Insights by Repucom 3

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

List of Available Videos

Artist Concert 3 Doors Down Live at the Download Festival 3 Doors Down Live At The Tabernacle 2014 30 Odd Foot Of Grunts Live at Soundstage 30 Seconds To Mars Live At Download Festival 2013 5 Seconds of Summer How Did We End Up Here? 6ft Hick Notes from the Underground A House Live on Stage A Thousand Horses Real Live Performances ABBA Arrival: The Ultimate Critical Review ABBA The Gold Singles Above And Beyond Acoustic AC/DC AC/DC - No Bull AC/DC In Performance AC/DC Live At River Plate\t AC/DC Live at the Circus Krone Acid Angels 101 A Concert - Band in Seattle Acid Angels And Big Sur 101 Episode - Band in Seattle Adam Jensen Live at Kiss FM Boston Adam Lambert Glam Nation Live Aerosmith Rock for the Rising Sun Aerosmith Videobiography After The Fire Live at the Greenbelt Against Me! Live at the Key Club: West Hollywood Aiden From Hell with Love Air Eating Sleeping Waiting and Playing Air Supply Air Supply Live in Toronto Air Supply Live in Hong Kong Akhenaton Live Aux Docks Des Sud Al Green Everything's Going To Be Alright Alabama and Friends Live at the Ryman Alain Souchon J'veux Du Live Part 2 Alanis Morissette Guitar Center Sessions Alanis Morissette Live at Montreux 2012 Alanis Morissette Live at Soundstage Albert Collins Live at Montreux Alberta Cross Live At The ATO Cabin Alejandro Fernández Confidencias Reales Alejandro Sanz El Alma al Aire en Concierto Ali Campbell Live at the Shepherds Bush Empire Alice Cooper AVO Session Alice Cooper Brutally Live Alice Cooper Good To See You Again Alice Cooper Live at Montreux Alice Cooper -

Tour Link Conference

JANUARY 2016 // ISSUE 1 Tour Link Magazine 1 officer, Eric Stuart, as he explained the mathematics involved in determining crowd size, and why num- Event Safety Alliance Event Safety bers alone are insufficient to predicting and prevent- Summit 2015 Recap ing potential issues. We applauded Professor Emma Story by Shelby Cude, Photos by Nicholas Karlin Parkinson of Bucks New University in the UK, as she explained near-miss and accident reporting in the This past December, industry professionals from all development of an effective safety culture, challeng- over the globe gathered in Lititz, Pennsylvania for ing the industry’s taboo that “the show must go on.” Closing out the Summit, Jim Digby left the group the 2nd Annual Event Safety Summit, hosted by The with a single, powerful statement – that true leaders Event Safety Alliance. Checking their competitive empower others to do the right thing. For those that agendas at the door, nearly 200 attendees repre- presented and participated in the 2015 Event Safety senting every inch of the event industry sat under the Summit, Tour Link thanks you for taking the initiative massive roof of rehearsal venue Rock Lititz to en- to actively promote life safety first. gage in three days of discussion on issues related to safety at live events. From crowd management tac- University Meteorologist, Kevin Kloesel, of the Okla- tics, to safe pyrotechnics practices, to severe weather homa University Office of Emergency Prepared- plans, to current and future technical standards, an ness demonstrated how little we understand when elite group of presenters took the stage to share their it comes to “predicting” the weather and strategies expertise, and issued a call to action to improve the for evacuating outdoor events in case of emergency. -

ANDERTON Music Festival Capitalism

1 Music Festival Capitalism Chris Anderton Abstract: This chapter adds to a growing subfield of music festival studies by examining the business practices and cultures of the commercial outdoor sector, with a particular focus on rock, pop and dance music events. The events of this sector require substantial financial and other capital in order to be staged and achieve success, yet the market is highly volatile, with relatively few festivals managing to attain longevity. It is argued that these events must balance their commercial needs with the socio-cultural expectations of their audiences for hedonistic, carnivalesque experiences that draw on countercultural understanding of festival culture (the countercultural carnivalesque). This balancing act has come into increased focus as corporate promoters, brand sponsors and venture capitalists have sought to dominate the market in the neoliberal era of late capitalism. The chapter examines the riskiness and volatility of the sector before examining contemporary economic strategies for risk management and audience development, and critiques of these corporatizing and mainstreaming processes. Keywords: music festival; carnivalesque; counterculture; risk management; cool capitalism A popular music festival may be defined as a live event consisting of multiple musical performances, held over one or more days (Shuker, 2017, 131), though the connotations of 2 the word “festival” extend much further than this, as I will discuss below. For the purposes of this chapter, “popular music” is conceived as music that is produced by contemporary artists, has commercial appeal, and does not rely on public subsidies to exist, hence typically ranges from rock and pop through to rap and electronic dance music, but excludes most classical music and opera (Connolly and Krueger 2006, 667). -

