FY18 Investment Advisory Committee Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Preqin Research Report Fig

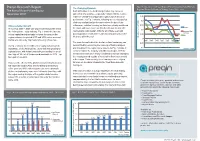

Preqin Research Report Fig. 3 Comparison of Private Equity Performance by Fund Primary The Changing Dynamic Regional Focus for Funds of Vintage Years 1995 - 2007 The Rise of Asian Private Equity Such diffi culties in the fundraising market may come as November 2010 somewhat of a surprise – especially considering the relative resilience of Asia-focused private equity funds in terms of 0.25 performance. As Fig. 3 shows, following an extended period 0.2 of strong median fund performance since the turn of the Unprecedented Growth millennium, vehicles focusing on Asia have clearly weathered 0.15 the storm with more success than their European and US Europe The period 2003 – 2008 saw unprecedented growth within 0.1 the Asian private equity industry. Fig. 1 shows the increase counterparts, with median IRRs for all vintage years still Asia and Rest of World posting positive results while funds focusing primarily on the 0.05 in total capital raised annually by funds focusing on the US region between the period 2003 and 2008, when a record West are still in the red. IRR Median Net-to-LP 0 $91bn was raised by 194 funds achieving a fi nal close. 1995 1997 1999 2001 2003 2005 2007 The main factors behind the decline in Asia fundraising can -0.05 As Fig. 2 shows, the record level of capital raised saw the be identifi ed by examining the make-up of fund managers -0.1 Vintage Year importance of the Asian private equity industry growing on and investors in the region more closely. As Fig. -

ANNUAL REVIEW 2017 Land of the Giants Cycle-Tested Credit Expertise Extensive Market Coverage Comprehensive Solutions Relative Value Focus

ANNUAL REVIEW 2017 Land of the giants Cycle-Tested Credit Expertise Extensive Market Coverage Comprehensive Solutions Relative Value Focus Ares Management is honored to be recognized as Lender of the Year in North America for the fourth consecutive year as well as Lender of the Year in Europe Lender of the year in Europe Ares Management, L.P. (NYSE: ARES) is a leading global alternative asset manager with approximately $106 billion of AUM1 and offices throughout the United States, Europe, Asia and Australia. With more than $70 billion in AUM1 and approximately 235 investment professionals, the Ares Credit Group is one of the largest global alternative credit managers across the non-investment grade credit universe. Ares is also one of the largest direct lenders to the U.S. and European middle markets, operating out of twelve office locations in both geographies. Note: As of December 31, 2017. The performance, awards/ratings noted herein may relate only to selected funds/strategies and may not be representative of any client’s given experience and should not be viewed as indicative of Ares’ past performance or its funds’ future performance. 1. AUM amounts include funds managed by Ivy Hill Asset Management, L.P., a wholly owned portfolio company of Ares Capital Corporation and a registered investment adviser. learn more at: www.aresmgmt.com | www.arescapitalcorp.com The battle of the brands the US market on page 80, advisor Hamilton TOBY MITCHENALL Lane said it had received a record number EDITOR'S of private placement memoranda in 2017 – ISSN 1474–8800 LETTER MARCH 2018 around 800 – and that this, combined with Senior Editor, Private Equity faster fundraising processes, has made it dif- Toby Mitchenall, Tel: +44 207 566 5447 [email protected] ficult to some investors to make considered Special Projects Editor decisions. -

PEI June2020 PEI300.Pdf

Cover story 20 Private Equity International • June 2020 Cover story Better capitalised than ever Page 22 The Top 10 over the decade Page 24 A decade that changed PE Page 27 LPs share dealmaking burden Page 28 Testing the value creation story Page 30 Investing responsibly Page 32 The state of private credit Page 34 Industry sweet spots Page 36 A liquid asset class Page 38 The PEI 300 by the numbers Page 40 June 2020 • Private Equity International 21 Cover story An industry better capitalised than ever With almost $2trn raised between them in the last five years, this year’s PEI 300 are armed and ready for the post-coronavirus rebuild, writes Isobel Markham nnual fundraising mega-funds ahead of the competition. crisis it’s better to be backed by a pri- figures go some way And Blackstone isn’t the only firm to vate equity firm, particularly and to towards painting a up the ante. The top 10 is around $30 the extent that it is able and prepared picture of just how billion larger than last year’s, the top to support these companies, which of much capital is in the 50 has broken the $1 trillion mark for course we are,” he says. hands of private equi- the first time, and the entire PEI 300 “The businesses that we own at Aty managers, but the ebbs and flows of has amassed $1.988 trillion. That’s the Blackstone that are directly affected the fundraising cycle often leave that same as Italy’s GDP. Firms now need by the pandemic, [such as] Merlin, picture incomplete. -

