Constructing and Regenerating

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

May CARG 2020.Pdf

ISSUE 30 – MAY 2020 ISSUE 30 – MAY ISSUE 29 – FEBRUARY 2020 Promoting positive mental health in teenagers and those who support them through the provision of mental health education, resilience strategies and early intervention What we offer Calm Harm is an Clear Fear is an app to Head Ed is a library stem4 offers mental stem4’s website is app to help young help children & young of mental health health conferences a comprehensive people manage the people manage the educational videos for students, parents, and clinically urge to self-harm symptoms of anxiety for use in schools education & health informed resource professionals www.stem4.org.uk Registered Charity No 1144506 Any individuals depicted in our images are models and used solely for illustrative purposes. We all know of young people, whether employees, family or friends, who are struggling in some way with mental health issues; at ARL, we are so very pleased to support the vital work of stem4: early intervention really can make a difference to young lives. Please help in any way that you can. ADVISER RANKINGS – CORPORATE ADVISERS RANKINGS GUIDE MAY 2020 | Q2 | ISSUE 30 All rights reserved. No part of this publication may be reproduced or transmitted The Corporate Advisers Rankings Guide is available to UK subscribers at £180 per in any form or by any means (including photocopying or recording) without the annum for four updated editions, including postage and packaging. A PDF version written permission of the copyright holder except in accordance with the provision is also available at £360 + VAT. of copyright Designs and Patents Act 1988 or under the terms of a licence issued by the Copyright Licensing Agency, Barnard’s Inn, 86 Fetter Lane, London, EC4A To appear in the Rankings Guide or for subscription details, please contact us 1EN. -

R Egeneration C Onstruction

Regeneration Annual Report 2016 Construction About us Morgan Sindall Group is a leading UK construction and regeneration group. We offer support at every stage of a project’s life cycle through our six divisions of Construction & Infrastructure, Fit Out, Property Services, Partnership Housing, Urban Regeneration and Investments. Construction Regeneration Our services include design, We work in close new build construction, partnership with land infrastructure works, owners, local authorities refurbishment and property and housing associations maintenance in the commercial to regenerate cities with and public sectors. Our multi-phased, mixed-use construction teams work developments. New housing, on projects of all sizes community buildings, shops, and complexity, either leisure facilities and public standalone or through spaces help stimulate local framework agreements economies and provide and strategic alliances. long-term social benefits. FRONT COVER: The Word, a new state-of-the-art Revenue Revenue cultural centre in South Shields containing a library, exhibition space, gaming area, ‘FabLab’ with 3D printers, IT suite, café £ 2.0bn £ 0.6bn and rooftop space. Delivered by Urban Regeneration in partnership 2015: £1.9bn 2015: £0.5bn with South Tyneside Council. Find out more about the Our activities touch the lives of a wide range of stakeholders. We have therefore Group from our website decided to embark on a new approach to our annual report, integrating financial at morgansindall.com. and non-financial reporting within our operating -

Louisiana Connection United Kingdom

LOUISIANA CONNECTION UNITED KINGDOM RECENT NEWS In January 2015, Louisiana Gov. Bobby Jindal visited the United Kingdom as part of an economic development effort. While there, he also addressed the Henry Jackson Society regarding foreign policy. FOREIGN DIRECT INVESTMENT The United Kingdom is the most frequent investor in Louisiana, with 31 projects since 2003 accounting for over $1.4 billion in capital expenditure and over 2,200 jobs. UK has invested many business service projects in Louisiana. Hayward Baker, a geotechnical contractor and a subsidiary of the UK-based Keller Group, has opened a new office in New Orleans to support customers and projects along the Gulf Coast. Atkins, a design an engineering consultancy, has opened a new office in Baton Rouge, the office aims to increase the firm’s support capabilities for projects throughout Louisiana. CONTACT INFORMATION Tymor Marine, an energy consultancy company, has opened a SANCHIA KIRKPATRICK new office in Kaplan, Louisiana, The opening will serve customers Chief Representative, United Kingdom operating in the Gulf of Mexico. [email protected] T +44.0.7793222939 In June 2013, Hunting Energy Services completed a $19.6 million investment in its new Louisiana facility. JAMES J. COLEMAN, JR., OBE Great Britain Louisiana companies have also established a presence in the UK. www.gov.uk/government/work/usa Including 15 direct investments in the U.K. since 2003 that have T 504.524.4180 resulted in capital expenditures totaling $253 million and the JUDGE JAMES F. MCKAY III creation of 422 jobs. Honorary Consul, Ireland [email protected] T 504.412.6050 TRADE EXPORTS IMPORTS The U.K. -

