Analyzing Mumbai's Housing Markets Post Rera

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Chief Minister to Inaugurate Eastern Freeway on June 13Th!

Chief Minister to inaugurate Eastern Freeway on June 13 th 13.59-km long Freeway reduces travel time and fuel Mumbaikars will travel from CST to Chembur in 25 minutes Will ease traffic congestion in Chembur, Sion and Dadar Mumbai, June 11, 2013 – The Chief Minister of Maharashtra Mr.Prithviraj Chavan will inaugurate the crucial Eastern Freeway on Thursday, June 13, 2013, at 3 p.m. along with Anik-Panjarpol Link Road. The 13.59-km signal- free stretch will ease traffic congestion in Chembur, Sion and Dadar areas and will reduce travel time from Chhatrapati Shivaji Terminus to Chembur to a mere 25 minutes. The Freeway will also provide the much needed speedy connectivity from the Island city to the eastern suburbs and to Navi Mumbai, Panvel, Pune and Goa. The project throws up a highlight that will make motorists happy. While the 9.29-km Eastern Freeway will be entirely elevated, the 4.3-km Anik-Panjarpol Link Road provides for a 550-meter long twin tunnel – first of its kind in urban setup of our country. Present on the occasion will be Mr. Milind Deora, Hon.Minister of State for Communication and Information Technology, Government of India, New Delhi; Mr. Ajit Pawar, Hon.Deputy Chief Minister, Maharashtra State; Mr. Jayant Patil, Hon.Minister for Rural Development and Guardian Minister, Mumbai City District, Mr.Mohd.Arif Naseem Khan, Hon.Minister for Textile and Guardian Minister, Mumbai Suburban District; Mr. Sunil Prabhu, Hon.Mayor, Mumbai; Mr.Eknath Gaikwad, Hon.MP, among other VIPs. The inauguration will take place at Orange Gate, P.D’Mello Road, Mumbai. -

Mindscapes of Space, Power and Value in Mumbai

Island Studies Journal, Vol. 9, No. 2, 2014, pp. 277-292 The epistemology of a sea view: mindscapes of space, power and value in Mumbai Ramanathan Swaminathan Senior Fellow, Observer Research Foundation (ORF) Fellow, National Internet Exchange of India (NIXI) Contributing Editor, Governance Now [email protected] ABSTRACT: Mumbai is a collection of seven islands strung together by a historically layered process of reclamation, migration and resettlement. The built landscape reflects the unique geographical characteristics of Mumbai’s archipelagic nature. This paper first explores the material, non-material and epistemological contours of space in Mumbai. It establishes that the physical contouring of space through institutional, administrative and non-institutional mechanisms are architected by complex notions of distance from the city’s coasts. Second, the paper unravels the unique discursive strands of space, spatiality and territoriality of Mumbai. It builds the case that the city’s collective imaginary of value is foundationally linked to the archipelagic nature of the city. Third, the paper deconstructs the complex power dynamics how a sea view turns into a gaze: one that is at once a point of view as it is a factor that provides physical and mental form to space. In conclusion, the paper makes the case that the mindscapes of space, value and power in Mumbai have archipelagic material foundations. Keywords : archipelago, form, island, mindscape, Mumbai, power, space, value © 2014 – Institute of Island Studies, University of Prince Edward Island, Canada. Introduction: unearthing the archipelagic historiography of Mumbai A city can best be described as a collection of spaces. Not in any ontological sense or in a physically linear form, but in an ever-changing, ever-interacting mesh of spatialities and territorialities that display the relative social relations of power existing at that particular point in time (Holstein & Appadurai, 1989). -

