Uniform Estate Tax Apportionment Act

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

G L O S S a R Y

G L O S S A R Y A Administrator: A court appointed person or corporation in charge of managing the estate of a person who dies without leaving a will. Administrators have the same duties as Executors. In Minnesota, the administrator or executor is called the Personal Representative. Affiant: A person who makes an oath or affirmation and acknowledges the same in writing. In Minnesota this is usually done before a notary public. Affidavit: A voluntary written statement of facts confirmed by the oath or affirmation of the affiant. Affidavit of Collection of Personal Property: A sworn, notarized statement, used to collect assets of a small estate without going through the probate process. (aka Affidavit of a Small Estate). Agent: A person authorized by another to act for him. AKA: Also Known As (also lower case: aka). Amendment: A change or modification. See Codicil. Ancestor (an Ascendant): A deceased relative such as a parent or grandparent from whom one is descended. Ancillary Administration: A secondary administration in a state where the decedent owned property and which is not the state where the decedent was domiciled. Annuity: The right to receive fixed sums of money at regular intervals. Appoint: To designate and empower particular person(s) with authority to perform specified duties. Appraisal: An evaluation by disinterested and qualified persons as to the value of assets. Assets: All property of a person, corporation or estate of a decedent; real or personal, tangible or intangible. Attorney-in-fact: A person with the power granted under a power of attorney. B Beneficiary: An entity who benefits from the act of another. -

Wills--Deceased Residuary Legatee's Share Held Not to Pass by Way Of

St. John's Law Review Volume 38 Number 1 Volume 38, December 1963, Number Article 11 1 Wills--Deceased Residuary Legatee's Share Held Not to Pass by Way of Intestacy Where It Is Clearly Manifested That Surviving Residuary Legatees Should Share in the Residuum (In re Dammann's Estate, 12 N.Y.2d 500 (1963)) St. John's Law Review Follow this and additional works at: https://scholarship.law.stjohns.edu/lawreview This Recent Development in New York Law is brought to you for free and open access by the Journals at St. John's Law Scholarship Repository. It has been accepted for inclusion in St. John's Law Review by an authorized editor of St. John's Law Scholarship Repository. For more information, please contact [email protected]. ST. JOHN'S LAW REVIEW [ VOL. 38 argument against such an extension was rejected. 52 Likewise, the presence of a compensation fund for prisoners was held not necessarily to preclude prisoner suits under the FTCA.53 The Court found the compensation scheme to be non-comprehensive.5 4 The government's contention that variations in state laws might hamper uniform administration of federal prisons, as it was feared they would with the military, was rejected. Admitting that prisoner recoveries might be prejudiced to some extent by variations in state law, the Court regarded no recovery at all as a more serious prejudice to the prisoner's rights.55 In this connection, it is interesting to consider the desirability of spreading tort liability in the governmental area.5" The impact of the principal case is, in some respects, clear. -

Wills and Trusts (4Thed

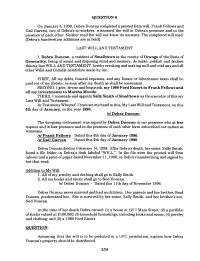

QUESTION 6 On January 5, 1990, Debra Duncan completed a printed form will. Frank Fellows and Gail Garven, two of Debra's co-workers, witnessed the will in Debra's presence and in the presence of each other. Neither read the will nor knew its contents. The completed will read: [Debra's handwritten additions are in bold] LAST WILL AND TESTAMENT I, Debra Duncan, a resident of Smalltown in the county of Orange of the State of Generality, being of sound and dsposing mind and memory, do make, publish and declare this my last WILL AND TESTAMENT, hereby revoking and making null and void any and all other Wills and Codicils heretofore made by me. FIRST, All my debts, funeral expenses, and any Estate or Inheritance taxes shall be paid out of my Estate, as soon after my death as shall be convenient. SECOND, I give, devise and bequeath, my 1989 Ford Escort to Frank Fellows and all my investments to Martha Murdo. THIRD, I nominate and appoint Sally Smith of Smalltown as the executor of this my Last Wlll and Testament. In Testimony Whereof, I have set my hand to this, My Last Will andTestarnent, on this 5th day of January, in the year 1990. IS/ Debra Duncan The foregoing instrument was signed by Debra Duncan in our presence who at her request and in her presence and in the presence of each other have subscribed our names as witnesses. Is/ Frank Fellows Dated this 5th day of January 1990. Is1 Gail Garven Dated this 5th day of January 1990. -

