ANNUAL REVIEW 2017 Land of the Giants Cycle-Tested Credit Expertise Extensive Market Coverage Comprehensive Solutions Relative Value Focus

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

PUBLIC NOTICE Federal Communications Commission 445 12Th St., S.W

PUBLIC NOTICE Federal Communications Commission 445 12th St., S.W. News Media Information 202 / 418-0500 Internet: https://www.fcc.gov Washington, D.C. 20554 TTY: 1-888-835-5322 DA 19-275 Released: April 10, 2019 MEDIA BUREAU ESTABLISHES PLEADING CYCLE FOR APPLICATIONS TO TRANSFER CONTROL OF NBI HOLDINGS, LLC, AND COX ENTERPRISES, INC., TO TERRIER MEDIA BUYER, INC., AND PERMIT-BUT-DISCLOSE EX PARTE STATUS FOR THE PROCEEDING MB Docket No. 19-98 Petition to Deny Date: May 10, 2019 Opposition Date: May 28, 2019 Reply Date: June 4, 2019 On March 4, 2019, Terrier Media Buyer, Inc. (Terrier Media), NBI Holdings, LLC (Northwest), and Cox Enterprises, Inc. (Cox) (jointly, the Applicants) filed applications with the Federal Communications Commission (Commission) seeking consent to the transfer of control of Commission licenses through two separate transactions.1 First, Terrier Media and Northwest seek consent for Terrier Media to acquire companies owned by Northwest holding the licenses of full-power broadcast television stations, low-power television stations, and TV translator stations (the Northwest Applications). Next, Terrier Media and Cox seek consent for Terrier Media to acquire companies owned by Cox holding the licenses of full-power broadcast television stations, low-power television stations, TV translator stations, and radio stations (the Cox Applications and, jointly with the NBI Applications, the Applications).2 Pursuant to a Purchase Agreement between Terrier Media and the equity holders of Northwest dated February 14, 2019, Terrier Media would acquire 100% of the interest in Northwest.3 Pursuant to a separate Purchase Agreement between Terrier Media and Cox and affiliates of Cox, Terrier Media would acquire the companies owning all of Cox’s television stations and the licenses and other assets of four of Cox’s radio stations.4 The Applicants propose that Terrier Media, which is a newly created company, will become the 100% indirect parent of the licensees listed in the Attachment. -

Apollo Global Management Appoints Tetsuji Okamoto to Head Private Equity Business in Japan

Apollo Global Management Appoints Tetsuji Okamoto to Head Private Equity Business in Japan NEW YORK, NY – December 5, 2019 – Apollo Global Management, Inc. (NYSE: APO) (together with its consolidated subsidiaries, “Apollo”) today announced the appointment of Tetsuji Okamoto as a Partner, Head of Japan, leading Apollo Private Equity’s efforts in Japan. Mr. Okamoto will play a lead role in building Apollo’s Private Equity business in Japan, including originating and executing deals and identifying cross-platform opportunities. He will report to Steve Martinez, Senior Partner, Head of Asia Pacific, and will begin in this newly created role on December 9, 2019. “This appointment and the new role we’ve created is a reflection of the importance we place on Japan and the opportunities we see in the wider region for growth and diversification,” Apollo’s Co-Presidents, Scott Kleinman and James Zelter said in a joint statement. “Tetsuji’s addition signals Apollo’s meaningful long-term commitment to expanding its presence in the Japanese market, which we view as a key area of investment focus as we seek to build value and drive growth for Japanese corporations and our investors and limited partners,” Mr. Martinez added. Mr. Okamoto, 39, brings more than 17 years of industry experience to the Apollo platform and the Private Equity investing team. Most recently, Mr. Okamoto was a Managing Director at Bain Capital, where he was a member of the Asia Pacific Private Equity team for eleven years, responsible for overseeing execution processes for new deals and existing portfolio companies in Japan. At Bain Capital he was also a leader on the Capital Markets team covering Asia. -

How Will Financial Services Private Equity Investments Fare in the Next Recession?

