FTSE Russell. Your Global Index Partner

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Tracking Errors of Exchange Traded Funds in Bursa Malaysia

Munich Personal RePEc Archive Tracking Errors of Exchange Traded Funds in Bursa Malaysia Ku, Alfred Ing-Soon and Liew, Venus Khim-Sen and Puah, Chin-Hong RHB Investment Bank Berhad, 102, Pusat Pedada, Jalan Pedada, 96000 Sibu, Sarawak, Malaysia., Faculty of Economics and Business, Universiti Malaysia Sarawak, Jalan Datuk Mohammad Musa, 94300 Kota Samarahan, Sarawak., Faculty of Economics and Business, Universiti Malaysia Sarawak, Jalan Datuk Mohammad Musa, 94300 Kota Samarahan, Sarawak. 2019 Online at https://mpra.ub.uni-muenchen.de/107990/ MPRA Paper No. 107990, posted 27 May 2021 07:20 UTC Tracking Errors of Exchange Traded Funds in Bursa Malaysia Alfred Ing-Soon Ku RHB Investment Bank Berhad, 102, Pusat Pedada, Jalan Pedada, 96000 Sibu, Sarawak, Malaysia. Tel: 6-084-329214 E-mail: [email protected] Venus Khim-Sen Liew Faculty of Economics and Business, Universiti Malaysia Sarawak, Jalan Datuk Mohammad Musa, 94300 Kota Samarahan, Sarawak. Tel: 6-082-584291 (Corresponding Author) E-mail: [email protected] Chin-Hong Puah Faculty of Economics and Business, Universiti Malaysia Sarawak, Jalan Datuk Mohammad Musa, 94300 Kota Samarahan, Sarawak. Tel: 6-082-584294 E-mail: [email protected] Citation: Liew, V.K.-S, Ku, A. I.-S., & Puah, C.-H. 2019. Tracking Errors of Exchange Traded Funds in Bursa Malaysia. Asian Journal of Accounting and Finance, 11(2), 96-109. Abstract This study measures the tracking errors of exchange traded funds (ETFs) listed in Bursa Malaysia. Five measures of tracking errors are estimated in this study for the seven ETFs involved. Overall, the best ETF is METFAPA with the least tracking error. -

2017 Contributing Editors Joshua Ford Bonnie and Kevin P Kennedy

GETTING THROUGH THE DEAL Initial Public Offerings Initial Public Offerings Public Initial Contributing editors Joshua Ford Bonnie and Kevin P Kennedy 2017 Law Business Research 2017 © Law Business Research 2016 Initial Public Offerings 2017 Contributing editors Joshua Ford Bonnie and Kevin P Kennedy Simpson Thacher & Bartlett LLP Publisher Law The information provided in this publication is Gideon Roberton general and may not apply in a specific situation. [email protected] Business Legal advice should always be sought before taking Research any legal action based on the information provided. Subscriptions This information is not intended to create, nor does Sophie Pallier Published by receipt of it constitute, a lawyer–client relationship. [email protected] Law Business Research Ltd The publishers and authors accept no responsibility 87 Lancaster Road for any acts or omissions contained herein. Although Senior business development managers London, W11 1QQ, UK the information provided is accurate as of July 2016, Alan Lee Tel: +44 20 3708 4199 be advised that this is a developing area. [email protected] Fax: +44 20 7229 6910 Adam Sargent © Law Business Research Ltd 2016 Printed and distributed by [email protected] No photocopying without a CLA licence. Encompass Print Solutions First published 2015 Tel: 0844 2480 112 Dan White Second edition [email protected] ISSN 2059-5484 © Law Business Research 2016 CONTENTS Global overview 5 Japan 51 Joshua Ford -

