KITS Eyecare Ltd. Canadian Equity Research Consumer Products 7 February 2021

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

KITS: Good Growth, Solid Unit Economics, Aligned Management

Matt Koranda, (949) 720-7119 [email protected] Gustavo Gala, (949) 720-7116 [email protected] Sales (800) 933-6830, Trading (800) 933-6820 COMPANY NOTE | EQUITY RESEARCH | February 16, 2021 Consumer: DTC & Disruptors Initiation of Coverage Kits Eyecare Ltd. | KITS.TO - C$8.13 - TSX | Buy Stock Data 52-Week Low - High C$7.55 - C$10.20 KITS: Good Growth, Solid Unit Economics, Shares Out. (mil) 31.00 Aligned Management; Initiate at Buy Mkt. Cap.(mil) C$252.03 3-Mo. Avg. Vol. NA With its digital-first approach to selling contacts and prescription glasses/ 12-Mo.Price Target C$13.00 sunglasses, we see a long runway of growth ahead as Kits capitalizes on a Cash (mil) C$43.2 steady shift of the USD $35bn North American eyewear market into online Tot. Debt (mil) C$11.0 channels (only 13% sold online in 2021, under-penetrated vs. most consumer Revenue (C$ millions) categories). We like Kits' dual-pronged strategy of converting customers into high-visibility auto-ship programs while driving glasses growth, as these Yr Dec —2020— —2021E— —2022E— improve customer-level profitability. Moreover, management has a track- Curr Curr 1Q NA 22.5E 32.4E record of success and owns ~70% of shares. 2Q NA 32.1E 45.3E ■ 3Q 20.2A 31.8E 44.9E We initiate coverage on Kits Eyecare at Buy with a $13 PT. Kits 4Q 19.6A 30.6E 41.2E offers vision testing, prescription renewals, and products such as contact YEAR 74.5A 116.9E 163.9E lenses and eyeglasses through its website, kits.com. -

A Large Vision Network Means There's Always a Provider In

Vision Plans Network Options A large vision network means there’s always a provider in sight. UnitedHealthcare knows how important it is to find a provider you can trust who meets your lifestyle, eye care and eyewear needs. With our large national eye care network, Spectera Eyecare Networks, you can choose to get more personalized care from a private practice. Or, take advantage of the convenience retail chains offer with evening and weekend hours. Either way, we’re focused on providing you with a better eye care experience. Well-known practices and brands in our large national network include: • 20/20 Vision Center • Eye Boutique • 3 Guys Optical • EyeCare Associates • AccurateOptical • Eye Express • All About Eyes • eyecarecenter Making it easier for you • Allegany Eyecare • Eyeglass World to find a provider. • America’s Best • EyeMart Express To find the provider who best • Bard Optical • Eyetique meets your needs, login to • BJ’s Optical • For Eyes myuhcvision.com or call • Boscov’s Optical • General Vision Services 1-800-638-3120. • Clarkson Eyecare • H. Rubin Vision Centers Some providers or locations may not participate in your plan. • Co/Op Optical • Henry Ford OptimEyes • Cohen’s Fashion Optical • Horizon Eye Care • Costco Optical • Houston Eye Associates • Crown Vision Center • JC Penney Optical • Dr. Travel Family Eye Care • Midwest Vision Centers CONTINUED • MyEyeDr. • Standard Optical • National Optometry • Stanton Optical • National Vision • Sterling Optical • Nationwide Vision • SVS Vision • NUCROWN • Target Optical (not available for • Optical Shop at Meijer all members) • Optyx • Texas State Optical • Ossip Optometry • The Eye Gallery • Pearle Vision • The Hour Glass • Rosin Eyecare • Thoma & Sutton Optical • RX Optical • Today’s Vision • Sam’s Club • Virginia Eye Institute • Schaeffer Eye Centers • Vision4Less • Sears Optical (not available for • Visionmart Express all members) • Visionworks • See Inc. -

