Transportation the Inexorable March of Innovation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

20Annual Report UNITED STATES SECURITIES and EXCHANGE COMMISSION Washington, D.C

20 20Annual Report UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 10-K È ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2020. OR ‘ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Transition Period from to . Commission file number 001-37713 eBay Inc. (Exact name of registrant as specified in its charter) Delaware 77-0430924 (State or other jurisdiction of (I.R.S. Employer incorporation or organization) Identification No.) 2025 Hamilton Avenue San Jose, California 95125 (Address of principal executive offices) (Zip Code) Registrant’s telephone number, including area code: (408) 376-7008 Securities registered pursuant to Section 12(b) of the Act: Title of each class Trading symbol Name of exchange on which registered Common stock EBAY The Nasdaq Global Select Market 6.00% Notes due 2056 EBAYL The Nasdaq Global Select Market Securities registered pursuant to Section 12(g) of the Act: None Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes È No ‘ Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ‘ No È Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

E-Commerce in South Korea: a Canadian Perspective

E-COMMERCE IN SOUTH KOREA: A CANADIAN PERSPECTIVE REPORT PREPARED BY: Theresa Eriksson, Luleå University of Technology, Sweden Kristin Matheson, Luleå University of Technology, Sweden Dr. Leyland Pitt, Professor of Marketing, Beedie School of Business, Simon Fraser University Dr. Kirk Plangger, King’s College, London, UK Dr. Karen Robson, University of Windsor 1 2 TABLE OF CONTENTS EXECUTIVE SUMMARY 4 INTRODUCTION 5 SOUTH KOREA: THE COUNTRY, THE ECONOMY 7 METHODOLOGY 8 THE SOUTH-KOREAN E-COMMERCE CONTEXT 9 Customer Context 9 The E-commerce Shopping process 11 Products and Brands 15 Online Behaviour 16 Shopping Events and Timing 20 Main Stakeholders 24 Technology and Infrastructure Landscape 27 For Canadian Firms Contemplating E-commerce in South Korea: 32 Marketing Considerations FUTURE OUTLOOK 40 CONCLUSION 41 CASE STUDIES 42 Case Study I: Yogiyo 42 Case Study II: Pinkfong and Baby Shark 46 APPENDIX 53 Digital Technology in South Korea and Canada — A Comparison of Digital Device Ownership, Digital Media Consumption, and Digital Behaviour. ABOUT THE AUTHORS 68 3 EXECUTIVE SUMMARY This report focuses on e-commerce opportunities for Canadian firms in South Korea, one of the world’s most connected markets. Korea is not for the faint-hearted: consumers are very sophisticated and markets are very competitive. Nevertheless, for Canadian firms with excellent offerings and a willingness to provide excellent service, coupled with patience and an ability to build good relationships at all levels, Korea offers significant opportunities. The report proceeds as follows: First, it provides a broad overview of the nation of South Korea with particular focus on e-commerce and online connectivity in that country. -

Transportation Beginning of Restructuring: Supply Is the Key Variable

2020 Outlook Transportation Beginning of restructuring: Supply is the key variable Jay JH Ryu +822-3774-1738 [email protected] Analysts who prepared this report are registered as research analysts in Korea but not in any other jurisdiction, including the U.S. PLEASE SEE ANALYST CERTIFICATIONS AND IMPORTANT DISCLOSURES & DISCLAIMERS IN APPENDIX 1 AT THE END OF REPORT. Contents [Summary] 3 I. Airlines 4 II. Mobility 17 III. Logistics 32 IV. Shipping 37 [Conclusion] 45 [Top picks] 46 [Summary] Momentum to diverge based on supply management OP vs. P/B: Amid market down cycle, earnings momentum to diverge based on each company’s supply management (Wbn) (x) OP (L) P/B (R) 1,500 2.5 Oil price decline; Air cargo Minimum Global Global High oil prices; greater Oil rebound; wage hike; Slowdown in Inventory housing financial shipping market logistics price LCC growth; economic Chinese stimulus restocking bubble crisis restructuring momentum rebound M&As slowdown 1,000 2.0 500 1.5 0 1.0 -500 0.5 -1,000 0.0 1Q04 1Q05 1Q06 1Q07 1Q08 1Q09 1Q10 1Q11 1Q12 1Q13 1Q14 1Q15 1Q16 1Q17 1Q18 1Q19 Source: Datastream, Mirae Asset Daewoo Research 3| 2020 Outlook [Transportation] Mirae Asset Daewoo Research I. Airlines: Weak demand to prompt restructuring Economic slowdown and • Outbound demand on Japan routes has declined, hurt by a slowing economy and the Korea-Japan diplomatic row. bottoming out of Japan • Japan routes appear to be bottoming out; declines in load factor should stabilize in early 2020, supported by supply cuts. route demand Sharp decline in outbound demand on Japan routes Passenger traffic growth on Japan routes ('000 persons) (%) (%, %p) 3,500 Korean outbound travelers (L) YoY (R) 35 20 YoY passenger growth L/F indicator 30 3,000 10 25 0 2,500 20 Week of -10 Chuseok 2,000 15 -20 1,500 10 5 -30 1,000 0 -40 500 -5 -50 0 -10 14 15 16 17 18 19 Source: Bloomberg, KTO, Mirae Asset Daewoo Research Source: Air Portal, Mirae Asset Daewoo Research 4| 2020 Outlook [Transportation] Mirae Asset Daewoo Research I. -

