Appendix D to Tradition SEF Rulebook Equities Product Listing

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

CS ETF (CH) on SLI Holding AG, Novartis AG and UBS AG

Simplified Prospectus • October 2011 ® the SLI® as at August 15, 2011 were as follows: Nestlé SA, Roche CS ETF (CH) on SLI Holding AG, Novartis AG and UBS AG. The composition of the index is Subfund of the Umbrella Fund of the Category periodically updated by SIX Swiss Exchange. “Other Funds for Traditional Investments” Risk Profile of the Subfund Simplified Prospectus The value of the Subfund’s investments is governed by the market value of investments at any given time. Depending on the prevailing stock October 2011 market trend and the performance of the stocks held in the portfolio, the net asset value can fluctuate considerably. The possibility of a depreciation Distribution in Switzerland and Liechtenstein in value over longer periods cannot be ruled out. There is no guarantee that the investors will receive a certain return and that they will be able to return their units to the fund management company for redemption at a certain price. When redeeming units, it is possible that an investor will not Note recoup the amount originally invested in the Subfund. This simplified prospectus contains a summary of the key information on CS ETF (CH) on SLI®1 (the “Subfund”). The legal and financial aspects Performance of the Subfund (in %) are governed conclusively by the full sales prospectus with integrated fund (change in the net asset value where distributions are reinvested) contract. These govern, among other things, the rights of the investors, the duties and obligations of the fund management company and the 40.0% custodian bank, and the investment policy of the Fund. -

Ishares SMI®

For Professional Clients Only. iShares SMI® ETF (CH) CSSMI August Factsheet Performance, Portfolio Breakdowns and Net Assets information as at: 31-Aug- 2021 All other data as at 07-Sep-2021 Investors should read the Key Investor Information Document and Prospectus prior to investing. Capital at risk. All financial investments involve an element of risk. Therefore, the value The Fund seeks to track the performance of an index composed of the 20 largest Swiss companies. of your investment and the income from it will vary and your initial investment amount cannot Effective from 18 September 2017, the maximum weighting to any one stock is restricted to 18% on be guaranteed. a quarterly basis KEY FACTS Asset Class Equity KEY BENEFITS Fund Base Currency CHF Share Class Currency CHF Targeted exposure to the 20 largest Swiss companies 1 Fund Launch Date 06-Oct-1999 Direct investment into blue-chip companies representative of leaders in Switzerland Share Class Launch Date 06-Oct-1999 2 Benchmark Swiss Market Index (SMI®) 3 Single country and large market capitalisation companies exposure ISIN CH0008899764 Total Expense Ratio 0.35% Distribution Type Ad-Hoc Key Risks: Investment risk is concentrated in specific sectors, countries, currencies or companies. Domicile Switzerland This means the Fund is more sensitive to any localised economic, market, political or regulatory Methodology Replicated events. The value of equities and equity-related securities can be affected by daily stock market Product Structure Physical movements. Other influential factors include political, economic news, company earnings and Rebalance Frequency Quarterly significant corporate events. Counterparty Risk: The insolvency of any institutions providing UCITS No services such as safekeeping of assets or acting as counterparty to derivatives or other Use of Income Distributing instruments, may expose the Fund to financial loss. -

FTSE Factsheet

FTSE Russell Factsheet FTSE LATIBEX Index Series Data as at: 29 December 2017 bmkTitle1 FTSE Group and Bolsas y Mercados Españoles (BME) have joined forces to create three indices, FEATURES the FTSE LATIBEX All-Share Index, FTSE LATIBEX TOP Index and the FTSE LATIBEX Brazil Index. These provide investors with real-time access, in one single point, to the performance of Coverage Latin American stocks listed on LATIBEX and denominated in Euros. The indexes measure the performance of Latin American stocks listed on LATIBEX The benchmark FTSE LATIBEX All-Share Index has been designed to represent the performance of the LATIBEX market in real-time. The index comprises all securities that are listed on the Objective market, covering eight countries: Argentina, Brazil, Mexico and Peru. LATIBEX offers international investors a gateway to Latin American equity markets. The FTSE LATIBEX TOP Index is a tradable index for derivatives, designed to represent the LATIBEX is a market segment for Latin performance of the largest and most liquid securities trading on LATIBEX. The index comprises American securities based in Madrid (Spain). the fifteen largest listed securities, who have specialist liquidity providers. The free-float weight Investment products such as warrants and is capped at 10% to ensure that it meets fund regulatory requirements worldwide to avoid over- certificates are already issued on FTSE concentration in any one stock. LATIBEX TOP and listed on the Spanish The FTSE LATIBEX BRAZIL Index is a Euro-denominated tradable index covering Brazilian Exchange, Deutsche Börse, Euronext and stocks, and ranks the most liquid listed on LATIBEX by free float adjusted market cap. -

