E.ON 2005 Annual Report on Form 20-F Entitled “Item 3

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Economics of the Nord Stream Pipeline System

The Economics of the Nord Stream Pipeline System Chi Kong Chyong, Pierre Noël and David M. Reiner September 2010 CWPE 1051 & EPRG 1026 The Economics of the Nord Stream Pipeline System EPRG Working Paper 1026 Cambridge Working Paper in Economics 1051 Chi Kong Chyong, Pierre Noёl and David M. Reiner Abstract We calculate the total cost of building Nord Stream and compare its levelised unit transportation cost with the existing options to transport Russian gas to western Europe. We find that the unit cost of shipping through Nord Stream is clearly lower than using the Ukrainian route and is only slightly above shipping through the Yamal-Europe pipeline. Using a large-scale gas simulation model we find a positive economic value for Nord Stream under various scenarios of demand for Russian gas in Europe. We disaggregate the value of Nord Stream into project economics (cost advantage), strategic value (impact on Ukraine’s transit fee) and security of supply value (insurance against disruption of the Ukrainian transit corridor). The economic fundamentals account for the bulk of Nord Stream’s positive value in all our scenarios. Keywords Nord Stream, Russia, Europe, Ukraine, Natural gas, Pipeline, Gazprom JEL Classification L95, H43, C63 Contact [email protected] Publication September 2010 EPRG WORKING PAPER Financial Support ESRC TSEC 3 www.eprg.group.cam.ac.uk The Economics of the Nord Stream Pipeline System1 Chi Kong Chyong* Electricity Policy Research Group (EPRG), Judge Business School, University of Cambridge (PhD Candidate) Pierre Noёl EPRG, Judge Business School, University of Cambridge David M. Reiner EPRG, Judge Business School, University of Cambridge 1. -

Germany - Regulatory Reform in Electricity, Gas, and Pharmacies 2004

Germany - Regulatory Reform in Electricity, Gas, and Pharmacies 2004 The Review is one of a series of country reports carried out under the OECD’s Regulatory Reform Programme, in response to the 1997 mandate by OECD Ministers. This report on regulatory reform in electricity, gas and pharmacies in Germany was principally prepared by Ms. Sally Van Siclen for the OECD. OECD REVIEWS OF REGULATORY REFORM REGULATORY REFORM IN GERMANY ELECTRICITY, GAS, AND PHARMACIES -- PART I -- ORGANISATION FOR ECONOMIC CO-OPERATION AND DEVELOPMENT © OECD (2004). All rights reserved. 1 ORGANISATION FOR ECONOMIC CO-OPERATION AND DEVELOPMENT Pursuant to Article 1 of the Convention signed in Paris on 14th December 1960, and which came into force on 30th September 1961, the Organisation for Economic Co-operation and Development (OECD) shall promote policies designed: • to achieve the highest sustainable economic growth and employment and a rising standard of living in Member countries, while maintaining financial stability, and thus to contribute to the development of the world economy; • to contribute to sound economic expansion in Member as well as non-member countries in the process of economic development; and • to contribute to the expansion of world trade on a multilateral, non-discriminatory basis in accordance with international obligations. The original Member countries of the OECD are Austria, Belgium, Canada, Denmark, France, Germany, Greece, Iceland, Ireland, Italy, Luxembourg, the Netherlands, Norway, Portugal, Spain, Sweden, Switzerland, Turkey, the United Kingdom and the United States. The following countries became Members subsequently through accession at the dates indicated hereafter: Japan (28th April 1964), Finland (28th January 1969), Australia (7th June 1971), New Zealand (29th May 1973), Mexico (18th May 1994), the Czech Republic (21st December 1995), Hungary (7th May 1996), Poland (22nd November 1996), Korea (12th December 1996) and the Slovak Republic (14th December 2000). -