Monthly Economic Update

122 Winnebago Street, Decorah, IA 52101 309 HWY 150 N, West Union, IA 52175 1-877-566-9468 Text: 563-412-4770 [email protected] Visit us at www.knoxfin.com In this month’s recap: stocks stay in rally mode, helped by hints that the U.S. and China may be closing in on a phase-one trade deal; hiring bounces back; key real estate indicators look stronger. Monthly Economic Update Presented by Jason Knox, AIF®, CRC®, December 2019 THE MONTH IN BRIEF The S&P 500 rose 3.4% in November and attained a series of record closes in the process. Earnings results helped stocks, as did intermittent signals that the first stage of a U.S.-China trade agreement might be near at hand. Job creation improved, and consumer spending lived up to market expectations; consumer confidence and business activity, not so much. Housing indicators communicated good news, and the rally in stocks made the commodity sector look less attractive. DOMESTIC ECONOMIC HEALTH Were the U.S. and China close to signing off on the first phase of a new trade deal? According to officials from both countries, the answer was yes. When would this phase- one deal be finalized? No definite answer emerged. On November 8, President Donald Trump said that such an agreement was near, and six days later, White House economic advisor Larry Kudlow said that negotiators were “getting close” to an accord. On November 26, China’s commerce ministry announced that trade representatives had “reached a consensus” on remaining issues, and President Trump said that negotiators were in the “final throes of a very important deal.” Still, November ended without any announcement that a phase-one pact had been reached.2,3 The Department of Labor’s latest employment report found that the economy generated 128,000 net new jobs in October. -

Does the Glass Ceiling Exist? a Longitudinal Study of Women's

The Journal of Applied Business Research – May/June 2014 Volume 30, Number 3 Does The Glass Ceiling Exist? A Longitudinal Study Of Women’s Progress On French Corporate Boards Rey Dang, La Rochelle Business School, France Duc Khuong Nguyen, IPAG Business School, France Linh-Chi Vo, EM Normandie, France ABSTRACT In this article, we conduct a longitudinal study of women’s progress on French corporate boards of directors. We particularly focus on the extent to which women directors have circumvented the glass ceiling. Using a sample of SBF 120 companies over a 10-year period from 2000 to 2009, our results provide evidence of a significant increase in the number of women on French corporate boards. However, the corporate glass ceiling hypothesis is consistently rejected whatever the considered measure of female directors; i.e., the number of board seats held by women, the number of firms with a critical mass of female directors, and the number of directorships held by each women director. Keywords: Boards of Directors; Gender; Diversity; Corporate Governance 1. INTRODUCTION ver the period 2000-2009, the average participation rate of women in the labor market increased from 60 to 64 percent across the European Union’s 27 Members States. More specifically, in France, it went up from 60.3 to 64.9 percent.1 However, despite this notable progress, women remain under-represented Oin senior or executive positions (ILO, 2009).2 This lack of female representation on corporate boards of directors, which is commonly referred to as glass ceiling in practice and past academic studies, seems to be a global phenomenon because women on corporate boards (WOCB) represents less than 15% of board members in the United States, United Kingdom, Canada, Australia, and many European countries (Dang & Vo, 2012).3 Morrison et al. -

FRC Board Diversity and Effectiveness in FTSE 350

Leadership Institute Board Diversity and Effectiveness in FTSE 350 Companies July 2021 Acknowledgements Report written by: Mary Akimoto, Osman Anwar, Molly Broome, Dragos Diac, Dr Randall S Peterson, Dr Sergei Plekhanov, Simon Osborne and Vyla Rollins We thank the following individuals on the joint LBSLI/SQW research team for their contributions to this research: • Ruth Cluness, LBSLI • Tom Gosling, LBSLI • Brent Hamerla, LBSLI • Letitia Joseph, LBSLI • Barbara Moorer, LBSLI • Andrei Visiteu, LBSLI • Desi Zlatanova, LBSLI We also give a special thank you to our team of research interviewers: • Eva Beazley • Helen Beedham • Christine de Largy • Kathryn Gordon • Dr JoEllyn Prouty McLaren The London Business School Leadership Institute expresses its thanks to all of our stakeholder and collaborators, who supported our research efforts. We would like to express our specific gratitude to the following individuals, for their invaluable guidance, comments, suggestions and support throughout this project: Kit Bingham, Charlie Brown, Gerry Brown, Sue Clark, Louis Cooper, John Dore, Lisa Duke, Roshy Dwyer, Farrer & Co (Anisha Birk, Natalie Rimmer, Peter Wienand), Louise Fowler, Dr Julian Franks, Dr Karl George MBE, Dr Tom Gosling, Dr Byron Grote, Fiona Hathorn, Jonathan Hayward, Susan Hooper, Dr Ioannis Ioannou, Bernhard Kerres, LBS Accounts department (Akposeba Mukoro, Janet Nippard), LBS Advancement department (Luke Ashby, Susie Balch, Nina Bohn, Ian Frith, Sarah Jeffs, Maria Menicou), LBS Executive Education, LBS Research & Faculty Office and -