Read PDF Edition

REVIEW OF OPTOMETRY EARN 2 CE CREDITS: Positive Visual Phenomena—Etiologies Beyond the Eye, PAGE 58 ■ VOL. 155 NO. 1 January 15, 2018 www.reviewofoptometry.comwww.reviewofoptometry.com ■ ANNUAL CORNEA REPORT JANUARY 15, 2018 ■ CXL ■ EPITHELIAL DEFECTS How to Heal Persistent Epithelial Defects PAGE 38 ■ TRANSPLANTS Corneal Transplants: The OD’s Role PAGE 44 ■ INFILTRATES Diagnosing Corneal Infiltrative Disease PAGE 50 ■ POSITIVE VISUAL PHENOMENA CXL: Your Top 12 Questions —Answered! PAGE 30 001_ro0118_fc.indd 1 1/5/18 4:34 PM ĊčĞĉėĆęĊĉĆĒēĎĔęĎĈĒĊĒćėĆēĊċĔėĎēǦĔċċĎĈĊĕėĔĈĊĉĚėĊĘ ĊđĎĊċĎēĘĎČčę ċċĊĈęĎěĊ Ȉ 1 Ȉ 1 ĊđđǦęĔđĊėĆęĊĉ Ȉ Ȉ ĎĒĕđĊĎēǦĔċċĎĈĊĕėĔĈĊĉĚėĊ Ȉ Ȉ ĔēěĊēĎĊēę Ȉ͝ Ȉ Ȉ Ƭ 1 ǡ ǡǡǤ͚͙͘͜Ǥ Ȁ Ǥ ͚͙͘͜ǣ͘͘ǣ͘͘͘Ǧ͘͘͘ ĕĕđĎĈĆęĎĔēĘ Ȉ Ȉ Ȉ Ȉ Ȉ čĊĚėĎĔē̾ėĔĈĊĘĘ Ȉ Ȉ Katena — Your completecomplete resource forfor amniotic membrane pprocedurerocedure pproducts:roducts: Single use speculums Single use spears ͙͘͘ǡ͘͘͘ήĊĞĊĘęėĊĆęĊĉ Forceps ® ,#"EWB3FW XXXLBUFOBDPNr RO0118_Katena.indd 1 1/2/18 10:34 AM News Review VOL. 155 NO. 1 ■ JANUARY 15, 2018 IN THE NEWS Accelerated CXL Shows The FDA recently approved Luxturna (voretigene neparvovec-rzyl, Spark Promise—and Caution Therapeutics), a directly administered gene therapy that targets biallelic This new technology is already advancing, but not without RPE65 mutation-associated retinal dystrophy. The therapy is designed to some bumps in the road. deliver a normal copy of the gene to By Rebecca Hepp, Managing Editor retinal cells to restore vision loss. While the approval provides hope for patients, wo new studies highlight the resulted in infection—while tradi- the $425,000 per eye price tag stands as pros and cons of accelerated tional C-CXL has a reported inci- a signifi cant hurdle. -

Case 1:21-Cv-06966 Document 1 Filed 08/18/21 Page 1 of 38

Case 1:21-cv-06966 Document 1 Filed 08/18/21 Page 1 of 38 UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF NEW YORK 1-800 CONTACTS, INC. ) ) Plaintiff, ) ) v. ) Case No. ________________ ) JAND, INC. d/b/a WARBY PARKER ) ) Jury Trial Demanded Defendant. ) COMPLAINT Plaintiff 1-800 Contacts, Inc. (“1-800 Contacts”) makes the following allegations in support of its Complaint against Defendant JAND, Inc., d/b/a Warby Parker (“Warby Parker”): NATURE OF THE ACTION 1. This is an action to stop and remedy Defendant Warby Parker’s continuing trademark infringement, unfair competition, and deceptive advertising practices. Plaintiff 1-800 Contacts is a well-known pioneer in the online contact lens marketplace. Over the past three decades, 1-800 Contacts has expended hundreds of millions of dollars on advertising, marketing, and promotion to cultivate strong consumer recognition of its brand, services, and trademarks. 2. 1-800 Contacts’ investments and decades-long commitment to its customers has paid off, as the company now serves millions of customers. Indeed, between June 1, 2020, and June 30, 2021, alone, the 1800contacts.com website averaged more than 1.5 million unique visitors monthly. Case 1:21-cv-06966 Document 1 Filed 08/18/21 Page 2 of 38 3. 1-800 Contacts is an online—rather than a brick-and-mortar—retailer, so millions of customers and prospective customers reach 1-800 Contacts by navigating to the 1800contacts.com website. In an effort to navigate to its online store at the 1800contacts.com website, many consumers type “1800 Contacts,” “1 800 Contacts,” “1800contacts.com,” “1800contacts,” or other of 1-800 Contacts’ trademarks as search terms in search engines such as Google. -