Decentralized Energy Master Planning

Decentralized Energy Master Planning The London Borough of Brent An Interactive Qualifying Project Report submitted to the Faculty of WORCESTER POLYTECHNIC INSTITUTE in partial fulfilment of the requirements for the Degree of Bachelor of Science Submitted by Anthony Aldi Karen Anundson Andrew Bigelow Andrew Capulli Sponsoring Agency London Borough of Brent Planning Service Advisors Dominic Golding Ruth Smith Liaison Joyce Ip 29 April 2010 This report represents the work of four WPI undergraduate students submitted to the faculty as evidence of completion of a degree requirement. WPI routinely publishes these reports on its web site without editorial or peer review. Abstract The London Borough of Brent aims to reduce its carbon emissions via implementation of decentralized energy schemes including combined heat and power systems. The objective of this project was to aid Brent in the early stages of its decentralized energy master planning. By examining policies of other boroughs and studying major development areas within Brent, the WPI project team has concluded that the council must actively facilitate the development of decentralized energy systems through the use of existing practices and development of well supported policies. i Authorship Page This report was developed through a collaborative effort by the project team: Anthony Aldi, Karen Anundson, Andrew Bigelow, and Andrew Capulli. All sections were developed as team with each member contributing equally. ii Acknowledgements The team would like to thank our advisors from Worcester Polytechnic Institute, Professor Dominic Golding and Professor Ruth Smith. The team would also like to thank the liaison Joyce Ip from the London Borough of Brent Planning Service and the entire Planning Service. -

Modified UK National Implementation Measures for Phase III of the EU Emissions Trading System

Modified UK National Implementation Measures for Phase III of the EU Emissions Trading System As submitted to the European Commission in April 2012 following the first stage of their scrutiny process This document has been issued by the Department of Energy and Climate Change, together with the Devolved Administrations for Northern Ireland, Scotland and Wales. April 2012 UK’s National Implementation Measures submission – April 2012 Modified UK National Implementation Measures for Phase III of the EU Emissions Trading System As submitted to the European Commission in April 2012 following the first stage of their scrutiny process On 12 December 2011, the UK submitted to the European Commission the UK’s National Implementation Measures (NIMs), containing the preliminary levels of free allocation of allowances to installations under Phase III of the EU Emissions Trading System (2013-2020), in accordance with Article 11 of the revised ETS Directive (2009/29/EC). In response to queries raised by the European Commission during the first stage of their assessment of the UK’s NIMs, the UK has made a small number of modifications to its NIMs. This includes the introduction of preliminary levels of free allocation for four additional installations and amendments to the preliminary free allocation levels of seven installations that were included in the original NIMs submission. The operators of the installations affected have been informed directly of these changes. The allocations are not final at this stage as the Commission’s NIMs scrutiny process is ongoing. Only when all installation-level allocations for an EU Member State have been approved will that Member State’s NIMs and the preliminary levels of allocation be accepted. -

London Electricity Companies Had Already Supply Co

printed LONDON AREA POWER SUPPLY A Survey of London’s Electric Lighting and Powerbe Stations By M.A.C. Horne to - not Copyright M.A.C. Horne © 2012 (V3.0) London’s Power Supplies LONDON AREA POWER SUPPLY Background to break up streets and to raise money for electric lighting schemes. Ignoring a small number of experimental schemes that did not Alternatively the Board of Trade could authorise private companies to provide supplies to which the public might subscribe, the first station implement schemes and benefit from wayleave rights. They could that made electricity publicly available was the plant at the Grosvenor either do this by means of 7-year licences, with the support of the Art Gallery in New Bond Street early in 1883. The initial plant was local authority, or by means of a provisional order which required no temporary, provided from a large wooden hut next door, though a local authority consent. In either case the local authority had the right supply was soon made available to local shopkeepers. Demand soon to purchase the company concerned after 21 years (or at 7-year precipitated the building of permanent plant that was complete by intervals thereafter) and to regulate maximum prices. There was no December 1884. The boiler house was on the south side of the power to supply beyond local authority areas or to interconnect intervening passage called Bloomfield Street and was connected with systems. It is importantprinted to note that the act did not prevent the generating plant in the Gallery’s basement by means of an creation of supply companies which could generate and distribute underground passage. -

