Monthly M&A Insider January 2015 – HY Edition

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

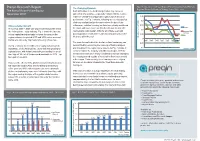

Preqin Research Report Fig

Preqin Research Report Fig. 3 Comparison of Private Equity Performance by Fund Primary The Changing Dynamic Regional Focus for Funds of Vintage Years 1995 - 2007 The Rise of Asian Private Equity Such diffi culties in the fundraising market may come as November 2010 somewhat of a surprise – especially considering the relative resilience of Asia-focused private equity funds in terms of 0.25 performance. As Fig. 3 shows, following an extended period 0.2 of strong median fund performance since the turn of the Unprecedented Growth millennium, vehicles focusing on Asia have clearly weathered 0.15 the storm with more success than their European and US Europe The period 2003 – 2008 saw unprecedented growth within 0.1 the Asian private equity industry. Fig. 1 shows the increase counterparts, with median IRRs for all vintage years still Asia and Rest of World posting positive results while funds focusing primarily on the 0.05 in total capital raised annually by funds focusing on the US region between the period 2003 and 2008, when a record West are still in the red. IRR Median Net-to-LP 0 $91bn was raised by 194 funds achieving a fi nal close. 1995 1997 1999 2001 2003 2005 2007 The main factors behind the decline in Asia fundraising can -0.05 As Fig. 2 shows, the record level of capital raised saw the be identifi ed by examining the make-up of fund managers -0.1 Vintage Year importance of the Asian private equity industry growing on and investors in the region more closely. As Fig. -

Capstone Headwaters Education Technology M&A Coverage Report

Capstone Headwaters EDUCATION TECHNOLOGY 2019 YEAR IN REVIEW TABLE OF CONTENTS MERGER & ACQUISTION OVERVIEW M&A Overview The Education Technology (EdTech) industry has continued to experience rapid consolidation with 195 transactions announced or completed in 2019. Active Buyers Heightened merger and acquisition (M&A) activity has been fueled by Notable Transactions persistent demand for disruptive and scalable technology as industry operators Select Transactions seek to expand product offerings and market share. In addition to robust transaction activity, recent investment patterns have targeted EdTech providers Public Company Data that offer innovative products for classroom teacher support and to streamline Firm Transactions in Market administrative operations in K-12 schools. Funding in the segment has risen Firm Track Record substantially with teacher needs and school operations garnering $95 million and $148 million in 2018, respectively, according to EdSurge.1 Large industry operators have remained acquisitive through year-end, evidenced by Renaissance Learning’s three acquisitions (page three) in 2019. CONTRIBUTORS EdTech providers have also utilized M&A as a means to diversify product offerings and end-markets outside of their core competencies. Notably, Health Jacob Voorhees & Safety Institute, a leader in environmental health and safety software and Managing Director, training services, acquired Martech Media, Inc, a provider of industrial Head of Education Practice, technology e-learning training solutions (December 2019, undisclosed). Head of Global M&A 617-619-3323 Private equity firms have remained active in the industry, accounting for 52% of [email protected] transaction volume. Operators that provide disruptive platforms and institutional business models, selling directly to schools districts, have garnered David Michaels significant investment interest and premium valuations. -

Partners Group Private Equity (Master Fund)

