Market Insight – October 2019

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Krause Fund Research Spring 2020

Krause Fund Research Spring 2020 The Carlyle Group (CG) April 14, 2020 Stock Rating HOLD Financial Services – Alternative Asset Management Analyst Target Price $25 - 27 Justin Koress Krause Fund DCF Model $27 [email protected] Relative P/E Ratio (EPS20) $21 Relative P/B Ratio $25 Investment Thesis Price Data Current Stock Price $22.68 We recommend a HOLD rating for The Carlyle Group because of its diversified 52Wk RanGe $15.21 - $34.98 investments within key drivers in the Asset Management industry, such as Key Statistics corporate private equity, with an emphasis to capitalize on the ESG investment Market Cap (B) $7.90 trend. However, CG’s use of leverage will expose them to extreme risks associated Shares OutstandinG (M) 348.23 with COVID-19. Five Year Beta 1.77 Current Dividend Yield 4.17% Drivers of Thesis Price/EarninGs (TTM) 8.04x Price/EarninGs (FY1) 13.98x • With private capital dry powder at a record $2.3 trillion dollars, Profitability alternative managers will be able to create high-quality investments at Profit MarGin 35.07% distressed valuations in response to COVID-19. Return on Equity (TTM) 39.88% Return on Assets (TTM) 17.15% • CGs management team has a proven track record in locating Debt to Equity Ratio 365.01% companies that weather economic downturns, providing tremendous investment opportunities in a destabilized market. 25.00 • The alternative asset management business is intensely competitive, with competition based on a variety of factors, including investment 20.00 performance, a record number of private investment funds, and lack of 19.00 20.28 investor liquidity due to COVID-19. -

Preqin Research Report Fig

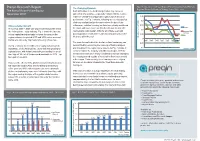

Preqin Research Report Fig. 3 Comparison of Private Equity Performance by Fund Primary The Changing Dynamic Regional Focus for Funds of Vintage Years 1995 - 2007 The Rise of Asian Private Equity Such diffi culties in the fundraising market may come as November 2010 somewhat of a surprise – especially considering the relative resilience of Asia-focused private equity funds in terms of 0.25 performance. As Fig. 3 shows, following an extended period 0.2 of strong median fund performance since the turn of the Unprecedented Growth millennium, vehicles focusing on Asia have clearly weathered 0.15 the storm with more success than their European and US Europe The period 2003 – 2008 saw unprecedented growth within 0.1 the Asian private equity industry. Fig. 1 shows the increase counterparts, with median IRRs for all vintage years still Asia and Rest of World posting positive results while funds focusing primarily on the 0.05 in total capital raised annually by funds focusing on the US region between the period 2003 and 2008, when a record West are still in the red. IRR Median Net-to-LP 0 $91bn was raised by 194 funds achieving a fi nal close. 1995 1997 1999 2001 2003 2005 2007 The main factors behind the decline in Asia fundraising can -0.05 As Fig. 2 shows, the record level of capital raised saw the be identifi ed by examining the make-up of fund managers -0.1 Vintage Year importance of the Asian private equity industry growing on and investors in the region more closely. As Fig. -

In a Year of Contraction, Asia Feels the Ripple Effect of Mifid II 2016 Greenwich Leaders: Asian Equities

In a Year of Contraction, Asia Feels the Ripple Effect of MiFID II 2016 Greenwich Leaders: Asian Equities Q1 2017 Three global brokers are pulling away from the pack in the Asian equity research/advisory business—a break from historical patterns characterized by a more gradual slope among major competitors. Credit Suisse, Bank of America Merrill Lynch and Morgan Stanley are statistically deadlocked atop the list of 2016 Greenwich Leaders in Asian Equity Research/Advisory Vote Share. These three firms have opened a significant lead over UBS, CLSA Asia-Pacific Markets and J.P. Morgan, which are also virtually tied in terms of vote share and round out the list of this year’s winners. In Asian Equity Trading, the same three firms are statistically tied for the top spot in overall share, but in this business, their lead over fellow Greenwich Share Leaders CLSA, UBS and Citi is much narrower. In the growing algorithmic trading business, Bank of America Merrill Lynch widened its lead over the competition. Credit Suisse and Morgan Stanley claim the title of 2016 Greenwich Quality Leaders in Asian Equity Research Product & Analyst Service, and Greenwich Share Leaders — 2016 GREENWICH ASSOCIATES Greenwich Share20 1Leade6r Asian Equity Research/Advisory Vote Share Asian Equity Algorithmic Trading Share Broker Statistical Rank Broker Statistical Rank Credit Suisse 1T Bank of America Merrill Lynch 1 Bank of America Merrill Lynch 1T UBS 2T Morgan Stanley 1T Morgan Stanley 2T UBS 4T Credit Suisse 2T CLSA Asia-Pacific Markets 4T Goldman Sachs 5T J.P. Morgan 4T Citi 5T ITG 5T Asian Equity Trading Share, Options & Volatility Product Important Relationships—Asia Broker Statistical Rank* Broker Statistical Rank Morgan Stanley 1T Morgan Stanley 1T Bank of America Merrill Lynch 1T Goldman Sachs 1T Credit Suisse 1T Bank of America Merrill Lynch 3T CLSA Asia-Pacific Markets 4T Deutsche Bank 3T UBS 4T J.P. -