Mumbai Residential March 2019 Marketbeats

MUMBAI RESIDENTIAL MARCH 2019 MARKETBEATS 20% 60% 49% GROWTH IN UNIT SHARE OF MID SHARE OF EXTENDED SUBURBS L A U N C H E S ( Q o Q ) SEGMENT IN Q1 2019 IN LAUNCHES (Q1 2019) HIGHLIGHTS RENTAL VALUES AS OF Q1 2019* Average Quoted Rent QoQ YoY Short term Submarket New launches continue to grow (INR/Month) Change (%) Change (%) outlook Quarterly unit launches continued to grow in Q1 2019, recording a 20% q-o-q increase, High-end segment South 60,000 – 700,000 0% 0% with majority of project launches seen in Extended Eastern and Western Suburbs along South Central 60,000 - 550,000 0% 0% Eastern with the Thane submarket. These three submarkets contributed nearly 72% of quarterly 25,000 – 400,000 0% 0% Suburbs Western launches in Q1 2019. Major developers active during the quarter were Puranik Builders, 50,000 – 800,000 0% 0% Suburbs-Prime Lodha Group, Hiranandani Developers, Shapoorji Pallonji Real Estate and SD Corp. Mid segment Eastern 18,000 – 70,000 0% 0% Suburbs Western Affordable and mid segment driving demand 20,000 – 80,000 0% 0% Suburbs Affordable and mid-segment housing continued to remain the preferred categories for Thane 14,000 – 28,000 0% 0% buyers when making home purchase decisions. To cater to this growth segment, Navi Mumbai 10,000 – 50,000 0% 0% developers remained focused on launching projects in these segments. The share of mid- segment projects was 60% of the total unit launches during the quarter, followed by the CAPITAL VALUES AS OF Q1 2019* Average Quoted Rate QoQ YoY Short term Submarket affordable segment holding a 36% share. -

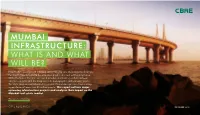

Mumbai Infrastructure: What Is and What Will Be?

MUMBAI INFRASTRUCTURE: WHAT IS AND WHAT WILL BE? Infrastructure development acts as a cornerstone for any city in order to determine the growth trajectory and to become an economic and real estate powerhouse. While Mumbai is the financial capital of India, its infrastructure has not been able to keep pace with the sharp rise in its demographic and economic profile. The city’s road and rail infrastructure is under tremendous pressure from serving a population of more than 25 million people. This report outlines major upcoming infrastructure projects and analyses their impact on the Mumbai real estate market. This report is interactive CBRE RESEARCH DECEMBER 2018 Bhiwandi Dahisar Towards Nasik What is Mumbai’s Virar Towards Sanjay Borivali Gandhi Thane Dombivli National current infrastructure Park framework like? Andheri Mumbai not only has a thriving commercial segment, but the residential real estate development has spread rapidly to the peripheral areas of Thane, Navi Mumbai, Vasai-Virar, Dombivli, Kalyan, Versova Ghatkopar etc. due to their affordability quotient. Commuting is an inevitable pain for most Mumbai citizens and on an average, a Mumbai resident Vashi spends at least 4 hours a day in commuting. As a result, a physical Chembur infrastructure upgrade has become the top priority for the citizens and the government. Bandra Mankhurd Panvel Bandra Worli Monorail Metro Western Suburban Central Rail Sea Link Phase 1 Line 1 Rail Network Network Wadala P D’Mello Road Harbour Rail Thane – Vashi – Mumbai Major Metro Major Railway WESTERN -

India- Mumbai- Residential Q4 2020

M A R K E T B E AT MUMBAI Residential Q4 2020 FESTIVE SEASON AND POLICY SUPPORT PROVIDES FURTHER IMPETUS TO LAUNCHES IN Q4 Mumbai’s residential sector rode on the policy support of lower stamp duty, developer incentives, low interest rates to record robust growth in quarterly launches in Y-O-Y DROP IN NEW LAUNCHES Q4, which also coincided with the festive season which has traditionally seen strong buyer and developer activity. Better sales momentum also allowed developers 46% IN 2020 the confidence to launch new projects, in H2 2020. A total of 11,492 units were launched during the quarter, which is nearly 2.4 times higher on a q-o-q basis. With 32,457 units launched in 2020, annual launches were down by 46% compared to 2019. Thane sub-market witnessed the highest launches in the quarter with a SHARE OF MID SEGMENTIN share of 26% followed by the sub-markets of Eastern Suburbs and Navi Mumbai with 22% and 16% share, respectively. Interestingly, Extended Eastern and 58% 2020 LAUNCHES Western Suburbs witnessed reduced launches during the quarter with elevated levels of unsold inventory being a major concern for developers in these sub- markets. Prominent developers like Dosti Realty, Runwal Group, Godrej Properties, Paradigm Realty, Raymond Realty and Marathon Realty were the most active during the quarter and contributed nearly 56% of the cumulative launches. Construction activity also gained some momentum during the quarter as developers 22% THANE’s SHARE IN LAUNCHES across sub-markets focused on completion of on-going projects. However, we expect delay in possession of new homes by nearly 3-6 months. -