How Will Financial Services Private Equity Investments Fare in the Next Recession? Leading funds are shifting to balance-sheet-light and countercyclical investments. By Tim Cochrane, Justin Miller, Michael Cashman and Mike Smith Tim Cochrane, Justin Miller, Michael Cashman and Mike Smith are partners with Bain & Company’s Financial Services and Private Equity practices. They are based, respectively, in London, New York, Boston and London. Copyright © 2019 Bain & Company, Inc. All rights reserved. How Will Financial Services Private Equity Investments Fare in the Next Recession? At a Glance Financial services deals in private equity have grown on the back of strong returns, including a pooled multiple on invested capital of 2.2x in recent years, higher than all but healthcare and technology deals. With a recession increasingly likely during the next holding period, PE funds need to develop plans to weather any storm and potentially improve their competitive position during and after the downturn. Many leading funds are investing in balance-sheet-light assets enabled by technology and regulatory change. Diligences now should test target companies under stressful economic scenarios and lay out a detailed value-creation plan, including how to mobilize quickly after acquisition. Financial services deals by private equity funds have had a strong run over the past few years, with deal value increasing significantly in Europe and the US(see Figure 1). Returns have been strong as well. Global financial services deals realized a pooled multiple on invested capital of 2.2x from 2009 through 2015, higher than all but healthcare and technology deals (see Figure 2). -

2016 Cross-Border M&A Conference

2016 CROSS-BORDER M&A CONFERENCE Investment, Digitization and Globalization in Times of Disruption DATE Tuesday, September 20, 2016 TIME 9.00 am - 4.00 pm CEST VENUE Hotel Bayerischer Hof, Munich Co-sponsored by Media Partners In partnership with 2016 CROSS-BORDER M&A CONFERENCE Investment, Digitization and Globalization in Times of Disruption US/Europe and Asia/Europe Cross-Border M&A and Activist Shareholders McDermott Will & Emery’s Munich M&A Conference In contrast with 2015, Q1of 2016 was considerably slow- (MuMAC) is celebrating its 6th year. We are looking forward er. M&A activity by deal volume globally was down by 24 to welcoming significant M&A market participants, strategic per cent this year, compared to Q1 of 2015. In the private and private equity investors, and individuals from the advi- equity market, buy-outs were down by 15.3 per cent and sory world to take part in discussions on topics relating to exits by 29.7 per cent over the same period. Was this as a cross-border M&A. result of the markets preparing for the uncertainty surround- ing the United Kingdom’s Brexit Referendum, or a sign of We would very much like to thank in advance our key note something wider? speaker Callum Mitchell-Thomson, Head of Investment Banking Germany for J.P. Morgan Chase & Co., and the MuMAC 2016 is the best place to get answers from experts. many speakers participating in the panel discussions. Come and join us. MuMAC 2016 will cover topics of major significance to the cross-border M&A markets, including regional investment trends in Europe, both from and into Asia and the United States. -

Takeovers + Schemes Review

TAKEOVERS + SCHEMES REVIEW 2018 GTLAW.COM.AU 1 THE GILBERT + TOBIN 2018 TAKEOVERS AND SCHEMES REVIEW 2017 demonstrated a distinct uptick in activity for Australian public company mergers and acquisitions. Some key themes were: + The number of transactions announced increased by 37% over 2016 and aggregate transaction values were among the highest in recent years. + The energy & resources sector staged a recovery in M&A activity, perhaps signalling an end to the downwards trend observed over the last six years. The real estate sector made the greatest contribution to overall transaction value, followed closely by utilities/infrastructure. + Despite perceived foreign investment headwinds, foreign interest in Australian assets remained strong, with Asian, North American and French acquirers featuring prominently. Four of the five largest transactions in 2017 (including two valued at over $5 billion) involved a foreign bidder. + There was a material decline in success rates, except for high value deals greater than $500 million. Cash transactions continued to be more successful than transactions offering scrip. Average premiums paid fell slightly. + Regulators continue to closely scrutinise public M&A transactions, with the attendant lengthening of deal timetables. This Review examines 2017’s public company transactions valued over $50 million and provides our perspective on the trends for Australian M&A in 2017 and what that might mean for 2018. We trust you will find this Review to be an interesting read and a useful resource for 2018. 2 -

