Pei-300-2020.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

PE Pulse Quarterly Insights and Intelligence on PE Trends February 2020

PE Pulse Quarterly insights and intelligence on PE trends February 2020 This document is interactive i. ii. iii. iv. v. Contents The PE Pulse has been designed to help you remain current on capital market trends. It captures key insights from subject-matter professionals across EY member firms and distills this intelligence into a succinct and user-friendly publication. The PE Pulse provides perspectives on both recent developments and the longer-term outlook for private equity (PE) fundraising, acquisitions and exits, as well as trends in private credit and infrastructure. Please feel free to reach out to any of the subject matter contacts listed on page 25 of this document if you wish to discuss any of the topics covered. PE to see continued strength in 2020 as firms seek clear air for deployment We expect overall PE activity to remain strong in 2020. From a deal perspective, deployment remains challenging. Geopolitical developments will continue to shape the 2019 was a strong year from a fundraising perspective, Currently, competition for deals is pushing multiples dispersion of activity. In the US, for example, activity has albeit slightly off the high-water mark of 2017. While well above the top of the last cycle. In the US, purchase continued largely unabated, driven by a strong macro valuations and the challenges in deploying capital multiples have reached 11.5x (versus 9.7x in 2007), and backdrop and accommodative lending markets. PE firms continue to raise concerns among some LPs, any 11.1x in Europe (versus 10.3x in 2007). As a result, firms announced deals valued at US$249b, up 3% from last hesitation in committing fresh capital is being offset to are seeking “clearer air” by moving downmarket into the year, making it among the most active years since the a degree by entirely new investors that are moving into growth capital space, where growth rates are higher and global financial crisis (GFC). -

Corporate Governance Positions and Responsibilities of the Directors and Nominees to the Board of Directors

CORPORATE GOVERNANCE POSITIONS AND RESPONSIBILITIES OF THE DIRECTORS AND NOMINEES TO THE BOARD OF DIRECTORS LIONEL ZINSOU -DERLIN (a) Born on October 23, 1954 Positions and responsibilities as of December 31, 2014 Age: 60 Positions Companies Countries Director (term of office DANONE SA (b) France from April 29, 2014 to the end of the Shareholders’ Meeting to approve the 2016 financial statements) Chairman and Chair- PAI PARTNERS SAS France man of the Executive Business address: Committee 232, rue de Rivoli – 75001 Paris – France Member of the Number of DANONE shares held Investment Committee as of December 31, 2014: 4,000 Director INVESTISSEURS & PARTENAIRES Mauritius Independent Director I&P AFRIQUE ENTREPRENEURS Mauritius Dual French and Beninese nationality KAUFMAN & BROAD SA (b) France PAI SYNDICATION GENERAL PARTNER LIMITED Guernsey Principal responsibility: Chairman of PAI partners SAS PAI EUROPE III GENERAL PARTNER LIMITED Guernsey Personal backGround – PAI EUROPE IV GENERAL PARTNER LIMITED Guernsey experience and expertise: Lionel ZINSOU-DERLIN, of French and Beninese PAI EUROPE V GENERAL PARTNER LIMITED Guernsey nationality, is a graduate from the Ecole Normale PAI EUROPE VI GENERAL PARTNER LIMITED Guernsey Supérieure (Ulm), the London School of Economics and the Institut d’Etudes Politiques of Paris. He holds Chairman and Member LES DOMAINES BARONS DE ROTHSCHILD SCA France a master degree in Economic History and is an Asso- of the Supervisory (LAFITE) ciate Professor in Social Sciences and Economics. Board Member of the Advisory MOET HENNESSY France He started his career as a Senior Lecturer and Pro- Council fessor of Economics at Université Paris XIII. Member of the CERBA EUROPEAN LAB SAS France From 1984 to 1986, he became an Advisor to the French Supervisory Board Ministry of Industry and then to the Prime Minister. -

Francesco Pascalizi Appointed Co-Head of the Milan Office Alongside Fabrizio Carretti