SECURITIES AND EXCHANGE COMMISSION FORM N-Q Quarterly schedule of portfolio holdings of registered management investment company filed on Form N-Q Filing Date: 2017-02-28 | Period of Report: 2016-12-31 SEC Accession No. 0001398344-17-002471 (HTML Version on secdatabase.com) FILER Partners Group Private Equity (Master Fund), LLC Mailing Address Business Address 1114 AVENUE OF THE 1114 AVENUE OF THE CIK:1447247| IRS No.: 800270189 | State of Incorp.:DE | Fiscal Year End: 0331 AMERICAS AMERICAS Type: N-Q | Act: 40 | File No.: 811-22241 | Film No.: 17644875 37TH FLOOR 37TH FLOOR NEW YORK NY 10036 NEW YORK NY 10036 212-908-2600 Copyright © 2017 www.secdatabase.com. All Rights Reserved. Please Consider the Environment Before Printing This Document UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC 20549 FORM N-Q QUARTERLY SCHEDULE OF PORTFOLIO HOLDINGS OF REGISTERED MANAGEMENT INVESTMENT COMPANY Investment Company Act file number 811-22241 Partners Group Private Equity (Master Fund), LLC (Exact name of registrant as specified in charter) 1114 Avenue of the Americas, 37th Floor New York, NY 10036 (Address of principal executive offices) (Zip code) Robert M. Collins 1114 Avenue of the Americas, 37th Floor New York, NY 10036 (Name and address of agent for service) Registrant's telephone number, including area code: (212) 908-2600 Date of fiscal year end: March 31 Date of reporting period: December 31, 2016 Form N-Q is to be used by management investment companies, other than small business investment companies registered on Form N-5 (ss.ss. 239.24 and 274.5 of this chapter), to file reports with the Commission, not later than 60 days after the close of the first and third fiscal quarters, pursuant to rule 30b1-5 under the Investment Company Act of 1940 (17 CFR 270.30b1-5). -

Global Trends in Insurance M&A in 2014 and Beyond Looking Back on 2014: the Return of the Billion Dollar Transactions

GLOBAL TRENDS IN INSURANCE M&A IN 2014 AND BEYOND LOOKING baCK ON 2014: THE RETURN OF thE BILLION DOLLAR TRANSACTIONS In recent years, insurance companies have largely focused on improving their performance by 1. ACQUISITIONS ARE ON THE UP cutting costs amidst a slow post-global financial The big insurance groups are buying again, even those that crisis environment. However, the past two years suffered during the global economic crisis and have been have seen the tide change: the industry is now quiet on the M&A radar for some time. The number of seeking to bolster profits by embarking upon publically disclosed insurance deals in 2014 is up around both domestic and the potentially more lucrative 11 percent on 2013 from 316 to 354 (mergermarket). emerging market M&A. Economic confidence is growing and those insurance companies that suffered, yet survived, the rock bottom of the Not only are acquisitions on the up, the value is economic crisis are beginning to bounce back up, too. and consider opportunities to invest in their now well capitalized companies both internally and by external expansion. After a slow 2013, we saw with some billion dollar deals including Dai-ichi Life Insurance Company’s acquisition of Protective Life in a deal valued a significant uplift in M&A activity in the sector at US$5.7 billion, Canada Pension Plan Investment Board’s in 2014. For the first time in a number of years, (CPPIB’s) US$1.8 billion acquisition of Wilton Re, Manulife’s the industry has seen billion-dollar deals, some of US$4 billion acquisition of the Canadian operations which are identified in this paper. -

Deals, Dollars, and Disputes

Deals, Dollars, and Disputes MAXIMIZING VALUE MINIMIZING RISK A Summary of Private Equity Transactions for the Quarter Ended September 30, 2014 CONTENTS Our Process and Methodology ................................................ 1 Summary of Q3 2014 PE Firm Transaction Activity ................ 2 Volume of PE Deals Announced and Completed ......................................... 2 Top 25 PE Firm Transactions by Deal Value Completed During Q3 2014 ............................................................................................... 3 Industry Sector Transaction Analyses ........................................................... 4 Purchase Price Premium for Transactions Involving Controlling Stakes ........................................................................................... 6 PE Acquisition Type Analyses ........................................................................ 7 Featured Transactions and Insights ........................................ 8 Value Creation through Industry Consolidation ........................................... 8 In Good Company with Private Equity: LuLu*s and H.I.G. ......................... 11 Introduction We are pleased to present you with our Deals, Dollars, and Disputes report for the quarter ended September 30th, 2014. Our analysis involves a study of the merger and and acquisition transactions involving private equity firms (“PE firms”) during the Our Objective recent quarter. Our objective in preparing this report is to provide a general overview of the volume and value -