Examining Drivers of Trading Volume in European Markets

Received: 28 July 2016 Accepted: 19 December 2017 DOI: 10.1002/ijfe.1608 RESEARCH ARTICLE Examining drivers of trading volume in European markets Bogdan Batrinca | Christian W. Hesse | Philip C. Treleaven Department of Computer Science, Abstract University College London, Gower Street, London WC1E 6BT, UK This study presents an in‐depth exploration of market dynamics and analyses potential drivers of trading volume. The study considers established facts from Correspondence Bogdan Batrinca, Department of the literature, such as calendar anomalies, the correlation between volume and Computer Science, University College price change, and this relation's asymmetry, while proposing a variety of time London, Gower Street, London WC1E series models. The results identified some key volume predictors, such as the 6BT, UK. Email: [email protected] lagged time series volume data and historical price indicators (e.g. intraday range, intraday return, and overnight return). Moreover, the study provides empirical evi- Funding information dence for the price–volume relation asymmetry, finding an overall price asymme- Engineering and Physical Sciences Research Council (EPSRC) UK try in over 70% of the analysed stocks, which is observed in the form of a moderate overnight asymmetry and a more salient intraday asymmetry. We conclude that JEL Classification: C32; C52; C58; G12; volatility features, more recent data, and day‐of‐the‐week features, with a notable G15; G17 negative effect on Mondays and Fridays, improve the volume prediction model. KEYWORDS asymmetric models, behavioural finance, European stock market, feature selection, price volume relation, trading volume 1 | INTRODUCTION which was $63tn in 2011 (World Federation of Exchanges, 2012) and $49tn in 2012 (World Federation of Exchanges, This study investigates the drivers affecting the trading 2013). -

Darkest Before Dawn – Shariah Perspective

Malaysia July 29, 2021 Strategy Darkest before dawn – Shariah perspective by Ivy NG Lee Fang, CFA │ T: (60) 3 2261 9073 │ E: [email protected] This report delineates our 2H21F equity strategy outlook from a Shariah perspective. The market was hit by a perfect storm in 1H21 with persistently high Covid-19 cases, multiple lockdowns, ESG concerns and political uncertainty. At the current run rate, we project Malaysia to be on track to inoculate around 70-80% of the population by 4Q21. We expect recovery stocks to see renewed interest in 4Q and the market to re-rate to our KLCI target of 1,604 pts, after an anticipated lacklustre 3Q21. We provide six trading themes for 2H21F in this report; our top Shariah sector picks are Islamic banking, healthcare, media, oil & gas, packaging, semiconductor, EMS, transport and utilities. Our top three Shariah stock picks are Gamuda, Telekom Malaysia and Unisem. IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CGS-CIMB SECURITIES (USA), INC. Powered by the EFA AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH. Platform Malaysia │ Strategy │ July 29, 2021 Content Page Key takeaways of our views on the outlook for 2H21F 3 Shariah-compliant investments 4 1H21 review 6 Outlook 17 Malaysian retail investors’ survey 27 ESG ratings from F4GBM index perspective 28 Key trading thematics 29 Risks 37 Market valuations 42 Economic outlook 44 Technical analysis 49 Top picks and sector ratings 51 2 Malaysia │ Strategy │ July 29, 2021 Key takeaways of our views on the outlook for 2H21F The market was hit by a perfect storm in 1H21 with persistently high Covid-19 cases, multiple lockdowns, ESG concerns and political uncertainty. -