TRS Contracted Investment Managers

TRS INVESTMENT RELATIONSHIPS AS OF DECEMBER 2020 Global Public Equity (Global Income continued) Acadian Asset Management NXT Capital Management AQR Capital Management Oaktree Capital Management Arrowstreet Capital Pacific Investment Management Company Axiom International Investors Pemberton Capital Advisors Dimensional Fund Advisors PGIM Emerald Advisers Proterra Investment Partners Grandeur Peak Global Advisors Riverstone Credit Partners JP Morgan Asset Management Solar Capital Partners LSV Asset Management Taplin, Canida & Habacht/BMO Northern Trust Investments Taurus Funds Management RhumbLine Advisers TCW Asset Management Company Strategic Global Advisors TerraCotta T. Rowe Price Associates Varde Partners Wasatch Advisors Real Assets Transition Managers Barings Real Estate Advisers The Blackstone Group Citigroup Global Markets Brookfield Asset Management Loop Capital The Carlyle Group Macquarie Capital CB Richard Ellis Northern Trust Investments Dyal Capital Penserra Exeter Property Group Fortress Investment Group Global Income Gaw Capital Partners AllianceBernstein Heitman Real Estate Investment Management Apollo Global Management INVESCO Real Estate Beach Point Capital Management LaSalle Investment Management Blantyre Capital Ltd. Lion Industrial Trust Cerberus Capital Management Lone Star Dignari Capital Partners LPC Realty Advisors Dolan McEniry Capital Management Macquarie Group Limited DoubleLine Capital Madison International Realty Edelweiss Niam Franklin Advisers Oak Street Real Estate Capital Garcia Hamilton & Associates -

LAZARD GROUP LLC (Exact Name of Registrant As Specified in Its Charter)

Table of Contents UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K (Mark One) ☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2008 OR ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to 333-126751 (Commission File Number) LAZARD GROUP LLC (Exact name of registrant as specified in its charter) Delaware 51-0278097 (State or Other Jurisdiction of Incorporation (I.R.S. Employer Identification No.) or Organization) 30 Rockefeller Plaza New York, NY 10020 (Address of principal executive offices) Registrant’s telephone number: (212) 632-6000 Securities Registered Pursuant to Section 12(b) of the Act: None Securities Registered Pursuant to Section 12(g) of the Act: None Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐ Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐ No ☒ Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐ Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. -

Meet Our Speakers

MEET OUR SPEAKERS DEBRA ABRAMOVITZ Morgan Stanley Debra Abramovitz is an Executive Director of Morgan Stanley and serves as Chief Operating Officer of Morgan Stanley Expansion Capital. Debra oversees all financial, administrative, investor relations and operational activities for Morgan Stanley Expansion Capital, and its predecessor Morgan Stanley Venture Partners funds. Debra also serves as COO of Morgan Stanley Credit Partners. Debra joined Morgan Stanley’s Finance Department in 1983 and joined Morgan Stanley Private Equity in 1988, with responsibility for monitoring portfolio companies. Previously, Debra was with Ernst & Young. Debra is a graduate of American University in Paris and the Columbia Business School. JOHN ALLAN-SMITH Barclays Americas John Allan-Smith leads the US Funds team for Corporate Banking at Barclays and is responsible for coordinating the delivery of products and services from our global businesses; ranging from debt, FX solutions, cash management and trade finance, to working capital lending and liquidity structures. John joined Barclays in 2014 and has 20 years of experience in the funds sector. Prior to joining Barclays, John worked at The Royal Bank of Scotland (RBS) in London, Stockholm and New York, spending 10 years in the RBS Leveraged Finance team. Subsequently, John had responsibility for the portfolios and banking sector of the Non-Core division of RBS in the Americas. John holds an ACA qualification from the Institute of Chartered Accountants of England and Wales and is a qualified accountant. He also has a BSc (Hons) in Chemistry from The University of Nottingham. ROBERT ANDREWS Ashurst LLP Robert is a partner in the banking group at Ashurst and is one of the most experienced funds finance specialists in Europe. -

ANNUAL REVIEW 2017 Land of the Giants Cycle-Tested Credit Expertise Extensive Market Coverage Comprehensive Solutions Relative Value Focus

