 available on http://www.adb.org/projects/documents/ashuganj-400mw-ccpp-east-updated-eia This environmental impact assessment is a document of the borrower. The views expressed herein do not necessarily represent those of ADB's Board of Directors, Management, or staff, and may be preliminary in nature. Your attention is directed to the “terms of use” section on ADB’s website. In preparing any country program or strategy, financing any project, or by making any designation of or reference to a particular territory or geographic area in this document, the Asian Development Bank does not intend to make any judgments as to the legal or other status of any territory or area. Erosion The Meghna river banks suffer from erosion problems annually, mostly in the monsoon and post monsoon periods. As the transmission line will not have any impact on erosion, a further detailed analysis of erosion was not required for the project. Flooding Flooding situation of the study area is very nominal. The local people informed that, only the historical flash flood occurred in the year of 1988, 1998 and 2004. Flooding of 1988 and 1998 severely affected almost the entire study area. The duration of 1988 and 1998 flood was around 1-1.5 months with flood level of 6-7 ft. -

SREP Investment Plan for Bangladesh

Sustainable & Renewable Energy Development Authority Power Division Ministry of Power, Energy, & Mineral Resources Government of the Peoples Republic of Bangladesh Scaling Up Renewable Energy in Low Income Countries (SREP) Investment Plan for Bangladesh October 2015 Government of the People’s Republic of Bangladesh Sustainable and Renewable Development Authority (SREDA) Power Division Ministry of Power, Energy & Mineral Resources www.sreda.gov Ref No: 27.02.0000.000.24.002.14-501 Date: 11/10/2015 Subject: Submission of SREP IP for Bangladesh I am pleased to submit the Investment Plan (IP) of Bangladesh’s Scaling-Up Renewable Energy Program (SREP) to the SREP Sub-Committee for endorsement. The SREP Investment Plan for Bangladesh has developed in collaboration and consultation with representatives from Government, particularly with the Sustainable and Renewable Energy Development Authority (SREDA), private industries, academia and with the expertise and support of our development partners, the World Bank Group and Asian Development Bank. The Government of Bangladesh is committed to the development of a stable and sustainable power supply that will increase electricity access, enhance energy security, reduce poverty and mitigate climate change. The Government recognizes the important role that renewable energy can play in achieving these goals. The Government has set a goal of total electrification by 2020, and has called for the development of domestic renewable energy resources to ensure that the share of domestic energy supply would remain over 50 percent. Renewable energy resources will ensure a stable and universal power supply that will reduce poverty by sustainable socio-economic growth. Though Bangladesh has a negligible carbon footprint, but remains one of the most vulnerable nations in the world for the effect of climate change, and we recognize the important role that renewable energy can play in reducing associated risks. -

New Template As on 09 May 2013

MID-TERM SCREENING AND SCOPING REPORT Volume 2: Mid-Term Scoping Report Prepared for the Strategic Environmental Assessment of South West Region of Bangladesh for Conserving the Outstanding Universal Value of the Sundarbans Dedication The SEA Team dedicates this report to our colleague and friend, Dr Jean Jean-Roger Mercier, who passed away on 5th July 2020 after a short illness. He gave us sage advice, guidance, wit and inspiration. We shall miss him. Acknowledgements This SEA was commissioned by the Bangladesh Forest Department of the Ministry of Environment, Forestry and Climate Change. The SEA Team is grateful to the SEA Project Director, Mr Md Zaheer Iqbal, Deputy Conservator of Forests, for his guidance and support. Grateful thanks are especially due to all those organisations and individuals who have provided information, advice and support, and participated in video-based meetings to discuss the approach and focus of the SEA. In particular, the team would like to thank colleagues in UNESCO for their sharing their perspectives on the SEA, IUCN for its support in identifying and sourcing materials concerning transboundary issues, and the Netherlands Commission for Environmental Assessment for its advice to the Ministry of Environment, Forest and Climate Change on the conduct of the SEA. i ii Transparency Statement This Mid-Term Scoping Report is a product of the strategic environmental assessment of the South West Region and Sundarbans, It is intended to provide information on the scoping phase of the SEA and progress to date, and is produced in support policy-making, planning and decision- taking by the government of Bangladesh. -

Development Coordination

SASEC Bangladesh India Electrical Grid Interconnection Project – Additional Financing (RRP BAN 44192) DEVELOPMENT COORDINATION A. Major Development Partners: Strategic Foci and Key Activities 1. Multilateral development partners in the energy sector in Bangladesh are the Asian Development Bank (ADB), Islamic Development Bank, and the World Bank. In addition, bilateral aid comes from France, Germany, Japan, Kuwait, Norway, the Russian Federation, the United Kingdom, and the United States. Subsectors receiving support include power generation, transmission and distribution upgrading, energy sector reforms and sector planning, energy efficiency, rural electrification, generation plant upgrades, and capacity building. Financing by other development partners is listed in the table. Major Development Partners Development Project Name Duration Amount Partner (million) ADB, KfW Development of New 132/33 kV and 33/11 kV Substation under 2006–2012 $53.00 DESA Project ADB, IDB Construction of Ashuganj 450 MW Combined-Cycle Power Plant 2011–2015 $365.40 (North) ADB, JBIC Construction and Expansion of Grid Substation with Distribution 2005–2012 $94.00 Line (Phase 1) CIS, Russian Rehabilitation and Modernization of Ghorashal Thermal Power 1997–2012 $30.80 Federation Station Unit 1 and 2 DFID Increasing Palli Bidyut Samiti’s customers by 1 million under its 2006–2013 $42.41 distribution system KfW Rehabilitation and Modernization of Ashuganj Power Station Unit 2000–2011 $125.00 3, 4, and 5 (revised) EDCF Bibiana-Kaliakoir 400 kV and Fenchuganj–Bibiana -

Institutional and Regulatory Economics of Electricity Market Reforms: the Evidence from India, Pakistan, Bangladesh, Nepal, and Sri Lanka

Institutional and Regulatory Economics of Electricity Market Reforms: the Evidence from India, Pakistan, Bangladesh, Nepal, and Sri Lanka by Bipulendu Singh A Dissertation submitted to The Faculty of Columbian College of Arts and Sciences of The George Washington University in partial fulfillment of the requirements for the degree of Doctor in Philosophy May 17, 2015 Dissertation directed by Gerald W. Brock Professor of Telecommunication and of Public Policy and Public Administration The Columbian College of Arts and Sciences of The George Washington University certifies that Bipulendu Singh has passed the Final Examination for the degree of Doctor of Philosophy as of 18 February 2015. This is the final and approved form of the dissertation. Institutional and Regulatory Economics of Electricity Market Reforms: the Evidence from India, Pakistan, Bangladesh, Nepal and Sri Lanka Bipulendu Singh Dissertation Research Committee: Gerald Brock, Professor of Telecommunication and of Public Policy and Public Administration, Dissertation Director Christopher Carrigan, Assistant Professor of Public Policy and Public Administration, Committee Member Davida Wood, Project Manager, World Resources Institute, Committee Member ii © Copyright 2015 by Bipulendu Singh All rights reserved iii Dedication I dedicate this work to Monika and Zev. iv Acknowledgements I am greatly indebted to many people for helping me in this journey. My professors at Wabash College, Ms. Joyce Burnette, Ms. Joyce Castro and Mr. William Placher (Late) were instrumental in inculcating a love of learning and scholarship in me. My supervisors at the Asian Development Bank, Mr. Sultan Hafeez Rahman and Mr. Sungsup Ra made me appreciate the links between economics and development and inspired me to continue my studies in this field.