Rural Households' Livelihood Capital, Risk Perception, And

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Post-Disaster Assessment of 2017 Catastrophic Xinmo Landslide (China) by Spaceborne Sar Interferometry

This paper has to be cited as: Dai K, Xu Q, Li Z, Tomás R, Fan X, Dong X, Li W, Zhou Z, Gou J and Ran P (2019) Post-disaster assessment of 2017 catastrophic xinmo landslide (china) by spaceborne sar interferometry. Landslides. doi: 10.1007/s10346-019-01152-4. The final publication is available at Springer via: https://link.springer.com/article/10.1007/s10346-019-01152-4 1 Post-disaster assessment of 2017 catastrophic Xinmo landslide 2 (China) by spaceborne SAR interferometry 3 Keren Dai1,2,3, Qiang Xu1*, Zhenhong Li4, Roberto Tomás5, Xuanmei Fan1, 4 Xiujun Dong1, Weile Li1, Zhiwei Zhou2, Jisong Gou3, Peilian Ran3 5 1. State Key Laboratory of Geohazard Prevention and Geoenviroment Protection, Chengdu 6 University of Technology, Chengdu 610059, China; 7 2. State Key Laboratory of Geodesy and Earth’s Dynamics, Institute of Geodesy and 8 Geophysics, Chinese Academy of Sciences, Wuhan 430077, China; 9 3. College of Earth Sciences, Chengdu University of Technology, Chengdu 610059, China; 10 4. COMET, School of Engineering, Newcastle University, Newcastle upon Tyne NE1 7RU, UK; 11 5. Departamento de Ingeniería Civil, Escuela Politécnica Superior, Universidad de Alicante, 12 P.O. Box 99, E-03080 Alicante, Spain 13 * Corresponding author. [email protected] 14 Abstract: Timely and effective post-disaster assessment is of significance for the 15 design of rescue plan, taking disaster mitigation measures and disaster analysis. Field 16 investigation and remote sensing methods are the common way to perform post-disaster 17 assessment, which are usually limited by dense cloud coverage, potential risk and tough 18 transportation etc. -

3 PRESENT CONDITION of ROADS and TRANSPORT 3.1 Condition of Road Facilities 3.1.1 Existing Road Network and Classification of R

3 PRESENT CONDITION OF ROADS AND TRANSPORT 3.1 Condition of Road Facilities 3.1.1 Existing Road Network and Classification of Roads (1) Primary Road Network in the Study Area As shown in Figure 3.1.1, the existing Primary Road network in the Study Area considers the Tianfu Square as its center and is made up of ring roads and radial roads. There are 5 ring roads at present including the existing roads and roads under construction. The existing roads include the Inner Ring Road with a radius of 2 km, the 1st Ring Road with a radius of 3 km, and the 2nd Ring Road with a radius of 4 km. There are two roads under construction, namely the 3rd Ring Road with a radius of 7 km, and the Outer Ring Road with a radius of 11 km. The construction of these two roads is underway, and most exits for expressways and main carriageway have been constructed already. It is expected that the 3rd Ring Road and the Outer Ring Road will be completed by 2001 and 2002, respectively. The Inner Ring Road has four lanes for both directions with a total road width of 25 m. The 1st Ring Road and 2nd Ring Road have not only four lanes for both directions but also a segregated bicycle lane on both sides with a total width of 40 m. Furthermore, the 3rd Ring Road and the Outer Ring Road under construction have 8 lanes and 6 lanes for both directions, respectively, with a total width of 80m. -