Some Basic Facts About Wills

SWEET& MAIER, S.C. SOME BASIC FACTS ABOUT WILLS What Property Will Pass Under Your Will? All property which is in your name alone will be disposed of by your Will, which would include, for example, a bank account, stock, real estate, your automobile, your television, household items and similar items held in your name alone. If you own an undivided interest in property with another, your undivided interest will pass under your Will, but not if the property which you own with another is joint with right of survivorship, or is owned by you and your spouse as marital property, with right of survivorship. Assets Which Do Not Pass Under Your Will: Property held in joint names with rights of survivorship will pass to the survivor (i.e. if the title to your house is held by you and your spouse as survivorship marital property). Life insurance payable to named beneficiaries will pass to the beneficiaries. Pension, retirement or other employee benefits payable to named beneficiaries will pass to the named beneficiaries. U.S. Savings Bonds which are in joint names will pass to the survivor. Those payable on death to a named beneficiary will pass to the named beneficiaries. If the named beneficiary in any of the above examples is “your estate” of your “executors and administrators”, then this property will pass under your Will. GENERAL DISPOSITION PLANS With property which will pass under your Will, it is not necessary that you name or describe each item. Your assets can be described by groups, categories or in any other way which adequately delineates your property. -

The Uniform Probate Code Upends the Law of Remainders

Michigan Law Review Volume 94 Issue 1 1995 The Uniform Probate Code Upends the Law of Remainders Jesse Dukeminier University of California, Los Angeles Follow this and additional works at: https://repository.law.umich.edu/mlr Part of the Estates and Trusts Commons, and the Legislation Commons Recommended Citation Jesse Dukeminier, The Uniform Probate Code Upends the Law of Remainders, 94 MICH. L. REV. 148 (1995). Available at: https://repository.law.umich.edu/mlr/vol94/iss1/4 This Article is brought to you for free and open access by the Michigan Law Review at University of Michigan Law School Scholarship Repository. It has been accepted for inclusion in Michigan Law Review by an authorized editor of University of Michigan Law School Scholarship Repository. For more information, please contact [email protected]. THE UNIFORM PROBATE CODE UPENDS THE LAW OF REMAINDERS Jesse Dukeminier* Nothing is more settled in the law of remainders than that an indefeasibly vested remainder is transmissible to the remainder man's heirs or devisees upon the remainderman's death. Thus, where a grantor conveys property "to A for life, then to B and her heirs," B's remainder passes to B's heirs or devisees if B dies during the life of A. Inheritability of vested remainders was recognized in the time of Edward I, and devisability was recognized with the Stat ute of Wills in 1540. Section 2-707 of the Uniform Probate Code (UPC),1 adopted in 1990, upends this law. In a comprehensive remake of the law of remainders, section 2-707 provides that, unless the trust instrument provides otherwise, all fu.ture interests in trust are contingent on the beneficiary's surviving the distribution date. -

Inheritance Taxes

Pfeufer v. Cyphers, No. 141, September Term 2004. Opinion by Bell, C.J. WILLS - INHERITANCE TAXES A testator may direct inheritance taxes to be paid from the entire residuary estate prior to apportionment among residuary legatees even when a statute exempts some of the residuary legatees from the payment of inheritance taxes. IN THE COURT OF APPEALS OF MARYLAND No. 141 September Term, 2004 ______________________________________ BRUCE PFEUFER v. PAMELA J. CYPHERS, PERSONAL REPRESENTATIVE OF THE ESTATE OF JAMES RUSSELL HOFFMAN ______________________________________ Bell, C.J. Raker *Wilner Cathell Harrell Battaglia Greene, JJ. ______________________________________ Opinion by Bell, C.J. ______________________________________ Filed: March 19, 2007 *Wilner, J., now retired, participated in the hearing and conference of this case while an active member of this Court; after being recalled pursuant to the Constitution, Article IV, Section 3A, he also participated in the decision and adoption of this opinion. The instant case involves the interpretation of language in the Last Will and Testament of James Russell Hoffman, the testator, and the effect of that language in light of Maryland Code (1988, 2004 Repl. Vol.), § 7-203(b)(2) of the Tax-General Article.1 The testator left his residuary estate to four people, three of whom are relatives of the testator and, therefore, pursuant to the above statute, each of whom is exempt from paying inheritance taxes on his or her share of the residuary estate. That is not the case with Bruce Pfeufer, the fourth residuary legatee, the appellant. He is not a relative of the testator and, thus, he does not enjoy any such exemption. -