PERMIRA STRENGTHENS ITS PRESENCE IN ITALY: FRANCESCO PASCALIZI APPOINTED CO-HEAD OF THE MILAN OFFICE ALONGSIDE FABRIZIO CARRETTI London/Milan, 24 October 2019 –Francesco Pascalizi has been appointed co-head of Permira in Italy and joins Fabrizio Carretti in the leadership of the Milan office. Francesco Pascalizi has worked closely with Fabrizio Carretti for more than 12 years and has contributed significantly to developing Permira’s business in the Italian market, having completed several investments in the industrial and consumer space. He currently serves on the Board of Arcaplanet and Gruppo La Piadineria, acquired by the Permira Funds respectively in 2016 and 2017. Fabrizio Carretti commented: “I am really delighted to have Francesco join the leadership of the Milan team – I am sure that his appointment will further strengthen our position in the Italian market”. Francesco Pascalizi added: “I am very pleased to join Fabrizio and look forward to continue developing Permira’s franchise in Italy, a country to which we are strongly committed”. Francesco Pascalizi joined Permira in 2007 and he is a member of the Industrial Tech & Services team. He has worked on a number of transactions including La Piadineria, Arcaplanet, eDreams OdigeO, and Marazzi Group. Prior to joining Permira, Francesco worked in the private equity group at Bain Capital and before that he was part of M&A team at UBS in both Milan and London. He has a degree in Business Administration from Bocconi University, Italy. ABOUT PERMIRA Permira is a global investment firm. Founded in 1985, the firm advises funds with total committed capital of approximately €44bn (US$48bn) and makes long-term investments, including majority control investments as well as strategic minority investments, in companies with the objective of transforming their performance and driving sustainable growth. -

A Listing of PSERS' Investment Managers, Advisors, and Partnerships

Pennsylvania Public School Employees’ Retirement System Roster of Investment Managers, Advisors, and Consultants As of March 31, 2015 List of PSERS’ Internally Managed Investment Portfolios • Bloomberg Commodity Index Overlay • Gold Fund • LIBOR-Plus Short-Term Investment Pool • MSCI All Country World Index ex. US • MSCI Emerging Markets Equity Index • Risk Parity • Premium Assistance • Private Debt Internal Program • Private Equity Internal Program • Real Estate Internal Program • S&P 400 Index • S&P 500 Index • S&P 600 Index • Short-Term Investment Pool • Treasury Inflation Protection Securities • U.S. Core Plus Fixed Income • U.S. Long Term Treasuries List of PSERS’ External Investment Managers, Advisors, and Consultants Absolute Return Managers • Aeolus Capital Management Ltd. • AllianceBernstein, LP • Apollo Aviation Holdings Limited • Black River Asset Management, LLC • BlackRock Financial Management, Inc. • Brevan Howard Asset Management, LLP • Bridgewater Associates, LP • Brigade Capital Management • Capula Investment Management, LLP • Caspian Capital, LP • Ellis Lake Capital, LLC • Nephila Capital, Ltd. • Oceanwood Capital Management, Ltd. • Pacific Investment Management Company • Perry Capital, LLC U.S. Equity Managers • AH Lisanti Capital Growth, LLC Pennsylvania Public School Employees’ Retirement System Page 1 Publicly-Traded Real Estate Securities Advisors • Security Capital Research & Management, Inc. Non-U.S. Equity Managers • Acadian Asset Management, LLC • Baillie Gifford Overseas Ltd. • BlackRock Financial Management, Inc. • Marathon Asset Management Limited • Oberweis Asset Management, Inc. • QS Batterymarch Financial Management, Inc. • Pyramis Global Advisors • Wasatch Advisors, Inc. Commodity Managers • Black River Asset Management, LLC • Credit Suisse Asset Management, LLC • Gresham Investment Management, LLC • Pacific Investment Management Company • Wellington Management Company, LLP Global Fixed Income Managers U.S. Core Plus Fixed Income Managers • BlackRock Financial Management, Inc. -