Open'er Festival

SHORTLISTED NOMINEES FOR THE EUROPEAN FESTIVAL AWARDS 2019 UNVEILED GET YOUR TICKET NOW With the 11th edition of the European Festival Awards set to take place on January 15th in Groningen, The Netherlands, we’re announcing the shortlists for 14 of the ceremony’s categories. Over 350’000 votes have been cast for the 2019 European Festival Awards in the main public categories. We’d like to extend a huge thank you to all of those who applied, voted, and otherwise participated in the Awards this year. Tickets for the Award Ceremony at De Oosterpoort in Groningen, The Netherlands are already going fast. There are two different ticket options: Premium tickets are priced at €100, and include: • Access to the cocktail hour with drinks from 06.00pm – 06.45pm • Three-course sit down Dinner with drinks at 07.00pm – 09.00pm • A seat at a table at the EFA awards show at 09.30pm – 11.15pm • Access to the after-show party at 00.00am – 02.00am – Venue TBD Tribune tickets are priced at €30 and include access to the EFA awards show at 09.30pm – 11.15pm (no meal or extras included). Buy Tickets Now without further ado, here are the shortlists: The Brand Activation Award Presented by: EMAC Lowlands (The Netherlands) & Rabobank (Brasserie 2050) Open’er Festival (Poland) & Netflix (Stranger Things) Øya Festivalen (Norway) & Fortum (The Green Rider) Sziget Festival (Hungary) & IBIS (IBIS Music) Untold (Romania) & KFC (Haunted Camping) We Love Green (France) & Back Market (Back Market x We Love Green Circular) European Festival Awards, c/o YOUROPE, Heiligkreuzstr. -

Download Mp3 Roar Katy Perry Free

Download mp3 roar katy perry free CLICK TO DOWNLOAD Download MP3 and Video For: Katy Perry - Roar (Official). Katy Perry - Roar (Official) Song Download - Listen Katy Perry - Roar (Official) MP3 songs online free. Play Shape of You album song MP3 by Katy Perry - Roar (Official). Aug 12, · Roar MP3 Song by Katy Perry from the album Roar. Download Roar song on renuzap.podarokideal.ru and listen Roar Roar song offline. Read about Roar mp3 (Free Download) by Katy Perry and see the artwork, lyrics and similar artists. Read about Katy Perry Roar mp3 Free Download-[Mp3 Download] by and see the artwork, lyrics and similar artists. Katy Perry - California Gurls ft. Snoop renuzap.podarokideal.ru3 download M Katy Perry - Chained To The Rhythm ft. Skip renuzap.podarokideal.ru3 download. Tags: Free Download Katy Perry - Roar mp3 Song, Listen Online Katy Perry - Roar Mp3 Track, Download Roar - Katy Perry Mp3 Song, Roar Full Audio Song Download, Katy Perry - Roar Mp3 Music Download, Katy Perry - Roar iTune Rip Song. Posted by Unknown at Email This BlogThis! Roar, Katy Perry I used to bite my tongue and hold my breath Scared to rock the boat and make | Tải download nhạc chờ Roar,Katy Perry. Zing MP3 vô cùng xin lỗi bạn vì sự cố đăng nhập xảy ra cách đây vài ngày đã ảnh hưởng đến trải nghiệm nghe nhạc của bạn trên website Zing MP3. Waptrick Katy Perry Mp3 Music. Download Free Katy Perry Mp3 Songs @ renuzap.podarokideal.ru Katy Perry Songs: Waptrick Katy Perry - Roar, free Katy Perry feat Migos - Bon Appetit, download Katy Perry - Firework, listen Katy Perry Ft Juicy J - Dark Horse, mp3 Katy Perry - Unconditionally, music mp3 Katy Perry - Love Me, mp3 download Katy Perry - By The Grace Of God, song Katy Perry - Never . -

Green Events & Innovations Conference 2019

GREEN EVENTS & INNOVATIONS CONFERENCE 2019 Tuesday 5th March 2019 Royal Garden Hotel, Kensington High St, London, W8 4PT GREEN EVENTS & INNOVATIONS CONFERENCE 2019 CONTENTS Welcome ..............................................................................................................................................................4 Schedule ..............................................................................................................................................................5 Agenda .................................................................................................................................................................6 AGF Juicy Stats ................................................................................................................................................12 Delegates ..........................................................................................................................................................16 International AGF Awards Shortlist ........................................................................................................21 Feature: Campsite waste ............................................................................................................................22 Note paper ........................................................................................................................................................26 Welcome to the eleventh edition of the Green Events & Innovations conference (GEI11), presented -