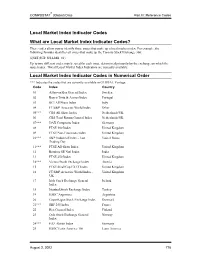

Local Market Index Indicator Codes in Numerical

® COMPUSTAT (Global) Data Part III: Reference Codes Local Market Index Indicator Codes What are Local Market Index Indicator Codes? These codes allow you to identify those issues that make up a local market index. For example, the following formula identifies all issues that make up the Toronto Stock Exchange 300: @SET($GI+$FI,LMII=81) Up to two different codes may be used for each issue, determined primarily by the exchange on which the issue trades. Not all Local Market Index Indicators are currently available. Local Market Index Indicator Codes in Numerical Order *** Indicates the codes that are currently available in GLOBAL Vantage Code Index Country 01 Affarsvarlden General Index Sweden 02 Banco Totta & Acores Index Portugal 03 BCI All Share Index Italy 04 FT/S&P Actuaries World Index Other 05*** CBS All Share Index Netherlands/UK 06 CBS Total Return General Index Netherlands/UK 07*** DAX Composite Index Germany 08 FTSE 100 Index United Kingdom 09 FTSE Non-Financials Index United Kingdom 10*** S&P Industrial Index - Last United States Trading Day 11*** FTSE All-Share Index United Kingdom 12 Bombay SE Natl Index India 13 FTSE 250 Index United Kingdom 14*** Vienna Stock Exchange Index Austria 15 FTSE SmallCap EX IT Index United Kingdom 16 FT/S&P Actuaries World Index - United Kingdom UK 17 Irish Stock Exchange General Ireland Index 18 Istanbul Stock Exchange Index Turkey 19 HSBC Argentina Argentina 20 Copenhagen Stock Exchange Index Denmark 21*** SBF 250 Index France 22 Hex General Index Finland 23 Oslo Stock Exchange General Norway -

FTSE Factsheet

FTSE Russell Factsheet FTSE LATIBEX Index Series Data as at: 29 December 2017 bmkTitle1 FTSE Group and Bolsas y Mercados Españoles (BME) have joined forces to create three indices, FEATURES the FTSE LATIBEX All-Share Index, FTSE LATIBEX TOP Index and the FTSE LATIBEX Brazil Index. These provide investors with real-time access, in one single point, to the performance of Coverage Latin American stocks listed on LATIBEX and denominated in Euros. The indexes measure the performance of Latin American stocks listed on LATIBEX The benchmark FTSE LATIBEX All-Share Index has been designed to represent the performance of the LATIBEX market in real-time. The index comprises all securities that are listed on the Objective market, covering eight countries: Argentina, Brazil, Mexico and Peru. LATIBEX offers international investors a gateway to Latin American equity markets. The FTSE LATIBEX TOP Index is a tradable index for derivatives, designed to represent the LATIBEX is a market segment for Latin performance of the largest and most liquid securities trading on LATIBEX. The index comprises American securities based in Madrid (Spain). the fifteen largest listed securities, who have specialist liquidity providers. The free-float weight Investment products such as warrants and is capped at 10% to ensure that it meets fund regulatory requirements worldwide to avoid over- certificates are already issued on FTSE concentration in any one stock. LATIBEX TOP and listed on the Spanish The FTSE LATIBEX BRAZIL Index is a Euro-denominated tradable index covering Brazilian Exchange, Deutsche Börse, Euronext and stocks, and ranks the most liquid listed on LATIBEX by free float adjusted market cap. -

Emergence of World-Stock-Market Network

Emergence of world-stock-market network M. Saeedian1, T. Jamali2, M. Z. Kamali1, H. Bayani3, T. Yasseri4,5, and G.R. Jafari1,6,7 1Department of Physics, Shahid Beheshti University, G.C., Evin, Tehran 19839, Iran 2School of Physics, Institute for Research in Fundamental Sciences (IPM), P.O. Box 19395-5531, Tehran, Iran 3Faculty of physics, Tehran Science and Research Branch, Islamic Azad University, Tehran, Iran 4Oxford Internet Institute, University of Oxford, 1 St Giles, OX13JS Oxford, UK 5Alan Turing Institute, London, UK 6The Institute for Brain and Cognitive Science (IBCS), Shahid Beheshti University, G.C., Evin, Tehran 19839, Iran 7Center for Network Science, Central European University, H-1051, Budapest, Hungary ABSTRACT In the age of globalization, it is natural that the stock market of each country is not independent form the other markets. In this case, collective behavior could be emerged form their dependency together. This article studies the collective behavior of a set of forty influential markets in the world economy with the aim of exploring a global financial structure that could be called world-stock-market network. Towards this end, we analyze the cross-correlation matrix of the indices of these forty markets using Random Matrix Theory (RMT). We find the degree of collective behavior among the markets and the share of each market in their structural formation. This finding together with the results obtained from the same calculation on four stock markets reinforce the idea of a world financial market. Finally, we draw the dendrogram of the cross-correlation matrix to make communities in this abstract global market visible. -