Fielmann Ag Company Report

MASTER IN FINANCE FIELMANN AG COMPANY REPORT EUROPEAN EYEWEAR RETAIL 4 JANUARY 2021 STUDENT: JAN-PHILIP JANSEN [email protected] Fashionable Glasses for Everyone Recommendation: BUY Fielmann Strengthens its Position in the Industry Price Target FY21: 79.01 € Price (as of 3-Jan-21) 66.45 € Our recommendation is to BUY Fielmann AG considering a Bloomberg: FIE target price of €79.01 as of 31.12.2021 reflected in an upside potential of 20.69% (thereof €1.19 expected dividend) to the current 52-week range (€) 41.90-76.25 Market Cap (€m) 5,581 share price of €66.45. Outstanding Shares (m) 84,000 Source: Thomson Reuters EIKON Market trends like an ever aging population, digitalization and industry consolidation set a solid foundation for further sustainable growth. We think Fielmann will be able to re-accelerate top-line growth back to 5%, achieved by a consistent realization of Fielmann’s corporate strategy “Vision 2025”. High Liquidity and strong Free Cash Flows provide sufficient funding for the renovation and internationalization Source: Yahoo Finance strategy. (Values in € millions) 2019 2020E 2021F The COVID-19 pandemic is currently the biggest threat for Revenues 1,524 1,385 1,556 the eyewear industry but at the same time a huge opportunity for EBITDA 410 328 382 EBIT 281 178 244 Fielmann due to its strong financial position. In contrast to other Capex 185 155 215 analysts, we expect Fielmann to be one of the post-crisis winners. FCF 126 118 68 Source: Annual Report 2019, Analyst Estimation We believe that the broad market might underestimate future profitabilty arising from further market consolidation. -

Kits Eyecare Ltd. Annual Information Form

KITS EYECARE LTD. ANNUAL INFORMATION FORM For the year ended December 31, 2020 Dated March 29, 2021 TABLE OF CONTENTS INTRODUCTION ............................................................................................................................................. 1 CAUTION REGARDING FORWARD-LOOKING INFORMATION AND STATEMENTS ......................................... 1 INDUSTRY METRICS ....................................................................................................................................... 2 CORPORATE STRUCTURE .............................................................................................................................. 3 Name, Address and Incorporation ........................................................................................................... 3 Intercorporate Relationships .................................................................................................................... 3 GENERAL DEVELOPMENT OF THE BUSINESS ................................................................................................ 4 Overview of the Business ......................................................................................................................... 4 Three Year History .................................................................................................................................... 7 RISK FACTORS ............................................................................................................................................... -

Luxottica (Borsa Italiana: LUX)

Luxottica (Borsa Italiana: LUX) NOTE: ADRs also trade under “LUX” on the NYSE priced in U.S. Dollars Gross EBITDA EBIT 71% 71% 71% 70% 70% 69% 70% 68% 68% 68% 68% 66% 66% 66% 65% 66% 65% 65% 24% 23% 24% 21% 22% 21% 20% 20% 20% 20% 19% 19% 18% 18% 19% 18% 17% 17% 16% 17% 17% 16% 16% 16% 16% 15% 15% 15% 15% 14% 14% 14% 13% 13% TABLE OF CONTENTS DURABILITY 2 SINGULAR DILIGENCE MOAT 4 Geoff Gannon, Writer Quan Hoang, Analyst QUALITY 6 Tobias Carlisle, Publisher CAPITAL ALLOCATION 8 VALUE 11 Luxottica (Borsa Italiana: LUX) is a Global Maker and GROWTH 13 Seller of Sunglasses and Eyeglasses MISJUDGMENT 15 FUTURE 17 APPRAISAL 20 OVERVIEW NOTES 22 Luxottica is a vertically integrated eyewear company. Although founded in Italy, it now gets much of its sales and profits from the United States. And although founded as a part maker for prescription eyeglass frames (optical glasses) it now gets much of its sales and profits from sunglasses. The company can’t really be referred to as either a producer or a retailer. Luxottica is truly vertically integrated. Last year, 59% of the company’s sales came from its own stores. And much of the products sold in its own stores is produced by Luxottica itself. The two constants in Luxottica’s history have been the focus on eyewear and the leadership of Leonardo Del Vecchio. Luxottica gets 59% of its revenue from sales made in its own stores. Del Vecchio moved to Agordo, Italy in by distributing its own frames. -