Section a Concept and Management

Section A Concept and Management 01-Raj-Ch-01-Section A.indd 1 24/01/2013 5:33:02 PM 01-Raj-Ch-01-Section A.indd 2 24/01/2013 5:33:02 PM Introduction to Events 1 Management In this chapter you will cover: x the historical development of events; x technical definitions of events management; x size of events within the sector; x an events industry; x value of areas of the events industry; x different types of events; x local authorities’ events strategies; x corporate events strategies; x community festivals; x charity events; x summary; x discussion questions; x case studies; x further reading. This chapter provides an historical overview of the events and festivals industry, and how it has developed over time. The core theme for this chapter is to establish a dialogue between event managers and event spe- cialists who need to have a consistent working relationship. Each strand of the chapter will be linked to industry best practice where appropriate. In addition, this chapter discusses the different types of events that exist within the events management industry. Specifically, the chapter will analyse and discuss a range of events and their implications for the events industry, including the creation of opportunities for community orientated events and festivals. 01-Raj-Ch-01-Section A.indd 3 24/01/2013 5:33:02 PM 4 SECTION A: CONCEPT AND MANAGEMENT The historical development of events Events, in the form of organised acts and performances, have their origins in ancient history. Events and festivals are well documented in the historical period before the fall of the Western Roman Empire (AD 476). -

Music Reading Read the Passage, the E-Mail and the Festival Guide. the Glastonbury Festival Is an Unforgettable Sight. for Three

Music Reading Read the passage, the e-mail and the festival guide. The Glastonbury Festival is an unforgettable sight. For three days, 280 hectares of peaceful farm country in the beautiful Somerset Valley become a vast, colourful tent city. The Glastonbury Festival is Britain's largest outdoor rock concert, and it attracts crowds of more than 100,000 people. It has six separate stages for musicians to play on. It has eighteen markets where fans can buy things. It has its own daily newspaper and is even broadcast live on television. It also raises large amounts of money for several charities, including Greenpeace and the Campaign for Nuclear Disarmament. Glastonbury is just one of many events on the international music festival calendar each year. For dance music fans, there's Creamfields, the Essential Festival and Homelands - all in the UK. Rock fans have Roskilde Festival in Denmark, Fuji Rock and Summer Sonic in Japan, and the Livid Festival and the Big Day Out in Australia. And the crowds just keep getting bigger. In fact, the size of some of these festivals is causing problems. Since the deaths of nine people at Roskiide in 2000 and the death of a young woman at the 2001 Big Day Out, festival organisers and local police have been working together to make sure festival-goers stay safe. Despite these tragic events, festivals are more popular than ever. And it's not just about the music. It's about making new friends and partying non-stop for days at a time. It's about dancing till you can't stand up anymore and then crashing in someone else's tent. -

Press Release – Launch of the Destination Contract

A new, creative, cultural, artistic and festive tourism offer from a bigger Paris www.exploreparis.com e-store launch #ExploreParis | PRESENTATION 3 Discover Greater Paris: a more generous tourism offer for original experiences Paris, the ultimate city break destination, is not simply a city centre. An abundance of cultural, artistic and festive offers on both sides of the ring road attract young tourists searching for something different. The aim is not only to develop the destination's image but also to increase Greater Paris has decided to boost and develop its tourism flows from the centre of Paris to tourism offer to meet young Europeans’ expectations the Capital's suburban districts and towns and gain their long-term loyalty. The comprehensive, - easily accessible by public transport - dynamic and creative offer is based on themes such and to promote these areas and their as street art, architecture, modern art, nature, tourist attractions. cosmopolitan Paris, and party-time Paris. A wide choice of venues, excursions and tours, often unknown The finalised offer has been launched in the to tourists, are available across the city. This new www.exploreparis.com e-store, both in French tourism scope also includes main attractions such and in English. Tourists can choose from a wide as the Royal Basilica of Saint-Denis, the Château choice of Greater Paris experiences to discover the de Vincennes and the Albert Kahn Museum. area and meet residents: tours, walks, workshops, cruises and parties, etc. Just like Berlin, London, Barcelona and Amsterdam, Greater Paris promises both exciting experiences in off-the-beaten-track venues and original encounters for a revamped tourism experience. -