Private Equity in Sweden

PRIVATE EQUITY IN SWEDEN An analysis of the private equity industry in Sweden and two case studies on individual companies’ competitive strategy JOHAN MATTISSON MASTER THESIS LUND UNIVERSITY, 2017 Abstract Private equity is a growing global phenomena and private equity companies have become a major force in many of Sweden’s industries. These companies own portfolio companies which together employs around 190 000 people and have an annual revenue of over 318 billion SEK. The purpose of this thesis was to describe and analyze the Swedish private equity industry and individual companies’ competitive strategy to increase value of portfolio companies and to attract capital. The methodical approach of this thesis was qualitative and abductive. Only public data was used bar the two interviews that was conducted with the case companies. The theoretical framework for the industry analysis was Porters five forces. The case companies were analyzed on the corporate, business and operational levels of strategy. A resource based view was used to further analyze the case companies’ strategic capabilities. The main findings from the industry analysis was that the vast majority of investors in Swedish private equity funds are made by professional institutions and a large amount of the investments were of international origin. The large pool of investors makes it easier for Swedish private equity companies to attract capital. The number of new private equity funds have been declining since 2007 but at the same time the average fund size has grown. There are many differentiating factors between private equity companies. This differentiation is beneficial for the private equity companies as they become less commoditized from the viewpoint of an investor. -

Southeast Asia

Asia’s Private Equity News Source avcj.com December 04 2012 Volume 25 Number 46 Ed itor’s VieWpoint German manufacturing might meets Chinese M&A ambition Page 3 neWs Carlyle, CDH, China Life, CITIC Capital, GPIF, Hamilton Lane, IDFC, IFC, L Capital, Lombard, MBK, Multiples, Oaktree, OPIC, Saratoga, Valar Page 5 a rsia aWa Ds Interviews with all the winners: Bain, CVC, Morgan Stanley, Qiming, Morningside, Navis, PAG, Helion, Inter-Asia Page 11 f ocus New beginnings? Secondaries: Do LPs sell fund positions in secret? VCs say cleantech is a viable investment option in a subsidy-free world Page 9 Page 22 Deal of the Week Deal of the Week At your convenience Welcome, traveler Morgan Stanley in China retail carve-out Page 23 Abraaj rides Thai medical tourism boom Page 23 Anything is possible... There are many barriers to liquidity in private equity: complexity, transaction size, deadlines, disparate assets, confidentiality, alignment, tax, shareholder sensitivities – the list goes on. But with creativity, experience and determination ... anything is possible. Secondaries Firm of the Year for the 8th consecutive year www.collercapital.com London New York Hong Kong 33 Cavendish Square 950 Third Avenue 20 Pedder Street London New York Hong Kong Liquidity solutions for private equity investors worldwide Contact: [email protected] Desert Ad_A4.indd 1 26/11/2012 15:43 Ed itor’s VieWpoint [email protected] Managing Editor Tim Burroughs (852) 3411 4909 Senior Editor Brian McLeod (1) 604 215 1416 Staff Writer Alvina Yuen (852) 3411 4907 Andrew Woodman (852) 3411 4852 Teutonic Creative Director Dicky Tang Designers Catherine Chau, Edith Leung, Mansfield Hor, Tony Chow Senior Research Manager Helen Lee Research Manager ambitions Alfred Lam Research Associates Kaho Mak, Jason Chong Circulation Manager Sally Yip Another week, Another Chinese There is clearly a role for private equity to play Circulation Administrator strategic acquisition of a German manufacturing in bringing investors and investees together, Prudence Lau asset. -