Failure of Gifts by Will

Failure of Gifts by Will This month’s CPD will examine the many reasons why a gift made by Will may fail. This paper will look at the most common reasons for the failure of gifts, listed below, but practitioner’s should be aware that this list is non-exhaustive and gifts may fail for other reasons; including a contingency for a gift not being met, as a matter of public policy, or even because a condition attached to a gift is void. MAIN REASONS A GIFT MAY FAIL A gift may fail for one of the following main reasons: The beneficiary or a spouse or civil partner of the beneficiary is an attesting witness The divorce or dissolution of a marriage or civil partnership between the testator and the beneficiary Lapse Ademption Abatement Uncertainty The beneficiary is guilty of the unlawful killing of the testator The beneficiary disclaims their gift BENEFICIARY OR THEIR SPOUSE IS AN ATTESTING WITNESS This is the most well-known reason for the failure of a gift. Section 15 of the Wills Act 1837 deprives an attesting witness and their spouse or civil partner from receiving any benefit under the Will which they attest. If a beneficiary or their spouse is an attesting witness the attestation itself will be valid and this will not cause the Will to fail; only the gift to the witness or their spouse shall be void. There are some key exceptions to this general rule: If a beneficiary was not married to the witness at the time the attestation took place but married the witness afterwards then they will not be deprived of their benefit. -

Estate Administration – a Guide for Beneficiaries

Estate Administration – A Guide for Beneficiaries While an executor of an estate will generally have If there is no Will, then an application is made to have regular contact with and advice from the lawyer someone (usually a spouse or child of the deceased) assisting them administer an estate, a beneficiary appointed administrator of the estate under ‘Letters of named in a Will often doesn’t have the same Administration.’ This application will generally take information available to them. longer to obtain than a Grant of Probate as a certificate from Births, Deaths and Marriages is When lawyers are instructed by executors to assist required along with confirmation that an with the administration of an estate, their duty is advertisement has appeared in the Law Society’s primarily to the executor. This limits the amount of publication before the application can be made. information or advice we can give to beneficiaries, especially in situations where there are conflicting Sometimes it is necessary to wait for a Death views among family. Certificate to become available before an application can be made. It usually takes two weeks for a Death Often beneficiaries may have a different idea of the Certificate to become available. nature of the work required to administer an estate or the time it can take for money to be available to them. 3. Collecting assets and paying debts The following is a brief outline of the process which is Lawyers write to all the banks and other institutions followed. where the deceased held assets to update them. Bank accounts are frozen at that point so that no further 1. -

Glossary of Terms

GLOSSARY OF TERMS Administrator/Administratrix A person appointed by the Register of Wills or the Court to gather and distribute assets of persons who died without leaving a will. Affidavit A written or printed declaration or statement of facts confirmed by the oath or affirmation of the party making it. Beneficiary A person who receives property or other benefits. Heir at law, in an intestate estate; devisee, in a testate estate. Claim A liability of the decedent, whether arising in contract, tort, or otherwise, and funeral expenses. The term does not include expenses of administration or estate, inheritance, succession, or other death taxes. Codicil A supplement or addition to a will. It may explain, modify, add to, subtract from, qualify, alter, restrain, or revoke provisions in a will. It must be executed with the same formalities as a will. Creditor An individual or entity to which an estate may be indebted. Decedent A deceased person; the person who died. Disclaimer The rejection, refusal, or renunciation of a claim to property. Domicile A person’s usual place of dwelling and shall be synonymous with “residence.” Elective Share The surviving spouse’s right to take a statutory share of the decedent’s estate rather than under a will or the intestate laws. Estate Property of a decedent that is the subject of administration. This does not include assets held in trust or assets with a living beneficiary. Executor/Executrix A person nominated by the testator (maker) of a will to carry out the provisions in the will. Filing/Registering a Will The filing of an original will at the Register of Wills office after an individual’s death. -