FT UK 500 2011 A-Z Company UK Rank 2011 3I Group 94 888 Holdings 485 Abcam 250 Aberdeen Asset Management 109 Admiral Group 72 A

FT UK 500 2011 A-Z UK rank Company 2011 3I Group 94 888 Holdings 485 Abcam 250 Aberdeen Asset Management 109 Admiral Group 72 Advanced Medical Solutions 488 Aegis Group 127 Afren 138 African Barrick Gold 118 African Minerals 131 Aggreko 69 Albemarle & Bond 460 Allied Gold 306 Amec 75 Amerisur Resources 426 Amlin 124 Anglo American 11 Anglo Pacific Group 327 Anglo-Eastern Plantations 370 Anite 445 Antofagasta 29 Aquarius Platinum 136 Archipelago Resources 346 Arm Holdings 42 Ashley (Laura) 476 Ashmore 112 Ashtead Group 206 Asian Citrus 263 Asos 171 Associated British Foods 41 Assura 449 Astrazeneca 12 Atkins (WS) 240 Aurelian Oil & Gas 334 Autonomy 76 Avanti Communications 324 Aveva 192 Avis Europe 326 Aviva 31 Avocet Mining 287 Axis-Shield 469 AZ Electronic Materials 199 Babcock International 117 Bae Systems 35 Bahamas Petroleum 397 Balfour Beatty 111 Barclays 16 Barr (AG) 289 Barratt Developments 197 BBA Aviation 209 Beazley 257 Bellway 216 Bellzone Mining 292 Berendsen 222 Berkeley 160 Betfair Group 202 BG Group 8 BHP Billiton 7 Big Yellow Group 308 Blinkx 344 Bodycote 259 Booker 213 Boot (Henry) 478 Borders & Southern Petroleum 378 Bovis Homes Group 268 Bowleven 220 BP 4 Brammer 351 Brewin Dolphin 319 British American Tobacco 9 British Land 61 British Sky Broadcasting 27 Britvic 210 Brown (N) 237 BT Group 28 BTG 235 Bunzl 107 Burberry 59 Bwin Party Digital Entertainment 223 Cable & Wireless Communications 181 Cable & Wireless Worldwide 158 Cairn Energy 49 Caledon Resources 380 Camellia 389 Cape 270 Capita 66 Capital & Counties Properties -

Real Estate & Construction Our Credentials

Real Estate & Construction Our credentials We are an international business communications consultancy Instinctif Partners combines teams across both capital markets strategic insight and a deep and corporate communications. understanding of the real estate We have extensive experience and construction sectors with an of advising clients that combines integrated approach spanning a deep understanding of the capital markets, corporate consumer and commercial drivers communications, crisis & affecting the sector, the changing reputation management, digital, legislative and policy landscape consumer, public policy and alongside the issues impacting business resilience. sentiment and regulating requirements in the City. We promote and protect the reputations of our clients and their Our integrated team is immersed brands, delivering communications in the sector, having led advice which supports strategic communications programmes needs. for a diverse range of national and international property and Our real estate and construction construction clients. These range team is unrivalled, boasting one of from FTSE listed companies to the largest and most experienced challenger brands and start-ups. Industry recognition CIPR Excellence PR Week Global Headlinemoney Awards 2018 PRCA City & Financial Awards 2017 & 2018 Awards 2017 Outstanding Large Public Awards 2016 & 2017 Relations Consultancy International Agency Thought Leadership of the Year of the Year City Agency of the Year Initiative of the Year We are Instinctif Partners Leading We work with -