Market Insight – October 2019

SYDNEY MELBOURNE Level 15 Level 9 60 Castlereagh Street 41 Exhibition Street SYDNEY NSW 2000 MELBOURNE VIC 3000 Tel 61 2 9235 9400 Tel 61 3 9653 8600 Market Insight – October 2019 “Movers & Shakers” INVESTMENT & CORPORATE BANKING Investment Banking • Hein Vogel has departed Investec where he was Head of Emerging Companies & Financial Services. • Duncan Hogg who was Managing Director, Investment Banking at BAML has joined EY as a Partner in Sydney. • Steven Boggiano has joined Allier Capital as Managing Director. Steven previously founded Magnes Capital and was also Managing Director & Head of Healthcare, Consumer, Retail & Real Estate at Barclays. • Anna Ellis previously Investment Director with Besen in Melbourne, has also joined EY as Director, PE & Deal Origination, Transaction Advisory Services. • Grant Mansell has joined Investec as Director, Corporate Advisory. He has prior experience as Director, M&A with HSBC. Pierre Josset also joins Investec’s Corporate Advisory team, he was previously an Associate with Aura Group. • Nomura has hired Srihari Sharma as a Senior Associate, FIG from Investec, Ben St Claire as an Associate from Blackpeak Capital and Henry Ball, ex EY as an Investment Banking Analyst, Consumer, Retail & Healthcare. • Benjamin Gribble has joined Houlihan Lokey as an Associate, he was previously with Moelis Australia as an Investment Banking Associate & Houlihan Lokey in London. • Nicholas Tregoning joined Moelis Australia as Senior Analyst, Investment Banking, Nicholas joins from Shaw & Partners. • Gigi Li has joined Ironstone Capital as an Analyst from KPMG. • Samantha Riegel (ex FTI Consulting) & Ice Tan & have joined Highbury Partnership as Analysts. • Macquarie Capital has hired Anthony Yao, ex Lazard, as an Analyst in the General Industrials teams, Rita Dalton joins as an Analyst in the TMET team from Nomura & James Watkins ex Flagstaff Partners Analyst joins the firm’s resources team. -

VENTURA COUNTY EMPLOYEES' RETIREMENT ASSOCIATION BOARD of RETIREMENT BUSINESS MEETING May 19, 2014 AGENDA

VENTURA COUNTY EMPLOYEES’ RETIREMENT ASSOCIATION BOARD OF RETIREMENT BUSINESS MEETING May 19, 2014 AGENDA PLACE: Ventura County Employees' Retirement Association Second Floor Boardroom 1190 South Victoria Avenue Ventura, CA 93003 TIME: 9:00 a.m. ITEM: I. CALL TO ORDER Master Page No. II. APPROVAL OF AGENDA 1 – 4 III. APPROVAL OF MINUTES A. Disability Meeting of May 5, 2014. 5 – 13 IV. CONSENT AGENDA A. Approve Regular and Deferred Retirements and 14 – 15 Survivors Continuances for the Month of April 2014. B. Receive and File Report of Checks Disbursed in April 16 – 25 2014. C. Receive and File Budget Summary for FY 2013-14 26 Month Ending April 2014. D. Receive and File Statements of Fiduciary Net Position, 27 – 38 Statements of Changes in Fiduciary Net Position, Investments & Cash Equivalents, and Schedules of Investment Management Fees for the Periods Ending March 31, 2014, and April 30, 2014. MASTER PAGE NO. 1 BOARD OF RETIREMENT May 19, 2014 AGENDA BUSINESS MEETING PAGE 2 V. STANDING ITEM A. Receive an Oral Update on Pensionable Compensation and PEPRA. VI. ANNUAL INVESTMENT PRESENTATIONS A. Receive Annual Investment Presentation, Bridgewater 39 – 91 Associates LP, Joel Whidden, Senior Relationship Manager, and David Greely, Senior Research Associate (30 Minutes). B. Receive Annual Investment Presentation, Tortoise 92 – 117 Capital Advisors LLC, Ken Malvey, Managing Director, and Andy Goldsmith, Head of Institutional Sales and Consultant Relations (30 Minutes). VII. INVESTMENT INFORMATION A. NEPC – Don Stracke, Senior Consultant, Chris Hill, Research Consultant. 1. Receive and File Performance Report Month 118 – 124 Ending April 30, 2014. 2. Receive and File Investment Summary – Quarter 125 – 176 Ending March 31, 2014. -