Internal Ex-Post Evaluation for Technical Cooperation Project

Internal Ex-Post Evaluation for Technical Cooperation Project conducted by China Office: November, 2018 Country Name People's Republic of Project on Forest Restoration after the Earthquake in Sichuan Province China I. Project Outline The Sichuan Earthquake, which occurred in Wenchuan County in Sichuan Province in China on May 12, 2008, caused a great deal of damages to forest vegetation. As measures to restore the disaster-affected forests, the Government of China launched a policy to restore multiple functions of forests in stages through combining natural regeneration and artificial restoration. Through JICA’s technical cooperation project “The Background Model Afforestation Project in Sichuan” (2000-2007), technologies such as “Chisan” technologies using simple work methods had been developed in Sichuan Province. However, because of diverse geographical conditions of the areas affected by the Sichuan Earthquake, it was difficult to determine the precise measures for each condition. In addition, technical and management capacity of the related agencies was not sufficient for restoration of forest vegetation which had been destroyed in an unprecedented scale in China. The project aims at improving technical capacity of the related agencies of Sichuan Province, engaged in restoration projects for typical disaster-affected forests in the project areas1 in the earthquake-stricken areas in Sichuan Province in China, through development of restoration plans for the typical disaster-affected forests, establishment of technological system concerning major forest restoration work methods, and enhancement of contents and system of technical training necessary for implementation of restoration works Objectives of the Project for the disaster-affected forests, thereby enabling sustainable and self-reliant implementation of restoration projects for the disaster-affected forests. -

China, Das Chinesische Meer Und Nordostasien China, the East Asian Seas, and Northeast Asia

China, das Chinesische Meer und Nordostasien China, the East Asian Seas, and Northeast Asia Horses of the Xianbei, 300–600 AD: A Brief Survey Shing MÜLLER1 iNTRODUCTION The Chinese cavalry, though gaining great weight in warfare since Qin and Han times, remained lightly armed until the fourth century. The deployment of heavy armours of iron or leather for mounted warriors, especially for horses, seems to have been an innovation of the steppe peoples on the northern Chinese border since the third century, as indicated in literary sources and by archaeological excavations. Cavalry had become a major striking force of the steppe nomads since the fall of the Han dynasty in 220 AD, thus leading to the warfare being speedy and fierce. Ever since then, horses occupied a crucial role in war and in peace for all steppe riders on the northern borders of China. The horses were selectively bred, well fed, and drilled for war; horses of good breed symbolized high social status and prestige of their owners. Besides, horses had already been the most desired commodities of the Chinese. With superior cavalries, the steppe people intruded into North China from 300 AD onwards,2 and built one after another ephemeral non-Chinese kingdoms in this vast territory. In this age of disunity, known pain- fully by the Chinese as the age of Sixteen States (316–349 AD) and the age of Southern and Northern Dynas- ties (349–581 AD), many Chinese abandoned their homelands in the CentraL Plain and took flight to south of the Huai River, barricaded behind numerous rivers, lakes and hilly landscapes unfavourable for cavalries, until the North and the South reunited under the flag of the Sui (581–618 AD).3 Although warfare on horseback was practised among all northern steppe tribes, the Xianbei or Särbi, who originated from the southeastern quarters of modern Inner Mongolia and Manchuria, emerged as the major power during this period. -

Earthquake and Poverty with Chinese Characteristics Wenchuan Earthquake Affected Communities Ten Years After the Disaster

UNIVERSITY OF OSLO Earthquake and poverty with Chinese characteristics Wenchuan earthquake affected communities ten years after the disaster Dragana Grulovic Asia and Middle East Studies/Chinese Society and Politics KIN4593 – Master’s Thesis in Chinese Society and Politics (30 credits) Department of Culture Studies and Oriental Languages Spring 2019 Earthquake and poverty with Chinese characteristics Wenchuan earthquake affected communities ten years after the disaster © Dragana Grulovic 2019 Earthquake and poverty with Chinese characteristics - Wenchuan earthquake affected communities ten years after the disaster Dragana Grulovic https://www.duo.uio.no Print: Webergs Print Abstract In May 2008, China was struck by a massive earthquake that killed closed to 70,000 people. Communities were torn to the ground, and the economic losses were enormous. Ten years have passed since the massive forces took place, and communities and lives have been rebuilt, with some preceding their pre-disaster economic levels. This study applies survey data to estimate the poverty rates in the Wenchuan earthquake affected communities ten years after the disaster. I find that in 2018, the poverty incidence was 3% in the overall area, as compared to 9% before the earthquake. Of the total of 198 sampled communities, 27 reported having no government- designated poor people. However, 23 communities have a poverty prevalence of 10% or higher. These communities have few characteristics in common in terms of demographic structure and access to public services. About half of the communities are located in government-designated poor counties, while the rest are not. Altogether, the poverty situation in the Wenchuan earthquake affected area reflects the complexity of poverty in China. -