Contents Introduction

Stock Market Research Platform November 2019 Could be a gem – selection Contents Introduction ............................................................................................................................ 2 ASA International Group Plc – ASAI -Asia & Africa Microfinance Bank - Could be a gem ................................................................................................................................................ 2 Clipper Logistics plc – CLG – hit alongside retail but it is e-fulfilment ............................... 4 Costain Group plc – COST – High pension risks .................................................................. 4 Forterra – FORT – depends on building market in the UK but looks good .......................... 5 Funding Circle PLC – FCH – interesting, trading at cash value but risky ............................ 6 Gem Diamonds Ltd – GEMD – interesting diamond market ................................................ 8 Georgia Capital Plc – CGEO – Interesting exposure to Georgia........................................... 8 Huntsworth plc – HNT – positive tailwinds, could be a gem, but insane............................ 12 Keller Group – KLR – Interesting business ......................................................................... 14 Menzies (John) plc – MNZS – ............................................................................................. 15 MJ Gleeson plc – GLE ......................................................................................................... 17 -

UK Annual Report 2015 (Including the Transparency Report)

Investing to become the Clear Choice UK Annual Report 2015 (including the Transparency Report) December 2015 KPMG.com/uk Highlights Strategic report Profit before tax and Revenue members’ profit shares £1,958m £383m (2014: £1,909m) (2014: £414m) +2.6% -7% 2013 2014 2015 2013 2014 2015 Average partner Total tax payable remuneration to HMRC £623k £786m (2014: £715K) (2014: £711m) -13% +11% 2013 2014 2015 2013 2014 2015 Contribution Our people UK employees KPMG LLP Annual Report 2015 Annual Report KPMG LLP 11,652 Audit Advisory Partners Tax 617 Community support Organisations supported Audit Tax Advisory Contribution Contribution Contribution £197m £151m £308m (2014: £181m) (2014: £129m) (2014: £324m) 1,049 +9% +17% –5% (2014: 878) © 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Strategic report Contents Strategic report 4 Chairman’s statement 10 Strategy 12 Our business model 16 Financial overview 18 Audit 22 Solutions 28 International Markets and Government 32 National Markets 36 People and resources 40 Corporate Responsibility 46 Our taxes paid and collected 47 Independent limited assurance report Governance 52 Our structure and governance 54 LLP governance 58 Activities of the Audit & Risk Committee in the year 59 Activities of the Nomination & Remuneration Committee in the year KPMG in the UK is one of 60 Activities of the Ethics Committee in the year 61 Quality and risk management the largest member firms 2015 Annual Report KPMG LLP 61 Risk, potential impact and mitigations of KPMG’s global network 63 Audit quality indicators 66 Statement by the Board of KPMG LLP providing Audit, Tax and on effectiveness of internal controls and independence Advisory services. -

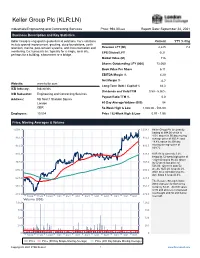

Keller Group Plc (KLR:LN)

Keller Group Plc (KLR:LN) Industrials/Engineering and Contracting Services Price: 994.00 GBX Report Date: September 24, 2021 Business Description and Key Statistics Keller Group is engaged in geotechnical solutions. Co.'s solutions Current YTY % Chg include ground improvement, grouting, deep foundations, earth retention, marine, post-tension systems, and instrumentation and Revenue LFY (M) 2,225 7.4 monitoring. Co.'s projects are typically for a single, local site, EPS Diluted LFY -0.21 perhaps for a building, a basement or a bridge. Market Value (M) 716 Shares Outstanding LFY (000) 72,060 Book Value Per Share 6.11 EBITDA Margin % 4.20 Net Margin % -0.7 Website: www.keller.com Long-Term Debt / Capital % 44.3 ICB Industry: Industrials Dividends and Yield TTM 0.59 - 5.96% ICB Subsector: Engineering and Contracting Services Payout Ratio TTM % 0.0 Address: 5th floor;1 Sheldon Square London 60-Day Average Volume (000) 54 GBR 52-Week High & Low 1,028.00 - 506.00 Employees: 10,554 Price / 52-Week High & Low 0.97 - 1.96 Price, Moving Averages & Volume 1,054.1 1,054.1 Keller Group Plc is currently trading at 994.00 which is 4.5% above its 50 day moving 982.3 982.3 average price of 950.84 and 19.8% above its 200 day 910.5 910.5 moving average price of 829.72. 838.8 838.8 KLR:LN is currently 3.3% below its 52-week high price of 1,028.00 and is 96.4% above 767.0 767.0 its 52-week low price of 506.00. -