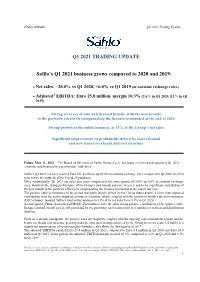

Q1 2021 TRADING UPDATE Safilo's Q1 2021 Business Grows Compared to 2020 and 2019

Press release Q1 2021 Trading Update Q1 2021 TRADING UPDATE Safilo’s Q1 2021 business grows compared to 2020 and 2019: Net sales: +20.0% vs Q1 2020, +6.0% vs Q1 2019 (at constant exchange rates) Adjusted1 EBITDA: Euro 25.8 million, margin 10.3% (2.6% in Q1 2020, 8.1% in Q1 2019) Strong recovery of own and licensed brands, with the new brands in the portfolio effectively compensating the licenses terminated at the end of 2020 Strong growth of the online business, at 13% of the Group’s net sales Significant improvement in profitability driven by sales rebound and now leaner overheads and cost structure Padua, May 11, 2021 – The Board of Directors of Safilo Group S.p.A. has today reviewed and approved Q1 2021 economic and financial key performance indicators. Safilo’s Q1 2021 net sales reached Euro 251.4 million, up 20.0% at constant exchange rates compared to Q1 2020, the first to be hit by the outbreak of the Covid-19 pandemic. More meaningfully, Q1 2021 net sales also grew compared to the same quarter of 2019, up 6.0% at constant exchange rates, thanks to the strong performance of the Group’s own brands and core licenses, and to the significant contribution of the new brands in the portfolio effectively compensating the licenses terminated at the end of last year. The positive sales performance of the period was again largely driven by the United States and by a better than expected contribution from the newly acquired ecommerce business, which, coupled with the growth of Smith’s direct-to-consumer (D2C) channel, boosted Safilo’s total online business to 13% of its net sales from 5.9% in Q1 2020. -

Universita' Degli Studi Di Padova

UNIVERSITA’ DEGLI STUDI DI PADOVA DIPARTIMENTO DI SCIENZE ECONOMICHE ED AZIENDALI “M.FANNO” CORSO DI LAUREA MAGISTRALE IN BUSINESS ADMINISTRATION TESI DI LAUREA “MERGERS AND ACQUISITIONS AS A WAY TO CREATE VALUE: ANALYSIS OF THE ESSILOR-LUXOTTICA CASE AND HOW THE EYEWEAR INDUSTRY IS CHANGING” RELATORE: CH.MO PROF. ANDREA FURLAN LAUREANDA: FRANCESCA MARTINI MATRICOLA N. 1132489 ANNO ACCADEMICO 2017 – 2018 Il candidato dichiara che il presente lavoro è originale e non è già stato sottoposto, in tutto o in parte, per il conseguimento di un titolo accademico in altre Università italiane o straniere. Il candidato dichiara altresì che tutti i materiali utilizzati durante la preparazione dell’elaborato sono stati indicati nel testo e nella sezione “Riferimenti bibliografici” e che le eventuali citazioni testuali sono individuabili attraverso l’esplicito richiamo alla pubblicazione originale. Firma dello studente ________________ Un ringraziamento speciale va alla mia famiglia, per avermi supportato e permesso di arrivare fin qui, sempre sostenendomi e credendo in me, se oggi sono riuscita a raggiungere questo traguardo è grazie a loro. In particolare ringrazio mia madre per la forza e la determinazione che mi ha trasmesso nei momenti in cui mi stavo perdendo, il suo appoggio è stato fondamentale in questo percorso. Vorrei inoltre ringraziare il Professor Furlan Andrea, relatore di questa tesi, per avermi guidata nel percorso di stesura di questo lavoro, permettendomi di appassionarmi all’argomento giorno dopo giorno. Table of contents INTRODUCTION -