– Onex Partners to Become a Majority Investor in Newport Healthcare –

FOR IMMEDIATE RELEASE All amounts in U.S. dollars unless otherwise stated – Onex Partners to Become a Majority Investor in Newport Healthcare – Toronto, June 7, 2021 – Onex Corporation (“Onex”) (TSX: ONEX) today announced that Onex Partners V (“Onex Partners”) has agreed to acquire Newport Healthcare (“Newport” or “the company”), in partnership with the company’s management team. Newport is a leading provider in the United States of evidence-based healing centers for teens and young adults struggling with primary mental health issues. Newport offers a family-systems approach, providing gender-specific, individualized, integrated programs that encompass clinical therapy, academic support, and experiential practices. Offerings include residential treatment centers, Partial Hospitalization Programs, and Intensive Outpatient Programs. Newport nurtures the physical, psychological, social, educational, and spiritual needs of individuals, from a foundation of compassionate care, clinical expertise, and unconditional love. Newport's primary mission is to empower lives and restore families. Joe Procopio, CEO of Newport stated, “At a time when our country is in the midst of a mental health epidemic, we are thrilled to be partnering with the team at Onex, continuing our mission to be at the forefront of providing life changing care, and extending those services to more families in need.” “Newport is committed to delivering the highest quality care to its clients and addressing the nationwide shortage of mental health resources for teens and young adults by expanding access to care. We are excited to support Newport and its vision to be the leader in the sustainable healing of teens and young adults,” said Josh Hausman, an Onex Managing Director. -

Notice of Annual Meeting of Shareholders to Be Held May 13, 2021 and Information Circular

NOTICE OF ANNUAL MEETING OF SHAREHOLDERS TO BE HELD MAY 13, 2021 AND INFORMATION CIRCULAR NOTICE OF ANNUAL MEETING OF SHAREHOLDERS NOTICE IS HEREBY GIVEN that an annual meeting of the shareholders of Onex Corporation (the “Corporation”) will be held on Thursday, the 13th day of May, 2021 at 10:00 a.m. (Eastern Daylight Savings Time). Due to the continuing public health impact of the global coronavirus (COVID-19) pandemic and in consideration of the health and safety of our shareholders, colleagues and the broader community, this year’s meeting will be held in a virtual meeting format only, by way of a live audio webcast. Shareholders will be able to listen, vote and submit questions at the meeting in real time through a web-based platform instead of attending the meeting in person. You can attend the virtual meeting by joining the live audio webcast online at https://web.lumiagm.com/465190078. The purpose of the meeting is the following: 1. to receive and consider the consolidated balance sheets of the Corporation as at December 31, 2020 and the consolidated statements of earnings, shareholders’ equity and cash flows for the year then ended, together with the report of the auditor thereon; 2. to appoint an auditor of the Corporation; 3. to authorize the directors of the Corporation to fix the remuneration of the auditor; 4. to elect directors of the Corporation; 5. to consider and approve, on an advisory basis, a resolution accepting the Corporation’s approach to executive compensation; and 6. to transact such further and other business as may properly come before the meeting or any adjournment to postponement thereof. -

081231 PGLI-LPE Monthly Report

Monthly Newsletter Partners Group Listed Investments - Listed Private Equity (I) as of 31 December 2008 The Partners Group Listed Investments - Listed Private Equity fund provides efficient access to the asset class private equity overcoming the normally associated hurdle of illiquidity. The Fund invests in companies, which do mainly private equity investments and are listed on major stock exchanges. Out of an investment universe of over 240 companies world wide, the fund management actively screens a target list of around 50 companies, which fit the minimum criteria. Monthly Facts ReportKey Date of Inception: 6 September 2004 Partners Group Listed Investments – Listed Private Equity (I) Fund Currency: EUR resembled its LPX50 benchmark index by declining 13.4% in Fund Domicile: Luxembourg December. Contributing significantly to the unusually Close of Financial Year: 31 December negative mood in the listed private equity market during the Investment Advisor: Partners Group AG month were the sharp drops in the share prices of Distributions: Accumulated heavyweights SVG Capital and 3i Group. SVG Capital, a Management Fee (Net of Administration and Custodian Fees): 1.15% London-listed fund of funds, announced that the uncalled ISIN: LU0196152606 commitments vis-à-vis its private equity partner Permira will Valor: 1902989 be reduced by 40% and that the company is planning launch WKN: A0B61A a capital GBP 200 million rights issue. Those announcements Bloomberg Ticker: PGILPQI LX led to a sharp drop in the price of SVG Capital’s shares. The Total Net Assets: EUR 43.26m stock of 3i Group also came under pressure after Moody’s downgraded the company’s rating. -