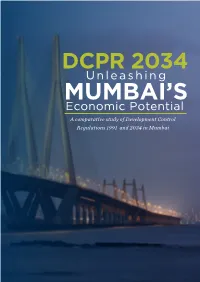

DCPR 2034 Unleashing MUMBAI’S Economic Potential a Comparative Study of Development Control Regulations 1991 and 2034 in Mumbai INTRODUCTION

DCPR 2034 Unleashing MUMBAI’S Economic Potential A comparative study of Development Control Regulations 1991 and 2034 in Mumbai INTRODUCTION INTRODUCTION GENERAL APPLICABILITY Real estate plays a crucial role in Mumbai’s economy The DCPR 2034 : and the government has been making concerted efforts to ensure that the sector functions efficiently and in a Came into effect from 1st September 2018 with some transparent manner in the city. With the launch of the 1. provisions notified later on 13th November 2018. Revised Draft Development Plan (RDDP) 2034 in May 2018, the state government laid down its vision for the city’s growth over the next two decades. Suggestions 2. Will govern all the building development activity were taken from various stakeholders, including the public, and development work in the entire jurisdiction of while formulating the plan. The Development Control and Municipal Corporation of Greater Mumbai (MCGM) Promotional Regulations (DCPR) 2034, which came into for the next two decades. effect in September 2018, is based on the provisions of the RDDP. 3. Will cover new redevelopment projects that are yet to obtain IOD/CC. Partially completed projects, which In order to revitalise Mumbai’s economic potential, there were started before the DCPR 2034 came into effect, is a need to give a concerted push to new development may be continued as per old regulations. However, while also seeking to redevelop private housing societies, if the owner/developer seeks further development cessed buildings, slums & MHADA colonies. Land in Mumbai permissions, then the DCPR 2034 provisions shall remains a scarce commodity and thus redevelopment is apply to the balance portion of the development. -

Mumbai Residential Marketbeat Q1 2021

MA R K E T B E AT MUMBAI Residential Q1 2021 Resurgence of COVID affected residential launches in Q1 Mumbai’s residential sector witnessed launch of 10,742 units during the first quarter of 2021 with a marginal q-o-q drop of 6.5%. Developers launched fewer units in the current quarter on the back of resurgence of COVID and rising infection levels in the city. On a y-o-y basis, launches were down by 39.1%, which Q-O-Q DROP IN NEW LAUNCHES indicates that sustained recovery is still a few quarters away though residential sales have been improving gradually. Eastern Suburbs submarket witnessed 6.5% (Q1 2021) the maximum launches during the quarter with a share of 29% followed by Extended Eastern Suburbs and Western Suburbs with 26% and 21% shares, respectively. On a quarterly basis, while all these submarkets witnessed growth in new launches, few other submarkets like Thane, Navi Mumbai and Extended Western Suburbs saw perceptible drop in quarterly launches. Prominent developers like Godrej Properties, Runwal Group, Oberoi Realty and 57% SHARE OF MID SEGMENT IN Raymond Realty were the most active during the quarter and contributed nearly 47% of the total new launched units. Developers across all submarkets have UNIT LAUNCHES (Q1 2021) been focusing on the completion of ongoing projects but rising Covid cases and localized restrictions might impact construction timelines and further delay the handover of new homes by at least 3-6 months. SHARE OF EASTERN SUBURBS During the quarter, sales activity remained healthy as developers continued to offer various payment incentives to attract homebuyers along with the 29% IN UNIT LAUNCHES (Q1 2021) reduction in stamp duty that drove the housing demand. -