Safety Assessment and Retrofit Techniques of Quake Lakes

Safety Assessment and Retrofit Techniques of Quake Lakes Xingguo Yang, Hongwei Zhou, Hongtao Li, Zhaohui Yang, Lu Qiao, Yuanyuan Lin July 13,2009 CONTENT 1.1 Introduction 2.2 Main Tasks and Basic Data Collection in Safety Assessment 3.3 Risk Level of Quake Lakes 4.4 Risk Assessment of Landslide Dam 5.5 Improvement and Protection of Quake Lakes 6.6 Conclusions July 13,2009 1 INTRODUCTION • The great Wenchuan Earthquake formed more than 100 Quake lakes with a dam taller than 10 m, a water storage capacity larger than 1.0×105 m3 and a catchment area greater than 20 km2. • Statistical data show that these are the largest number of Quake lakes created by a single earthquake in human history. July 13,2009 1 INTRODUCTION • These Quake lakes have the following common features: – Extensive and dense distributed; – Formed in rivers where the landslide dams had already formed within 40 years, indicating that the river banks are not stable; – Treated or self-burst, not causing any disaster or casualty, and – 90% of them are in stable, healthy conditions. July 13,2009 2 Main Tasks and Basic Data Collection in Safety Assessment • The main tasks of safety assessment of Quake lakes include: – Assessment of risk level of Quake lake; – Assessment of stability of landslide dam; – Assessment of impact to the upstream and downstream areas, and – Comprehensive evaluation of risk of quake lake. July 13,2009 2 Main Tasks and Basic Data Collection in Safety Assessment • Related standard has detailed provision for basic data collection. It is suggested that: 1. -

Study on the Qiang's Costume Culture—A Case Study of the Qiang's Costumes in Li County

Open Journal of Social Sciences, 2018, 6, 225-234 http://www.scirp.org/journal/jss ISSN Online: 2327-5960 ISSN Print: 2327-5952 Study on the Qiang’s Costume Culture—A Case Study of the Qiang’s Costumes in Li County Chunlei Song, Bing Zhao* Southwest University for Nationalities, Chengdu, China How to cite this paper: Song, C.L. and Abstract Zhao, B. (2018) Study on the Qiang’s Cos- tume Culture—A Case Study of the Qiang’s As a part of fifty-six ethnic minorities, the Qiang ethnic has long-established Costumes in Li County. Open Journal of national culture and is also an important part of intangible cultural heritage. Social Sciences, 6, 225-234. The article outlines the connotation of the Qiang’s culture, elaborates the aes- https://doi.org/10.4236/jss.2018.66020 thetic characteristics, pattern characteristics, color characteristics, and com- Received: June 1, 2018 positional characteristics of the Qiang’s costumes. Taking the Qiang’s cos- Accepted: June 26, 2018 tumes in the Mao County area as an example, through analysing the materials Published: June 29, 2018 of Qiang’s costumes in the Mao County, the paper deeply analyzes the differ- Copyright © 2018 by authors and ences in cultural customs and dressing habits between different regions. The Scientific Research Publishing Inc. unique geographical features of Li County’s clothing are summarized based This work is licensed under the Creative on these differences. The Qiang ethnic calls itself “er ma” or “er mie”, and it is Commons Attribution International also being called “nation on the cloud”. -

