COVID-19: Household Debt During the Pandemic

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Income Distribution, Household Debt, and Aggregate Demand: a Critical Assessment

Working Paper No. 901 Income Distribution, Household Debt, and Aggregate Demand: A Critical Assessment J. W. Mason* Department of Economics, John Jay College-CUNY and The Roosevelt Institute March 2018 * I thank David Alpert, Heather Boushey, Barry Cynamon, Sandy Darity, Steve Fazzari, Arjun Jayadev, Matthew Klein, and Suresh Naidu for helpful comments on earlier versions of this paper. The Levy Economics Institute Working Paper Collection presents research in progress by Levy Institute scholars and conference participants. The purpose of the series is to disseminate ideas to and elicit comments from academics and professionals. Levy Economics Institute of Bard College, founded in 1986, is a nonprofit, nonpartisan, independently funded research organization devoted to public service. Through scholarship and economic research it generates viable, effective public policy responses to important economic problems that profoundly affect the quality of life in the United States and abroad. Levy Economics Institute P.O. Box 5000 Annandale-on-Hudson, NY 12504-5000 http://www.levyinstitute.org Copyright © Levy Economics Institute 2018 All rights reserved ISSN 1547-366X ABSTRACT During the period leading up to the recession of 2007–08, there was a large increase in household debt relative to income, a large increase in measured consumption as a fraction of GDP, and a shift toward more unequal income distribution. It is sometimes claimed that these three developments were closely linked. In these stories, the rise in household debt is largely due to increased borrowing by lower-income households who sought to maintain rising consumption in the face of stagnant incomes; this increased consumption in turn played an important role in maintaining aggregate demand. -

Corporate Bonds and Debentures

Corporate Bonds and Debentures FCS Vinita Nair Vinod Kothari Company Kolkata: New Delhi: Mumbai: 1006-1009, Krishna A-467, First Floor, 403-406, Shreyas Chambers 224 AJC Bose Road Defence Colony, 175, D N Road, Fort Kolkata – 700 017 New Delhi-110024 Mumbai Phone: 033 2281 3742/7715 Phone: 011 41315340 Phone: 022 2261 4021/ 6237 0959 Email: [email protected] Email: [email protected] Email: [email protected] Website: www.vinodkothari.com 1 Copyright & Disclaimer . This presentation is only for academic purposes; this is not intended to be a professional advice or opinion. Anyone relying on this does so at one’s own discretion. Please do consult your professional consultant for any matter covered by this presentation. The contents of the presentation are intended solely for the use of the client to whom the same is marked by us. No circulation, publication, or unauthorised use of the presentation in any form is allowed, except with our prior written permission. No part of this presentation is intended to be solicitation of professional assignment. 2 About Us Vinod Kothari and Company, company secretaries, is a firm with over 30 years of vintage Based out of Kolkata, New Delhi & Mumbai We are a team of qualified company secretaries, chartered accountants, lawyers and managers. Our Organization’s Credo: Focus on capabilities; opportunities follow 3 Law & Practice relating to Corporate Bonds & Debentures 4 The book can be ordered by clicking here Outline . Introduction to Debentures . State of Indian Bond Market . Comparison of debentures with other forms of borrowings/securities . Types of Debentures . Modes of Issuance & Regulatory Framework . -

Interest-Rate-Growth Differentials and Government Debt Dynamics

From: OECD Journal: Economic Studies Access the journal at: http://dx.doi.org/10.1787/19952856 Interest-rate-growth differentials and government debt dynamics David Turner, Francesca Spinelli Please cite this article as: Turner, David and Francesca Spinelli (2012), “Interest-rate-growth differentials and government debt dynamics”, OECD Journal: Economic Studies, Vol. 2012/1. http://dx.doi.org/10.1787/eco_studies-2012-5k912k0zkhf8 This document and any map included herein are without prejudice to the status of or sovereignty over any territory, to the delimitation of international frontiers and boundaries and to the name of any territory, city or area. OECD Journal: Economic Studies Volume 2012 © OECD 2013 Interest-rate-growth differentials and government debt dynamics by David Turner and Francesca Spinelli* The differential between the interest rate paid to service government debt and the growth rate of the economy is a key concept in assessing fiscal sustainability. Among OECD economies, this differential was unusually low for much of the last decade compared with the 1980s and the first half of the 1990s. This article investigates the reasons behind this profile using panel estimation on selected OECD economies as means of providing some guidance as to its future development. The results suggest that the fall is partly explained by lower inflation volatility associated with the adoption of monetary policy regimes credibly targeting low inflation, which might be expected to continue. However, the low differential is also partly explained by factors which are likely to be reversed in the future, including very low policy rates, the “global savings glut” and the effect which the European Monetary Union had in reducing long-term interest differentials in the pre-crisis period. -