Open Spaces & Water Bodies in Greater Mumbai

Inventorisation of Open spaces & Water Bodies in Greater Mumbai PREFACE Mumbai, the largest metropolis of India and the third largest in the world, is a unique city. It enjoys both, a dense and multi cultural demographic diversity as well as a varied range of environmental features. There are rivers, natural drains, lakes, hills, forests and coastal features like beaches, rocky outcrops, mangroves and creeks. However, growth in population and changes in the State policies, in the past few decades has resulted in phenomenal construction activity adversely affecting all the environmental features. While the natural water bodies are fast disappearing through negligence, and uncontrolled development, the open spaces meant for recreation and sports are grossly inadequate, both in their numbers and in their areas, to address the bare minimum needs of Mumbai’s growing population. The Open Spaces, marked as Reservations on the Development Plan of Greater Mumbai, as Recreational Grounds, Play Grounds, Gardens etc, account for only 6% of the land area. On the other hand the locations of the existing water bodies are not even indicated on the Development Plan. This Development Plan was prepared in the 1980s, for which the survey was undertaken in 1980. Needless to say, that the ground reality of these reservations, after 30 years, is enormously different. The current reality therefore needs to be thoroughly examined on two levels: a) with respect to their deficiency and b) with respect to their current status and conditions. Only after such an assessment that an appropriate strategy can be devised; a strategy which will ensure the provision of Open Spaces that are both, adequate and accessible to all. -

Worli-Micro-Market-Overview-Report

South WORLI Central The Rise of Worli, the most sought-after Real Estate in Mumbai December 2017 CONTENTS Micro Market Overview 4 - 8 Evolution of the Micro Market Location Mapping Connectivity & Major Growth Drivers Social Infrastructure Physical Infrastructure – Existing/Ongoing/Proposed Commercial Market Overview 10 - 11 Overview Rental Values Comparison – Mumbai Metropolitan Region Capital Value Trends – Worli Key Completed Commercial Developments in the Precinct Residential Market Overview 12 - 16 Inventory Summary New Launch Supply-Unsold Inventory Dynamics-Under Construction Projects Unsold Inventory Breakup with Absorption Micro Market Price Trends Unit Size-Ticket Price Breakup with Absorption Graphical Representation – Key projects Livability Assessment 17 Why Worli? 18 Worli I Micro Market Overview | 3 Bandra-Worli Sea Link Micro Market Overview Evolution of the Micro Market Worli, known as a destination of textile mills a few decades ago, has now completely transformed into a posh neighborhood of South Mumbai. Located in the southern part of Mumbai, Worli has emerged as one of the prime residential areas in the last decade. The micro market is considered to be the new luxury housing destination for industrialists, business honchos, sports personalities and celebrities. Proximity and easy access to the seashore has significantly transformed the realty landscape of Worli. Whilst premium residential micro markets in South Mumbai were struggling for large scale residential developments, due to unavailability of large land parcels, Worli emerged as a prime residential market for luxury developments overlooking the sea. Due to its distinct “downtown” image and seamless connectivity to the Mumbai’s de-facto CBD (Bandra- Kurla Complex), Worli has become one of the most sought after residential destination in the city. -