ANNUAL REVIEW 2017 Land of the Giants Cycle-Tested Credit Expertise Extensive Market Coverage Comprehensive Solutions Relative Value Focus

ANNUAL REVIEW 2017 Land of the giants Cycle-Tested Credit Expertise Extensive Market Coverage Comprehensive Solutions Relative Value Focus Ares Management is honored to be recognized as Lender of the Year in North America for the fourth consecutive year as well as Lender of the Year in Europe Lender of the year in Europe Ares Management, L.P. (NYSE: ARES) is a leading global alternative asset manager with approximately $106 billion of AUM1 and offices throughout the United States, Europe, Asia and Australia. With more than $70 billion in AUM1 and approximately 235 investment professionals, the Ares Credit Group is one of the largest global alternative credit managers across the non-investment grade credit universe. Ares is also one of the largest direct lenders to the U.S. and European middle markets, operating out of twelve office locations in both geographies. Note: As of December 31, 2017. The performance, awards/ratings noted herein may relate only to selected funds/strategies and may not be representative of any client’s given experience and should not be viewed as indicative of Ares’ past performance or its funds’ future performance. 1. AUM amounts include funds managed by Ivy Hill Asset Management, L.P., a wholly owned portfolio company of Ares Capital Corporation and a registered investment adviser. learn more at: www.aresmgmt.com | www.arescapitalcorp.com The battle of the brands the US market on page 80, advisor Hamilton TOBY MITCHENALL Lane said it had received a record number EDITOR'S of private placement memoranda in 2017 – ISSN 1474–8800 LETTER MARCH 2018 around 800 – and that this, combined with Senior Editor, Private Equity faster fundraising processes, has made it dif- Toby Mitchenall, Tel: +44 207 566 5447 [email protected] ficult to some investors to make considered Special Projects Editor decisions. -

Onex Falcon BDC Fund Form 40-APP Filed 2021-06-02

SECURITIES AND EXCHANGE COMMISSION FORM 40-APP Application for exemption and other relief filed under the Investment Company Act of 1940 Filing Date: 2021-06-02 SEC Accession No. 0001193125-21-179460 (HTML Version on secdatabase.com) FILER Onex Falcon BDC Fund Mailing Address Business Address 21 CUSTOM HOUSE STREET21 CUSTOM HOUSE STREET CIK:1860424| IRS No.: 000000000 10TH FLOOR 10TH FLOOR Type: 40-APP | Act: 40 | File No.: 812-15234 | Film No.: 21988135 BOSTON MA 02110 BOSTON MA 02110 (617) 412-2700 OCP EURO CLO 2020-4 Designated Activity Co Mailing Address Business Address 930 SYLVAN AVENUE 930 SYLVAN AVENUE CIK:1865062| IRS No.: 000000000 SUITE 105 SUITE 105 Type: 40-APP | Act: 40 | File No.: 812-15234-38 | Film No.: 21988173 ENGLEWOOD CLIFFS NJ ENGLEWOOD CLIFFS NJ 07632 07632 (201) 541-2121 Falcon Strategic Partners IV, LP Mailing Address Business Address C/O FALCON INVESTMENT C/O FALCON INVESTMENT CIK:1557006| IRS No.: 000000000 | State of Incorp.:DE | Fiscal Year End: 1231 ADVISORS LLC ADVISORS LLC Type: 40-APP | Act: 40 | File No.: 812-15234-10 | Film No.: 21988145 21 CUSTOM HOUSE 21 CUSTOM HOUSE STREET, 10TH FLOOR STREET, 10TH FLOOR BOSTON MA 02110 BOSTON MA 02110 617-412-2700 Falcon Strategic Partners V, LP Mailing Address Business Address C/O FALCON INVESTMENT C/O FALCON INVESTMENT CIK:1654984| IRS No.: 000000000 | State of Incorp.:DE | Fiscal Year End: 1231 ADVISORS LLC ADVISORS LLC Type: 40-APP | Act: 40 | File No.: 812-15234-09 | Film No.: 21988144 21 CUSTOM HOUSE STREET21 CUSTOM HOUSE STREET 10TH FLOOR 10TH FLOOR BOSTON MA 02110 BOSTON MA 02110 617-412-2700 Onex Credit Lending Partners I LP Mailing Address Business Address CAYMAN CORPORATE CAYMAN CORPORATE CIK:1707973| IRS No.: 000000000 | State of Incorp.:E9 | Fiscal Year End: 1231 CENTER CENTER Type: 40-APP | Act: 40 | File No.: 812-15234-37 | Film No.: 21988172 27 HOSPITAL ROAD, 27 HOSPITAL ROAD, GEORGE TOWN GEORGE TOWN GRAND CAYMAN E9 GRAND CAYMAN E9 KY1-9008 KY1-9008 Copyright © 2021 www.secdatabase.com. -