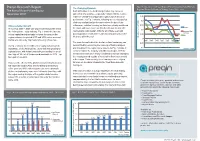

Preqin Research Report Fig

Preqin Research Report Fig. 3 Comparison of Private Equity Performance by Fund Primary The Changing Dynamic Regional Focus for Funds of Vintage Years 1995 - 2007 The Rise of Asian Private Equity Such diffi culties in the fundraising market may come as November 2010 somewhat of a surprise – especially considering the relative resilience of Asia-focused private equity funds in terms of 0.25 performance. As Fig. 3 shows, following an extended period 0.2 of strong median fund performance since the turn of the Unprecedented Growth millennium, vehicles focusing on Asia have clearly weathered 0.15 the storm with more success than their European and US Europe The period 2003 – 2008 saw unprecedented growth within 0.1 the Asian private equity industry. Fig. 1 shows the increase counterparts, with median IRRs for all vintage years still Asia and Rest of World posting positive results while funds focusing primarily on the 0.05 in total capital raised annually by funds focusing on the US region between the period 2003 and 2008, when a record West are still in the red. IRR Median Net-to-LP 0 $91bn was raised by 194 funds achieving a fi nal close. 1995 1997 1999 2001 2003 2005 2007 The main factors behind the decline in Asia fundraising can -0.05 As Fig. 2 shows, the record level of capital raised saw the be identifi ed by examining the make-up of fund managers -0.1 Vintage Year importance of the Asian private equity industry growing on and investors in the region more closely. As Fig. -

TRS Contracted Investment Managers

TRS INVESTMENT RELATIONSHIPS AS OF DECEMBER 2020 Global Public Equity (Global Income continued) Acadian Asset Management NXT Capital Management AQR Capital Management Oaktree Capital Management Arrowstreet Capital Pacific Investment Management Company Axiom International Investors Pemberton Capital Advisors Dimensional Fund Advisors PGIM Emerald Advisers Proterra Investment Partners Grandeur Peak Global Advisors Riverstone Credit Partners JP Morgan Asset Management Solar Capital Partners LSV Asset Management Taplin, Canida & Habacht/BMO Northern Trust Investments Taurus Funds Management RhumbLine Advisers TCW Asset Management Company Strategic Global Advisors TerraCotta T. Rowe Price Associates Varde Partners Wasatch Advisors Real Assets Transition Managers Barings Real Estate Advisers The Blackstone Group Citigroup Global Markets Brookfield Asset Management Loop Capital The Carlyle Group Macquarie Capital CB Richard Ellis Northern Trust Investments Dyal Capital Penserra Exeter Property Group Fortress Investment Group Global Income Gaw Capital Partners AllianceBernstein Heitman Real Estate Investment Management Apollo Global Management INVESCO Real Estate Beach Point Capital Management LaSalle Investment Management Blantyre Capital Ltd. Lion Industrial Trust Cerberus Capital Management Lone Star Dignari Capital Partners LPC Realty Advisors Dolan McEniry Capital Management Macquarie Group Limited DoubleLine Capital Madison International Realty Edelweiss Niam Franklin Advisers Oak Street Real Estate Capital Garcia Hamilton & Associates -

People Purpose Performance

ANNUAL REPORT 2013 People Purpose Performance Toronto London Hong Kong Corporate Profile Canada Pension Plan Investment Board (CPPIB) is a professional investment management organization with a critical purpose – to help provide a foundation on which Canadians build financial security in retirement. We invest the assets of the Canada Pension Plan (CPP) not currently needed to pay pension, disability and survivor benefits. — CPPIB is headquartered in Toronto with offices in London and Hong Kong. We invest in public equities, private equities, bonds, private debt, real estate, infrastructure and other areas. Assets currently total $183.3 billion. Of this total, 36.7% or $67.4 billion is invested in Canada and the rest globally at 63.3% or $116.1 billion of the portfolio. Our investments have become increasingly international as we diversify risk and seek growth opportunities in growing global markets. Created by an Act of Parliament in 1997, CPPIB is accountable to Parliament and to the federal and provincial finance ministers who serve as the CPP’s stewards. However, we are governed and managed independently from the CPP, operating at arm’s length from governments with a singular objective: to maximize returns without undue risk of loss. The funds that we invest belong to the 18 million Canadians who are current and future CPP beneficiaries. We adhere to high standards of transparency and accountability. The CPP Fund ranks among the world’s 10 largest retirement funds. In managing the Fund, CPPIB pursues a diverse set of investment programs that contribute to the long-term sustainability of the CPP. The most recent triennial report by the Chief Actuary of Canada indicated that the CPP is sustainable over a 75-year projection period, and that contributions to the Fund will exceed benefits paid until 2021. -