ANNUAL REVIEW 2017 Land of the giants Cycle-Tested Credit Expertise Extensive Market Coverage Comprehensive Solutions Relative Value Focus Ares Management is honored to be recognized as Lender of the Year in North America for the fourth consecutive year as well as Lender of the Year in Europe Lender of the year in Europe Ares Management, L.P. (NYSE: ARES) is a leading global alternative asset manager with approximately $106 billion of AUM1 and offices throughout the United States, Europe, Asia and Australia. With more than $70 billion in AUM1 and approximately 235 investment professionals, the Ares Credit Group is one of the largest global alternative credit managers across the non-investment grade credit universe. Ares is also one of the largest direct lenders to the U.S. and European middle markets, operating out of twelve office locations in both geographies. Note: As of December 31, 2017. The performance, awards/ratings noted herein may relate only to selected funds/strategies and may not be representative of any client’s given experience and should not be viewed as indicative of Ares’ past performance or its funds’ future performance. 1. AUM amounts include funds managed by Ivy Hill Asset Management, L.P., a wholly owned portfolio company of Ares Capital Corporation and a registered investment adviser. learn more at: www.aresmgmt.com | www.arescapitalcorp.com The battle of the brands the US market on page 80, advisor Hamilton TOBY MITCHENALL Lane said it had received a record number EDITOR'S of private placement memoranda in 2017 – ISSN 1474–8800 LETTER MARCH 2018 around 800 – and that this, combined with Senior Editor, Private Equity faster fundraising processes, has made it dif- Toby Mitchenall, Tel: +44 207 566 5447 [email protected] ficult to some investors to make considered Special Projects Editor decisions. -

Espinal, Et Al. V. Didi Global Inc., Et Al. 21-CV-05807-U.S. District Court

Espinal v. Didi Global Inc. et al, Docket No. 1:21-cv-05807 (S.D.N.Y. Jul 06, 2021), Court Docket Current on Bloomberg Law as of 2021-07-08 13:03:33 U.S. District Court Southern District of New York (Foley Square) CIVIL DOCKET FOR CASE #: 1:21-cv-05807-LAK Espinal v. Didi Global Inc. et al Date Filed: Jul 6, 2021 Nature of suit: 850 Securities/ Commodities Assigned to: Judge Lewis A. Kaplan Cause: 15:77 Securities Fraud Jurisdiction: Federal Question Jury demand: Plaintiff Parties and Attorneys Plaintiff Rafaela Espinal individually and on behalf of all others similarly situated Representation Gregory Bradley Linkh Glancy Prongay & Murray LLP 230 Park Avenue Suite 358 New York, NY 10169 (212) 682-5340 [email protected] ATTORNEY TO BE NOTICED Defendant Didi Global Inc. formerly known as: Xiaoju Kuaizhi Inc. Defendant Will Wei Cheng © 2021 The Bureau of National Affairs, Inc. All Rights Reserved. Terms of Service // PAGE 1 Espinal v. Didi Global Inc. et al, Docket No. 1:21-cv-05807 (S.D.N.Y. Jul 06, 2021), Court Docket Defendant Alan Yue Zhuo Defendant Jean Qing Liu Defendant Stephen Jingshi Zhu Defendant Zhiyi Chen Defendant Martin Chi Ping Lau Defendant Kentaro Matsui Defendant Adria Perica Defendant Daniel Yong Zhang Defendant Goldman Sachs (ASIA) L.L.C. Defendant Morgan Stanley & Co. LLC Defendant J.P. Morgan Securities LLC Defendant Bofa Securities, Inc. Defendant Barclays Capital Inc. Defendant China Renaissance Securities (Hong Kong) Limited Defendant China International Capital Corporation Hong Kong Securities Limited © 2021 The Bureau of National Affairs, Inc. -

Reverse Convertible Notes Linked to Blackstone Group

Structured Products Research Report Report Prepared On: 12/14/12 Structured Product Details Reverse Convertible Notes linked to Blackstone Group Name Reverse Convertible Notes linked to Blackstone Group Description HSBC issued $784,000 of Reverse Convertible Notes linked to Blackstone Group on Issue Size $784,000 October 31, 2007 at $1,000 per note. Issue Price $1,000 Term 6 Months These notes are HSBC-branded reverse convertibles. Reverse convertibles pay periodic Annualized Coupon 11.50% interest coupons and at maturity convert into shares of the reference security if the price of the reference stock at the notes’ maturity is below its price when the notes were issued Pricing Date October 26, 2007 and had closed below a specified “trigger” during the term of the notes. Issue Date October 31, 2007 Valuation Date April 25, 2008 April 30, 2008 These 6-month notes pay monthly coupons at an annualized rate of 11.50%. In addition Maturity Date to the monthly coupons, at maturity on April 30, 2008 investors will receive the mar- Issuer HSBC ket value of 39.08 shares of Blackstone Group’s stock if on April 25, 2008 Blackstone CDS Rate 43.4 bps Group’s stock price closes below $25.59 (Blackstone Group’s stock price on October 26, Swap Rate 4.78% 2007) and had ever closed at or below $17.91 during the term of the notes. Otherwise, investors will receive the $1,000 face value per note. Reference Asset Blackstone Group’s stock Initial Level $25.59 Valuation Trigger Price $17.91 This HSBC reverse convertible linked to Blackstone Group’s stock can be valued as a Conversion Price $19.20 combination of a note from HSBC and a short down-and-in, at-the-money put option on Dividend Rate 0.00% Blackstone Group’s stock. -

