List of Marginable Securities with Effect from 12 October 2017 (Hk Market)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

China's Merchant Marine

“China’s Merchant Marine” A paper for the China as “Maritime Power” Conference July 28-29, 2015 CNA Conference Facility Arlington, Virginia by Dennis J. Blasko1 Introductory Note: The Central Intelligence Agency’s World Factbook defines “merchant marine” as “all ships engaged in the carriage of goods; or all commercial vessels (as opposed to all nonmilitary ships), which excludes tugs, fishing vessels, offshore oil rigs, etc.”2 At the end of 2014, the world’s merchant ship fleet consisted of over 89,000 ships.3 According to the BBC: Under international law, every merchant ship must be registered with a country, known as its flag state. That country has jurisdiction over the vessel and is responsible for inspecting that it is safe to sail and to check on the crew’s working conditions. Open registries, sometimes referred to pejoratively as flags of convenience, have been contentious from the start.4 1 Dennis J. Blasko, Lieutenant Colonel, U.S. Army (Retired), a Senior Research Fellow with CNA’s China Studies division, is a former U.S. army attaché to Beijing and Hong Kong and author of The Chinese Army Today (Routledge, 2006).The author wishes to express his sincere thanks and appreciation to Rear Admiral Michael McDevitt, U.S. Navy (Ret), for his guidance and patience in the preparation and presentation of this paper. 2 Central Intelligence Agency, “Country Comparison: Merchant Marine,” The World Factbook, https://www.cia.gov/library/publications/the-world-factbook/fields/2108.html. According to the Factbook, “DWT or dead weight tonnage is the total weight of cargo, plus bunkers, stores, etc., that a ship can carry when immersed to the appropriate load line. -

New Port Development and Global City Making: Emergence of the Shanghai-Yangshan Multilayered Gateway Hub Chengjin Wang, César Ducruet

New port development and global city making: Emergence of the Shanghai-Yangshan multilayered gateway hub Chengjin Wang, César Ducruet To cite this version: Chengjin Wang, César Ducruet. New port development and global city making: Emergence of the Shanghai-Yangshan multilayered gateway hub. Journal of Transport Geography, Elsevier, 2012, 25, pp.58-69. halshs-00717879 HAL Id: halshs-00717879 https://halshs.archives-ouvertes.fr/halshs-00717879 Submitted on 13 Nov 2012 HAL is a multi-disciplinary open access L’archive ouverte pluridisciplinaire HAL, est archive for the deposit and dissemination of sci- destinée au dépôt et à la diffusion de documents entific research documents, whether they are pub- scientifiques de niveau recherche, publiés ou non, lished or not. The documents may come from émanant des établissements d’enseignement et de teaching and research institutions in France or recherche français ou étrangers, des laboratoires abroad, or from public or private research centers. publics ou privés. New port development and global city making: Emergence of the Shanghai-Yangshan multilayered gateway hub Chengjin WANG Key Laboratory of Regional Sustainable Development Modeling Institute of Geographical Sciences and Natural Resources Research (IGSNRR) Chinese Academy of Sciences (CAS) Beijing 100101, China [email protected] César DUCRUET French National Centre for Scientific Research (CNRS) UMR 8504 Géographie-cités F-75006 Paris, France [email protected] Abstract Planned as Shanghai's new port, Yangshan is currently expanding its roles as transhipment hub and integrated logistics/industrial center in the Asia-Pacific region. This paper examines the impact of the emergence of Yangshan on the spatial pattern of the Yangtze River Delta since the 1970s, with reference to existing port system spatial evolutionary models. -

Polar Seaways? Maritime Transport in the Arctic: an Analysis of Shipowners’ Intentions II