BMO Private Equity Trust PLC

BMO Private Equity Trust PLC Annual Report and Accounts 31 December 2019 BMO Private Equity Trust PLC Celebrating1 | BMO Private 20 Equity years Trust PLC– 1999 to 2019 Report and Accounts 2019 | PB 2 | BMO Private Equity Trust PLC Report and Accounts 2019 | 1 Overview Overview Contents Chairman’s statement Strategic Auditor’s Report Overview Independent Auditor’s Report 40 Company Overview 2 Report Financial Highlights 3 Summary of Performance 4 Financial Report Statement of Comprehensive Income 46 5 Balance Sheet 47 Chairman’s Statement Statement of Changes in Equity 48 Governance Statement of Cash Flows 49 Strategic Report Notes to the Financial Statements 50 Strategic Report – Introduction 7 M DisclosuresAIF 63 Principal Policies 9 Report Promoting the Success and Sustainability of the Company 11 Sustainability and ESG 12 Annual General Meeting Key Performance Indicators 13 Notice of Annual General Meeting 64 Investment Manager 14 Investment Manager’s Review 15 Other Information Auditor’s Shareholder Information 69 Portfolio Summary 19 Top Ten Holdings 20 History 70 Report Portfolio Holdings 22 Historical Record 70 Principal Risks 24 Alternative Performance Measures 71 Glossary of Terms 73 Governance Report w Ho to Invest 75 Corporate Information 76 d of BoarDirectors 26 Financial Report of the Directors 27 Report Corporate Governance Statement 31 Report of the Audit Committee 33 Report of the Nomination Committee 35 Directors’ Remuneration Report 36 Report of the Management Engagement Committee 38 Statement of Directors’ Responsibilities 39 AGM Other Information 2 | BMO Private Equity Trust PLC Report and Accounts 2019 | 1 185155 PET AR19 PRINT.indd 1 16/04/2020 13:58 BMO Private Equity Trust PLC Company Overview The Company BMO Private Equity Trust PLC (‘the Company’) is an investment trust and its Ordinary Shares are traded on the Main Market of the London Stock Exchange. -

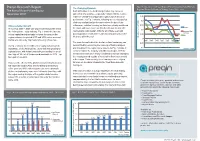

Preqin Research Report Fig

Preqin Research Report Fig. 3 Comparison of Private Equity Performance by Fund Primary The Changing Dynamic Regional Focus for Funds of Vintage Years 1995 - 2007 The Rise of Asian Private Equity Such diffi culties in the fundraising market may come as November 2010 somewhat of a surprise – especially considering the relative resilience of Asia-focused private equity funds in terms of 0.25 performance. As Fig. 3 shows, following an extended period 0.2 of strong median fund performance since the turn of the Unprecedented Growth millennium, vehicles focusing on Asia have clearly weathered 0.15 the storm with more success than their European and US Europe The period 2003 – 2008 saw unprecedented growth within 0.1 the Asian private equity industry. Fig. 1 shows the increase counterparts, with median IRRs for all vintage years still Asia and Rest of World posting positive results while funds focusing primarily on the 0.05 in total capital raised annually by funds focusing on the US region between the period 2003 and 2008, when a record West are still in the red. IRR Median Net-to-LP 0 $91bn was raised by 194 funds achieving a fi nal close. 1995 1997 1999 2001 2003 2005 2007 The main factors behind the decline in Asia fundraising can -0.05 As Fig. 2 shows, the record level of capital raised saw the be identifi ed by examining the make-up of fund managers -0.1 Vintage Year importance of the Asian private equity industry growing on and investors in the region more closely. As Fig. -

Annual Report

Building Long-term Wealth by Investing in Private Companies Annual Report and Accounts 12 Months to 31 January 2021 Our Purpose HarbourVest Global Private Equity (“HVPE” or the “Company”) exists to provide easy access to a diversified global portfolio of high-quality private companies by investing in HarbourVest-managed funds, through which we help support innovation and growth in a responsible manner, creating value for all our stakeholders. Investment Objective The Company’s investment objective is to generate superior shareholder returns through long-term capital appreciation by investing primarily in a diversified portfolio of private markets investments. Our Purpose in Detail Focus and Approach Investment Manager Investment into private companies requires Our Investment Manager, HarbourVest Partners,1 experience, skill, and expertise. Our focus is on is an experienced and trusted global private building a comprehensive global portfolio of the markets asset manager. HVPE, through its highest-quality investments, in a proactive yet investments in HarbourVest funds, helps to measured way, with the strength of our balance support innovation and growth in the global sheet underpinning everything we do. economy whilst seeking to promote improvement in environmental, social, Our multi-layered investment approach creates and governance (“ESG”) standards. diversification, helping to spread risk, and is fundamental to our aim of creating a portfolio that no individual investor can replicate. The Result Company Overview We connect the everyday investor with a broad HarbourVest Global Private Equity is a Guernsey base of private markets experts. The result is incorporated, London listed, FTSE 250 Investment a distinct single access point to HarbourVest Company with assets of $2.9 billion and a market Partners, and a prudently managed global private capitalisation of £1.5 billion as at 31 January 2021 companies portfolio designed to navigate (tickers: HVPE (£)/HVPD ($)). -