PEI June2020 PEI300.Pdf

Cover story 20 Private Equity International • June 2020 Cover story Better capitalised than ever Page 22 The Top 10 over the decade Page 24 A decade that changed PE Page 27 LPs share dealmaking burden Page 28 Testing the value creation story Page 30 Investing responsibly Page 32 The state of private credit Page 34 Industry sweet spots Page 36 A liquid asset class Page 38 The PEI 300 by the numbers Page 40 June 2020 • Private Equity International 21 Cover story An industry better capitalised than ever With almost $2trn raised between them in the last five years, this year’s PEI 300 are armed and ready for the post-coronavirus rebuild, writes Isobel Markham nnual fundraising mega-funds ahead of the competition. crisis it’s better to be backed by a pri- figures go some way And Blackstone isn’t the only firm to vate equity firm, particularly and to towards painting a up the ante. The top 10 is around $30 the extent that it is able and prepared picture of just how billion larger than last year’s, the top to support these companies, which of much capital is in the 50 has broken the $1 trillion mark for course we are,” he says. hands of private equi- the first time, and the entire PEI 300 “The businesses that we own at Aty managers, but the ebbs and flows of has amassed $1.988 trillion. That’s the Blackstone that are directly affected the fundraising cycle often leave that same as Italy’s GDP. Firms now need by the pandemic, [such as] Merlin, picture incomplete. -

Landscape Portrait

CLSA (UK) ORDER EXECUTION POLICY 1 General Information about this Policy 1.1 Background CLSA UK (“CLSA”) provides general broker dealer and other ancillary services to its clients. It is authorised and regulated by the Financial Conduct Authority of the United Kingdom (the "FCA") and is an investment firm subject to the requirements of the rules of the FCA (the “FCA Rules”) that implement the Markets in Financial Instruments Directive 2014/65/EU ("MiFID II"). CLSA executes orders in relation to financial instruments on behalf of its clients. There are two methods that it can use to execute those orders that are distinguished for the purposes of the FCA Rules. (A) First, CLSA can execute the relevant transaction on behalf of the client directly with a counterparty or on an exchange or other trading system (e.g., by dealing directly with a market maker on a “request for quote” basis). The counterparty, exchange or trading system with which CLSA chooses to execute such a transaction is referred to in this policy as an “Execution Venue”. In accordance with the FCA Rules, an Execution Venue can include an EEA regulated market, or other exchange, a multilateral trading facility, organised trading facility, a systematic internaliser, a market maker or other liquidity provider or non-EEA entity performing similar functions to the Execution Venues listed above. (B) Secondly, CLSA can place an order as agent with a third party (e.g., another broker or investment bank) and/or any of its affiliates for that third party or affiliate to execute on behalf of the client. -

China 2025 16

China | Equity Strategy China 14 December 2014 EQUITY RESEARCH China The Year of the Ram: Stars Aligned for a Historic Bull Run Key Takeaway The Ram, the Bull and the Heavenly Twins – the stars are now aligned for China’s historic bull-run. China's stock market offers massive untapped potential given the high savings rate and low penetration. “Keeping Growth Steady” is a top priority for 2015; we expect SHCOMP and HSCEI to test 4,050 and 15,420, up 38% and 37% from current levels. As confidence gains momentum, volatility becomes the investors’ best friend. CHINA China Gallops into a Historic Bull Run. On Nov 20, 2013, we wrote “The Year of the Horse will see China unleash its full potential, as President Xi ushers in a new era of profound change.” “We expect capital markets to gradually gain confidence in China’s ability to drive fundamental reforms and expect Chinese stocks to enter a historic multi-year bull run.” Indeed, 2014 has been a remarkable year. As of Dec.12, SHCOMP surged 39% to 2938, breaking a seven-year bearish trend to become the best performing index in the world. China Stock Market: Massive Untapped Potential. According to China Household Finance Survey, property accounted for 66.4% of total Chinese household assets in 2013. Financial assets accounted for a mere 10.1% of household wealth. While over 61% of Chinese families have bank deposits, only 6.5% of them invested in the stock market. Given China’s high savings rate and low stock market penetration, we believe the A-share market offers significant upside potential.