FTSE Factsheet

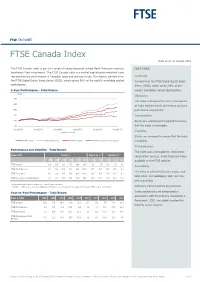

FTSE FACTSHEET FTSE Canada Index Data as at: 31 August 2015 bmkTitle1 The FTSE Canada Index is part of a range of indices designed to help North American investors FEATURES benchmark their investments. The FTSE Canada index is a market-capitalisation weighted index representing the performance of Canadian large and mid cap stocks. The index is derived from Coverage the FTSE Global Equity Index Series (GEIS), which covers 98% of the world’s investable market Derived from the FTSE Global Equity Index capitalization. Series (GEIS), which covers 98% of the 5-Year Performance - Total Return world’s investable market capitalisation. (CAD) Objective 300 The index is designed for use in the creation 250 of index tracking funds, derivatives and as a 200 performance benchmark. 150 Investability 100 Stocks are selected and weighted to ensure 50 that the index is investable. Aug-2010 Aug-2011 Aug-2012 Aug-2013 Aug-2014 Aug-2015 Liquidity Data as at month end Stocks are screened to ensure that the index FTSE Canada FTSE North America FTSE Developed FTSE Developed ex North America is tradable. Transparency Performance and Volatility - Total Return The index uses a transparent, rules-based Index (CAD) Return % Return pa %* Volatility %** construction process. Index Rules are freely 3M 6M YTD 12M 3YR 5YR 3YR 5YR 1YR 3YR 5YR available on the FTSE website. FTSE Canada -6.5 -7.4 -3.1 -7.1 29.8 33.3 9.1 5.9 13.3 11.9 9.6 Availability FTSE North America -0.2 0.4 10.9 21.0 96.4 149.1 25.2 20.0 14.9 11.6 8.4 The index is calculated based on price and FTSE Developed -1.0 0.3 12.5 17.8 86.2 114.6 23.0 16.5 12.4 11.0 9.1 total return methodologies, both real time FTSE Developed ex North America -2.3 0.1 14.9 13.5 72.8 78.1 20.0 12.2 12.3 12.3 11.4 and end-of-day. -

Swiss Leader Index Price Index Index

BLUE-CHIP INDICES 1 SWISS LEADER INDEX PRICE INDEX INDEX Index description Key facts The SLI Swiss Leader Index includes the 30 most liquid stocks traded in the » "In order to achieve the stated index objective SIX Swiss Ex-change defines Swiss equity market, the developments of which are reflected by the SPI® the general principles that govern the index methodology. SIX Swiss Family. Consequently, the index weighting of a given issue is limited by Exchange publishes the index objective and rules for all indices. means of a 9/4,5 capping model. In other words, the weighting of each of the four companies with the largest market capitalisation is capped at a » Representative: the development of the market is represented by the maximum of 9 %. The weightings of all lower-ranked companies are if index necessary capped at 4.5 %. This limitation will be calculated by applying a » Tradable: the index components are tradable in terms of company size capping factor, which as a general rule will remain constant for a three- and market month period. The SLI offers a number of advantages: for investors, the capping feature improves their stock- and sector specific diversification and, » Replicable: the development of the index can be replicated in practise with because the new index fulfils Swiss, EU and US regulatory requirements, a portfolio new markets can be opened with products based on the SLI. That, in turn, generates liquidity for the stocks included in the basket. » Stable: high index continuity » Rules-based: index changes and calculations -