The IMS Talent Challenge CEO Reward Analysis Contents

Acolyte Presents CEO REWARD & REMUNERATION IN THE CONSTRUCTION SECTOR Talent Insight Hub – Salary Benchmarking 2020 1.0 The IMS Talent Challenge CEO Reward Analysis Contents 1.0 PROJECT BACKGROUND 3 2.0 EXECUTIVE SUMMARY 5 3.0 APPROACH 8 4.0 CEO REWARDS IN THE UK CONSTRUCTION MARKET 10 5.0 CEO REWARDS IN THE GLOBAL CONSTRUCTION MARKET 15 6.0 CEO REWARDS IN SIMILAR SIZED COMPANIES 20 7.0 APPENDICES 25 6.1 Remuneration Data 26 6.2 UK Company Profiles 30 6.3 Global Company Profiles 41 6.4 Similar Sized Company Profiles 52 8.0 ABOUT ACOLYTE 63 1.0 Project Background CEO Reward Analysis Project Background PROJECT BACKGROUND With CEOs of the ten largest construction companies in the UK taking home circa £25m between them last year, how does their compensation compare to CEOs of globally leading construction companies and CEOs of similar sized firms in other sectors? The competitive nature of operating in the construction market can create an inflationary pressure on rewards paid to executives. There is a balancing act between aligning a company's success with their CEO’s remuneration (i.e. bonus, stock options etc.) and ensuring that the base salary is competitive enough to attract strong leadership talent. To address this challenge, this whitepaper examines the rewards paid to the CEOs of top ten UK construction companies in the context of both CEO rewards in the the top ten global construction firms and the remuneration earned by CEOs in ten companies of a similar scale across different sectors in the UK. -

HW&Co. Industry Reader Template

EUROPEAN UPDATE INDUSTRY UPDATE │ SUMMER 2015 www.harriswilliams.com www.harriswilliams.de Harris Williams & Co. Ltd is a private limited company incorporated under English law having its registered office at 5th Floor, 6 St. Andrew Street, London EC4A 3AE, UK, registered with the Registrar of Companies for England and Wales under company number 7078852. Directors: Mr. Christopher Williams, Mr. Ned Valentine, Mr. Paul Poggi and Mr. Thierry Monjauze, authorised and regulated by the Financial Conduct Authority. Harris Williams & Co. Ltd Niederlassung Frankfurt (German branch) is registered in the Commercial Register (Handelsregister) of the Local Court (Amtsgericht) of Frankfurt am Main, Germany, under registration number HRB 96687, having its business address at Bockenheimer Landstrasse 33-35, 60325 Frankfurt am Main, Germany. Permanent Representative (Ständiger Vertreter) of the Branch Niederlassung: Mr. Jeffery H. Perkins. EUROPEAN UPDATE INDUSTRY UPDATE │ SUMMER 2015 HARRIS WILLIAMS & CO. CONTACTS CONTENTS Thierry Monjauze Managing Director QUARTERLY QUICK READ 63 Brook Street London W1K 4HS United Kingdom EUROPEAN ECONOMIC CLIMATE Phone: +44 20 7518 8901 [email protected] EUROPEAN M&A ENVIRONMENT Red Norrie Managing Director EUROPEAN INBOUND M&A ENVIRONMENT 63 Brook Street London W1K 4HS United Kingdom AEROSPACE, DEFENCE & GOVERNMENT SERVICES Phone: +44 20 7518 8906 [email protected] BUSINESS SERVICES Jeffery Perkins Managing Director CONSUMER Bockenheimer Landstr. 33-35 60325 Frankfurt Germany ENERGY & POWER Phone: +49 69 3550638 00 [email protected] HEALTHCARE & LIFE SCIENCES LONDON OFFICE 63 Brook Street INDUSTRIALS London W1K 4HS United Kingdom Phone: +44 20 7518 8900 TECHNOLOGY, MEDIA & TELECOM FRANKFURT OFFICE Bockenheimer Landstrasse TRANSPORTATION & LOGISTICS 33-35 60325 Frankfurt am Main Germany FEATURED THEME Phone: +49 69 3650638 00 FEATURED THEME – MOMENTUM IN ACQUISITIONS BY STRATEGIC BUYERS1 . -