1 Polar Seaways? Maritime Transport in the Arctic: An Analysis of Shipowners’ Intentions II. Frédéric Lasserre Corresponding author Professor, Laval University [email protected] Leah Beveridge Research Assistant, Dalhousie University [email protected] Mélanie Fournier Post-doctoral Fellow, Dalhousie University [email protected] Pierre-Louis Têtu PhD student, Laval University [email protected] Linyan Huang PhD student, Laval University [email protected] Abstract Climate change in the Arctic is leading to the fast recession of the sea ice extent in the summer. This evolution leads several observers, scientists, media and government officials, to consider the possibility of developing new shipping routes along Arctic routes, as these routes are much shorter between Europe and Asia. The literature displays a strong interest for these potential shipping routes while the media often assume shipping companies nurture a sustained attraction for Arctic routes. This paper tackles with this idea and examines to what extent shipping companies, the ultimate economic agents, are really interested in Arctic shipping routes. The image the research portrayed is that only a minority of shipping companies are indeed interested, and those that are interested stress the destinational dimension of Arctic shipping, not transit shipping. Keywords: Arctic shipping; NSR; NWP; transit; destinational traffic; business strategy. Lasserre, F.; Beveridge, L. ; Fournier, M.; Têtu, P-L, Huang, L. (2016). Polar seaways? Maritime transport in the Arctic: An analysis of shipowners' intentions II. Journal of Transport Geography, 57(2016) 105-114, http://dx.doi.org/10.1016/j.jtrangeo.2016.10.004 2 Acknowledgements This research was funded by ArcticNet Research Network (Canada); the Social Sciences and Humanities Research Council of Canada (SSHRC); the Natural Sciences and Engineering Research Council of Canada (NSERC). -

Privatization Amid Ongoing Recovery, Maintain "Accumulate"

股 票 Research 研 [Table_Title] Company Report: Sinotrans Shipping (00368 HK) Spencer Fan 范明 究 (86755) 2397 6686 Equity 公司报告: 中外运航运 (00368 HK) [email protected] 21 September 2018 Privatization[Table_Summary] amid Ongoing Recovery, Maintain "Accumulate" 复苏在途,计划私有化,维持“收集” Privatization planned: In accordance with SASAC rules and the Company’s [Table_Rank] valuation in recent years, we estimate 0.9x-1.0x acquisition PBR for the Rating: Accumulate Maintained privatization of Sinotrans Shipping, which corresponds to approx. 100% 公 upward price potential. We await further disclosure of details. 司 评级: 收集 (维持) Operating strategy in 1H18 was unexpectedly cautious. The Company’s 报 1H18 revenue declined 0.7% YoY to US$497 mn due to less dry bulk 6[Table_Price-18m TP目标价] : HK$2.22 告 shipping capacity in control, yet shareholders' profit surged 399.85% YoY to Revised from 原目标价: HK$2.36 US$40.018 mn amid effective cost control. The price of 70% of self-owned Company Report vessels will be locked in in 2H18 to secure stable margins. Sino-U.S trade Share price 股价: HK$1.810 tension will have limited impact on dry bulk profitability. Improving capacity structure with possible higher-than-expected Stock performance demand in 2H18. Projected supply/ demand growth has been revised to 股价表现 1.7%/ 3.2% for 2018. Average grain shipping distance might rise. Iron ore [Table_QuotePic] import is expected to stay robust amid heating housing construction; we % of return 30.0 estimate 2018 dry bulk revenue to slightly decline by 2.2% YoY. 20.0 Container business gradually forming into good shape. -