Quarterly Portfolio Holdings

T. Rowe Price Extended Equity Market Index Fund PEXMX 06/30/2021 (Unaudited) Portfolio of Investments Investments in Securities Coupon % Maturity Shares/Par Value ($) % of Net Assets 10X Genomics 13,000 2,545,660 0.183% 1-800-Flowers.com 7,768 247,566 0.018% 1Life Healthcare 14,500 479,370 0.034% 1st Source 8,652 401,972 0.029% 22nd Century 46,800 216,684 0.016% 2U 13,500 562,545 0.040% 3D Systems 26,350 1,053,210 0.076% 8x8 19,600 544,096 0.039% AAON 6,690 418,727 0.030% Aaron s 7,567 242,068 0.017% Abercrombie & Fitch 14,500 673,235 0.048% ABM Industries 11,150 494,503 0.035% Abraxas Petroleum 15,382 49,684 0.004% Acadia Healthcare 16,900 1,060,475 0.076% ACADIA Pharmaceuticals 25,800 629,262 0.045% Acadia Realty Trust, REIT 16,650 365,634 0.026% Acceleron Pharma 9,500 1,192,155 0.086% Acco Brands 21,900 188,997 0.014% AcelRx Pharmaceuticals 95,700 132,066 0.009% ACI Worldwide 20,300 753,942 0.054% Aclaris Therapeutics 25,400 446,024 0.032% ACM Research 2,800 286,216 0.021% ACRES Commercial Realty, REIT 15,332 246,232 0.018% Acuity Brands 6,300 1,178,289 0.085% Acushnet Holdings 7,475 369,265 0.026% Adamas Pharmaceuticals 33,700 177,936 0.013% Adams Resources & Energy 3,341 92,512 0.007% AdaptHealth 12,200 334,402 0.024% Adaptive Biotechnologies 15,500 633,330 0.045% Addus HomeCare 2,300 200,652 0.014% Adient 18,000 813,600 0.058% ADT 29,300 316,147 0.023% Adtalem Global Education 12,200 434,808 0.031% Advanced Drainage Systems 8,791 1,024,767 0.074% Advanced Energy Industries 5,750 648,083 0.047% Adverum Biotechnologies 46,900 164,150 -