Morgan Sindall Group's Roadmap for Sustainability

16 DELIVERING TODAY FOR TOMORROW autumn 2011 Construction & Infrastructure Affordable Housing Fit Out Urban Regeneration DELIVERING TODAY FOR TOMORROW Investments In order to drive sustainability forward within the Morgan Sindall Group, we must give our Total Commitment to making it happen. Our Ynysowen Community Primary School – Roadmap for Sustainability An exemplar of sustainable design maps out targets, milestones A Focus On: and actions for each division and the Group as a whole TODAY is published by: to aim for. From this, six Key Commitments have Morgan Sindall Group plc Morgan Sindall Group plc is a been identified that will Kent House leading UK construction and Morgan Sindall steer us in the right direction. 14-17 Market Place regeneration group with a turnover So, whether it is helping London W1W 8AJ of £2 billion, employing over to reduce the energy and Tel: 020 7307 9200 7,000 people and operating in the waste from our offices and www.morgansindall.com public and commercial sectors. Group’s Roadmap sites, staying safe at work or email: [email protected] It operates through five divisions getting involved with local of construction and infrastructure, communities, each and affordable housing, fit out, urban every one of us has a part regeneration and investments. for Sustainability to play in helping us achieve our Total Commitment. 2 DELIVERING TODAY FOR TOMORROW IT’S ALL ABOUT SUSTAINABILITY 3 In the long term the only businesses that are going to succeed are those In this issue… that deliver sustainable solutions. Sustainability opens new market This issue of TODAY focuses on Morgan Sindall Total opportunities and so ultimately the Group’s new Roadmap for Sustainability. -

The Stonework Contractor Contemporary Traditional

The Stonework Contractor Contemporary Traditional 2 “They are easy and approachable to work with and have the ability to ‘think outside the box’ when challenges present themselves. I would most definitely work with Putney & Wood again should the opportunity present itself.” Mark Craig - Wates 3 10 Eastbourne Terrace, London W2 I Fletcher Priest I Wates Group Limited I 10 Portman Square, London W1 I Squire & Partners I BAM Construction Limited I 41 Lothbury, London EC2 I GMW Architects I Skanska UK Plc I 150 New Bond Street, London W1 I Sidell Gibson I Kier Construction I 311-318 High Holborn, London WC1 I Foster & Partners I Balfour Beatty Construction Limited I The Mansion, Courtenay Avenue, London N6 I Rolfe Judd I Como Group Limited I University of Portsmouth Library I Trehearne Architects I Mace Group Limited I 1-3 Kings Arms Yard, London EC2 I EPR Architects I VolkerFitzpatrick Limited I Kinnaid House, 1 Pall Mall, London W1 I BFLS Architects I Miller Group Limited I Thornwood Gardens, Kensington, London W8 I M R Partnership I Structure Tone UK I 30 Kings Street, London, EC2 I TTSP Architects I St James Group Limited I 16 Great Queen Street, London WC2 I HLM Architects I St George plc I 1 Grafton Street, London W1 I Rick Mather Architects I J Murphy & Sons Limited I 10 St Martins Courtyard, London WC2 I Burberry Limited I John F Hunt Limited I 1 Bartholomew Lane, London EC2 I DAKS Limited I Chorus Group Limited I 1 Angel Lane, London EC4 I Marks & Spencer plc I Faithdean plc I Woolwich Civic Centre, London SE18 I Tiffany & Co Limited