6.1.1. Storm Water Drainage Network

6. STORM WATER DRAINAGE 6.1. Existing Situation 6.1.1. Storm Water Drainage Network Mumbai city receives seasonal rainfall for four months i.e. from June to September. Average rainfall is 2,000 mm, of which 70 per cent is during July & August. Mumbai is lined on the west by Arabian Sea and is intercepted by number of creeks (Mahim, Mahul and Thane creeks), rivers (Mithi, Dahisa, Poisar and Oshiwara rivers, and their tributaries) and a complex nallah system. The SWD system of Mumbai comprises a hierarchical network of roadside surface drains (about 2,000 km mainly in the suburbs), underground drains and laterals (about 440 km in the island city area), major and minor nallahs (200 km and 87 km respectively) and 186 outfalls, which discharge all the surface runoff into rivers and the Arabian Sea. Table 24: Summary of the storm water drainage system Western Eastern Sl. Drain Hierarchy / Type Island City Total Suburbs Suburbs 1 Major Nallah (width >1.5m) 9 90 102 200 2 Minor Nallah (width <1.5m) 21 66 87 3 Arch/Box Drains 59 40 52 151 4 Roadside Open Drains 20 669 1,298 1,987 5 Closed Pipe or Dhapa Drains 443 36 86 565 6 Total SWD length 531 857 1,603 2,991 7 No. of Water Entrances 27,893 609 1,706 30,208 Note: The above figures (for Sl. 1 to 6) are lengths in kilometers Of the 186 outfalls, there are 107 major outfalls in city, which drain to Arabian Sea directly, 4 at Mahim creek and 4 at Mahul creek. -

Urban Transport Unlocking the Realty Potential

RESEARCH URBAN TRANSPORT UNLOCKING THE REALTY POTENTIAL MUMBAI METROPOLITAN REGION INFRASTRUCTURE DEVELOPMENT ANALYSIS TABLE OF CONTENTS Introduction 4 How does the MMR and Mumbai city compare with each other? 6 What are the characteristics of the residential micro-markets in the MMR? 6 What drives the MMR residential market? 9 What are the implications of the infrastructure development in the MMR? 11 Metro rail corridors 12 Coastal Road project 14 Mumbai Trans Harbour Link (MTHL) project 20 “URBAN TRANSPORT” UNLOCKING THE REALTY POTENTIAL RESEARCH Introduction Sustaining the country’s rapid urbanisation would require corresponding infrastructure development. The need for infrastructure development, particularly urban transport, in a megapolis like Mumbai, is unquestionable. While the benefits of urban transport in terms of enhanced connectivity and an improved quality of life have been widely recognised, unlocking the realty potential in terms of better development prospects is also an interesting arena for stakeholders. In fact, the high price gradient of `3,000–100,000 per sq ft for residential property in the MMR makes it even more important to stay ahead of time and decipher the impact of infrastructure development on property demand and the resultant impact on prices. With this white paper, we provide an assessment of select urban transport projects that are high on the state government’s priority list and also have an ambitious yet attainable completion target of 2019, which is within the term of the present government. Accordingly, an assessment of the metro corridors of Dahisar West–DN Nagar, Andheri East–Dahisar East, the Coastal Road and the Mumbai Trans Harbour Link has been presented in the report. -

Upgrading Housing Settlements in Developing Countries

Cities, Vol. 18, No. 4, pp. 213–222, 2001 Pergamon PII: S0264-2751(01)00014-2 2001 Elsevier Science Ltd. All rights reserved Printed in Great Britain 0264-2751/01 $ - see front matter www.elsevier.com/locate/cities Upgrading Housing Settlements in Developing Countries The Impact of Existing Physical Conditions Vinit Mukhija University of California Los Angeles, 3250 Public Policy Building, Los Angeles, CA 90095-1656, USA Both conventional policy, and the literature on housing consolidation for low-income groups in developing countries typically focus only on tenure status as the key variable in housing improvement, and on tenure legalization, as the preferable, in situ improvement strategy. Demolition of slums and their redevelopment is not considered as an option that may be in the best interest of slum dwellers. This paper, however, presents evidence from Mumbai’s experience with slum redevelopment programs that suggests that the prevailing wisdom has limitations and that under certain conditions, there is a constituency among slum dwellers for redevelopment. Secondly, the Mumbai case suggests that policy makers and analysts, apart from focusing on tenure status should also pay attention to the existing physical conditions within settlements. Physical conditions — the location of settlements; the land uses in them; settlement layouts; and the sizes of the lots within them — can impact the success of upgrading strategies, particularly, the preference of beneficiaries for different strategies. However, the slum dwellers’ interest in redevelopment is not simply because of a consumer preference for better housing conditions but more likely because of an economic interest in more valuable housing. 2001 Elsevier Science Ltd.