The Rise of Start-Ups Source List

The Rise Of Start-Ups Source List Top 25 Start-Ups https://www.investopedia.com/investing/10-biggest-start-ups-valuation-recode/ https://www.cbinsights.com/research-unicorn-companies Toutiao (Bytedance) https://en.wikipedia.org/wiki/ByteDance https://pandaily.com/bytedance-rumored-to-hit-20-billion-revenue-goal-for-2019/ JUUL Labs https://news.crunchbase.com/news/juul-lands-12-8b-from-big-tobacco-as-vaping-grows-up-sells-out/ Nubank https://en.wikipedia.org/wiki/Nubank https://techcrunch.com/2014/09/25/finance-startup-nubank-nabs-14-3m-in-sequoias-first-brazil-investment/ Stripe https://en.wikipedia.org/wiki/Stripe_(company) Airbnb https://en.wikipedia.org/wiki/Airbnb https://www.businessinsider.com.au/estimating-airbnbs-revenues-2012-3 https://www.businessinsider.com/how-airbnb-was-founded-a-visual-history-2016-2 https://www.reuters.com/article/us-airbnb-results/airbnb-had-substantially-more-than-1-billion-in-quarterly-revenue-idUSKCN1NL270 Kuaishou https://www.reuters.com/article/us-kuaishou-fundraising/chinas-kuaishou-in-1-billion-tencent-led-funding-round-eyes-ipo-sources-idUSKBN1FE11D Oyo Rooms https://www.businesstoday.in/top-story/oyo-hotel-sales-globally-jump-over-4-fold-to-usd-18-bn-in-2018/story/318233.html https://www.financialexpress.com/industry/even-as-revenue-soared-14x-to-rs-32-8-cr-oyo-rooms-posts-24x-jump-in-losses-in-fy16/785161/ Coupang https://techcrunch.com/2018/11/20/coupang-raises-2-billion-from-softbanks-vision-fund/ https://venturebeat.com/2012/05/30/koreas-21-month-old-e-commerce-startup-coupang-will-generate-600m-in-revenue-this-year/ -

International Ecommerce

A special report from the editors of International Ecommerce The challenges and opportunities in global e-retail PRESENTED BY: The growth opportunity of international ecommerce International shipping is complex. It can be costly to send products to customers in other countries, and it may also require retailers to clear hurdles they don’t normally face with domestic shipments. Because of these complexities, many retailers--especially small and midsized businesses--don’t bother to ship abroad, which limits their opportunities for growth. Some leading North American brands and retailers have seen those opportunities and expanded their international and cross-border operations in the past year. And many see global expansion as an important source of growth, according to a recent survey of 111 retailers and brands by Internet Retailer and the Global E-Commerce Leaders Forum, an organization dedicated to helping retailers and brands sell internationally via ecommerce. Nearly 48% of survey respondents reported 2017 growth in overseas web sales of at least 15% and 80% of respondents called international ecommerce “a critical source of our ecommerce growth in the future.” This e-book, brought to you by GlobalPost, presents articles and data previously published by Internet Retailer and helps to define these issues and uncover the opportunities. Reaching global online shoppers . .. 3 How retailers can overcome international shipping challenges and open up new markets . .. 8 The top hurdles to international ecommerce . 10 Building a marketing strategy for global ecommerce . 11 Case Study: Victoria’s Secret enters China ecommerce with a flourish . 19 Emerging legal trends in international ecommerce . 21 Copyright 2018-2019 Internet Retailer and DigitalCommerce360.com. -

Retail(Neutral/Maintain)

[Korea] January 25, 2021 Retail (Neutral/Maintain) Coupang: Putting doubts to rest Mirae Asset Daewoo Co., Ltd. Myoungjoo Kim [email protected] Minjeong Kyeong [email protected] Coupang IPO coming into view IPO looking increasingly likely Coupang has reportedly passed preliminary screening for listing on the US Nasdaq market. Media reports have suggested the company could be worth around US$25-40bn, which implies a P/S of 1.7-2.8x based on our 2021 estimates. Amazon traded at 3.95x P/S in 2003, the year it first turned a profit (2002-04 average of 2.8x). In 2021, Coupang should benefit from a steady increase in commission income along with falling parcel delivery rates (due to volume growth), potentially leading to meaningful improvement in profitability. Potential valuation levels should also be viewed in the context of the company’s expanding retail market share. E-commerce market Coupang driving e -commerce market re alignment realignment has begun Coupang has regained its parcel delivery business license. In 2021, we expect the company to expand its fulfillment services in order to: 1) strengthen the competitiveness of its platform categories; and 2) raise commission income. The company should gain share in the e-commerce market, backed by: 1) enhanced competitiveness in directly sourced merchandise (especially in fashion); and 2) GMV growth of its marketplace resulting from the expansion of fulfillment services. Coupang looks likely to expand its e-commerce market share to 15.7% (+2.4%p) in 2021 and 19.3% (+3.6%p) in 2022. Retail market share to expand Market leadership to expand beyond e -commerce to broader retail sector Furthermore, Coupang appears likely to expand its share of the broader retail market to 5.8% (+1.4%p) in 2021 and 7.8% (+2.0%p) in 2022. -