Sichuan Explorer

Sichuan Explorer Sichuan Explorer 13 Days Your Tour Dossier Fully Inclusive from the UK This document is designed to be read in conjunction with the other pre- Sichuan Province is the natural habitat of one of the world’s departure information provided by Wendy Wu Tours including the tour endangered species – the panda. We observe these magnificent itinerary as described in our brochure and/or website. It aims to creatures at the famous Panda Reserve in Chengdu as well as provide a straightforward description of the physical activities involved admire the Grand Buddha in Leshan. We also visit Mt Emei, in sightseeing or travelling during the tour. Buddhist Dazu and beautiful Nine Villages Valley. If there are any particular challenges, from the length of time spent on This tour reaches a maximum altitude of 3,500m at Huanglong your feet, the length of drives and flights, to the standard of remote Temple. accommodation; they will be explained here. Fully Inclusive price includes: All passengers must read this document to ensure the itinerary is • International flights and current taxes suitable for their interests and physical capabilities. This is not your final • Domestic transportation itinerary and therefore does not mention all the sites visited. • Accommodation • All meals (excluding drinks) • T ouring with guides and entrance fees • Visa fees for UK passport holders Book now on 0844 499 3899 visit www.wendywutours.co.uk or see your preferred travel agent. Welcome to Wendy Wu Tours China continues to amaze, fascinate and thrill our passengers, many of whom have travelled to one country in Asia with us, then another, year after year. -

Major Parameters of Wenchuan Earthquake

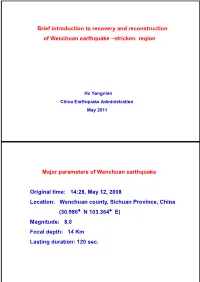

Brief introduction to recovery and reconstruction of Wenchuan earthquake –stricken region He Yongnian China Earthquake Administration May 2011 Major parameters of Wenchuan earthquake Original time: 14:28, May 12, 2008 Location: Wenchuan county, Sichuan Province, China (30. 986°N 103. 364°E) Magnitude: 8.0 Focal depth: 14 Km Lasting duration: 120 sec. Outline of Damage and loss of the earthquake Items Total* Total affected area 500,000 km2, 417 counties, 4,667 towns, 48,810 villages Severely affected area 130,000 km2, 51 counties Evacuated and temporarily 151.1 million people resettled IjInjure d 43 million peopl e Severely injured Over 10,000 sent to 370 hospitals Rescued and saved 84,017 people Received relief aid 8,810,000 people Economic loss RMB Yuan 845 billion * Include Sichuan, Gansu and Shaanxi Provinces Distribution of the Main Shock and Aftershocks (M>4.0) The seismic intensity (MMS) reached IX degree in epicenter region between Yingxiu town, Wenchuan county and Qushan town, Beichuan county, the area is 2419 KM2 The seismic intensity of X degree is of 3144 Km2; The seismic intensity of XI degree is 7738 Km2. SiSeismogen ic t ect oni cs of fW Wench uan earth quak e WenchuanWenchuan Longmenshan Longmenshan Maowen-Maochuan fault M=8.0 Yingxiu-Beichuan fault Dujiangyan-Jiangyou fault Longmenshan fault zone, consisting of three faults: Maowen-Maochuan fault, Yingxiu-Beichuan fault and Dujiangyan-Jiangyou fault, is one of the major seismic zones in China. The Wenchuan earthquake with M=8.0 occurred on the Yingxiu- Beichuan fault. General picture of urban destruction of Wenchuan earthquake: Qushan town, Beichuan county Almost all buildings were destructed in Yingxiu Town, Wenchuan county The Xioayudong bridge was collapsed due to the earthquake, Pengzhou city , Sichuan province. -