Annual Report

ANNUAL REPORT CENTRE FOR INTERNATIONAL GOVERNANCE INNOVATION ANNUAL REPORT 2016 Copyright © 2016 by the Centre for International Governance Innovation Photo and image credits: Carol Bonnett, Denis Chatterton, Johannes Granseth, Trevor Hunsberger, Tim Hutchinson, iStock, Lisa Malleck, Lisa Sakulensky, Jeff Stoub, TEPAV, Som Tsoi, UN Photo (Fred Fath) and Emilia Zibeal. This work is licensed under a Creative Commons Attribution, Non- commercial, No Derivatives License. To view this license, visit: www.creativecommons.org/licenses/by-nc-nd/3.0/ For re-use or distribution, please include this copyright notice. ii CIGI Annual Report 2016 • Overview ABOUT CIGI The Centre for International Governance Innovation (CIGI) is an independent, non-partisan think tank on international governance. Led by experienced practitioners and distinguished academics, CIGI supports research, forms networks, advances policy debate and generates ideas for multilateral governance improvements. With an active agenda of research, events and publications, CIGI’s interdisciplinary work includes collaboration with policy, business and academic communities around the world. CIGI was founded in 2001 by Jim Balsillie, then Co-CEO of Research In Motion (BlackBerry), and Canadian Prime Minister Justin Trudeau on April 22, 2016, at the historic signing of the Paris Agreement, agreed to at the twenty-first session of the Conference of the collaborates with and gratefully acknowledges support from Parties (COP21). CIGI experts from all three programs were active at COP21. a number of strategic partners, in particular the Government of Canada and the Government of Ontario. For more information, please visit www.cigionline.org. Vision CIGI strives to be the world’s leading think tank on international governance, with recognized impact on significant global problems. -

BBG Jan 2014

BlockBuster1213SK:Layout 1 12/18/13 11:08 AM Page 1 VOL. XXXIX NO. 1 JANUARY 2014 Practice Management and Purchasing Services for Independent Eye Care Professionals BBG Bottom Line Block Notes What’s Your Value Proposition? t’s the new year, with all of its hope and prom- hat sets you apart from the competition? Many eye care professionals will say Iise for greater productivity, efficiency and prof- Wthat it’s the quality of their products and professional services. So while you are itability before us. The Block Business Academy not trying to compete on price, it’s still important for you and your staff to under- by the Beach provides an opportunity to help stand how to articulate the value of the services and products you provide. you realize those goals with top-quality educa- Your optical dispensary provides continuity from the start of the process to tion for eye care professionals and staff mem- the end. Unlike a chain, the eye care professional or staff member who helps with bers. The continuing education covers clinical frame selection and measurements will likely be the one who dispenses the final eyewear. It is important to explain to patients that their measurements are cus- education as well as practice management Michael Block hours. In addition, Block Business Group ven- tomized and personalized at a higher level. You back up the product, and in fact, dors will be on hand with tremendous purchasing opportunities— provide free service for the useful life of the eyewear. and members have a chance to share business strategies in a There’s tremendous value in that kind of service—but that value must be made relaxing atmosphere. -

See Through This Optical Illusion Warby Parker Inc

IPO RESEARCH 9/8/21 Warby Parker Direct Listing: See Through This Optical Illusion Warby Parker Inc. (WRBY) is set to debut as a public company via a direct listing on September 29. For its last round of funding, the firm fetched a roughly $3 billion valuation. At this valuation the stock earns our Very Unattractive rating. At first glance, it may seem like Warby Parker is a highly profitable company, given its well-known brand and early entrance into the ecommerce eyewear space, but we urge investors to see through this optical illusion, as the company wasn’t profitable in 2020 and barely broke even in 2019. With an expected valuation of $3 billion, we don’t think investors should expect to make any money in this stock. We believe the stock is worth as little as ~$600 million. A $3 billion valuation implies that Warby Parker will achieve some very optimistic milestones, including reversing a downward trend in profits, growing revenue by more than 600%, and generating more revenue than the current eyewear market leader, Vision Source. Despite a strong brand and visibility in the marketplace, Warby Parker maintains a very small share of the highly fragmented eyewear market and to make matters worse, consumers are reluctant to purchase eyeglasses online, instead favoring in-store purchases. Our IPO research aims to provide investors with more reliable fundamental research. Learn more about the best fundamental research Ecommerce Strategy Is Flawed Warby Parker’s initial focus on ecommerce-based eyewear may have been novel in 2010, but this concept hasn’t lived up to the success ecommerce has seen in other industries.