VP for VC and PE.Indd

EUROPEAN VENTURE PHILANTHROPY ASSOCIATION A guide to Venture PhilAnthroPy for Venture Capital and Private Equity investors Ashley Metz CummingS and Lisa Hehenberger JUNE 2011 2 A guidE to Venture Philanthropy for Venture Capital and Private Equity investors LETTER fROM SERgE RAICHER 4 Part 2: PE firms’ VP engAgement 20 ContentS Executive Summary 6 VC/PE firms and Philanthropy PART 1: Introduction 12 Models of engagement in VP Purpose of the document Model 1: directly support Social Purpose Organisations Essence and Role of Venture Philanthropy Model 2: Invest in or co-invest with a VP Organisation Venture Philanthropy and Venture Capital/Private Equity Model 3: found or co-found a VP Organisation Published by the European Venture Philanthropy Association This edition June 2011 Copyright © 2011 EVPA Email : [email protected] Website : www.evpa.eu.com Creative Commons Attribution-Noncommercial-No derivative Works 3.0 You are free to share – to copy, distribute, display, and perform the work – under the following conditions: Attribution: You must attribute the work as A gUIdE TO VENTURE PHILANTHROPY fOR VENTURE CAPITAL ANd PRIVATE EqUITY INVESTORS Copyright © 2011 EVPA. Non commercial: You may not use this work for commercial purposes. No derivative Works: You may not alter, transform or build upon this work. for any reuse or distribution, you must make clear to others the licence terms of this work. ISbN 0-9553659-8-8 Authors: Ashley Metz Cummings and dr Lisa Hehenberger Typeset in Myriad design and typesetting by: Transform, 115b Warwick Street, Leamington Spa CV32 4qz, UK Printed and bound by: drukkerij Atlanta, diestsebaan 39, 3290 Schaffen-diest, belgium This book is printed on fSC approved paper. -

Joshua Smith

Joshua Smith Associate London | 160 Queen Victoria Street, London, UK EC4V 4QQ T +44 20 7184 7824 | F +44 20 7184 7001 [email protected] Services Mergers and Acquisitions > Private Equity > Corporate Finance and Capital Markets > Corporate Governance > Joshua Smith practices in the area of corporate law, advising on a wide range of domestic and cross-border mergers and acquisitions, private equity transactions, joint ventures, fundraisings, public offerings, reorganisations and other general corporate matters. Mr. Smith trained at Dechert and qualified as a solicitor in 2014. EXPERIENCE Hellenic Telecommunications Organization S.A (OTE) in connection with the sale of its stake in fixed telecommunications operator Telekom Romania for €268 million to Orange Romania. ICTS International N.V. and ABC Technologies B.V. on (i) a US$60 million equity investment by an affiliate of TPG Global into ABC, a subsidiary of ICTS and the owner of Au10tix Limited, a leader in the ID documentation and know-your-customer on- boarding automation software industry and (ii) a further US$20 million equity investment by Oak HC/FT into ABC and related shareholder agreements. The transactions valued Au10tix at US$280 million. A substantial family office as investor in a substantive venture investment in a UK ticketing and events hosting company. Centaur Media plc, as part of its strategic divestment program on the sale of (i) its financial services division to Metropolis Group; (ii) Centaur Human Resources Limited, to DVV Media International Ltd; (iii) Centaur Media Travel and Meetings Limited, to Northstar Travel Media UK Limited; and (iv) its engineering portfolio, including The Engineer and Subcon, to Mark Allen Group. -

Private Equity 05.23.12

This document is being provided for the exclusive use of SABRINA WILLMER at BLOOMBERG/ NEWSROOM: NEW YORK 05.23.12 Private Equity www.bloombergbriefs.com BRIEF NEWS, ANALYSIS AND COMMENTARY CVC Joins Firms Seeking Boom-Era Size Funds QUOTE OF THE WEEK BY SABRINA WILLMER CVC Capital Partners Ltd. hopes its next European buyout fund will nearly match its predecessor, a 10.75 billion euro ($13.6 billion) fund that closed in 2009, according to two “I think it would be helpful people familiar with the situation. That will make it one of the largest private equity funds if Putin stopped wandering currently seeking capital. One person said that CVC European Equity Partners VI LP will likely aim to raise 10 around bare-chested.” billion euros. The firm hasn’t yet sent out marketing materials. Two people said they expect it to do so — Janusz Heath, managing director of in the second half. Mary Zimmerman, an outside spokeswoman for CVC Capital, declined Capital Dynamics, speaking at the EMPEA to comment. conference on how Russia might help its reputation and attract more private equity The London-based firm would join only a few other firms that have closed or are try- investment. See page 4 ing to raise new funds of similar size to the mega funds raised during the buyout boom. Leonard Green & Partners’s sixth fund is expected to close shortly on more than $6 billion, more than the $5.3 billion its last fund closed on in 2007. Advent International MEETING TO WATCH Corp. is targeting 7 billion euros for its seventh fund, larger than its last fund, and War- burg Pincus LLC has a $12 billion target on Warburg Pincus Private Equity XI LP, the NEW JERSEY STATE INVESTMENT same goal as its predecessor. -