Exploring the Relationship Between the Arid Valley Boundary's

International Journal of Geo-Information Article Exploring the Relationship between the Arid Valley Boundary’s Displacement and Climate Change during 1999–2013 in the Upper Reaches of the Min River, China Yalin Guo, Qing Wang * and Min Fan School of Environment and Resource, Southwest University of Science and Technology, Mianyang 621010, Sichuan, China; [email protected] (Y.G.); fi[email protected] (M.F.) * Correspondence: [email protected]; Tel.: +86-28-6608-9459 Academic Editor: Wolfgang Kainz Received: 2 March 2017; Accepted: 24 April 2017; Published: 6 May 2017 Abstract: The arid valley is a unique type of ecological fragile landscape in the Hengduan Mountain Area, China. The boundary of the arid valley is one of the response indicators to mountainous climate change. Based on the meteorological data from 1999 to 2013 and the SPOT remote sensing images in 1999 and 2013 this study explored the response characteristics of the arid valley boundary to regional climate change in the upper reaches of the Min River in the Hengduan Mountains. The results are as follows: (1) During 1999–2013, the temperature, precipitation, and evaporation increased, and the sunshine duration and relative humidity showed decreasing trends at the rates of 0.008 ◦C/a, 2.25 mm/a, 5.51 mm/a, −8.72 h/a, and −0.19%/a, respectively. Meanwhile, the climate showed the warm-dry tendency in the southern region and the warm-humid tendency in the central and northern areas. (2) On the whole, the arid valley boundary mainly distributed between 1601–3200 m and moved downward to 2428 m at the speed of −0.76 ± 0.26 m/a along with global warming. -

Summary of the Present Situation of Inheritance of Qiang Dance in Pre-School Education

Review of Educational Theory Summary of the Present Situation of Inheritance of Qiang Dance in Pre-School Education Haolin Shi Sichuan Preschool Educators College, Jiangyou, Sichuan, 621709, China Abstract: The Qiang Nationality has a long history and forms a dance form rich in lively rhythm, beats and heroic dance postures in the long process of its development. As a member of the Chinese traditional dance culture, and affected by Qiang Nationality's no written language, the Qiang dance can only be inherited by means of oral or mental instruction. Therefore, its inheritance has already been in crisis with the Qiang people's gradually going out of the national and geographical restrictions. At this time, teaching Qiang dance in the pre-school education can achieve the purpose of cultivating the traditional dance feelings of Qiang Nationality from the early childhood, thus making the children become inheritor and disseminator of Qiang culture. At the present stage, many scholars in our country have explored the inheritance of Qiang dance in pre-school education, and have reached certain research results. Af- ter clarifying the internal and external influencing factors of the Qiang dance and its inheritance, this paper summarizes the existing research results mainly from the two aspects including the problems of Qiang dance inheritance existing in the pre-school education and its application to the inheritance strategy. Keywords: Qiang dance; Pre-School education; Culture inheritance 1. Introduction dance teaching in the pre-school education and the inheri- tance of Qiang dance culture. he Chinese nation is composed of fifty-six nation- alities and each nation has its own unique national 2. -

IACP Newsletter

Issue No. 6 December 31, 2011 IACP Newsletter Newsletter Editor: Richard LeGates Email: [email protected] Chinese version: Jianxiang Huang E-mail: [email protected] 2011 in Review Sixth IACP Conference at Wuhan University The 6th annual IACP conference will take place at Wuhan University (Page 17) June 17 - 19, 2012 June 17-19, 2012. The sixth annual IACP conference will th The 5 annual IACP conference was held at take place at Wuhan University June 17- Renmin University in Beijing (Page 2). 19, 2012. Registration and possible pre- conference events will be on June 17. Nick Smith from Harvard University received the Polenske award at the The conference is being organized by the IACP-Renmin conference (Page 5). IACP and Wuhan University. The Urban Planning Society of China will co-sponsor HOU Yuan from Hong Kong Baptist the conference. University and MA Yiqiu from Shanghai Jiaotong University shared the IACP best A call for paper abstracts will be posted on student paper award at the IACP-Renmin the IACP website and sent to members conference. (Page 5). soon. Seven new IACP board members were The conference language will be English elected in the 2011 IACP elections (Page 7). with simultaneous translation into Chinese of keynote speeches and plenary sessions. IACP and Renmin University organized a There will be help at paper sessions for foreign experts tour of Chengdu’s coord- Chinese speakers who would like inated urban-rural development (Page 9). assistance translating their presentations from Chinese to English. th The 6 annual IACP general membership meeting took place at the ACSP conference in Salt Lake City, Utah in November (Page 13).