The Impact of Us Lng on Russian Natural Gas Export Policy

THE IMPACT OF US LNG ON RUSSIAN NATURAL GAS EXPORT POLICY BY TATIANA MITROVA AND TIM BOERSMA DECEMBER 2018 ABOUT THE CENTER ON GLOBAL ENERGY POLICY The Center on Global Energy Policy provides independent, balanced, data-driven analysis to help policymakers navigate the complex world of energy. We approach energy as an economic, security, and environmental concern. And we draw on the resources of a world- class institution, faculty with real-world experience, and a location in the world’s finance and media capital. Visit us at www.energypolicy.columbia.edu @ColumbiaUenergy ABOUT THE SCHOOL OF INTERNATIONAL AND PUBLIC AFFAIRS SIPA’s mission is to empower people to serve the global public interest. Our goal is to foster economic growth, sustainable development, social progress, and democratic governance by educating public policy professionals, producing policy-related research, and conveying the results to the world. Based in New York City, with a student body that is 50 percent international and educational partners in cities around the world, SIPA is the most global of public policy schools. For more information, please visit www.sipa.columbia.edu THE IMPACT OF US LNG ON RUSSIAN NATURAL GAS EXPORT POLICY BY TATIANA MITROVA AND TIM BOERSMA DECEMBER 2018 1255 Amsterdam Ave New York NY 10027 www.energypolicy.columbia.edu @ColumbiaUenergy THE IMPACT OF US LNG ON RUSSIAN NATURAL GAS EXPORT POLICY ACKNOWLEDGEMENTS For comments on earlier drafts of this paper and editorial guidance, the authors would like to thank Jason Bordoff, Jonathan Elkind, Anna Galkina, Matthew Robinson, Morena Skalamera, Rik Komduur, and Megan Burak. All remaining errors are the authors’ own. -

E.ON 2003 Annual Report

Financial Calendar 2003 Annual Report E.ON Group Financial Highlights in millions 2003 20021 +/– % Electricity sales volume (in billion kWh)2 387.6 333.6 +16 Gas sales volume (in billion kWh)2 803.7 721.3 +11 April 28, 2004 2004 Annual Shareholders Meeting Sales 46,364 36,624 +27 April 29, 2004 Dividend Payment EBITDA3 9,458 7,558 +25 EBIT3 6,228 4,649 +34 May 13, 2004 Interim Report: January–March 2004 Internal operating profit4 4,565 3,817 +20 Income/(loss) from continuing operations August 12, 2004 Interim Report: January–June 2004 before income taxes and minority interests 5,538 –759 – November 11, 2004 Interim Report: January–September 2004 Income/(loss) from continuing operations 3,950 –720 – Income/(loss) from discontinued operations 1,137 3,306 –66 March 10, 2005 Annual Press Conference, Net income 4,647 2,777 +67 Release of 2004 Annual Report Investments 9,196 24,159 –62 Cash provided by operating activities 5,538 3,614 +53 March 10, 2005 Annual Analysts Conference Stockholders’ equity 29,774 25,653 +16 Total assets 111,850 113,503 –1 April 27, 2005 2005 Annual Shareholders Meeting ROCE6 (in %) 9.9 9.2 +0.75 Cost of capital (in %) 9.5 9.5 – Return on equity after taxes7 (in %) 16.8 11.1 5.75 Employees at year end 66,549 101,336 –34 Earnings per share from (in ) on•top continuing operations 6.04 –1.10 – discontinued operations 1.74 5.07 –66 cumulative effect of changes in accounting principles, net –0.67 0.29 – net income 7.11 4.26 +67 2003 Annual Report Per share (in ) Dividend 2.00 1.75 +14 Stockholders’ equity8 45.39 39.33 +15 1Adjusted for discontinued operations (see commentary on pages 133–141). -