HVPE Prospectus

MERRILL CORPORATION GTHOMAS// 1-NOV-07 23:00 DISK130:[07ZDA1.07ZDA48401]BA48401A.;44 mrll.fmt Free: 11DM/0D Foot: 0D/ 0D VJ J1:1Seq: 1 Clr: 0 DISK024:[PAGER.PSTYLES]UNIVERSAL.BST;67 8 C Cs: 17402 PROSPECTUS, DATED 2 NOVEMBER 2007 Global Offering of up to 40,000,000 Shares of 1NOV200718505053 This document describes related offerings of Class A ordinary shares (the ‘‘Shares’’) of HarbourVest Global Private Equity Limited (the ‘‘company’’), a closed-ended investment company organised under the laws of Guernsey. Our Shares are being offered (a) outside the United States, and (b) inside the United States in a private placement to certain qualified institutional buyers (‘‘QIBs’’) as defined in Rule 144A under the U.S. Securities Act of 1933, as amended (the ‘‘U.S. Securities Act’’), who are also qualified purchasers (‘‘qualified purchasers’’) as defined in the U.S. Investment Company Act of 1940, as amended (the ‘‘U.S. Investment Company Act’’) (the ‘‘Global Offering’’). We intend to issue up to 40,000,000 Shares in the Global Offering. In addition, we intend separately to issue Shares to certain third parties in a private placement in exchange for either cash or limited partnership interests in various HarbourVest-managed funds (the ‘‘Directed Offering’’ and, together with the Global Offering, the ‘‘Offerings’’). We will not issue, in the aggregate, more than 85,000,000 Shares in the Offerings. The Shares carry limited voting rights. No public market currently exists for the Shares. We have applied for the admission to trading all of the Shares on Euronext Amsterdam by NYSE Euronext (‘‘Euronext Amsterdam’’), the regulated market of Euronext Amsterdam N.V. -

ANNUAL REVIEW 2017 Land of the Giants Cycle-Tested Credit Expertise Extensive Market Coverage Comprehensive Solutions Relative Value Focus

ANNUAL REVIEW 2017 Land of the giants Cycle-Tested Credit Expertise Extensive Market Coverage Comprehensive Solutions Relative Value Focus Ares Management is honored to be recognized as Lender of the Year in North America for the fourth consecutive year as well as Lender of the Year in Europe Lender of the year in Europe Ares Management, L.P. (NYSE: ARES) is a leading global alternative asset manager with approximately $106 billion of AUM1 and offices throughout the United States, Europe, Asia and Australia. With more than $70 billion in AUM1 and approximately 235 investment professionals, the Ares Credit Group is one of the largest global alternative credit managers across the non-investment grade credit universe. Ares is also one of the largest direct lenders to the U.S. and European middle markets, operating out of twelve office locations in both geographies. Note: As of December 31, 2017. The performance, awards/ratings noted herein may relate only to selected funds/strategies and may not be representative of any client’s given experience and should not be viewed as indicative of Ares’ past performance or its funds’ future performance. 1. AUM amounts include funds managed by Ivy Hill Asset Management, L.P., a wholly owned portfolio company of Ares Capital Corporation and a registered investment adviser. learn more at: www.aresmgmt.com | www.arescapitalcorp.com The battle of the brands the US market on page 80, advisor Hamilton TOBY MITCHENALL Lane said it had received a record number EDITOR'S of private placement memoranda in 2017 – ISSN 1474–8800 LETTER MARCH 2018 around 800 – and that this, combined with Senior Editor, Private Equity faster fundraising processes, has made it dif- Toby Mitchenall, Tel: +44 207 566 5447 [email protected] ficult to some investors to make considered Special Projects Editor decisions.