NYSCRF Monthly Transacation Report December 2017

THOMAS P. DiNAPOLI 110 STATE STREET STATE COMPTROLLER ALBANY, NEW YORK 12236 STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER NEW YORK STATE COMMON RETIREMENT FUND Thomas P. DiNapoli New York State Comptroller MONTHLY TRANSACTION REPORT December 2017 Global Equity The New York State Common Retirement Fund (CRF) invests with external managers to meet its global equity allocation. This report will include additions and terminations of external managers or addition or removal of assets from an existing manager. The Channing Capital Management Domestic Equity account was funded with an additional $227 million in December 2017. The account was funded from cash. No placement agents were involved in this transaction. The Brown Capital Management Domestic Equity account was reduced by $300 million in December 2017 and allocated to cash. No placement agents were involved in this transaction. Private Equity CRF invests in private equity partnerships directly and through separately managed accounts. Significant activity includes new commitments to private equity partnerships, as well as new commitments made through separately managed accounts. Affinity Equity Partners – Affinity Asia Pacific Fund V, L. P. - $350 million commitment. Affinity will make investments across a diverse mix of industries within Asia, focusing on 4 regions; Korea, Australia/New Zealand, Southeast Asia and China. The funding of capital calls will come from cash. Affinity is an existing relationship for the CRF. No placement agents were involved in this transaction. This investment closed on December 15, 2017. New York State Common Retirement Fund Monthly Transaction Report December 2017 Page 2 DCP Capital I, L. P. – through Asia Alternatives IV, L. -

Investment Fees for the Fiscal Year Ended June 30, 2018 Transparency of the Montana Investment Expenses

Investment Fees For the Fiscal Year Ended June 30, 2018 Transparency of the Montana Investment Expenses The Montana Board of Investment’s Investment Fees Report is a breakdown of the Investment Fees section of the Unified Investment Program (UIP) Financial Statements. The Investment Fees Report is unaudited and may be subject to change. Board expenses are allocated and segmented using an activity-based budgeting process that incorporates time estimates, functional investment activities and cost centers that can change over time. Custodial bank fees are contractual based on holdings, transactions and other pre-defined variables such as the number of active accounts. Custody expenses are allocated across the various investment pools based on holdings, transactions, or a direct charge. Contractual fees for external managers are aggregated at the parent company level across all partnerships and investment accounts. Additional information can be found at www.investmentmt.com Montana Board of Investments | June 30, 2018 | 2 Table of Contents FY2018 Investment Fees from UIP Financial Statements 4 Consolidated Asset Pension Pool (CAPP) 5 Trust Funds Investment Pool (TFIP) 8 Short Term Investment Pool (STIP) 9 Separately Managed Investments (SMI) 10 End Notes 11 Montana Board of Investments | June 30, 2018 | 3 Total Fiscal Year 2018 Investment Fees (in thousands) Custodial External Pool and SMI Board Bank Managers Total Consolidated Asset Pension Pool (CAPP) $ 3 ,730 $ 1 ,249 $ 4 7,834 $ 5 2,813 Trust Funds Investment Pool (TFIP) 331 126 1,648 -