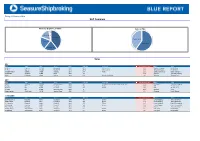

S&P Summary Sales

Friday 31 October 2014 S&P Summary Sales by Buyers Location Sales by Type Europe, 7.6 Unknown, 40.65 China 98.5 Tankers, 100.30 Greece 49.7 Bulkers, 148.85 Hong Kong, 52.7 Sales DRY Name Type DWT Yard Built USD mill Comments VesselsValue.com Buyer Seller ER Beilun Capesize 179,400 Hyundai HI 2010 49.25 TCB to sellers 43.7 Sinotrans Shipping ER Schiffahrt ER Brazil Capesize 179,400 Hyundai HI 2010 49.25 TCB to sellers 43.7 Sinotrans Shipping ER Schiffahrt Mandarin Wisdom Ultramax 64,000 Hantong 2015 28.7 Resale 26.9 Erasmus Shipinvest Dasin Holdings Pte Darya Bhakti Supramax 56,000 Mitsui 2005 16.8 16.7 Unknown Chellaram Shipping Nestor Handysize 28,600 Hudong 1997 4.85 At auction in Piraeus 5.6 Unknown Tsangaris Bros WET Name Type DWT Yard Built USD mill Comments VesselsValue.com Buyer Seller Amin 2 Suezmax 158,000 Hyundai Samho 2009 52.7 At auction in Xiamen, after being laid up 1 year 56.0 HK based Irano Hind Shipping Risanger MR 46,300 Daedong 2000 10.5 En bloc 10.6 IMS Westfal Larsen Ravnanger MR 46,300 Daedong 2000 10.5 En bloc 10.6 IMS Westfal Larsen Nord Star MR 46,000 Shin Kurushima 2009 19 22.2 Unknown Torm Clipper Leander Small Clean 10,100 Yardimci Deniz 2006 7.6 9.3 European Nordic Tankers CONTAINER Name Type TEU Yard Built USD mill Comments VesselsValue.com Buyer Seller SCI Nhava Sheva Panamax 5,042 Hyundai HI 2005 17.5 En bloc 16.5 Lomar Shipping Offen Claus-Peter Santa Priscilla Panamax 5,042 Hyundai HI 2005 17.5 En bloc 16.5 Lomar Shipping Offen Claus-Peter HS Livingstone Panamax 4,990 Hanjin HI 2004 15.5 En bloc 14.5 -

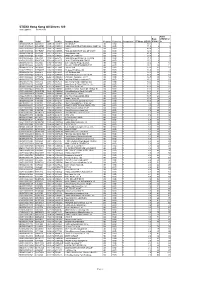

STOXX Hong Kong All Shares 180 Last Updated: 03.04.2018

STOXX Hong Kong All Shares 180 Last Updated: 03.04.2018 Rank Rank (PREVIOU ISIN Sedol RIC Int.Key Company Name Country Currency Component FF Mcap (BEUR) (FINAL) S) HK0000069689 B4TX8S1 1299.HK HK1013 AIA GROUP HK HKD Y 83.1 1 1 CNE1000002H1 B0LMTQ3 0939.HK CN0010 CHINA CONSTRUCTION BANK CORP H CN HKD Y 71.5 2 2 CNE1000003G1 B1G1QD8 1398.HK CN0021 ICBC H CN HKD Y 49.4 3 3 CNE1000003X6 B01FLR7 2318.HK CN0076 PING AN INSUR GP CO. OF CN 'H' CN HKD Y 42.9 4 4 HK0941009539 6073556 0941.HK 607355 China Mobile Ltd. CN HKD Y 41.6 5 5 CNE1000001Z5 B154564 3988.HK CN0032 BANK OF CHINA 'H' CN HKD Y 33.3 6 7 HK0388045442 6267359 0388.HK 626735 Hong Kong Exchanges & Clearing HK HKD Y 31.0 7 6 KYG217651051 BW9P816 0001.HK 619027 CK HUTCHISON HOLDINGS HK HKD Y 27.1 8 8 HK0016000132 6859927 0016.HK 685992 Sun Hung Kai Properties Ltd. HK HKD Y 20.2 9 10 HK0027032686 6465874 0027.HK 646587 GALAXY ENTERTAINMENT GP. HK HKD Y 20.1 10 11 HK0883013259 B00G0S5 0883.HK 617994 CNOOC Ltd. CN HKD Y 19.0 11 12 KYG2177B1014 BYZQ077 1113.HK HK50CI CK Asset Holdings Ltd HK HKD Y 18.8 12 9 HK0002007356 6097017 0002.HK 619091 CLP Holdings Ltd. HK HKD Y 18.3 13 13 CNE1000002Q2 6291819 0386.HK CN0098 China Petroleum & Chemical 'H' CN HKD Y 18.2 14 15 CNE1000002L3 6718976 2628.HK CN0043 China Life Insurance Co 'H' CN HKD Y 16.7 15 14 HK0823032773 B0PB4M7 0823.HK B0PB4M Link Real Estate Investment Tr HK HKD Y 15.1 16 16 HK2388011192 6536112 2388.HK 653611 BOC Hong Kong (Holdings) Ltd. -