FTSE TWSE Taiwan Technology Index

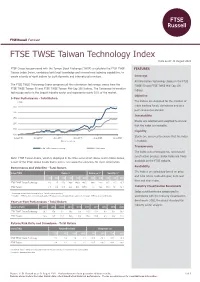

FTSE Russell Factsheet FTSE TWSE Taiwan Technology Index Data as at: 31 August 2021 bmkTitle1 FTSE Group has partnered with the Taiwan Stock Exchange (TWSE) to calculate the FTSE TWSE FEATURES Taiwan Index Series, combining both local knowledge and international indexing capabilities, to create a family of eight indices for both domestic and international investors. Coverage All information technology stocks in the FTSE The FTSE TWSE Technology Index comprises all the information technology stocks from the TWSE 50 and FTSE TWSE Mid Cap 100 FTSE TWSE Taiwan 50 and FTSE TWSE Taiwan Mid-Cap 100 Indices. The Taiwanese information indices. technology sector is the largest industry sector and represents nearly 30% of the market. Objective 5-Year Performance - Total Return (TWD) The indices are designed for the creation of 350 index tracking funds, derivatives and as a performance benchmark. 300 Investability 250 Stocks are selected and weighted to ensure 200 that the index is investable. 150 Liquidity 100 Stocks are screened to ensure that the index Aug-2016 Aug-2017 Aug-2018 Aug-2019 Aug-2020 Aug-2021 Data as at month end is tradable. Transparency FTSE TWSE Taiwan Technology FTSE Taiwan The index uses a transparent, rules-based bmkTitle3 construction process. Index Rules are freely Note: FTSE Taiwan Index, which is displayed in the time-series chart above and in tables below, available on the FTSE website. is part of the FTSE Global Equity Index Series. See www.ftse.com/geis for more information. Availability Performance and Volatility - Total Return The indices are calculated based on price Index (TWD) Return % Return pa %* Volatility %** and total return methodologies, both real 3M 6M YTD 12M 3YR 5YR 3YR 5YR 1YR 3YR 5YR time and end-of-day. -

For Additional Information

April 2015 Attached please find the updated Foreign Listed Stock Index Futures and Options Approvals Chart, current as of April 2015. All prior versions are superseded and should be discarded. Please note the following developments since we last distributed the Approvals Chart: (1) The CFTC has approved the following contracts for trading by U.S. Persons: (i) Singapore Exchange Derivatives Trading Limited’s futures contract based on the MSCI Malaysia Index; (ii) Osaka Exchange’s futures contract based on the JPX-Nikkei Index 400; (iii) ICE Futures Europe’s futures contract based on the MSCI World Index; (iv) Eurex’s futures contracts based on the Euro STOXX 50 Variance Index, MSCI Frontier Index and TA-25 Index; (v) Mexican Derivatives Exchange’s mini futures contract based on the IPC Index; (vi) Australian Securities Exchange’s futures contract based on the S&P/ASX VIX Index; and (vii) Moscow Exchange’s futures contract based on the MICEX Index. (2) The SEC has not approved any new foreign equity index options since we last distributed the Approvals Chart. However, the London Stock Exchange has claimed relief under the LIFFE A&M and Class Relief SEC No-Action Letter (Jul. 1, 2013) to offer Eligible Options to Eligible U.S. Institutions. See note 16. For Additional Information The information on the attached Approvals Chart is subject to change at any time. If you have questions or would like confirmation of the status of a specific contract, please contact: James D. Van De Graaff +1.312.902.5227 [email protected] Kenneth M. -