Monthly M&A Insider January 2015 – HY Edition

HALF-YEAR EDITION A MERGERMARKET REPORT ON GLOBAL M&A ACTIVITY MONTHLY M&A INSIDER JANUARY 2015 INSIDE: GLOBAL OVERVIEW LATIN AMERICA NORTH AMERICA ASIA-PACIFIC EUROPE MIDDLE EAST & AFRICA ABOUT MERRILL CORPORATION & MERRILL DATASITE MERRILL CORPORATION CONTACTS Monthly M&A Insider | October GLOBAL OVERVIEW The buzzword for 2014 – revival – was played out throughout the entire year and ended with a bang. M&A not only revisited pre-crisis levels, but actually surpassed previous heights in terms of the total number of global transactions. In 2014, there were 16,588 deals worth roughly US$3.2tn. Before that, 2007 was the high-water mark with 16,060 transactions worth about US$3.7tn. There were many factors that propelled the M&A market to Exit fever these hyper elevated levels of dealmaking. There is, of course, the improving economy that gave CEOs the confidence to execute Private equity exits also had an unparalleled year as both the acquisitions. On top of this, companies had at their disposal, volume and value of these deals topped prior records. Last year cash piles they accumulated throughout the crisis. Interest rates there were 2,099 transactions worth US$489.6bn, surpassing remained low and cheap financing was readily available. the previous high in 2007 of 1,794 deals worth US$403bn. Large-cap deals also made a strong comeback in several Last year, private equity firms found effective exit strategies that industries including the Pharmaceutical, Medical & Biotech would allow them to pursue new growth areas. Many of the firms sector. In fact, for most of the year, the list of mega issues that were selling their portfolio companies had been holding on included high-profile pharmaceutical deals, so-called corporate to these assets since prior to the crisis, the period from 2006 to inversions. -

Affinity Equity Partners Makes S$200 Million Investment Into M-DAQ

Affinity Equity Partners makes S$200 million investment into M-DAQ M-DAQ’s Series D round anchored by Affinity Equity Partners, to support M-DAQ’s global expansion and creation of new FinTech ecosystem SINGAPORE, August 11, 2021 – Affinity Equity Partners (“Affinity”), one of the largest dedicated Asian private equity firms, made a substantial investment of ~S$200 million into M-DAQ Pte Ltd (“M-DAQ”). This is M-DAQ’s Series D round of fundraising, and sees Affinity join an esteemed list of international strategic and financial investors such as Ant Group, EDBI, NTT Communications, Samsung and Kiwoom-Shinhan as investors and business partners of M-DAQ. M-DAQ, founded and headquartered in Singapore, is one of the top FinTech enterprise SaaS companies, focusing on providing specialiZed technology-enabled financial services to enterprise customers and other downstream FinTechs. M-DAQ’s proprietary FX solutions process over S$10 billion in cross border transactions annually, primarily catering to the world’s largest eCommerce and technology companies including the two leading eCommerce players in China. M-DAQ’s sharp growth in recent years comes on the back of macro tailwinds from rapid growth in cross-border eCommerce globally. M-DAQ’s Founder and CEO Richard Koh was the recipient of the 2018 SCS Entrepreneur of the Year award and 2020 EY Entrepreneur of the Year (FinTech) award, while M-DAQ was a recipient of the Inaugural Singapore MAS FinTech Award (2016), Inaugural SG:D Techblazer Gold Award (2018), SCS Best Tech Company to Work For - biennial award (2019) and the inaugural Enterprise 50 Digital Economy Award (2019) to recogniZe the next potential unicorn. -

This Edition of the 2016 PEI 300 Updates the Version Originally Published

This edition of the 2016 PEI 300 updates the version originally published. The new world order For the first time in the history of the PEI 300 one firm has eclipsed the rest. By Marine Cole, Isobel Markham and Toby Mitchenall Private equity is a long-term business. Our [Blackstone has] Schwarzman described the firm as annual ranking of the most significant man- the platform having a culture of “innovation with safety”. agers of private equity funds has historically “We continue to quickly launch and scale reflected this; the five-year time horizon we to go to huge new products, leveraging our talent, knowl- use to calculate each manager’s firepower investors and say, ‘Just edge and brand in order to take immediate means that shifts in the upper reaches of give us your money and advantage of market opportunity,” he said the league table have been gradual. Until in January. now. we will invest it wherever One of the best illustrations of this agil- This year’s winner takes the crown for the opportunities are’ ity is the Tactical Opportunities platform, the first time since Private Equity Interna- led by senior managing director David tional began ranking private equity firms Blitzer, which launched three years ago. in 2007 in what was then the PEI 50, and It had already raised $15 billion for the takes it in spectacular fashion, with a including $30 billion for private equity strategy by the end of 2015. five-year fundraising total outstripping across several vehicles, including its colos- But Blackstone is not the only firm that its closest rival by a mind-bending $25 sal $18 billion Blackstone Capital Partners has had an impressive year. -