Eligible Assets and Credit-To-Asset Ratio for Secured Credit

Eligible Assets and Credit-to-asset Ratio for Secured Credit Effective from 30 Sep 2021 List of Eligible Assets (Excluding Stocks) Asset Types Credit-to-asset Ratio HKD Time Deposits 100% Foreign Currency Time or Saving Deposits 85% Deposit Plus 70% Structured Investment Deposits (Including Capital Protected Investment Deposits) 70% Unit Trusts*/Bonds*#/Certificates of Deposit/Equity Link Notes/Equity Link Investment with Product Risk Level 1 70% Product Risk Level 2 70% Product Risk Level 3 50% Product Risk Level 4 30% Product Risk Level 5 – *exclude the Non-eligible Products listed below. #For new bonds issued on or after 17 Mar 2020, the timeline for assignment of Credit -to-asset Ratio for Secured Credit Facility will be revised follow: for new bonds issued between 1 Jan to 30 Jun each year, Credit-to-asset Ratio will be assigned in Sep of the same year (where applicable); for new bonds issued between 1 Jul to 31 Dec, Credit-to-asset Ratio will be assigned in Mar of next year (where applicable); Please refer to the relevant bond term sheet or the bond details in our website for the issue date of the relevant bond. Gold 0% (Credit-to-asset Ratio for Gold (Wayfoong Statement Gold) is removed from 20 Dec 2019) List of Non-eligible Products (Capital in Nature Instruments and Other TLAC-eligible Instruments, Hedge Funds, Liquid Alternative Funds are not eligible) Product Type Bond / Fund Code Bond / Fund Name Bonds US404280AN99 HSBC HOLDINGS PLC 4% USD BOND 3/30/2022 Bonds US404280AL34 HSBC HOLDINGS PLC 4.875% USD BOND 1/14/2022 Bonds -

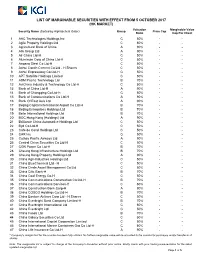

List of Marginable Securities with Effect from 5 October 2017 (Hk Market)

LIST OF MARGINABLE SECURITIES WITH EFFECT FROM 5 OCTOBER 2017 (HK MARKET) Valuation Marginable Value Security Name (Sorted by Alphabetical Order) Group Price Cap Ratio Cap Per Client 1 AAC Technologies Holdings Inc C 50% - - 2 Agile Property Holdings Ltd C 50% - - 3 Agricultural Bank of China A 90% - - 4 AIA Group Ltd A 90% - - 5 Air China Ltd-H C 50% - - 6 Aluminum Corp of China Ltd-H C 50% - - 7 Angang Steel Co Ltd-H C 50% - - 8 Anhui Conch Cement Co Ltd - H Shares C 50% - - 9 Anhui Expressway Co Ltd-H C 50% - - 10 APT Satellite Holdings Limited C 50% - - 11 ASM Pacific Technology Ltd B 70% - - 12 AviChina Industry & Technology Co Ltd-H C 50% - - 13 Bank of China Ltd-H A 90% - - 14 Bank of Chongqing Co Ltd-H C 50% - - 15 Bank of Communications Co Ltd-H A 90% - - 16 Bank Of East Asia Ltd A 90% - - 17 Beijing Capital International Airport Co Ltd-H B 70% - - 18 Beijing Enterprises Holdings Ltd B 70% - - 19 Belle International Holdings Ltd B 70% - - 20 BOC Hong Kong (Holdings) Ltd A 90% - - 21 Brilliance China Automotive Holdings Ltd C 50% - - 22 Byd Co Ltd-H C 50% - - 23 Cafe de Coral Holdings Ltd C 50% - - 24 CAR Inc C 50% - - 25 Cathay Pacific Airways Ltd A 90% - - 26 Central China Securities Co Ltd-H C 50% - - 27 CGN Power Co Ltd-H B 70% - - 28 Cheung Kong Infrastructure Holdings Ltd B 70% - - 29 Cheung Kong Property Holdings Ltd A 90% - - 30 China Agri-Industries Holdings Ltd C 50% - - 31 China BlueChemical Ltd - H C 50% - - 32 China Cinda Asset Management Co Ltd C 50% - - 33 China Citic Bank-H B 70% - - 34 China Coal Energy Co-H C -