Thomson One Symbols

THOMSON ONE SYMBOLS QUICK REFERENCE CARD QUOTES FOR LISTED SECURITIES TO GET A QUOTE FOR TYPE EXAMPLE Specific Exchange Hyphen followed by exchange qualifier after the symbol IBM-N (N=NYSE) Warrant ' after the symbol IBM' When Issued 'RA after the symbol IBM'RA Class 'letter representing class IBM'A Preferred .letter representing class IBM.B Currency Rates symbol=-FX GBP=-FX QUOTES FOR ETF TO GET A QUOTE FOR TYPE Net Asset Value .NV after the ticker Indicative Value .IV after the ticker Estimated Cash Amount Per Creation Unit .EU after the ticker Shares Outstanding Value .SO after the ticker Total Cash Amount Per Creation Unit .TC after the ticker To get Net Asset Value for CEF, type XsymbolX. QRG-383 Date of issue: 15 December 2015 © 2015 Thomson Reuters. All rights reserved. Thomson Reuters disclaims any and all liability arising from the use of this document and does not guarantee that any information contained herein is accurate or complete. This document contains information proprietary to Thomson Reuters and may not be reproduced, transmitted, or distributed in whole or part without the express written permission of Thomson Reuters. THOMSON ONE SYMBOLS Quick Reference Card MAJOR INDEXES US INDEXES THE AMERICAS INDEX SYMBOL Dow Jones Industrial Average .DJIA Airline Index XAL Dow Jones Composite .COMP AMEX Computer Tech. Index XCI MSCI ACWI 892400STRD-MS AMEX Institutional Index XII MSCI World 990100STRD-MS AMEX Internet Index IIX MSCI EAFE 990300STRD-MS AMEX Oil Index XOI MSCI Emerging Markets 891800STRD-MS AMEX Pharmaceutical Index -

Download Investment Profile

Vanguard® Vanguard® FTSE Social Index Fund Product Summary Vanguard Style View : Large Growth Seeks to track the performance of the FTSE4Good US Select Index. Index of large- and mid-capitalization U.S. companies screened for certain social criteria. Market cap weighted index composed of large- and Investment style mid-capitalization stocks. Value Blend Growth Screened for certain environmental, social, and corporate Large governance (ESG) criteria. Specifically excludes stocks of certain companies in the following Mid industries: adult entertainment, alcohol, tobacco, weapons, fossil Small fuels, gambling, and nuclear power.* Market capitalization Excludes stocks of certain companies that do not meet standards Central tendency of U.N. global compact principles and companies that do not meet Expected range of fund holdings certain diversity criteria.* Employs a passively managed, full-replication approach. Quarterly Commentary People and Process The human toll of COVID-19 further mounted during the second Vanguard FTSE Social Index Fund seeks to track the performance quarter of 2021 amid fresh outbreaks of the virus and new of the FTSE4Good US Select Index, a market cap weighted index variants. The global economy nevertheless continued to rebound composed of large- and mid-capitalization stocks that is screened sharply if unevenly. Countries that have better succeeded in for certain environmental, social, and corporate governance (ESG) containing the virus—whether through vaccinations, lockdowns, or criteria by the Index sponsor, which is independent of Vanguard. both—tended to fare the best. With the reopening of economies Specifically, the Index excludes stocks of certain companies in the and pent-up demand boosting corporate profits, global stocks following industries: adult entertainment, alcohol, tobacco, finished the quarter significantly higher. -

Xtrackers FTSE All-World Ex UK UCITS ETF Supplement to The

Xtrackers FTSE All-World ex UK UCITS ETF Supplement to the Prospectus This Supplement contains information in relation to Xtrackers FTSE All-World ex UK UCITS ETF (the “Fund”), a sub-fund of Xtrackers (IE) plc (the “Company”) an umbrella type open-ended investment company with segregated liability between sub-funds and with variable capital governed by the laws of Ireland and authorised by the Central Bank of Ireland (the “Central Bank”). This Supplement forms part of, may not be distributed unless accompanied by (other than to prior recipients of the prospectus of the Company dated 26 February 2021 (the “Prospectus”)), and must be read in conjunction with, the Prospectus. An investment in the Fund should not constitute a substantial proportion of an investment portfolio and may not be appropriate for all investors. Xtrackers (IE) plc Dated 26 February 2021 M-19981595-71 ________________________________________________________________________________________ IMPORTANT INFORMATION The Fund is an ETF. The Shares of this Fund are fully transferable to investors and will be listed for trading on one or more stock exchanges. 2 M-19981595-71 ________________________________________________________________________________________ TERMS OF THE SHARES REPRESENTING INTERESTS IN THE FUND ________________________________________________________________________________________ Investment Objective The investment objective of the Fund is to track the performance before fees and expenses of the Underlying Asset, which is the FTSE All-World ex UK Index (the “Reference Index”). The Reference Index is designed to reflect the performance of shares of companies from developed countries and emerging markets worldwide excluding the UK. Further information on the Reference Index is contained under "General Description of the Underlying Asset". Investment Policy In order to seek to achieve the investment objective, the Fund will adopt a Direct Investment Policy. -