Living Blues 2021 Festival Guide

Compiled by Melanie Young Specific dates are provided where possible. However, some festivals had not set their 2021 dates at press time. Due to COVID-19, some dates are tentative. Please contact the festivals directly for the latest information. You can also view this list year-round at www.LivingBlues.com. Living Blues Festival Guide ALABAMA Foley BBQ & Blues Cook-Off March 13, 2021 Blues, Bikes & BBQ Festival Juneau Jazz & Classics Heritage Park TBA TBA Foley, Alabama Alabama International Dragway Juneau, Alaska 251.943.5590 2021Steele, Alabama 907.463.3378 www.foleybbqandblues.net www.bluesbikesbbqfestival.eventbrite.com jazzandclassics.org W.C. Handy Music Festival Johnny Shines Blues Festival Spenard Jazz Fest July 16-27, 2021 TBA TBA Florence, Alabama McAbee Activity Center Anchorage, Alaska 256.766.7642 Tuscaloosa, Alabama spenardjazzfest.org wchandymusicfestival.com 205.887.6859 23rd Annual Gulf Coast Ethnic & Heritage Jazz Black Belt Folk Roots Festival ARIZONA Festival TBA Chandler Jazz Festival July 30-August 1, 2021 Historic Greene County Courthouse Square Mobile, Alabama April 8-10, 2021 Eutaw, Alabama Chandler, Arizona 251.478.4027 205.372.0525 gcehjazzfest.org 480.782.2000 blackbeltfolkrootsfestival.weebly.com chandleraz.gov/special-events Spring Fling Cruise 2021 Alabama Blues Week October 3-10, 2021 Woodystock Blues Festival TBA May 8-9, 2021 Carnival Glory Cruise from New Orleans, Louisiana Tuscaloosa, Alabama to Montego Bay, Jamaica, Grand Cayman Islands, Davis Camp Park 205.752.6263 Bullhead City, Arizona and Cozumel, -

Participation and Formation in Europe

4th issue May-October 2009 PROEUROPE1 1 4th issue May-October 2009 Index 4 WHAT IS PROEUROPE1? 5 PARTICIPATION AND FORMATION IN EUROPE ● Participate in the Hemispheres project 7 WORK AND COOPERATE IN EUROPE ● Working in the European Parliament 12 DISCOVERINGS Seinajoki‟s Finnish city Schwedt, Germany city 18 CULTURAL EUROPE ● The house of word 21 EUROCALENDAR ● Look for all the funny, exotic and special festivals, traditions and festivities all over Europe 33 WE BUILD EUROPE ● The clash of “civilizations”or the intercultural dialogue? 37 YOU TALK ● European Youth Parliament of Macedonia and PROEUROPE1 2 4th issue May-October 2009 training of Hemispheres project 40 A LOOK AT THE WORLD ●The artistic and cultural Morelia PROEUROPE1 3 4th issue May-October 2009 We build Europe In the new magazine‟s issue Proeurope1 we have a new section for you. The section, we build Europe, conduced by Martina Braggion, informs to youths about decrees, treaties, agreements, finally, about policies being carried out at European level. As a European citizens, that all of us, we must Know events are held. Despite the doubts that we have about the usefulness of the EU and we are missing of European identity, all affects us, the Bolonya Process, the crisis, etc. Europe is the future. Is important young people can build it, but just we can do it, if we know well their social, cultural and political issues, if we want to be active youths and we participate in the spaces that we have, one of them is the European Parliament elections, next June; Europe is the culmination of the diversity and progress. -

Canal Convergence Events

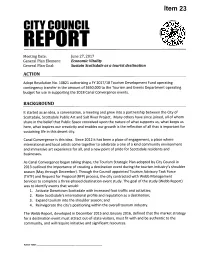

Item 23 CITY COUNCIl REPORT Meeting Date: June 27, 2017 General Plan Element: Economic Vitality General Plan Goal: Sustain Scottsdale as a tourist destination ACTION Adopt Resolution No. 10821 authorizing a FY 2017/18 Tourism Development Fund operating contingency transfer in the amount of $650,000 to the Tourism and Events Department operating budget for use in supporting the 2018 Canal Convergence events. BACKGROUND It started as an idea, a conversation, a meeting and grew into a partnership between the City of Scottsdale, Scottsdale Public Art and Salt River Project. Many others have since joined, all of whom share in the belief that Public Space conceived upon the nature of what supports us, what keeps us here, what inspires our creativity and enables our growth is the reflection of all that is important for sustaining life in this desert city. Canal Convergence is this idea. Since 2012 it has been a place of engagement, a place where international and local artists come together to celebrate a one of a kind community environment and immersive art experience for all, and a new point of pride for Scottsdale residents and businesses. As Canal Convergence began taking shape, the Tourism Strategic Plan adopted by City Council in 2013 outlined the importance of creating a destination event during the tourism industry's shoulder season (May through December). Through the Council appointed Tourism Advisory Task Force (TATF) and Request for Proposal (RFP) process, the city contracted with Webb Management Services to complete a three-phased destination event study. The goal of the study (Webb Report) was to identify events that would: 1.