The Intestacy Manual 2016

THE INTESTACY MANUAL 2016 FOR PROCEEDINGS IN TEXAS PROBATE COURTS STEVE M. KING JUDGE TARRANT COUNTY PROBATE COURT NUMBER ONE FORT WORTH , TEXAS REVISION DATE – OCTOBER 2015 DIVISION OF PROPERTY UPON INTESTACY IN TEXAS I. COMMUNITY PROPERTY (§201.0032, Texas Estates Code) 1. With Surviving Spouse, and Children (or their descendants): A) where Surviving Spouse and Decedent are parents of all Children Surviving Spouse ------------------------------------------------------------------------ All B) where Surviving Spouse and Decedent are NOT the parents of all Children: Surviving Spouse retains Surviving Spouse’s ½, takes NONE of Decedent's ½ Children or their descendants -------------------------- take ALL of Decedent’s ½ ------------------------------------------------------------------------------ 2. With Surviving Spouse only: Surviving Spouse---------------------------------------- All 3. With Children or their descendants only Children or their descendants ---------- All II. SEPARATE PROPERTY 1. With Surviving Spouse (§201.002, Texas Estates Code) A) With Children or their descendants 1) Pers Prop: a) Surviving Spouse -------------------------------------------------- ⅓ b) Children and their descendants ----------------------------------- ⅔ 2) Real Prop: a) Surviving Spouse has life interest in ---------------------------- ⅓ (with remainder to Children and their descendants) b) Children and their descendants have fee in --------------------- ⅔ & remainder in ------------------------------------ ⅓ B) Without Children or their descendants -

What's Wrong with Partial Intestacy? Richard F

CORE Metadata, citation and similar papers at core.ac.uk Provided by Marquette University Law School Marquette Law Review Volume 100 Article 8 Issue 4 Summer 2017 What's Wrong with Partial Intestacy? Richard F. Storrow School of Law, City University of New York Follow this and additional works at: http://scholarship.law.marquette.edu/mulr Part of the Estates and Trusts Commons, and the Property Law and Real Estate Commons Repository Citation Richard F. Storrow, What's Wrong with Partial Intestacy?, 100 Marq. L. Rev. 1387 (2017). Available at: http://scholarship.law.marquette.edu/mulr/vol100/iss4/8 This Article is brought to you for free and open access by the Journals at Marquette Law Scholarly Commons. It has been accepted for inclusion in Marquette Law Review by an authorized editor of Marquette Law Scholarly Commons. For more information, please contact [email protected]. 39332-mqt_100-4 Sheet No. 137 Side A 07/17/2017 08:32:28 ͵ʹ͵͵Ǧͷ ͷǦͶǦͻͶǦͲͷʹ͵ͻʹȋȌ ȀͳͶȀʹͲͳǣͲͶ WHAT’S WRONG WITH PARTIAL INTESTACY? Ǥȗ This article questions whether wills law’s disapproval of partial intestacy rests on defensible assumptions about testamentary intent. After examining the causes of and antidotes to partial intestacy, I make three primary points. First, the presumption against intestacy applies only to wills that contain an ambiguous bequest of the residue. Second, the law’s disapproval of partial intestacy is due in part to its failure to make an important distinction between testamentary intention and dispositive intention. Third, a theory of passive intention, heretofore barely alluded to in the law of wills, supplies the necessary validation of partially intestate estates. -

Last Will and Testament Of

LAST WILL AND TESTAMENT OF _________________________ PERSONAL INFORMATION I, NAME OF TESTATOR, a resident of {STATE}, county of {COUNTY} declare that this is my will. My Social Security Number is {SOCIAL SECURITY}. REVOCATION OF PREVIOUS WILLS FIRST: I revoke all wills and codicils that I have previously made. MARITAL STATUS SECOND: I am married to {SPOUSE'S NAME}. CHILDREN THIRD: I have the following child(ren) now living: {NAME OF CHILDREN}. FAILURE TO LEAVE PROPERTY FOURTH: If I do not leave property in this will to one or more of the children or grandchildren whom I have identified above, my failure to do so is intentional. DEFINITIONS FIFTH: As used in this will, the term "specific bequest" refers to a gift of specifically identified property that I leave in this will. The term "residuary estate" refers to all property subject to this will that is not passed by specific bequest or that is specifically left to or becomes a part of my residuary estate when a beneficiary of a specific bequest fails to survive me. The term "residuary bequest" refers to a gift of all or a portion of my residuary estate. SPECIFIC BEQUESTS OF PROPERTY SIXTH: I give {SPECIFIC PROPERTY BEQUESTED} to {NAME OF BENEFICIARIES FOR SPECIFIC BEQUEST}. However, if {NAME OF BENEFICIARIES FOR SPECIFIC BEQUEST} does not survive me, the living children of {NAME OF BENEFICIARIES FOR SPECIFIC BEQUEST} shall take the property. If there are no living children, the property shall go to {ALTERNATE BENEFICIARY FOR SPECIFIC BEQUEST}. RESIDUARY ESTATE SEVENTH: I give my residuary estate to {BENEFICIARY FOR RESIDUARY ESTATE}.