Sinotrans Limited: Sinotrans – Negatives in the Price; Valuation

Sinotrans Limited | February 23, 2016 MORGAN STANLEY RESEARCH February 23, 2016 MORGAN STANLEY ASIA LIMITED+ Edward H Xu, CFA Sinotrans Limited [email protected] +852 2239-1521 Watson Lau Sinotrans – Negatives In The Price; [email protected] +852 2239-1523 Victoria Wong, CFA Valuation Support From Sinoair [email protected] +852 2239-7817 Yufei Wu Industry View Stock Rating Price Target [email protected] +852 2239-7505 In-Line Overweight HK$5.11 Sinotrans Limited ( 0598.HK, 598 HK ) While we lower our earnings expectations amid sustained macro Hong Kong/China Transportation & Infrastructure / China headwinds, we think the negatives have been priced in by a Stock Rating Overweight Industry View In-Line significant stock correction in the last 3 months. We expect valuation Price target HK$5.11 support from a potential re-rating of Sinoair, which we are Up/downside to price target (%) 59 Shr price, close (Feb 22, 2016) HK$3.21 upgrading to OW. 52-Week Range HK$6.65-2.68 Sh out, dil, curr (mn) 4,406 What's Changed? From: To: Mkt cap, curr (mn) Rmb11,862 EV, curr (mn) Rmb14,276 Sinotrans Limited Avg daily trading value (mn) HK$75 Price Target HK$7.99 HK$5.11 2015e Net Profit Rmb1,606m Rmb1,460m Fiscal Year Ending 12/14 12/15e 12/16e 12/17e 2016e Net Profit Rmb1,721m Rmb1,423m ModelWare EPS (Rmb) 0.26 0.33 0.34 0.39 2017e Net Profit Rmb1,927m Rmb1,735m Consensus EPS (Rmb)§ 0.28 0.31 0.34 0.38 Revenue, net (Rmb 45,863 45,567 45,285 46,892 What has caused the dip: We think the -33% stock performance in the past mn) EBITDA (Rmb mn) 2,604 3,249 3,287 3,574 52 weeks has fully reflected market disappointment caused by: 1) weaker- ModelWare net inc 1,150 1,454 1,518 1,716 than-expected organic business led by a macro downturn; 2) delay in asset (Rmb mn) injections without clarity; and 3) a lack of management incentives with delays P/E 15.8 10.6 7.8 6.9 P/BV 1.4 1.1 0.8 0.7 in SOE reform. -

Can Now Offer You Shipbuilding and Fleet Forecasting

POR 0002 13JO AN REV CONTAINERISATION INGLES 210x297MM.pdf 1 16/11/15 10:19 CONTENTS THE RANKINGS TOP LISTS 04 Introduction 26 Top 10 box port operators 08 Numbers 1-10 45 Top 50 beneficial owners 28 Numbers 11-20 60 Top 10 brokers 44 Numbers 21-30 61 Top 50 owners by country 57 Numbers 31-40 71 Top 50 flags 69 Numbers 41-50 72 Top 10 insurers 84 Numbers 51-60 79 Top 10 regulators 94 Numbers 61-70 104 Top 10 classification societies 101 Numbers 71-80 115 Top 10 ship finance 111 Numbers 81-90 119 Top 10 lawyers 120 Numbers 91-100 Top 100 Editor Chief executive Printing Lloyd’s List is available online in every country Nicola Good Michael Dell St Ives plc in the world by placing a subscription with the publishers in London, Informa UK Ltd. Please Lloyd’s List Managing Editor Head of Marketing Services Editoral, advertising and place your order with the Lloyd’s List marketing Richard Meade Fergus Gregory sponsorship inquiries team at Informa. This special supplement is Lloyd’s List, Christchurch Court, 10-15 Lloyd’s List Asia Editor-in-Chief Head of Sales – Marketing Services issued free to subscribers. Newgate Street, London, EC1A 7AZ Tom Leander David O’Neill Tel: +44 (0)20 7017 5000 For further information please email: Lloyd’s List Deputy Editor Marketing Services Sales Fax: +44 (0)20 7017 4782 [email protected] Craig Eason Janet Wood (Greece & Cyprus) Email: [email protected] or telephone: +44 (0)20 3377 3792 Linsey Dinesan-Rajan (The Americas) Lloyd’s Digital Content Manager Published by Informa UK Ltd. -