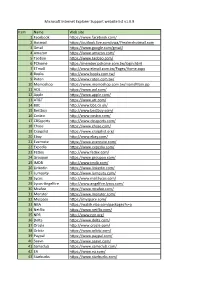

Item Name Web Site 1 Facebook

Microsoft Internet Explorer Support website list v1.0.9 Item Name Web site 1 Facebook https://www.facebook.com/ 2 Hotmail https://outlook.live.com/owa/?realm=hotmail.com 3 Gmail https://www.google.com/gmail/ 4 Amazon https://www.amazon.com/ 5 Taobao https://www.taobao.com/ 6 PChome https://member.pchome.com.tw/login.html 7 ETmall http://www.etmall.com.tw/Pages/Home.aspx 8 Books http://www.books.com.tw/ 9 Ruten http://www.ruten.com.tw/ 10 Momoshop https://www.momoshop.com.tw/main/Main.jsp 11 AOL https://www.aol.com/ 12 Apple https://www.apple.com/ 13 AT&T https://www.att.com/ 14 BBC http://www.bbc.co.uk/ 15 Bestbuy http://www.bestbuy.com/ 16 Costco http://www.costco.com/ 17 CBSsports http://www.cbssports.com/ 18 Chase https://www.chase.com/ 19 Craigslist https://www.craigslist.org/ 20 Ebay http://www.ebay.com/ 21 Evernote https://www.evernote.com/ 22 Expedia https://www.expedia.com/ 23 FEDex http://www.fedex.com/ 24 Groupon https://www.groupon.com/ 25 IMDB http://www.imdb.com/ 26 Linkedin https://www.linkedin.com/ 27 Lumosity https://www.lumosity.com/ 28 Lycos http://www.mail.lycos.com/ 29 Lycos-Angelfire http://www.angelfire.lycos.com/ 30 Mcafee https://www.mcafee.com/ 31 Monster https://www.monster.com/ 32 Myspace https://myspace.com/ 33 NBA https://watch.nba.com/packages?s=o 34 Netflix https://www.netflix.com/ 35 NPR http://www.npr.org/ 36 Delta https://www.delta.com/ 37 Oracle http://www.oracle.com/ 38 Orbitz https://www.orbitz.com/ 39 Paypal https://www.paypal.com/ 40 Saavn https://www.saavn.com/ 41 Samsclub https://www.samsclub.com/ -

Domestic Ride-Hailing Services: Potential W10tr Valuation?

Kakao (035720 KS ) Domestic ride -hailing services: Potential W10tr valuation? Internet High valuations of Uber/Lyft Company Update US ride-hailing companies Uber and Lyft have filed for IPOs with the Securities and January 8, 2019 Exchange Commission (SEC) in December 2018. Of note, Uber provides a wide range of services, including ride-hailing (with options like Standard, Luxury, and SUV), shared rides, food delivery (Uber Eats), a shipping platform (Uber Freight), ride-hailing exclusively for healthcare organizations (Uber Health), and a staffing platform (Uber Works). (Maintain) Buy In 2018, Uber recorded an estimated US$46.8bn in total gross bookings and US$10.8bn in net revenue. However, the company is still incurring huge losses, with a net loss of Target Price (12M, W) 130,000 US$1.07bn in 3Q18. Meanwhile, Lyft controls 29% of the North American market as of October 2018, up from 22% in October 2017. US media reports suggest Uber and Lyft Share Price (01/07/19, W) 103,000 could be valued at US$120bn (W135tr) and US$15.1bn (W17tr), respectively, in their IPOs. Success will depend on traffic and revenue growth Expected Return 26% We believe the success of Uber’s and Lyft’s IPOs will be tied to the pace of growth of their user traffic and revenue around the time of their listings. In addition, we think OP (18F, Wbn) 102 these two companies’ stock market performances will be reflected in the Korean stock Consensus OP (18F, Wbn) 102 market by their effect on growth expectations on the domestic ride-sharing market. -

Exploring Potential Cooperation Opportunity Between Ride-Hailing Operator and Automotive Battery Supplier