GESCHÄFTSBERICHT 2007 ANNUAL REPORT 2007 Pearl 2007.Qxp:Pearl 2005 18.3.2008 11:18 Uhr Seite 2

Pearl_2007.qxp:Pearl_2005 18.3.2008 11:18 Uhr Seite 1 GESCHÄFTSBERICHT 2007 ANNUAL REPORT 2007 Pearl_2007.qxp:Pearl_2005 18.3.2008 11:18 Uhr Seite 2 JAHRESBERICHT 2007 WERTENTWICKLUNG 2007 PERFORMANCE 2007 MITTELKURS- UND NAV-ENTWICKLUNG MID-MARKET PRICE AND NAV DEVELOPMENT 140% 130% 120% 110% 100% 90% 80% 70% 31.12.00 31.03.01 30.06.01 30.09.01 31.12.01 31.03.02 30.06.02 30.09.02 31.12.02 31.03.03 30.06.03 30.09.03 31.12.03 31.03.04 30.06.04 30.09.04 31.12.04 31.03.05 30.06.05 30.09.05 31.12.05 31.03.06 30.06.06 30.09.06 31.12.06 31.03.07 30.06.07 30.09.07 31.12.07 NAV – NAV NAV inkl. ausgeschüttetem und aufgelaufenem Zins – NAV incl. accrued and paid-out coupon Mittelkurs – Mid-market price 2 Pearl_2007.qxp:Pearl_2005 18.3.2008 11:18 Uhr Seite 3 ANNUAL REPORT 2007 Firmenprofil Company profile Pearl Holding Limited («Pearl») ist eine Private Equity- Pearl Holding Limited (“Pearl”) is a Guernsey-registered pri- Investmentgesellschaft mit Sitz in Guernsey. Die von der vate equity investment company. Pearl Holding’s convert- Pearl Holding emittierte Wandelanleihe eröffnet sowohl ible bond enables institutional and private investors to par- institutionellen als auch privaten Investoren die ticipate in a professionally managed, broadly diversified Möglichkeit, an einem professionell betreuten und breit portfolio of investments in private equity partnerships, list- diversifizierten Portfolio aus Beteiligungen an Private ed private equity vehicles and direct investments. -

Private Equity Spotlight

Welcome to the latest edition of Private Equity Spotlight, the Private Equity Spotlight monthly newsletter from Preqin providing insights into private equity June 2015 performance, investors, deals and fundraising. Private Equity Spotlight combines information from our online products Performance Analyst, Investor Intelligence, Fund Manager Feature Article Profi les, Funds in Market, Secondary Market Monitor, Buyout Deals Analyst Performance of Sector-Specifi c vs. Generalist Buyout Funds and Venture Deals Analyst. Returns offered by the private equity asset class are often a hot topic for discussion in the investment industry. With yields varying between fund types, sectors and managers active June 2015 within different industries, we investigate the differences in performance of sector-specifi c Volume 11 - Issue 5 buyout funds and buyout funds that are diversifi ed in their investment approach. Page 3 FEATURED PUBLICATION: Lead Article 2015 Preqin Investor Network Top 10 Fund Managers by Strategy Global Alternatives Report We compile league tables of the top 10 fund managers by strategy to take a closer look at which GPs have raised the most capital and which have the most available to invest. Page 7 2015 Preqin Investor Network Global Alternatives Report Preqin Industry News We take a closer look into Preqin’s interim and fi nal close data in the private equity industry, as well as large and mega buyout fundraising and buyout deal activity over the past month. Page 11 978-1-907012-83-9 $175 / £95 / €115 www.preqin.com alternative assets. intelligent data. More from Preqin: New Private Equity Research To find out more, download sample pages or to obtain your See what’s new from Preqin this month in the fi eld of private equity research.