Swiss Performance Index Spi Price Index

BENCHMARK INDICES 1 SWISS PERFORMANCE INDEX SPI PRICE INDEX Stated objective Key facts "The SPI Family comprises various indices compiled and published » "In order to achieve the stated index objective SIX Swiss Exchange by the SIX Swiss Exchange. The underlying share universe includes defines the general principles that govern the index methodology. approximately 230 equity issues. For a companys shares to be SIX Swiss Exchange publishes the index objective and rules for all included in the SPI universe, the company must be primary listed in indices. Switzerland and the shares must have a free float equal to or greater than 20 %. In 1998, all investment companies were taken out of the » Representative: the development of the market is represented by SPI Family and put into the specially designed Investment Index." the index » Tradable: the index components are tradable in terms of company size and market » Replicable: the development of the index can be replicated in practise with a portfolio » Stable: high index continuity » Rules-based: index changes and calculations are rule-based » Projectable: changes in rules are with appropriate lead time (usually at least 2 trading days) no retrospective rule changes" Descriptive statistics Index Market cap (CHF bn.) Components (CHF bn.) Component weight (%) Turnover (%) Full Free-float Mean Median Largest Smallest Largest Smallest Last 12 months Swiss Performance Index SPI Price Index 1,374,397. 1,218,423. 5886.1 485.4 239767. 1.6 19.7 0.0 N/A Swiss All Share Index Price Index 1,427,211.1 1,230,610. 5304.4 406.1 239767. 0.3 19.5 0.0 N/A Supersector weighting (top 10) Country weighting Risk and return figures1 Index returns Return (%) Annualized return (%) Last month YTD 1Y 3Y 5Y Last month YTD 1Y 3Y 5Y Swiss Performance Index SPI Price Index 52,65 55614. -

![Evaluation by Outside Stakeholders [PDF:322KB]](https://docslib.b-cdn.net/cover/6360/evaluation-by-outside-stakeholders-pdf-322kb-2246360.webp)

Evaluation by Outside Stakeholders [PDF:322KB]

Businesses Business Corporate 28 Evaluation by Outside Stakeholders Ⅰ and Strategy Segment Data Information The Dow Jones Sustainability Index (DJSI)* recognizes companies that exceed certain Selected for Dow Jones Sustainability standards for sustainability using detailed research to assess their economic, environmental, and social performance. Index for 18th consecutive year * The DJSI is an investment index jointly operated by S&P Dow Jones Indices LLC, a U.S.-based investment research firm, and RobecoSAM AG, a Switzerland-based firm that conducts CSR research and ratings. The FTSE4Good Index* is one of the two leading indexes for investors who are concerned Selected for FTSE4Good Index for about corporate social responsibility. The other major index is the DJSI. the 18th Straight Year * FTSE4Good Index: Launched by the UK-based FTSE Group, which is jointly owned by the Financial Times and the London Stock Exchange. NYK has been included in the MSCI ESG Leaders Indexes, which are internationally Included in the MSCI ESG leading stock indexes for socially responsible investing. Developed by U.S.-based MSCI Leaders Indexes Inc., the MSCI ESG Leaders Indexes recognize companies that are particularly outstanding according to environmental, social, and corporate governance criteria. NYK have been added to the A List by CDP*, an international environmental NPO, putting us in their highest possible tier of rankings for leading global companies in climate change response. Selected for CDP’s A List, the CDP has also selected NYK for their Supplier Engagement Leaderboard. Leaderboard is maximum possible rank, and its the highest rank in their Supplier Engagement Rating, where they select companies Supplier Engagement Leaderboard excelling in actions taken against climate change across the entire supply chain.