Iowa State University Capstones, Theses and Creative Components Dissertations Fall 2019 Exploring Potential Cooperation Opportunity between Ride-Hailing Operator and Automotive Battery Supplier Jingwen Zhang Follow this and additional works at: https://lib.dr.iastate.edu/creativecomponents Part of the Business Intelligence Commons Recommended Citation Zhang, Jingwen, "Exploring Potential Cooperation Opportunity between Ride-Hailing Operator and Automotive Battery Supplier" (2019). Creative Components. 442. https://lib.dr.iastate.edu/creativecomponents/442 This Creative Component is brought to you for free and open access by the Iowa State University Capstones, Theses and Dissertations at Iowa State University Digital Repository. It has been accepted for inclusion in Creative Components by an authorized administrator of Iowa State University Digital Repository. For more information, please contact [email protected]. Exploring Potential Cooperation Opportunity between Ride-Hailing Operator and Automotive Battery Supplier Creative Component presented to the faculty of Management Information Systems in partial fulfillment of the requirements for the degree of Master of Science by Jingwen Zhang Iowa State University Ames, Iowa 2019 Abstract With the growing popularity of ride-hailing services like Uber in recent years, many industries are looking for opportunities to cooperate with ride-hailing companies. Similarly, ride-hailing platforms are also looking for potential opportunities to cooperate with other service providers or product industries to bring more comprehensive, convenient, and personalized services to their customers. This research is dedicated to studying potential cooperation opportunities between ride- hailing platforms and automotive battery suppliers. There are extensive studies and research focuses on the topic of ride-hailing companies' future growth and direction as well as some studies on the impact of the ride-hailing market. -

ANNUAL REPORT PURSUANT to SECTION 13 OR 15(D) of the SECURITIES EXCHANGE ACT of 1934 for the Fiscal Year Ended December 31, 2019

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 10-K ☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2019. OR ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Transition Period from to . Commission file number 001-37713 eBay Inc. (Exact name of registrant as specified in its charter) Delaware 77-0430924 (State or other jurisdiction of (I.R.S. Employer incorporation or organization) Identification No.) 2025 Hamilton Avenue San Jose , California 95125 (Address of principal executive offices) (Zip Code) Registrant’s telephone number, including area code: (408) 376-7008 Securities registered pursuant to Section 12(b) of the Act: Title of each class Trading symbol Name of exchange on which registered Common stock EBAY The Nasdaq Global Select Market 6.00% Notes due 2056 EBAYL The Nasdaq Global Select Market Securities registered pursuant to Section 12(g) of the Act: None Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐ Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒ Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

Baron Global Advantage Strategy

Baron Global Advantage Strategy March 31, 2021 Dear Investor: • Financials – the sector was up 11.4%, and we were 12.4% Performance underweight. • Industrials – the sector was up 7.5%, and we were 9.0% underweight. Baron Global Advantage Strategy declined 1.8% during the first quarter. The MSCI ACWI Index and the MSCI ACWI Growth Index, the Strategy’s Looking on a level deeper, within Consumer Discretionary our results were benchmarks, gained 4.6% and 0.3%, respectively, for the quarter. After a impacted by not being in the right sub-industries as we had no exposure to few years of very strong performance, including last year’s best absolute double-digit gainers such as hotels, casinos, and homebuilders, and instead and relative returns in the nine-year history of the Strategy, it was time for were significantly overweight e-commerce (internet & direct marketing many of our investments to take a breather. retail) and education services, sub-industries that were down 2.8% and 24.4%, respectively, during the quarter. Similarly, in IT, we had almost no Table I. exposure to the more cyclical sub-industries, such as communications Performance† equipment and semiconductors, which performed very well, and were Annualized for periods ended March 31, 2021 significantly overweight software and internet services & infrastructure which were either flat or down in the quarter. Baron Baron Global Global MSCI Advantage Advantage MSCI ACWI Ironically, the picture is similar from a geographical perspective, where we Strategy Strategy ACWI Growth seemed to have been in mostly the wrong places. Per usual, we were (net)1 (gross)1 Index1 Index1 overweight emerging markets, which underperformed and were responsible Three Months2 (1.80)% (1.60)% 4.57% 0.28% for about half of our underperformance.