M&A in the Transport & Logistics Industry

M&A in the Transport & Logistics Industry January–December 2018 Highlights Results M&A activity 2018: strong first half- Analysis of M&A activity by sector Table of year, weak second half and investor type China: still acting locally, some Outlook for 2019 contents with a global vision Europe: Brexit with mixed Methodology repercussions Contacts 1 Highlights – Highlights M&A activity 2018: strong first half-year, weak second half: The first half-year of 2018 was a record period for the T&L industry in terms of deal value ($74.3 billion), while a slight slowdown in the number of deals (127) in comparison with previous half-years could be observed. However, in the second half of 2018 only 92 deals were announced, which is the lowest number in five years. The total deal value also nearly halved in comparison with the first half-year ($41.0 billion). Deal value is mainly driven by megadeals. Intense competition for target properties in combination with investment pressure, especially from institutional investors, has led to a surge in prices for fewer T&L deals in 2018 companies or equity interests in the area of infrastructure, railways and airlines, with the result that various 23% than the year before transactions were initially discontinued. Furthermore, global factors, such as uncertainty surrounding the China-US trade dispute – an example of increasing protectionism – weighed on both the logistics and the general transaction markets. Measured by the number of deals announced, 2018 showed a slowdown in deal activity across all industries, but the decline in T&L is particularly strong at –22.6% compared with 2017. -

中遠海運發展股份有限公司 COSCO SHIPPING Development Co., Ltd.*

THIS CIRCULAR IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION If you are in any doubt as to any aspect of this circular or as to the action to be taken, you should consult a licensed securities dealer and other registered institution in securities, bank manager, solicitor, professional accountant or other professional adviser. If you have sold or transferred all your shares in COSCO SHIPPING Development Co., Ltd., you should at once hand this circular, the form of proxy and reply slip to the purchaser or the transferee or to licensed securities dealer or registered institution in securities or other agent through whom the sale or transfer was effected for transmission to the purchaser or transferee. Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this circular, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this circular. 中遠海運發展股份有限公司 COSCO SHIPPING Development Co., Ltd.* (A joint stock limited company incorporated in the People’s Republic of China with limited liability) (Stock Code: 02866) (1) 2016 REPORT OF THE BOARD (2) 2016 REPORT OF THE SUPERVISORY COMMITTEE (3) 2016 WORK REPORT OF INDEPENDENT DIRECTORS (4) 2016 FINANCIAL STATEMENTS AND AUDITORS’ REPORT (5) 2016 ANNUAL REPORT (6) 2016 PROFIT DISTRIBUTION PLAN (7) REMUNERATION OF DIRECTORS AND SUPERVISORS FOR THE YEAR 2017 (8) RE-APPOINTMENT OF PRC AUDITOR, INTERNAL CONTROL AUDITOR AND INTERNATIONAL AUDITOR FOR THE YEAR 2017 (9) DISCLOSEABLE AND CONNECTED TRANSACTION – ASSIGNMENT AND NOVATION OF SHIPBUILDING CONTRACTS (10) CAPITAL CONTRIBUTION TO CHINA BOHAI BANK (11) PROVISIONS OF GUARANTEES AND (12) SUPPLEMENTAL NOTICE OF AGM Independent Financial Adviser to the Independent Board Committee and Independent Shareholders Capitalised terms used in this cover shall have the same meanings as those defined in this circular.