CASE AT.39767 – E.ON GAS ANTITRUST PROCEDURE Council Regulation

CASE AT.39767 – E.ON GAS (Only the English text is authentic) ANTITRUST PROCEDURE Council Regulation (EC) 1/2003 Article 9 Regulation (EC) 1/2003 Date: 26/07/2016 This text is made available for information purposes only. A summary of this decision is published in all EU languages in the Official Journal of the European Union. Parts of this text have been edited to ensure that confidential information is not disclosed. Those parts are replaced by a non-confidential summary in square brackets or are shown as […]. EN EN TABLE OF CONTENTS 1. Introduction ................................................................................................................... 3 2. Review of the Commitments on the Basis of Article 9(2) of Regulation No 1/2003 ... 5 3. Relevant market ............................................................................................................ 6 3.1. Gas wholesale markets .................................................................................................. 6 3.1.1. Relevant product market ............................................................................................... 6 3.1.2. Relevant geographic market ......................................................................................... 7 3.2. Gas retail market ........................................................................................................... 8 3.2.1. Relevant product market ............................................................................................... 8 3.2.2. Relevant geographic -

No. 208, Winter 2017 What Is the Future for Enfield Town? on 25Th September 2017, the Consultation Period Ended for the Draft Enfield Town Master Plan

Enfield Society News No. 208, Winter 2017 What is the future for Enfield Town? On 25th September 2017, the consultation period ended for the draft Enfield Town Master Plan. The plan was summarised in the Autumn newsletter and is an advisory document designed to provide a framework for future developments. The Society’s Architecture and Planning Group gave careful consideration to the plan, holding a joint meeting with the Enfield Town Conservation Area Study Three adjacent empty shop units in Enfield Church Street Group and meeting the planning officers involved in the masterplan preparation. The idea of a bridge linking the Tesco should review how market places operate The Plan states that Enfield Town Centre site with the Town Centre is strongly in other towns. now needs to respond to a series of supported because this could be an We noted that the plan does not make challenges and opportunities in order to attractive landscaped feature. reference to any significant consultation successfully define its future. In general terms the lack of any proposals with the Palace Gardens and Palace for community use – schools, childcare, Exchange shopping centres. The number These include: health facilities, sheltered housing etc. – of empty units along Church Street ● A series of site development opportunities, is noted and regretted. If more residential continues to cause serious concern. Some which need a coordinated response to development is encouraged, supporting of these units need considerable control the form, quality and density of community infrastructure is essential. modernisation and yet landlords continue new development. The Society has reviewed the various to charge very high rents. -

Nord Stream: Not Just a Pipeline

FNI Report 15/2008 Nord Stream: Not Just a Pipeline An analysis of the political debates in the Baltic Sea region regarding the planned gas pipeline from Russia to Germany Bendik Solum Whist Nord Stream: Not Just a Pipeline An analysis of the political debates in the Baltic Sea Region regarding the planned gas pipeline from Russia to Germany Bendik Solum Whist [email protected] November 2008 Copyright © Fridtjof Nansen Institute 2008 Title: Nord Stream: Not Just a Pipeline. An analysis of the political debates in the Baltic Sea region regarding the planned gas pipeline from Russia to Germany Publication Type and Number Pages FNI Report 15/2008 79 Author ISBN Bendik Solum Whist 978-82-7613-546-6-print version 978-82-7613-547-3-online version Project ISSN 1504-9744 Abstract This report is an analysis of the planned gas pipeline from Russia to Germany through the Baltic Sea known as Nord Stream. Although not yet realised, the project has, since its birth, been the subject of harsh criticism and opposition by a significant number of states that consider themselves affected by the pipeline. Whereas the Baltic States and Poland have interpreted the pipeline as a political- ly motivated strategy that will increase Russia’s leverage on them and threaten their energy security, the debate in Sweden was at first mostly concerned with the prospect of increased Russian military presence in the Swedish Exclusive Economic Zone. The potential environmental impact of the pipeline has been, and continues to be, an overarching concern shared by all the littoral states of the Baltic Sea. -