Sample Debt Validation Letter (Send Via Certified Mail, Return Receipt Requested)

Sample Debt Validation Letter (Send via certified mail, return receipt requested) Date: Your Name Your Address Your City, State, Zip Collection Agency Name Collection Agency Address Collection Agency City, State, Zip RE: Account # (Fill in Account Number) To Whom It May Concern: Be advised this is not a refusal to pay, but a notice that your claim is disputed and validation is requested. Under the Fair Debt collection Practices Act (FDCPA), I have the right to request validation of the debt you say I owe you. I am requesting proof that I am indeed the party you are asking to pay this debt, and there is some contractual obligation that is binding on me to pay this debt. This is NOT a request for “verification” or proof of my mailing address, but a request for VALIDATION made pursuant to 15 USC 1692g Sec. 809 (b) of the FDCPA. I respectfully request that your offices provide me with competent evidence that I have any legal obligation to pay you. At this time I will also inform you that if your offices have or continue to report invalidated information to any of the three major credit bureaus (Equifax, Experian, Trans Union), this action might constitute fraud under both federal and state laws. Due to this fact, if any negative mark is found or continues to report on any of my credit reports by your company or the company you represent, I will not hesitate in bringing legal action against you and your client for the following: Violation of the Fair Debt Collection Practices Act and Defamation of Character. -

Box A: Household Sector Risks in China

Box A Household Sector Risks in China The growth and level of corporate debt in decline in interest rates in China over the China has received significant attention, but 2010s have also raised households’ ability to household debt has also grown rapidly, albeit service debt. The increase in debt has also from a much lower base. The rise in been accompanied by a sharp rise in housing household debt over the past decade is prices. notable because it can negatively affect both Mortgage debt has been the biggest driver [1] financial stability and economic growth. of the increase in household debt over the This Box assesses the direct risk that past decade, and now accounts for around household debt poses to the financial system half of household debt in China (Graph A.2). in China. Credit card debt has also risen strongly. Household debt in China has grown at an Growth in personal business loans has been average annual rate of more than 20 per cent less pronounced, but these loans still account over the past decade. As a result, the ratio of for around 20 per cent of household debt. household debt to GDP has increased Growth in some riskier types of household sharply, from about 20 per cent in 2009 to debt not measured in official household debt around 55 per cent currently (Graph A.1). This statistics, such as peer-to-peer (P2P) and ratio is lower than in most advanced other online lending, has been particularly economies, but is higher than in many other strong in the past few years, although it has large emerging market economies. -

Does Greater Inequality Lead to More Household Borrowing? New Evidence from Household Data

FEDERAL RESERVE BANK OF SAN FRANCISCO WORKING PAPER SERIES Does Greater Inequality Lead to More Household Borrowing? New Evidence from Household Data Olivier Coibion UT Austin and NBER Yuriy Gorodnichenko UC Berkeley and NBER Marianna Kudlyak Federal Reserve Bank of San Francisco John Mondragon Northwestern University August 2016 Working Paper 2016-20 http://www.frbsf.org/economic-research/publications/working-papers/wp2016-20.pdf Suggested citation: Coibion, Olivier, Yuriy Gorodnichenko, Marianna Kudlyak, John Mondragon. 2016. “Does Greater Inequality Lead to More Household Borrowing? New Evidence from Household Data” Federal Reserve Bank of San Francisco Working Paper 2016-20. http://www.frbsf.org/economic-research/publications/working-papers/wp2016-20.pdf The views in this paper are solely the responsibility of the authors and should not be interpreted as reflecting the views of the Federal Reserve Bank of San Francisco or the Board of Governors of the Federal Reserve System. Does Greater Inequality Lead to More Household Borrowing? New Evidence from Household Data Olivier Coibion Yuriy Gorodnichenko UT Austin and NBER UC Berkeley and NBER [email protected] [email protected] Marianna Kudlyak John Mondragon Federal Reserve Bank of San Francisco Northwestern University [email protected] [email protected] First Draft: December, 2013 This Draft: August, 2016 Abstract: Using household-level debt data over 2000-2012 and local variation in inequality, we show that low-income households in high-inequality regions (zip-codes, counties, states) accumulated less debt (relative to their income) than low-income households in lower-inequality regions, contrary to the prevailing view. -