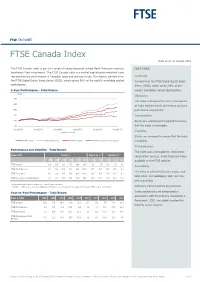

FTSE Factsheet

FTSE FACTSHEET FTSE Canada Index Data as at: 31 August 2015 bmkTitle1 The FTSE Canada Index is part of a range of indices designed to help North American investors FEATURES benchmark their investments. The FTSE Canada index is a market-capitalisation weighted index representing the performance of Canadian large and mid cap stocks. The index is derived from Coverage the FTSE Global Equity Index Series (GEIS), which covers 98% of the world’s investable market Derived from the FTSE Global Equity Index capitalization. Series (GEIS), which covers 98% of the 5-Year Performance - Total Return world’s investable market capitalisation. (CAD) Objective 300 The index is designed for use in the creation 250 of index tracking funds, derivatives and as a 200 performance benchmark. 150 Investability 100 Stocks are selected and weighted to ensure 50 that the index is investable. Aug-2010 Aug-2011 Aug-2012 Aug-2013 Aug-2014 Aug-2015 Liquidity Data as at month end Stocks are screened to ensure that the index FTSE Canada FTSE North America FTSE Developed FTSE Developed ex North America is tradable. Transparency Performance and Volatility - Total Return The index uses a transparent, rules-based Index (CAD) Return % Return pa %* Volatility %** construction process. Index Rules are freely 3M 6M YTD 12M 3YR 5YR 3YR 5YR 1YR 3YR 5YR available on the FTSE website. FTSE Canada -6.5 -7.4 -3.1 -7.1 29.8 33.3 9.1 5.9 13.3 11.9 9.6 Availability FTSE North America -0.2 0.4 10.9 21.0 96.4 149.1 25.2 20.0 14.9 11.6 8.4 The index is calculated based on price and FTSE Developed -1.0 0.3 12.5 17.8 86.2 114.6 23.0 16.5 12.4 11.0 9.1 total return methodologies, both real time FTSE Developed ex North America -2.3 0.1 14.9 13.5 72.8 78.1 20.0 12.2 12.3 12.3 11.4 and end-of-day. -

Financial Market Data for R/Rmetrics

Financial Market Data for R/Rmetrics Diethelm Würtz Andrew Ellis Yohan Chalabi Rmetrics Association & Finance Online R/Rmetrics eBook Series R/Rmetrics eBooks is a series of electronic books and user guides aimed at students and practitioner who use R/Rmetrics to analyze financial markets. A Discussion of Time Series Objects for R in Finance (2009) Diethelm Würtz, Yohan Chalabi, Andrew Ellis R/Rmetrics Meielisalp 2009 Proceedings of the Meielisalp Workshop 2011 Editor Diethelm Würtz Basic R for Finance (2010), Diethelm Würtz, Yohan Chalabi, Longhow Lam, Andrew Ellis Chronological Objects with Rmetrics (2010), Diethelm Würtz, Yohan Chalabi, Andrew Ellis Portfolio Optimization with R/Rmetrics (2010), Diethelm Würtz, William Chen, Yohan Chalabi, Andrew Ellis Financial Market Data for R/Rmetrics (2010) Diethelm W?rtz, Andrew Ellis, Yohan Chalabi Indian Financial Market Data for R/Rmetrics (2010) Diethelm Würtz, Mahendra Mehta, Andrew Ellis, Yohan Chalabi Asian Option Pricing with R/Rmetrics (2010) Diethelm Würtz R/Rmetrics Singapore 2010 Proceedings of the Singapore Workshop 2010 Editors Diethelm Würtz, Mahendra Mehta, David Scott, Juri Hinz R/Rmetrics Meielisalp 2011 Proceedings of the Meielisalp Summer School and Workshop 2011 Editor Diethelm Würtz III tinn-R Editor (2010) José Cláudio Faria, Philippe Grosjean, Enio Galinkin Jelihovschi and Ri- cardo Pietrobon R/Rmetrics Meielisalp 2011 Proceedings of the Meielisalp Summer Scholl and Workshop 2011 Editor Diethelm Würtz R/Rmetrics Meielisalp 2012 Proceedings of the Meielisalp Summer Scholl and Workshop 2012 Editor Diethelm Würtz Topics in Empirical Finance with R and Rmetrics (2013), Patrick Hénaff FINANCIAL MARKET DATA FOR R/RMETRICS DIETHELM WÜRTZ ANDREW ELLIS YOHAN CHALABI RMETRICS ASSOCIATION &FINANCE ONLINE Series Editors: Prof.