TEI Times May 2019

THE ENERGY INDUSTRY May 2019 • Volume 12 • No 3 • Published monthly • ISSN 1757-7365 www.teitimes.com TIMES Sleepless nights? Getting closer Final Word Energy storage and digitalisation are Europe’s Clean Energy Package We live in a rebellious two areas that are keeping energy should bring markets closer together climate, says Junior Isles. executives awake at night. but some of its provisions need further Page 16 Page 13 clarification. Page 14 News In Brief Wind to become “truly global market” in five years National Plans The Global Wind Energy Council forecasts that 300 GW of new wind capacity will be added globally by 2024. Page 2 will not deliver Opportunity Zones offer tax breaks A tax break offered to investors in so-called ‘Opportunity Zones’ may provide extra capital for renewable energy developers in the USA renewables as other support mechanisms are phased out. Page 4 Coal still part of balanced energy mix target The Philippines still sees coal as an important part of its future energy mix, as developers continue to outline plans for future coal fired WindEurope’s Giles Dickson says none of the power plants. plans properly spell out policy measures Page 6 Ofgem addresses supplier The EU has concluded negotiations on its Clean Energy Package but recent research shows that rules A series of company collapses in the National Plans might not deliver the previously agreed 32 per cent renewables target. Junior Isles UK’s energy retail sector has forced Europe’s draft National Energy and this. But none of the Plans properly simplifying rules on planning and per- Another issue the Plans need to ad- the regulator to revise the rules for Climate Plans are insufficient to de- spell out the policy measures by which mitting, such as common sense re- dress is how to get more renewables new entrants. -

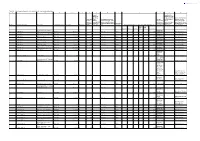

Table A.1 - List of Combustion Plants to Be Included in the Transitional National Plan a B C D E F G H I J K L M

Table A.1 - List of combustion plants to be included in the transitional national plan A B C D E F G H I J K L M Annual Quantity of S in number of indigenous solid operating fuels used which Conversion factor(s) Total rated hours Pollutant(s) (SO2, NOx, Average was introduced used in case the thermal (ANOH); dust) for which the plant annual waste into the waste gas flow rate input on (average 2001- concerned is NOT covered gas flow rate combustion plan was calculated from 31/12/2010 2010 if less by the transitional national Gas turbine (average 2001- (avergae 2001- the fuel input (per fuel Number Operating Company Plant name Location (Postcode) 1st permit Extension (MWth) than 1500) plan or engine Annual amount of fuel used (average 2001-2010) (TJ/year) 2010) (Nm³/y) 2010) (tpa) type) (Nm³/GJ) other solid liquid hard coal lignite biomass fuels fuels gaseous fuels Kemsley CHP – GT & WHRB Natural Gas: 1 E.ON UK Plc A/B ME10 2TD 23-mars-95 nr 348 nr SO2; Dust Turbine 0 0 0 0 0 7482 6299837158 nr Natural Gas: 842; Kemsley CHP – Package boilers Natural Gas: 2 E.ON UK Plc D-F 2 ME10 2TD 23-mars-95 nr 74 nr nr nr 0 0 0 0 0 81 22724094 nr Natural Gas: 279 Natural Gas: 3 E.ON UK Plc Killingholme GT 22 DN40 3LU 14-nov-91 nr 445 nr SO2; Dust Turbine 0 0 0 0 0 4724 3977321358 nr Natural Gas: 842; Natural Gas: 4 E.ON UK Plc Killingholme GT 21 DN40 3LU 14-nov-91 nr 445 nr SO2; Dust Turbine 0 0 0 0 0 4914 4137193588 nr Natural Gas: 842; Natural Gas: 5 E.ON UK Plc Killingholme GT 12 DN40 3LU 14-nov-91 nr 445 nr SO2; Dust Turbine 0 0 0 0 0 5128 4317570970