Nber Working Papers Series

NBER WORKING PAPERS SERIES WAS THERE A BUBBLE IN THE 1929 STOCK MARKET? Peter Rappoport Eugene N. White Working Paper No. 3612 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge, MA 02138 February 1991 We have benefitted from comments made on earlier drafts of this paper by seminar participants at the NEER Summer Institute and Rutgers University. We are particularly indebted to Charles Calomiris, Barry Eicherigreen, Gikas Hardouvelis and Frederic Mishkiri for their suggestions. This paper is part of NBER's research program in Financial Markets and Monetary Economics. Any opinions expressed are those of the authors and not those of the National Bureau of Economic Research. NBER Working Paper #3612 February 1991 WAS THERE A BUBBLE IN THE 1929 STOCK MARKET? ABSTRACT Standard tests find that no bubbles are present in the stock price data for the last one hundred years. In contrast., historical accounts, focusing on briefer periods, point to the stock market of 1928-1929 as a classic example of a bubble. While previous studies have restricted their attention to the joint behavior of stock prices and dividends over the course of a century, this paper uses the behavior of the premia demanded on loans collateralized by the purchase of stocks to evaluate the claim that the boom and crash of 1929 represented a bubble. We develop a model that permits us to extract an estimate of the path of the bubble and its probability of bursting in any period and demonstrate that the premium behaves as would be expected in the presence of a bubble in stock prices. -

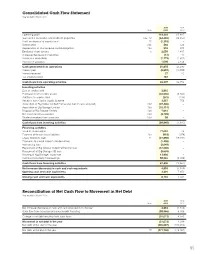

Reconciliation of Net Cash Flow to Movement in Net Debt Year Ended 31 March 2015

Consolidated Cash Flow Statement Year ended 31 March 2015 2015 2014 Note £000 £000 Operating profit 114,203 67,887 Gain on the revaluation of investment properties 13a, 14 (64,465) (28,350) Profit on disposal of surplus land 15 (1,318) – Depreciation 13b 566 526 Depreciation of finance lease capital obligations 13a 918 974 Employee share options 6 2,059 1,437 (Increase)/decrease in inventories (14) 10 Increase in receivables (1,172) (1,652) Increase in payables 1,098 2,458 Cash generated from operations 51,875 43,290 Interest paid (9,692) (10,558) Interest received 27 20 Tax credit received 187 – Cash flows from operating activities 42,397 32,752 Investing activities Sale of surplus land 2,815 – Purchase of non-current assets (42,555) (8,460) Additions to surplus land (231) (136) Receipts from Capital Goods Scheme 3,557 756 Acquisition of Big Yellow Limited Partnership (net of cash acquired) 13d (37,406) – Acquisition of Big Storage Limited 13a (15,114) – Disposal of Big Storage Limited 13a 7,614 – Net investment in associates 13d (3,709) – Dividend received from associate 13d 89 – Cash flows from investing activities (84,940) (7,840) Financing activities Issue of share capital 77,094 42 Payment of finance lease liabilities 13a (918) (974) Equity dividends paid 11 (27,890) (19,591) Payments to cancel interest rate derivatives (1,408) – Refinancing fees (2,649) – Repayment of Big Yellow Limited Partnership loan (57,000) – Repayment of Big Storage AIB loan (9,659) – Drawing of Big Storage Lloyds loan 13,900 – Increase/(reduction) in borrowings -

Information Paper on Quarterly

information paper on economic statistics QUARTERLY HOUSEHOLD SECTOR BALANCE SHEET Singapore Department of Statistics October 2012 Papers in this Information Paper Series are intended to inform and clarify conceptual and methodological changes and improvements in official statistics. The views expressed are based on the latest methodological developments in the international statistical community. Statistical estimates presented in the papers are based on new or revised official statistics compiled from the best available data. Comments and suggestions are welcome. © Singapore Department of Statistics. All rights reserved. Please direct enquiries on this information paper to: Institutional Sector Accounts Singapore Department of Statistics Tel : 6332 7096 Email : [email protected] Application for the copyright owner’s written permission to reproduce any part of this publication should be addressed to the Chief Statistician and emailed to the above address. QUARTERLY HOUSEHOLD SECTOR BALANCE SHEET I. Introduction 1. Since 2003, the Singapore Department of Statistics (DOS) has compiled the household balance sheet on an annual basis from reference year 2000. DOS has successfully developed and compiled the quarterly household sector balance sheet from reference quarter Q1 1995 (Annex A). DOS has not only improved the frequency and timeliness on the release of the household sector balance sheet, but has also incorporated methodological, conceptual and data refinements underlying the development of the quarterly series. 2. This paper is structured as follows: Section II provides the concepts and definitions. Section III highlights improvements in concepts, methodologies and data sources. Section IV analyses and identifies key trends underlying the quarterly household sector balance sheet. Section V compares the health of household sector balance sheets among selected countries. -

February 9, 2020 Falling Real Interest Rates, Rising Debt: a Free Lunch?