PEI June2020 PEI300.Pdf

Cover story 20 Private Equity International • June 2020 Cover story Better capitalised than ever Page 22 The Top 10 over the decade Page 24 A decade that changed PE Page 27 LPs share dealmaking burden Page 28 Testing the value creation story Page 30 Investing responsibly Page 32 The state of private credit Page 34 Industry sweet spots Page 36 A liquid asset class Page 38 The PEI 300 by the numbers Page 40 June 2020 • Private Equity International 21 Cover story An industry better capitalised than ever With almost $2trn raised between them in the last five years, this year’s PEI 300 are armed and ready for the post-coronavirus rebuild, writes Isobel Markham nnual fundraising mega-funds ahead of the competition. crisis it’s better to be backed by a pri- figures go some way And Blackstone isn’t the only firm to vate equity firm, particularly and to towards painting a up the ante. The top 10 is around $30 the extent that it is able and prepared picture of just how billion larger than last year’s, the top to support these companies, which of much capital is in the 50 has broken the $1 trillion mark for course we are,” he says. hands of private equi- the first time, and the entire PEI 300 “The businesses that we own at Aty managers, but the ebbs and flows of has amassed $1.988 trillion. That’s the Blackstone that are directly affected the fundraising cycle often leave that same as Italy’s GDP. Firms now need by the pandemic, [such as] Merlin, picture incomplete. -

Partners Group Private Equity

SECURITIES AND EXCHANGE COMMISSION FORM NPORT-P Filing Date: 2020-08-26 | Period of Report: 2020-06-30 SEC Accession No. 0001752724-20-174334 (HTML Version on secdatabase.com) FILER Partners Group Private Equity (Master Fund), LLC Mailing Address Business Address 1114 AVENUE OF THE 1114 AVENUE OF THE CIK:1447247| IRS No.: 800270189 | State of Incorp.:DE | Fiscal Year End: 0331 AMERICAS AMERICAS Type: NPORT-P | Act: 40 | File No.: 811-22241 | Film No.: 201137479 37TH FLOOR 37TH FLOOR NEW YORK NY 10036 NEW YORK NY 10036 212-908-2600 Copyright © 2020 www.secdatabase.com. All Rights Reserved. Please Consider the Environment Before Printing This Document ITEM 1. SCHEDULE OF INVESTMENTS. The Schedule(s) of Investments is attached herewith. Partners Group Private Equity (Master Fund), LLC (a Delaware Limited Liability Company) Consolidated Schedule of Investments — June 30, 2020 (Unaudited) The unaudited consolidated schedule of investments of Partners Group Private Equity (Master Fund), LLC (the “Fund”), a Delaware limited liability company that is registered under the Investment Company Act of 1940, as amended (the “Investment Company Act”), as a non-diversified, closed-end management investment company, as of June 30, 2020 is set forth below: INVESTMENT PORTFOLIO AS A PERCENTAGE OF TOTAL NET ASSETS Copyright © 2020 www.secdatabase.com. All Rights Reserved. Please Consider the Environment Before Printing This Document Partners Group Private Equity (Master Fund), LLC (a Delaware Limited Liability Company) Consolidated Schedule of Investments — June 30, 2020 (Unaudited) Acquisition Fair Industry Shares Date Value Common Stocks (2.38%) Asia - Pacific (0.06%) Alibaba Group Holding Ltd. Technology 06/19/20 4,439 $ 957,581 APA Group Utilities 02/11/16 360,819 2,765,432 Total Asia - Pacific (0.06%) 3,723,013 North America (1.09%) American Tower Corp.