Kathmandu Holdings Limited

66 Kathmandu Holdings Limited Independent Adviser’s Report On the full takeover offer by Briscoe Group Limited July 2015 Grant Samuel confirms that it: §. has no conflict of interest that could affect its ability to provide an unbiased report; and §. has no direct or indirect pecuniary or other interest in the Briscoe Group Offer considered in this report, including any success or contingency fee or remuneration, other than to receive the cash fee for providing this report. Grant Samuel has satisfied the Takeovers Panel, on the basis of the material provided to the Panel, that it is independent under the Takeovers Code for the purposes of preparing this report. LEVEL 31, VERO CENTRE, 48 SHORTLAND STREET, PO BOX 4306, AUCKLAND 1140 T: +64 9 912 7777 F: +64 9 912 7788 WWW.GRANTSAMUEL.CO.NZ KATHMANDU TARGET COMPANY STATEMENT 67 Table of Contents Glossary 69 1. Terms of the Full Takeover Offer from Briscoe 70 1.1 Background 70 1.2 Details of the Briscoe Offer 70 1.3 Requirements of the Takeovers Code 71 2. Scope of the Report 72 2.1 Purpose of the Report 72 2.2 Basis of Evaluation 72 2.3 Approach to Valuation 72 3. Profile of Kathmandu 74 3.1 History and Background 74 3.2 Operations 75 3.3 Markets and Competitors 77 3.4 Growth Strategies 80 3.5 Financial Performance 81 3.6 Country Results 84 3.7 Financial Position 87 3.8 Cash Flows 88 3.9 Capital Structure and Ownership 89 3.10 Share Price Performance 90 4. -

Avcal Members

ANNUAL REPORT 2018 AVCAL.COM.AU CONTENTS INTRODUCTION 03 AVCAL MEMBERS 04 AVCAL BOARD OF DIRECTORS 05 CHAIRMAN & DEPUTY CHAIRMAN’S MESSAGE 07 CHIEF EXECUTIVE’S MESSAGE 11 AVCAL AT A GLANCE 13 POLICY & ADVOCACY 14 AVCAL MEDIA COVERAGE 20 RESEARCH PUBLICATIONS 21 DIVERSITY & INCLUSION 22 INDUSTRY AWARDS 23 AVCAL IN THE COMMUNITY 24 INDUSTRY EVENTS 28 STAKEHOLDER ENGAGEMENT 32 CODE OF CONDUCT 34 COMMITTEES & WORKING GROUPS 35 BUILDING CONCISE FINANCIAL REPORT 37 BETTER BUSINESSES OUR STRATEGIC PILLARS POLICY & ADVOCACY CONNECTED COMMUNITY INVESTOR ENGAGEMENT THE AUSTRALIAN PRIVATE EQUITY INTRODUCTION AVCAL’s members comprise most of the active private AND VENTURE CAPITAL ASSOCIATION equity and venture capital firms in Australia, as well LIMITED (AVCAL) IS A NATIONAL as the institutional investors into the industry. These ASSOCIATION WHICH REPRESENTS THE firms provide capital for early stage companies, later stage expansion capital, and capital for management PRIVATE EQUITY AND VENTURE CAPITAL buyouts of established companies. INVESTMENT INDUSTRY. AVCAL MEMBERS BUILD BETTER BUSINESSES The investment model used by the private equity and venture capital industry supports the building of stronger businesses that can deliver sustainable increases in enterprise value over the long-term. AVCAL’S CORE OBJECTIVE To ensure the business community and other key stakeholders understand the benefits of the private capital model of business ownership, and the role it can play in contributing to investment and employment growth across the Australian economy.