February 9, 2020 Falling Real Interest Rates, Rising Debt: A Free Lunch? By Kenneth Rogoff, Harvard University1 1 An earlier version of this paper was presented at the American Economic Association January 3 2020 meeting in San Diego in a session entitled “The United States Economy: Growth, Stagnation or New Financial Crisis?” chaired by Dominick Salvatore. The author is grateful to Molly and Dominic Ferrante Fund at Harvard University for research support. 1 With real interest rates hovering near multi-decade lows, and even below today’s slow growth rates, has higher government debt become a proverbial free lunch in many advanced countries?2 It is certainly true that low borrowing rates help justify greater government spending on high social return investment and education projects, and should make governments more relaxed about countercyclical fiscal policy, the “free lunch” perspective is an illusion that ignores most governments’ massive off-balance-sheet obligations, as well the possibility that borrowing rates could rise in a future economic crisis, even if they fell in the last one. As Lawrence Kotlikoff (2019) has long emphasized (see also Auerbach, Gokhale and Kotlikoff, 1992) 3 standard measures of government in debt have in some sense become an accounting fiction in the modern post World War II welfare state. Every advanced economy government today spends more on publicly provided old age support and pensions alone than on interest payment, and would still be doing so even if real interest rates on government debt were two percent higher. And that does not take account of other social insurance programs, most notably old-age medical care. -

Will US Consumer Debt Reduction Cripple the Recovery?

McKinsey Global Institute March 2009 Will US consumer debt reduction cripple the recovery? McKinsey Global Institute The McKinsey Global Institute (MGI), founded in 1990, is McKinsey & Company’s economics research arm. MGI’s mission is to help business and government leaders develop a deeper understanding of the evolution of the global economy and provide a fact base that contributes to decision making on critical management and policy issues. MGI’s research is a unique combination of two disciplines: economics and management. By integrating these two perspectives, MGI is able to gain insights into the microeconomic underpinnings of the broad trends shaping the global economy. MGI has utilized this “micro-to-macro” approach in research covering more than 15 countries and 28 industry sectors, on topics that include productivity, global economic integration, offshoring, capital markets, health care, energy, demographics, and consumer demand. Our research is conducted by a group of full-time MGI fellows based in of fices in San Francisco, Washington, DC, London, and Shanghai. MGI project teams also include consultants drawn from McKinsey’s offices around the world and are supported by McKinsey’s network of industry and management experts and worldwide partners. In addition, MGI teams work with leading economists, including Nobel laureates and policy experts, who act as advisers to MGI projects. MGI’s research is funded by the par tners of McKinsey & Company and not commissioned by any business, government, or other institution. Further information about MGI and copies of MGI’s published reports can be found at www.mckinsey.com/mgi. Copyright © McKinsey & Company 2009 McKinsey Global Institute March 2009 Will US consumer debt reduction cripple the recovery? Martin N. -

Debt Collection Guide Update

Debt Collection Guide Update This Update includes new information you should know when dealing with debt collectors. 1. In New York, a debt collector cannot collect or attempt to collect on a payday loan. Payday loans are illegal in New York. A payday loan is a high-interest loan borrowed against your next paycheck. To apply for a payday loan, you need to have a checking account and proof of income. In New York State, most payday loans are handled by phone or online. If a collection agency tries to collect on a payday loan, visit nyc.gov/dca or contact 311 to file a complaint with DCA. 2. Beware of debt collection companies or companies working with debt collection companies that offer you a credit card if you repay, in part or in full, an old debt that may have expired. Companies may use terms like “Fresh Start Program” or “Balance Transfer Program” to describe offers to transfer your old debt to a new credit card account after you make a certain number of payments. If you accept the credit card offer and start making pay- ments, the debt collection agency’s time limit (statute of limitations) for suing you to collect this debt will restart. The company offering the credit card may not tell you that this is a consequence of getting the credit card. See the section What Should You Do When a Debt Collection Agency Contacts You? for information about statute of limitations. 3. It is illegal for a debt collection agency to use “caller ID spoofing.” Some debt collection agencies are using spoofed (or faked) phone numbers to disguise their identities on caller ID.